Home>Finance>How Do Interest Rates Affect Retirement Planning

Finance

How Do Interest Rates Affect Retirement Planning

Published: January 22, 2024

Learn how the fluctuation of interest rates impacts retirement planning and get financial advice to navigate this crucial aspect of personal finance.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

Introduction

When it comes to retirement planning, there are numerous factors that need to be taken into consideration. One of the most critical factors is the impact of interest rates. Interest rates play a vital role in shaping the financial landscape and can significantly affect retirement savings in various ways.

Understanding how interest rates work and their implications on retirement planning is essential for anyone looking to secure a comfortable post-work life. This article will delve into the intricacies of interest rates and explore how they can impact retirement savings, fixed income investments, mortgage payments, and debt management.

Interest rates are determined by various factors, including government policies, inflation rates, and global economic conditions. They have a direct influence on borrowing costs and investment returns, which can significantly impact retirement planning.

Whether you are nearing retirement or have just started your savings journey, understanding the correlation between interest rates and your financial future is crucial. By exploring the intricacies of this relationship, you can make informed decisions and adapt your retirement strategy accordingly.

So, let’s dive into the world of interest rates and uncover the ways in which they can shape your retirement planning.

Understanding Interest Rates

Interest rates refer to the cost of borrowing money or the return on investment. They are expressed as a percentage and play a significant role in the overall economy. Understanding how interest rates work is crucial to grasp their implications on retirement planning.

Interest rates are influenced by several factors, including the monetary policies of central banks, inflation rates, and the supply and demand for credit. When central banks increase interest rates, borrowing becomes more expensive, which can impact mortgage payments, credit card debt, and other loans. On the other hand, when interest rates are low, borrowing costs decrease, allowing individuals to access credit at a more affordable rate.

When it comes to savings and investments, interest rates also have a direct impact. Higher interest rates generally result in higher returns on savings accounts, certificates of deposit (CDs), and other fixed income investments. However, lower interest rates can mean lower returns on these investments, potentially affecting the growth of retirement savings.

It’s important to note that interest rates can fluctuate over time. They are influenced by various economic factors and can be adjusted by central banks in response to economic conditions. For retirees or those close to retirement, understanding the current interest rate environment is vital for effective retirement planning.

Furthermore, interest rates can vary for different types of loans and investments. For example, mortgage rates are typically different from credit card interest rates or rates on personal loans. Each loan or investment product comes with its own set of terms and conditions, including the interest rate that will be applied.

To effectively navigate retirement planning, individuals must stay informed about the current interest rate environment, monitor any changes, and make adjustments to their financial strategies accordingly. By understanding interest rates and their implications, individuals can make educated decisions that align with their retirement goals.

The Impact of Interest Rates on Retirement Savings

Interest rates have a significant impact on retirement savings. The returns on investments and the growth of savings are influenced by the prevailing interest rate environment. Understanding this impact is crucial for effective retirement planning.

When interest rates are high, retirees and those nearing retirement may enjoy higher returns on their investments. Fixed income investments such as bonds, certificates of deposit (CDs), and savings accounts tend to offer more attractive yields when interest rates are higher. This can be beneficial for individuals who rely on these investments to generate income during their retirement years.

Conversely, when interest rates are low, the returns on fixed income investments may decrease. This can pose challenges for individuals relying heavily on interest income to fund their retirement. In such cases, retirees may need to explore alternative investment options or adjust their retirement budget to compensate for the lower interest income.

It’s important to note that interest rates also impact the compounding of savings over time. Higher interest rates can accelerate the growth of retirement savings, while lower interest rates may slow down the accumulation of wealth. This emphasizes the need for a proactive approach to retirement planning that considers the prevailing interest rate environment.

Furthermore, the impact of interest rates extends beyond investment returns. Mortgage rates, for example, can have a significant influence on retirement savings. When interest rates are lower, individuals may have the opportunity to refinance their mortgages and potentially reduce monthly payments. This can free up extra funds to allocate towards retirement savings or other financial goals. On the other hand, when interest rates are higher, refinancing may not provide the same level of benefit, and individuals may need to allocate more of their income towards mortgage payments, potentially limiting their ability to save for retirement.

Ultimately, the impact of interest rates on retirement savings highlights the importance of staying informed and adapting one’s retirement strategy accordingly. By monitoring interest rate trends, individuals can make adjustments to their investment portfolio, explore different savings vehicles, and anticipate the potential impact on their retirement goals.

Effect on Fixed Income Investments

Fixed income investments, such as bonds and certificates of deposit (CDs), are particularly sensitive to changes in interest rates. The interest rates prevailing in the market directly impact the returns and value of these investments, making it essential to understand how interest rates can affect fixed income investments in retirement planning.

When interest rates rise, the value of existing fixed income investments may decline. This is because newly issued bonds or CDs offer higher interest rates, making existing investments with lower rates less desirable. As a result, the value of previously purchased fixed income investments in the secondary market may decrease. However, if these investments are held until maturity, the principal amount will still be returned.

On the other hand, when interest rates fall, the value of existing fixed income investments may increase. Investors holding bonds or CDs with higher interest rates than the current market rates can benefit from the higher yield on their investments. This increased value can be advantageous for retirees who rely on fixed income investments for a stable source of income during retirement.

Additionally, the impact of interest rates on fixed income investments extends to the income generated. Higher interest rates translate to higher returns on these investments, providing retirees with more income to support their retirement expenses. Conversely, lower interest rates can result in lower income from fixed income investments, potentially impacting retirement income planning.

It is crucial to consider the potential risks associated with fixed income investments when interest rates fluctuate. When interest rates rise, the fixed income investments may face an increased risk of price depreciation, affecting the overall value of the investment portfolio. This risk can be managed by diversifying the fixed income portfolio across different types of bonds and maturities.

Retirement planning should involve a well-balanced and diversified investment strategy that takes into account the potential impact of interest rates on fixed income investments. By assessing the current interest rate environment and adjusting the allocation of fixed income investments accordingly, individuals can better position themselves to achieve their retirement goals.

Impact on Mortgage and Debt Payments

Interest rates not only affect savings and investments in retirement planning, but they also have a significant impact on mortgage and debt payments. The fluctuation in interest rates can directly influence the affordability and repayment structure of debts, which has important implications for retirees.

When interest rates increase, mortgage payments on adjustable-rate mortgages (ARMs) and other variable-rate loans can also increase. This means that retirees with such loans may experience higher mortgage payments, potentially affecting their monthly budget and ability to allocate funds towards other retirement expenses. It is essential for retirees to factor in potential increases in mortgage payments when planning their retirement budget.

On the other hand, when interest rates decrease, there may be an opportunity for retirees to refinance their mortgages at a lower rate. Refinancing can potentially reduce monthly mortgage payments, freeing up funds that can be redirected towards retirement savings or other financial goals. This can offer financial relief and increase cash flow during retirement.

In addition to mortgage payments, interest rates can affect other types of debts. For example, credit card interest rates are often tied to the prevailing interest rates. If interest rates rise, credit card debt can become more expensive to carry, potentially impacting retirees’ ability to manage and pay off their debts.

When it comes to retirement planning, managing debt becomes crucial to ensure financial stability. Retirees should consider prioritizing debt repayment and explore ways to reduce interest costs, such as consolidating high-interest debt into a lower interest loan.

Overall, interest rate fluctuations affect mortgage and debt payments, either by increasing or decreasing monthly obligations. This can significantly impact retirees’ cash flow, budgeting, and overall financial well-being in retirement. It is important for individuals in retirement planning to consider the potential impact of interest rates on their mortgage and debt payments, and make necessary adjustments to their financial strategy to ensure a sustainable and comfortable retirement.

Considerations for Retirement Planning

Retirement planning involves careful consideration of various factors, and interest rates are a crucial element to keep in mind. Here are some key considerations to take into account when planning for retirement in the context of interest rates:

- Timing: The timing of retirement can be influenced by interest rates. Higher interest rates may provide an opportunity to accumulate more savings before retiring, as investments can yield higher returns. Conversely, lower interest rates may necessitate an adjustment to retirement timelines to allow for potentially lower investment returns.

- Risk Tolerance: The impact of interest rates on investments and savings should be considered in relation to risk tolerance. Higher risk investments may offer the potential for higher returns, but they also come with increased volatility. Retirees with a lower risk tolerance may opt for more conservative investments to mitigate the impact of fluctuating interest rates.

- Diversification: A well-diversified investment portfolio can help manage the impact of interest rates on retirement savings. Diversification across different asset classes, such as stocks, bonds, and real estate, can help mitigate risks and capture opportunities in varying interest rate environments.

- Longevity: Interest rates can affect the longevity of retirement savings. Lower interest rates may result in slower growth of savings, potentially requiring retirees to adjust their spending habits or seek additional sources of income to support a longer retirement period.

- Inflation: It’s important to consider the impact of inflation alongside interest rates. Inflation erodes the purchasing power of retirement savings over time. Retirees must ensure that their investment returns and savings keep pace with inflation to maintain their desired lifestyle.

- Professional Advice: Given the complexity and ever-changing nature of interest rates and retirement planning, seeking guidance from a financial advisor can be invaluable. A professional can help assess individual circumstances, provide tailored advice, and offer strategies to navigate the impact of interest rates on retirement planning.

Understanding the considerations associated with interest rates in retirement planning is essential for ensuring financial security and achieving retirement goals. By evaluating these factors and making informed decisions, individuals can adapt their strategies to navigate the fluctuations in interest rates and build a solid foundation for a comfortable retirement.

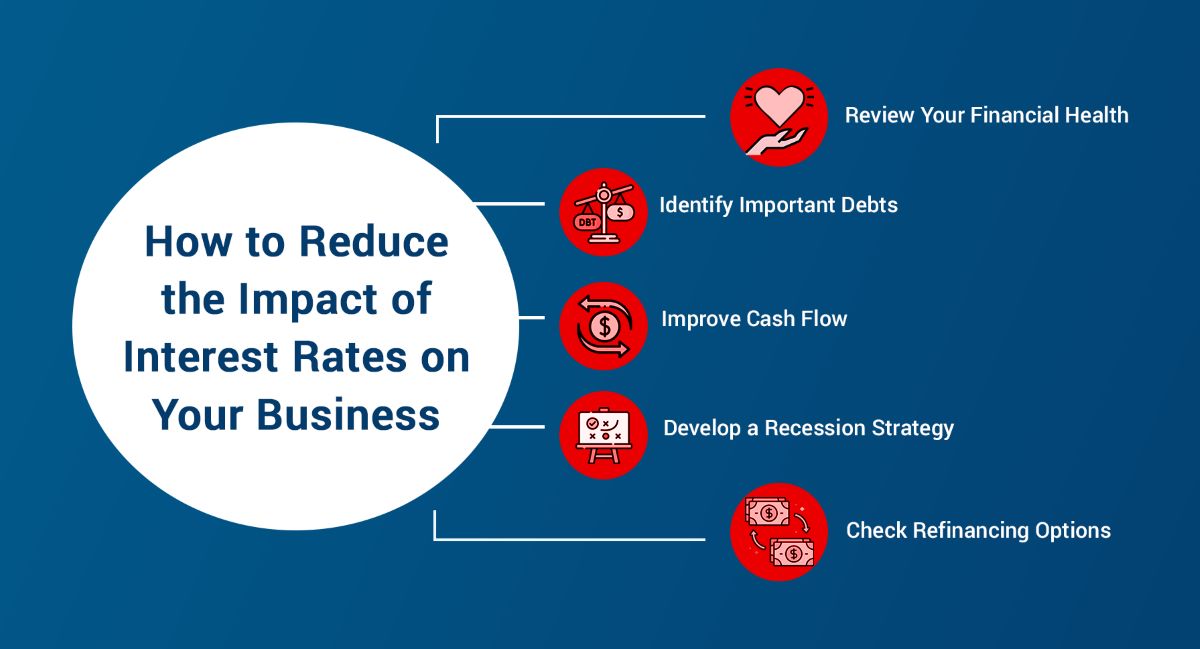

Strategies for Adapting to Changing Interest Rates

Adapting to changing interest rates is crucial for effective retirement planning. Here are some strategies to consider when facing fluctuating interest rate environments:

- Stay Informed: Stay updated on current interest rate trends and forecasts. Monitor changes in central bank policies and keep an eye on economic indicators that can impact interest rates. This knowledge will help inform your financial decisions and allow you to be proactive in adjusting your retirement plan.

- Review and Adjust Investments: Periodically review your investment portfolio in light of changing interest rates. Allocate investments across different asset classes to diversify risk. Consider adjusting the mix of investments based on the prevailing interest rates to optimize growth and income potential.

- Consider Bond Duration: When interest rates are expected to rise, consider shorter duration bonds that are less vulnerable to interest rate increases. On the other hand, when interest rates are expected to decline, longer duration bonds may provide higher yields. Evaluate your risk tolerance and investment objectives before making decisions regarding bond durations.

- Explore Fixed vs. Variable Rate Loans: If you have outstanding loans, such as a mortgage, evaluate whether a fixed-rate or variable-rate loan is more suitable. Fixed-rate loans provide stability in payments regardless of interest rate fluctuations, while variable-rate loans may offer lower initial rates but can increase over time.

- Consider Refinancing: When interest rates are low, explore the option of refinancing your mortgage or other debts to take advantage of lower rates. This can help reduce monthly payments and free up funds for retirement savings or other financial goals.

- Build an Emergency Fund: An emergency fund is crucial during periods of economic uncertainty or rising interest rates. Having readily available cash can help cover unexpected expenses, mitigate the need to dip into retirement savings, and maintain financial stability.

- Seek Professional Advice: Consulting with a financial advisor can provide valuable insights and guidance when navigating changing interest rates. They can help assess your individual situation, develop a tailored retirement plan, and provide recommendations on adjusting your strategy to align with shifting interest rate environments.

Remember, adapting to changing interest rates requires careful consideration and a flexible approach to retirement planning. By staying informed, reviewing and adjusting investments, analyzing loan options, and seeking professional advice, you can optimize your retirement strategy and effectively navigate the impact of changing interest rates.

Conclusion

Understanding the impact of interest rates is essential for successful retirement planning. Interest rates play a significant role in shaping the financial landscape and can have a profound influence on retirement savings, fixed income investments, mortgage payments, and overall financial stability.

Throughout this article, we have explored the various ways in which interest rates can affect retirement planning. We have discussed how interest rates impact investment returns and the compounding of savings, as well as the potential effects on mortgage and debt payments. Additionally, we have highlighted important considerations and strategies to adapt to changing interest rate environments.

It is crucial for individuals to stay informed about current interest rate trends, understand the relationship between interest rates and their financial goals, and make necessary adjustments to their retirement strategy. Considerations such as timing, risk tolerance, diversification, inflation, and professional advice should be taken into account when planning for retirement.

Rather than viewing interest rates as an obstacle, it is important to approach them as a factor to be actively considered and navigated. By evaluating the impact of interest rates on savings, investments, and debt, individuals can make informed decisions and adjust their retirement strategies accordingly.

In conclusion, a well-informed and proactive approach to retirement planning, taking into account the impact of interest rates, can help individuals achieve their desired retirement lifestyle and financial security. By staying attuned to interest rate fluctuations and implementing appropriate strategies, individuals can navigate the ever-changing financial landscape and enjoy a comfortable retirement.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance