Home>Finance>How Does Debt Consolidation Affect Credit Score

Finance

How Does Debt Consolidation Affect Credit Score

Published: March 6, 2024

Learn how debt consolidation can impact your credit score and improve your financial standing. Discover the effects of debt consolidation on your overall financial health and creditworthiness. Gain insights into managing your finances better with debt consolidation.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

Introduction

Debt consolidation is a financial strategy that many individuals consider when they find themselves struggling to manage multiple debts. It involves combining various high-interest debts into a single, more manageable loan or payment plan. This approach can potentially simplify the repayment process and reduce the overall interest burden. However, it's crucial to understand how debt consolidation can impact your credit score before deciding whether it's the right solution for your financial situation.

When exploring the relationship between debt consolidation and credit scores, it's essential to consider various factors that could influence the outcome. By delving into the mechanics of debt consolidation and its potential effects on credit scores, individuals can make informed decisions about their financial well-being. Understanding the nuances of this process empowers individuals to take proactive steps toward achieving financial stability and improving their creditworthiness.

In the following sections, we will explore the concept of debt consolidation, its potential impact on credit scores, and the essential factors to consider before pursuing this financial strategy. Additionally, we will provide practical tips for using debt consolidation wisely and discuss the broader implications of this approach. By gaining a comprehensive understanding of debt consolidation and its relationship to credit scores, readers will be better equipped to navigate their financial journeys with confidence and clarity.

What is Debt Consolidation?

Debt consolidation is a financial technique that involves combining multiple debts into a single, more manageable form of repayment. This can be achieved through various methods, such as taking out a consolidation loan, using a balance transfer credit card, or enrolling in a debt management program. The primary goal of debt consolidation is to streamline the repayment process and potentially reduce the overall interest burden, making it easier for individuals to regain control of their finances.

One common approach to debt consolidation is obtaining a consolidation loan, which allows individuals to pay off their existing debts and then make a single monthly payment toward the new loan. This simplifies the repayment process by consolidating multiple debts into one, potentially at a lower interest rate. Another method involves utilizing a balance transfer credit card, which allows individuals to transfer high-interest credit card balances to a card with a lower or zero percent introductory interest rate, providing temporary relief from accruing additional interest.

Debt management programs offered by credit counseling agencies also provide a structured approach to debt consolidation. These programs involve working with a credit counselor to negotiate with creditors for lower interest rates or more favorable repayment terms, consolidating multiple debts into a single monthly payment. While debt consolidation can offer immediate relief and simplify the repayment process, it’s essential to carefully consider the potential impact on credit scores and overall financial well-being.

By consolidating debts, individuals may benefit from a more organized and structured approach to repayment, potentially reducing the risk of missed payments and late fees. However, it’s important to assess the terms and conditions of the consolidation method chosen, as well as the long-term implications for financial health and creditworthiness. Understanding the various options for debt consolidation and their potential impact on credit scores is crucial for making informed decisions about managing and reducing debt.

How Debt Consolidation Can Affect Your Credit Score

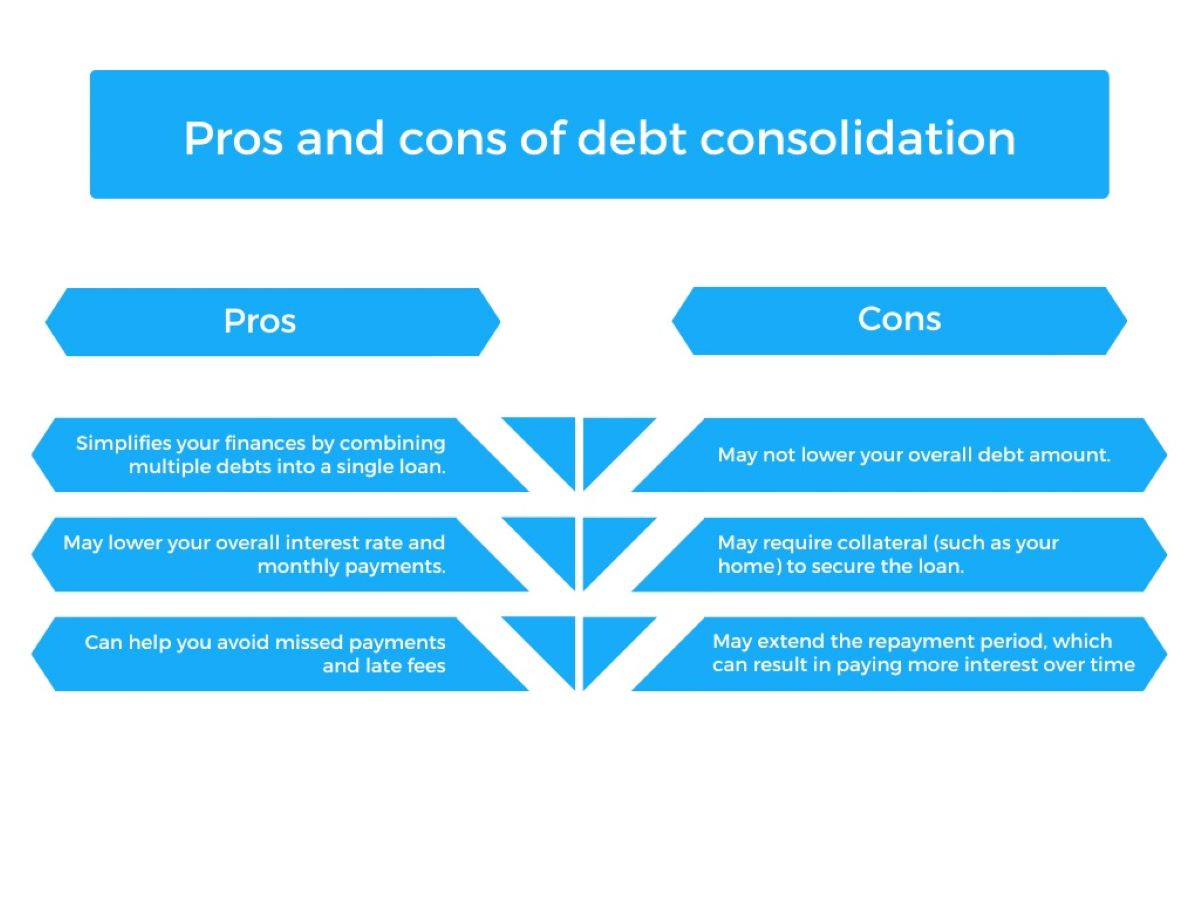

Debt consolidation can have both positive and negative effects on an individual’s credit score, depending on how the process is managed and the specific consolidation method chosen. Understanding these potential effects is crucial for individuals considering debt consolidation as a means of improving their financial situation.

One potential positive impact of debt consolidation on credit scores is the ability to simplify the repayment process, which can reduce the likelihood of missed or late payments. By consolidating multiple debts into a single, more manageable form of repayment, individuals may find it easier to stay on top of their financial obligations, potentially leading to a more consistent payment history. A history of on-time payments is a significant factor in determining credit scores, and debt consolidation can provide a structured approach to meeting repayment deadlines.

However, it’s essential to approach debt consolidation with caution, as certain methods can also have negative implications for credit scores. For example, applying for a new consolidation loan or balance transfer credit card may result in a hard inquiry on the individual’s credit report, which can temporarily lower their credit score. Additionally, closing existing credit accounts after consolidating their balances can affect the individual’s credit utilization ratio, which compares the amount of credit used to the total available credit. A higher credit utilization ratio can negatively impact credit scores.

Furthermore, if individuals fail to make timely payments on their new consolidation loan or credit card, their credit scores could suffer as a result of the negative payment history. It’s crucial for individuals considering debt consolidation to carefully assess their ability to meet the new repayment obligations and to choose a method that aligns with their financial capabilities and goals.

Overall, debt consolidation can impact credit scores in various ways, and the specific outcomes depend on how the process is managed and the individual’s financial behavior following consolidation. By weighing the potential benefits and drawbacks of debt consolidation, individuals can make informed decisions that support their overall financial well-being and creditworthiness.

Factors to Consider Before Using Debt Consolidation

Before pursuing debt consolidation as a solution for managing overwhelming debt, individuals should carefully evaluate several key factors to determine if this approach aligns with their financial goals and circumstances.

- Financial Discipline: Assessing one’s financial discipline and spending habits is crucial before opting for debt consolidation. Without addressing the root causes of debt accumulation, individuals may find themselves in a cycle of recurring debt even after consolidation.

- Interest Rates: Comparing the interest rates of current debts with those offered through consolidation is essential. If the new interest rate is significantly lower, it can lead to savings on interest payments over time. However, individuals should be wary of introductory rates that may increase after a certain period.

- Impact on Credit Score: Understanding the potential impact of debt consolidation on credit scores is vital. While consolidation can streamline repayment, it may also involve a hard inquiry and changes to credit utilization, which can affect credit scores in the short term.

- Repayment Terms: Evaluating the repayment terms of the consolidation loan or program is crucial. Individuals should consider the monthly payment amount, the total interest paid over the life of the loan, and any potential penalties for early repayment.

- Long-Term Financial Goals: Considering long-term financial goals is essential. Debt consolidation should align with an individual’s broader financial objectives, such as saving for retirement, purchasing a home, or investing in higher education.

By carefully considering these factors, individuals can make informed decisions about whether debt consolidation is the right strategy for their unique financial circumstances. It’s important to approach debt consolidation with a clear understanding of its potential benefits and drawbacks, as well as a realistic assessment of one’s ability to manage the new repayment obligations effectively.

Tips for Using Debt Consolidation Wisely

When considering debt consolidation as a means of managing and reducing debt, individuals can benefit from implementing the following tips to ensure they use this financial strategy wisely:

- Understand the Total Cost: Before committing to a debt consolidation loan or program, individuals should carefully assess the total cost of the new arrangement, including interest charges, origination fees, and any other associated costs. Understanding the overall expense can help individuals make informed decisions about the feasibility of consolidation.

- Compare Lenders and Programs: It’s essential to explore multiple lenders and consolidation programs to find the most favorable terms and interest rates. Comparing offers from different sources can help individuals secure the best option for their financial needs.

- Create a Repayment Plan: Developing a structured repayment plan is crucial for effectively managing consolidated debt. By establishing a budget and payment schedule, individuals can ensure that they meet their repayment obligations consistently.

- Avoid Accumulating New Debt: After consolidating existing debts, individuals should strive to avoid accumulating new debt. Responsible financial behavior, such as limiting credit card usage and adhering to a budget, can prevent the reemergence of financial challenges.

- Seek Financial Guidance: Consulting with financial advisors or credit counselors can provide valuable insights into the best debt consolidation options and strategies for long-term financial stability. Professional guidance can help individuals navigate the complexities of debt consolidation effectively.

By following these tips, individuals can maximize the benefits of debt consolidation while mitigating potential risks. It’s essential to approach the process with careful consideration and a proactive approach to financial management.

Conclusion

Debt consolidation can be a valuable tool for individuals seeking to regain control of their finances and manage overwhelming debt. By consolidating multiple debts into a single, more manageable form of repayment, individuals can potentially streamline the process and reduce the overall interest burden. However, it’s crucial to approach debt consolidation with a thorough understanding of its potential impact on credit scores and overall financial well-being.

Before pursuing debt consolidation, individuals should carefully consider various factors, including their financial discipline, the impact on credit scores, and the long-term implications for their financial goals. By weighing these considerations, individuals can make informed decisions about whether debt consolidation aligns with their unique circumstances and objectives.

Furthermore, using debt consolidation wisely requires a proactive approach to financial management. By understanding the total cost, comparing lenders and programs, and creating a structured repayment plan, individuals can maximize the benefits of consolidation while avoiding potential pitfalls. Seeking professional financial guidance can also provide valuable support in navigating the complexities of debt consolidation.

In conclusion, debt consolidation can serve as a valuable tool for individuals striving to achieve financial stability and reduce the burden of debt. By approaching the process with careful consideration, proactive financial management, and a realistic assessment of one’s financial capabilities, individuals can leverage debt consolidation to pave the way toward a more secure financial future.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance