Finance

How Can I Get A Repo Off My Credit

Modified: February 21, 2024

Looking to improve your credit? Learn how to remove a repossession from your credit report and regain control of your finances.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

Introduction

Having a repossession on your credit report can be a daunting and stressful situation. It can negatively impact your credit score and make it challenging to secure loans or obtain favorable interest rates in the future. However, it’s important to remember that there are steps you can take to remove a repo from your credit and improve your financial standing.

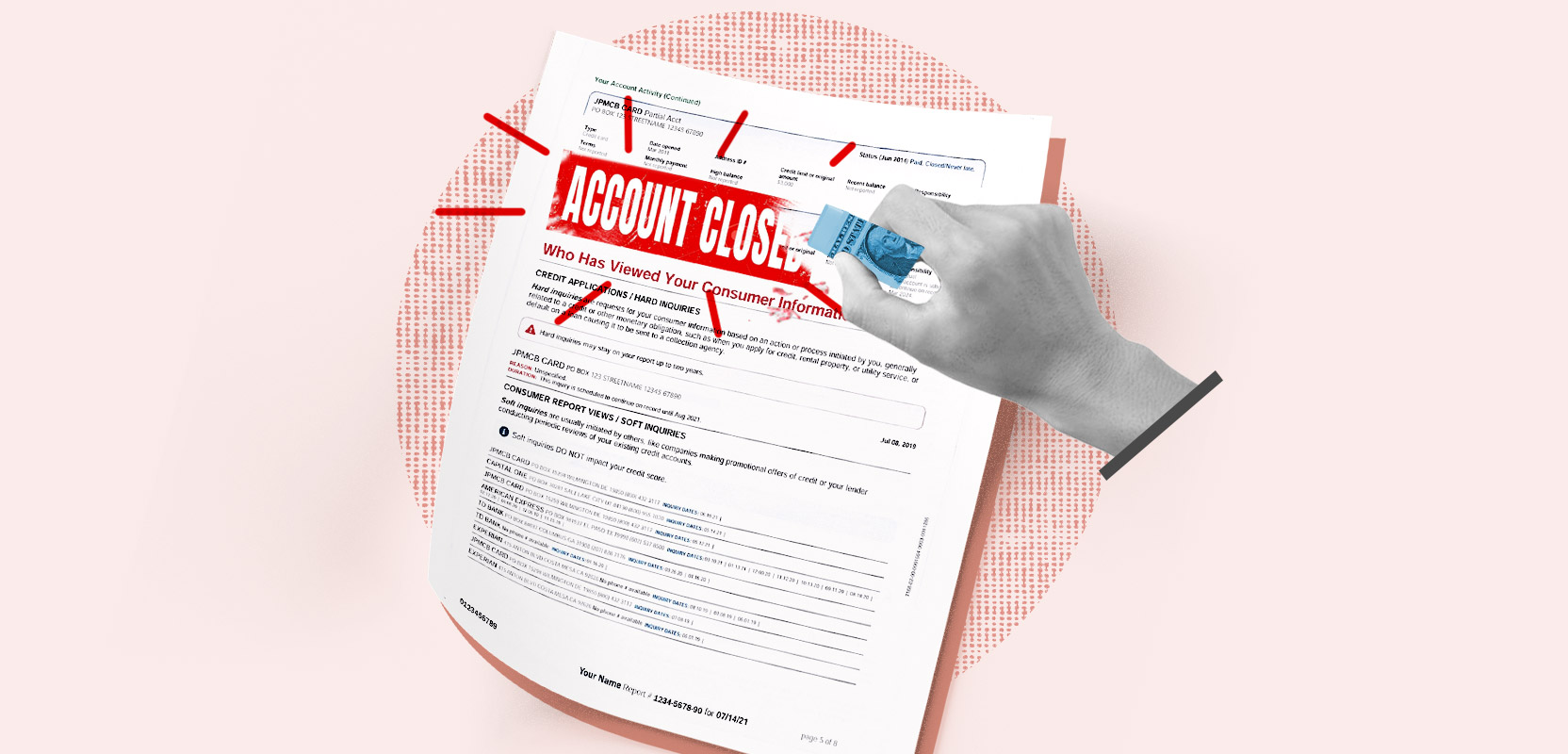

Before diving into the strategies to remove a repo from your credit, it’s essential to understand what a repo is and how it affects your credit score. In simple terms, a repo, short for repossession, occurs when you fail to make timely payments on an asset, such as a car or a boat, that was collateral for a loan. The lender then repossesses the asset as a means to recoup their losses.

Once a repo is reported to credit bureaus, it stays on your credit report for a significant period, typically up to seven years. During this time, it can have a significant impact on your credit score, making it more challenging to obtain credit or secure affordable loan terms. However, despite the negative impact, there are steps you can take to remove a repo from your credit report.

In this article, we will explore actionable strategies that can help you get a repo off your credit and improve your financial standing. It’s important to note that while these strategies have proven to be effective for many, there is no guarantee of success in every situation. Additionally, it may take time and determination to fully recover from a repo on your credit.

Now, let’s dive into the steps you can take to remove a repo from your credit and regain financial stability.

Understanding Credit Repos and their Impact

Before delving into the steps to remove a repo from your credit, it’s crucial to understand the impact repossession can have on your financial health. A credit repo, short for repossession, occurs when you fail to make timely payments on an asset that serves as collateral for a loan, such as a car, boat, or even furniture.

When you default on your loan, the lender has the right to repossess the asset to recover their losses. They then report the repossession to the credit bureaus, which significantly influences your credit standing. A repo can lower your credit score by a substantial amount and remains on your credit report for up to seven years.

The impact of a repo on your credit can be far-reaching. Here are some ways repossession can affect your financial standing:

- Negative Impact on Credit Score: A repo is considered a severe delinquency and can cause a significant drop in your credit score. This makes it difficult to obtain new credit or secure favorable loan terms in the future.

- Limited Access to Credit: With a repo on your credit report, lenders may perceive you as high-risk. As a result, obtaining credit cards, loans, or mortgages may be challenging, and if you are approved, you may be subject to higher interest rates.

- Higher Insurance Premiums: Insurance companies often use credit scores to determine premiums. A repo on your credit report can lead to higher insurance rates, affecting your overall financial well-being.

- Difficulty Renting or Leasing: Many landlords and leasing companies run credit checks on potential tenants. With a repo on your credit, you may face difficulties securing tenancy or favorable lease terms.

- Employment and Security Clearance Issues: Some employers and government agencies conduct credit checks, particularly for positions that involve financial responsibilities. A repo on your credit report may raise concerns about your financial stability and impact job prospects or security clearances.

Understanding the significant impact of repossession on your credit is crucial for taking the necessary steps to remove it and rebuild your financial standing. In the next section, we will discuss actionable strategies to help you remove a repo from your credit report and improve your creditworthiness.

Steps to Remove a Repo from Your Credit

While a repossession on your credit report can be disheartening, it’s important to remember that you have options to remove it and improve your credit standing. Here are six steps you can take to remove a repo from your credit:

- Review Your Credit Report: Start by obtaining a copy of your credit report from the major credit bureaus – Equifax, Experian, and TransUnion. Carefully review the report to ensure that all the information related to the repossession is accurate.

- Dispute Inaccurate Information: If you notice any errors or inaccuracies in the repo information on your credit report, gather supporting documentation and file a dispute with the credit bureau. They have 30 days to investigate your claim and remove the incorrect information if found to be valid.

- Negotiate with the Lender: Reach out to the lender who repossessed the asset and inquire about the possibility of negotiating a settlement. If you can come to an agreement, make sure to get the agreement in writing, including the terms of payment and the removal of the repo from your credit report once paid.

- Pay off the Remaining Balance: If you still owe a balance after the repossession, it’s crucial to pay it off as soon as possible. This demonstrates responsible financial behavior and can work in your favor when negotiating with the lender or requesting a removal of the repo from your credit report.

- Request a Deletion or Goodwill Adjustment: Contact the lender or collection agency and politely request that they remove the repossession from your credit report in exchange for full payment or goodwill. While there is no guarantee of success, some lenders may be willing to work with you, especially if you have a history of on-time payments or faced extenuating circumstances leading to the repossession.

- Seek Professional Assistance: If all else fails, consider seeking assistance from a reputable credit repair agency or a credit attorney who specializes in repossession removal. They can navigate the complex process on your behalf and increase your chances of success.

Remember, removing a repo from your credit report takes time, patience, and persistence. It’s essential to continue practicing responsible financial habits, such as making your payments on time and maintaining a low credit utilization ratio, to improve your credit score gradually.

Now that you have a clear understanding of the steps to remove a repo from your credit, it’s time to take action and regain your financial stability. In the next section, we will explore some additional tips and considerations to help you along the way.

Review Your Credit Report

The first step in the process of removing a repo from your credit is to review your credit report. You can request a copy of your credit report from the major credit bureaus – Equifax, Experian, and TransUnion. It’s important to obtain reports from all three bureaus since the information may vary between them.

When reviewing your credit report, pay close attention to any accounts or entries related to the repossession. Look for inaccuracies, such as incorrect dates, loan amounts, or even the presence of the repo itself. Discrepancies in your credit report could give you grounds for disputing the information and having it removed.

If you find any errors or inconsistencies, gather the necessary documentation to support your claim. This can include payment receipts, loan agreements, or any correspondence with the lender pertaining to the repossession. Having this evidence will be beneficial when filing a dispute with the credit bureaus or negotiating with the lender.

It’s also worth noting that under the Fair Credit Reporting Act (FCRA), consumers have the right to a free credit report from each credit bureau once every 12 months. Taking advantage of this benefit allows you to stay informed about your credit history and address any issues promptly.

Take the time to carefully review your credit report and make note of any errors or discrepancies. By doing so, you will have a solid foundation for the next steps in the process of removing a repo from your credit.

Dispute Inaccurate Information

After reviewing your credit report and identifying any inaccuracies related to the repossession, your next step is to dispute the information with the credit bureaus. Disputing inaccurate information is an essential part of the process to remove a repo from your credit.

To initiate a dispute, you need to send a formal letter to the credit bureaus outlining the errors and providing supporting documentation. The letter should clearly state the specific information being disputed, explain the reasons for the dispute, and include copies of any relevant documents or evidence.

When gathering evidence, be sure to include any documentation that proves the repo information is incorrect. This could include payment receipts, loan statements, or correspondence with the original lender. Providing a solid case with supporting evidence increases the likelihood of a successful dispute.

Once the credit bureaus receive your dispute letter, they are required by law to investigate the claim within 30 days. During this period, the credit bureau will contact the lender or collection agency responsible for reporting the repossession and request verification of the information.

If the lender fails to provide verification or if they are unable to validate the accuracy of the repo information, the credit bureaus must remove it from your credit report. In some cases, the entire account associated with the repossession may be deleted.

It’s crucial to monitor your credit report closely after filing a dispute to ensure that the inaccuracies are resolved. The credit bureaus will provide you with an updated copy of your credit report once the investigation is complete. Review the updated report and verify that the repo has been removed.

Disputing inaccurate information can be a powerful tool in removing repossession from your credit report. By taking the time to gather evidence and submit a formal dispute, you increase the chances of achieving a positive outcome and improving your credit standing.

Negotiate with the Lender

One of the proactive steps you can take to remove a repo from your credit report is to negotiate with the lender who repossessed the asset. By engaging in open and honest communication, you may be able to reach a settlement agreement that benefits both parties.

When negotiating with the lender, it’s essential to approach the conversation with a clear understanding of your financial situation and a willingness to find a resolution. Here are some key points to consider:

- Contact the Lender: Reach out to the lender who repossessed the asset and express your desire to resolve the situation. It’s important to establish open lines of communication and discuss potential solutions.

- Explain Your Circumstances: Provide an honest explanation of any extenuating circumstances that led to the repossession, such as a job loss or medical emergency. By sharing your situation, the lender may be more inclined to work with you to find a resolution.

- Propose a Settlement: Offer a reasonable settlement amount that you are able to pay in exchange for the removal of the repo from your credit report. Calculate a realistic amount that takes into account your financial capabilities.

- Get the Agreement in Writing: If the lender agrees to a settlement, make sure to obtain a written agreement outlining the terms. This includes the exact amount to be paid, the payment schedule, and the agreement to remove the repo from your credit report upon completion of the settlement.

- Follow Through on the Agreement: Once you have reached an agreement, it’s crucial to honor your commitment and make the agreed-upon payments on time. By fulfilling your end of the agreement, you demonstrate responsibility and increase the chances of the repo being removed from your credit report.

Keep in mind that negotiating with the lender is not always guaranteed to be successful. Some lenders may be more willing to negotiate than others, depending on their internal policies and the circumstances surrounding the repossession. However, it’s still worth exploring this option as it could lead to a favorable outcome.

Remember to be courteous, professional, and persistent throughout the negotiation process. By maintaining a cooperative and respectful approach, you increase the likelihood of finding a mutually beneficial solution.

Negotiating with the lender is another proactive step you can take to remove a repo from your credit report. By engaging in effective communication and proposing reasonable settlements, you increase your chances of resolving the repossession and improving your credit standing.

Pay off the Remaining Balance

If you still have an outstanding balance after the repo, it’s crucial to prioritize paying off that debt. Paying off the remaining balance demonstrates financial responsibility and can positively impact your credit standing.

Here are some important steps to consider when paying off the remaining balance:

- Assess Your Financial Situation: Take a close look at your current financial situation and determine how much you can reasonably allocate towards paying off the remaining balance. Consider your income, expenses, and other financial obligations to come up with a realistic repayment plan.

- Contact the Lender: Reach out to the lender who holds the remaining balance and discuss your intention to pay it off. Inquire about any possible arrangements or payment plans that can accommodate your financial circumstances.

- Negotiate Payment Terms: If necessary, negotiate with the lender to establish a payment plan that fits your budget. They may be willing to extend the repayment period or reduce the interest rate to make it more manageable for you.

- Make Timely Payments: Stick to the agreed-upon payment schedule and ensure that payments are made on time. Late or missed payments can further damage your credit, making it harder to remove the repo from your credit report.

- Track Payment Progress: Keep a record of your payments and monitor your progress in paying off the remaining balance. This will not only help you stay organized but also serve as evidence of your commitment to resolving the debt.

By paying off the remaining balance, you demonstrate to future lenders that you fulfill your financial obligations. This responsible behavior can help improve your creditworthiness over time.

If you’re struggling to pay off the balance in one lump sum, consider alternatives such as obtaining a personal loan or working with a credit counseling service that can help you consolidate your debts and create a feasible repayment plan.

Remember, paying off the remaining balance is an essential step in removing a repo from your credit report. By diligently making your payments, you can show creditors that you are committed to resolving your debts and improving your financial standing.

Request a Deletion or Goodwill Adjustment

While it may not always be successful, requesting a deletion or goodwill adjustment from the lender or collection agency can be another avenue to remove a repo from your credit report. A deletion or goodwill adjustment involves asking the creditor to remove the repossession from your credit history as a gesture of goodwill.

Here are some steps to follow when requesting a deletion or goodwill adjustment:

- Contact the Creditor: Reach out to the lender or collection agency responsible for reporting the repossession on your credit report. Explain your situation, apologize for any past delinquency, and express your desire to rebuild your credit.

- Provide Supporting Documentation: If you have made recent efforts to improve your financial situation, such as consistent on-time payments or completing a credit counseling program, include supporting documentation to strengthen your case. This can help demonstrate your current responsible financial behavior.

- Compose a Well-Crafted Letter: Write a formal letter explaining your request for a deletion or goodwill adjustment. Be sincere, clear, and concise in expressing your desire to have the repossession removed from your credit report. Emphasize any extenuating circumstances that led to the repossession and highlight your efforts to rectify the situation.

- Follow Up: If you don’t receive a response within a reasonable timeframe, follow up with the creditor to inquire about the status of your request. Persistence and regular communication can sometimes make a difference.

- Be Prepared for Possible Outcomes: It’s important to set realistic expectations. While some creditors may be willing to consider your request, others may decline. However, don’t let a denial discourage you. There are still other avenues you can explore to have the repossession removed from your credit report.

Remember, not all creditors will agree to a deletion or goodwill adjustment, as it is at their discretion. However, by respectfully making your case and providing supporting documentation, you may increase your chances of success.

Even if your request is denied, don’t lose hope. You can still focus on other strategies, such as improving your financial habits, making on-time payments, and reducing your overall debt. Over time, these positive changes can help offset the impact of the repossession on your credit report.

Requesting a deletion or goodwill adjustment can be a worthwhile step in your journey to remove a repo from your credit report. Stay persistent, keep your communication professional, and don’t be discouraged by setbacks along the way.

Seek Professional Assistance

If you’ve tried the previous steps to remove a repo from your credit without success, or if you feel overwhelmed by the process, seeking professional assistance can be a wise decision. Credit repair agencies and credit attorneys specialize in helping individuals navigate complex credit situations and can provide valuable guidance and support.

Here are a few reasons why seeking professional assistance may be beneficial:

- Expertise and Experience: Credit repair professionals have in-depth knowledge of credit laws, regulations, and strategies for improving credit. They can leverage their expertise and experience to formulate personalized solutions for your specific situation.

- Negotiation Skills: Professionals who specialize in credit repair often have established relationships with lenders and collection agencies. They can use their negotiation skills to advocate on your behalf and potentially reach a resolution that results in the removal of the repo from your credit report.

- Proven Strategies: Credit repair professionals are familiar with various strategies to remove negative items from credit reports. They can develop a customized plan to address the repossession, leveraging proven techniques that may yield positive results.

- Paperwork and Documentation: Credit repair involves submitting meticulous paperwork and documentation to support your case. Professionals can ensure that all necessary paperwork is prepared accurately and submitted in a timely manner, optimizing your chances of success.

- Time and Convenience: Repairing your credit can be a time-consuming process. By seeking professional assistance, you can save time and energy, allowing the experts to handle the complexities while you focus on other important aspects of your financial life.

When seeking professional assistance, it’s crucial to choose a reputable credit repair agency or credit attorney. Do thorough research, read reviews, and consider recommendations from trusted sources before making a decision. Verify the track record and credentials of the professionals you are considering to ensure they have the necessary expertise.

While professional assistance may come at a cost, it can be a worthwhile investment in your financial future. The guidance and expertise offered by credit repair professionals can help you navigate the challenges of removing a repo from your credit report efficiently and effectively.

Remember, seeking professional assistance is an option if you feel overwhelmed or have exhausted other avenues. A credit repair professional can provide the guidance and support needed to help you remove the repo from your credit report and improve your overall financial situation.

Conclusion

A repo on your credit report can have a significant impact on your financial standing. However, with determination and the right strategies, you can take steps to remove the repo and rebuild your credit.

In this article, we have explored various approaches to remove a repo from your credit report. It begins with reviewing your credit report for inaccuracies and disputing any errors. Negotiating with the lender to reach a settlement and paying off the remaining balance demonstrate responsible financial behavior.

Additionally, requesting a deletion or goodwill adjustment from the lender and seeking professional assistance are viable options to explore. Though success is not guaranteed, these steps can greatly improve your chances of removing the repo from your credit report.

Throughout the process, it is important to continue practicing good financial habits, such as making payments on time and keeping your credit utilization ratio low. Over time, these positive habits will contribute to the improvement of your credit score and financial well-being.

Remember, repairing your credit and removing a repo takes time and persistence. Do not get discouraged if you encounter setbacks along the way. Stay committed to the process and remain proactive in your efforts to improve your credit standing.

Lastly, it’s essential to educate yourself about credit, financial responsibility, and managing debt. By understanding the factors that influence your credit and implementing sound financial practices, you can prevent future repos and maintain a healthy credit profile.

Removing a repo from your credit report is a journey, but with the right strategies and mindset, you can overcome the challenges and achieve financial stability. Start taking action today and take control of your credit future.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance