Finance

How To Calculate Income Tax Expense Accounting

Published: November 2, 2023

Learn how to calculate income tax expense in accounting and ensure accurate financial reporting. Enhance your understanding of finance with our step-by-step guide.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

- Introduction

- Basics of Income Tax Expense Accounting

- Understanding Taxable Income

- Determining Tax Rate

- Calculating Income Tax Expense

- Recognizing Deferred Tax Assets and Liabilities

- Accounting Treatment for Income Tax Expense

- Recording Income Tax Expense in Financial Statements

- Disclosure Requirements for Income Tax Expense

- Conclusion

Introduction

Welcome to the world of income tax expense accounting, where businesses and individuals navigate the complex realm of taxation. Income tax expense accounting is a crucial aspect of financial management, as it ensures compliance with tax regulations and provides insights into a company’s financial performance. In this article, we will explore the basics of income tax expense accounting, including how to calculate income tax expense and the accounting treatment for it.

Income tax expense refers to the amount a company or individual is required to pay to the government based on their taxable income. It is an unavoidable cost that affects a company’s profitability and cash flow. Properly accounting for income tax expense is essential for accurate financial reporting and providing transparency to stakeholders.

Throughout this article, we will delve into the key concepts of income tax expense accounting, including understanding taxable income, determining tax rates, calculating income tax expense, and addressing deferred tax assets and liabilities. We will also explore the appropriate accounting treatment for income tax expense and the disclosure requirements for financial statements.

It is crucial to note that income tax laws and regulations vary between jurisdictions, and professionals in finance and accounting must stay up-to-date with the latest changes. This article provides a general overview of income tax expense accounting principles, but it is always recommended to consult with tax professionals and refer to the specific regulations in your jurisdiction.

Now, let’s dive into the fascinating world of income tax expense accounting and uncover the ins and outs of this crucial aspect of financial management.

Basics of Income Tax Expense Accounting

Income tax expense accounting involves the process of recognizing and recording the amount of tax a company or individual owes to the government based on their taxable income. To understand how income tax expense accounting works, let’s explore the key elements involved:

- Taxable Income: Taxable income is the amount of income that is subject to taxation. It is derived by subtracting allowable deductions from total income. Deductions may include expenses incurred in the course of business, such as salaries, rent, and supplies. Calculating taxable income accurately is crucial, as it forms the basis for determining the amount of income tax expense.

- Tax Rates: Tax rates vary depending on the jurisdiction and the level of income. Governments typically use progressive tax brackets, where higher income earners are taxed at a higher rate. Understanding the applicable tax rates is vital for accurate calculation of income tax expense.

- Income Tax Expense Calculation: Once the taxable income and tax rates are determined, the next step is to calculate the income tax expense. This involves multiplying the taxable income by the applicable tax rate to arrive at the amount of tax owed to the government.

- Deferred Tax Assets and Liabilities: In some cases, there may be differences between taxable income and financial income. These differences can arise due to timing or valuation discrepancies. Deferred tax assets and liabilities are created to account for these differences. Deferred tax assets represent potential future tax benefits, while deferred tax liabilities represent future tax obligations.

Proper accounting for income tax expense is essential for accurate financial reporting. It ensures that a company’s financial statements reflect the true tax obligations and provides transparency to stakeholders. Income tax expense is typically recognized in the income statement as an expense and may also be disclosed in the footnotes of the financial statements.

By understanding the basics of income tax expense accounting, businesses and individuals can navigate the intricacies of taxation and ensure compliance with tax regulations. It is crucial to seek guidance from tax professionals and stay updated on the latest tax laws to accurately account for income tax expense and optimize tax planning strategies.

Understanding Taxable Income

Taxable income is a key concept in income tax expense accounting. It is the amount of income that is subject to taxation after allowable deductions have been subtracted. Understanding how taxable income is determined is essential for accurate calculation of income tax expense. Let’s explore the factors that affect taxable income:

- Total Income: Total income includes all sources of income earned by an individual or generated by a business. This can include salaries, wages, rental income, capital gains, and dividends, among others. It is important to accurately identify and account for all sources of income to determine the initial figure for taxable income.

- Allowable Deductions: Allowable deductions are expenses that can be subtracted from total income to arrive at taxable income. These deductions are often related to business expenses, such as salaries, rent, supplies, and marketing expenses. Deductions may also include personal expenses, such as mortgage interest or charitable contributions, depending on the jurisdiction. It is crucial to understand the specific deductions allowed by the tax laws in your jurisdiction and ensure proper documentation and substantiation.

- Tax Exemptions and Credits: Tax exemptions and credits can further reduce taxable income. Exemptions are specific types of income that are not subject to taxation, such as certain government benefits or income earned in tax-free zones. Tax credits, on the other hand, directly reduce the amount of tax owed, providing a dollar-for-dollar reduction in the tax liability. Examples of tax credits include child tax credits, education credits, and renewable energy credits.

- Tax Planning Strategies: Effective tax planning strategies can also impact taxable income. By utilizing legal methods such as deferring income or accelerating deductions, businesses and individuals can minimize their taxable income and reduce their overall tax liability. Tax planning should always be done in accordance with applicable laws and regulations and with the guidance of tax professionals.

Understanding taxable income is crucial for accurate calculation of income tax expense. By properly identifying and documenting income sources, deducting allowable expenses, and taking advantage of exemptions and credits, businesses and individuals can optimize their tax positions and ensure compliance with tax laws. It is crucial to stay updated on changes in tax regulations and consult with tax professionals to navigate the complexities of determining taxable income and accurately account for income tax expense.

Determining Tax Rate

Determining the tax rate is a critical step in calculating income tax expense. The tax rate varies depending on the jurisdiction and the level of income. Understanding how tax rates are determined is essential for accurate calculation of income tax expense. Let’s explore the factors involved in determining the tax rate:

- Progressive Tax System: Many jurisdictions employ a progressive tax system, where tax rates increase as income levels rise. This means that higher-income earners are subject to higher tax rates. The progressive tax system aims to achieve a fair distribution of the tax burden, with individuals and businesses paying taxes proportionate to their ability to pay.

- Tax Brackets: Tax rates are typically structured in brackets, with each bracket corresponding to a specific range of income. As income increases and surpasses the threshold of a specific bracket, the higher tax rate of that bracket is applied to the excess income. For example, the first bracket may have a lower tax rate applied to income up to a certain threshold, while the second bracket has a higher tax rate applied to income above that threshold.

- Tax Laws and Regulations: The tax laws and regulations of a jurisdiction dictate the specific tax rates that apply. These laws are enacted by the government and can be subject to changes over time. It is crucial to stay updated on the latest tax legislation to accurately determine the applicable tax rates.

- Tax Planning Considerations: When planning for income taxes, businesses and individuals may consider various strategies to optimize their tax position. This may involve taking advantage of deductions, exemptions, and credits to lower taxable income and reduce the overall tax liability. Tax planning should always be conducted ethically and in compliance with tax laws and regulations.

To determine the appropriate tax rate, individuals and businesses must identify the applicable tax brackets based on their level of income. By multiplying the taxable income by the corresponding tax rate for each bracket and summing up the results, they can calculate the total income tax expense. It is important to ensure accuracy in applying the correct tax rates to avoid underpayment or overpayment of taxes.

Consulting with tax professionals and staying informed about tax legislation and regulations is crucial for effectively determining the tax rate and accurately calculating income tax expense. By understanding the factors involved in determining tax rates, businesses and individuals can meet their tax obligations while optimizing their overall tax position.

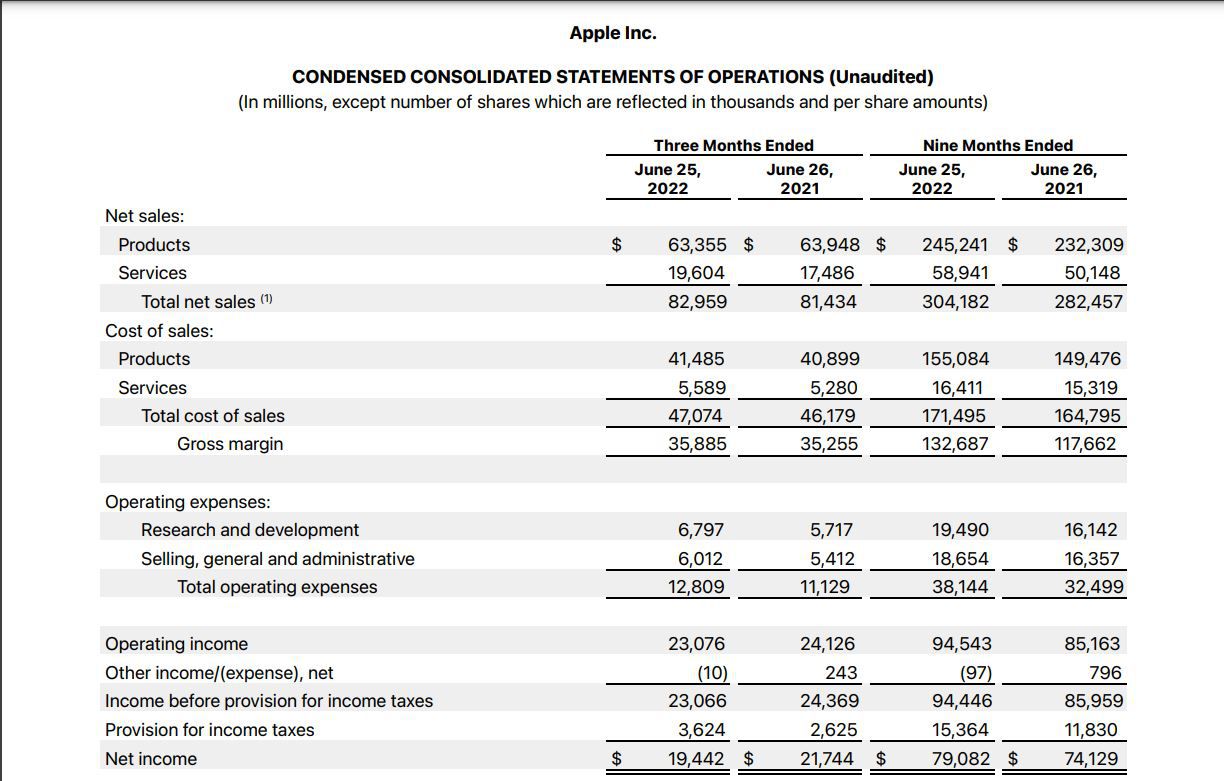

Calculating Income Tax Expense

Calculating income tax expense is a crucial step in income tax expense accounting. It involves determining the amount of tax a company or individual owes to the government based on their taxable income. Understanding the process of calculating income tax expense is essential for accurate financial reporting. Let’s explore the steps involved:

- Determine Taxable Income: The first step in calculating income tax expense is to determine the taxable income. This is done by subtracting allowable deductions from total income. Through proper documentation and accounting practices, businesses and individuals can identify all sources of income and the deductions allowed by the tax laws in their respective jurisdictions.

- Identify Applicable Tax Rates: The next step is to identify the applicable tax rates. Tax rates can vary based on the jurisdiction and the level of income. Progressive tax systems are commonly used, where tax rates increase as income levels rise. By understanding the tax brackets and rates that apply, businesses and individuals can accurately calculate their income tax expense.

- Apply Tax Rates: Once the taxable income and applicable tax rates are determined, the next step is to apply the tax rates to the taxable income. This involves multiplying the taxable income by the respective tax rate for each tax bracket. The resulting amounts are then summed up to calculate the total income tax expense.

- Consider Deductions, Exemptions, and Credits: Deductions, exemptions, and credits can further impact the calculation of income tax expense. By taking advantage of eligible deductions, exemptions, and credits, businesses and individuals can reduce their taxable income and, subsequently, their income tax expense. It is crucial to accurately calculate and document these deductions, exemptions, and credits to ensure compliance with tax laws.

It is important to note that calculating income tax expense can be complex, especially in cases where there are multiple sources of income, international operations, or specific tax regulations applicable to certain industries. In such cases, seeking guidance from tax professionals is highly recommended to ensure accurate calculations and compliance with tax laws.

By accurately calculating income tax expense, businesses and individuals can reflect their tax obligations in their financial statements. This provides transparency to stakeholders and enables informed decision-making. It also ensures compliance with tax laws and regulations, mitigating the risk of penalties or legal issues.

Proper documentation, adherence to tax regulations, and consultation with tax professionals are key to accurately calculating income tax expense and optimizing the tax position of businesses and individuals.

Recognizing Deferred Tax Assets and Liabilities

In the realm of income tax expense accounting, recognizing deferred tax assets and liabilities is an important aspect. These assets and liabilities are created to account for differences between taxable income and financial income that may have future tax implications. Let’s explore what deferred tax assets and liabilities are and how they are recognized:

- Deferred Tax Assets: Deferred tax assets arise when taxable income is lower than financial income. This may occur due to temporary differences between when revenues and expenses are recognized for tax purposes versus financial reporting purposes. Deferred tax assets represent potential future tax benefits that can be utilized to offset future tax liabilities. These benefits may arise from deductible temporary differences, such as tax losses carried forward, unused tax credits, or future deductions that will reduce taxable income.

- Deferred Tax Liabilities: On the other hand, deferred tax liabilities are created when taxable income is higher than financial income. This may result from temporary differences that will reverse in the future, generating tax obligations. Deferred tax liabilities represent future tax obligations that will be incurred when these temporary differences reverse. These obligations may arise from taxable temporary differences, such as accelerated depreciation for tax purposes or revenue recognition that is deferred for financial reporting purposes.

- Recognition and Measurement: The recognition and measurement of deferred tax assets and liabilities follow accounting standards such as the Generally Accepted Accounting Principles (GAAP) or the International Financial Reporting Standards (IFRS). These standards require businesses to assess the likelihood of realizing the future benefits associated with deferred tax assets. If it is more likely than not that the benefits will be realized, the deferred tax assets are recognized and measured at their estimated values.

- Impact on Financial Statements: Deferred tax assets and liabilities have implications for financial statements. They are recorded on the balance sheet as non-current assets or liabilities. Changes in their values are recognized in the income statement as deferred tax expense or income. The recognition and measurement of deferred tax assets and liabilities require professional judgment and consideration of future expectations and tax planning strategies.

Recognizing deferred tax assets and liabilities is essential for accurately reflecting the future tax implications of temporary differences between taxable income and financial income. Proper recognition ensures that financial statements present a comprehensive and transparent picture of a company’s tax position and financial standing.

It is important to note that the recognition and measurement of deferred tax assets and liabilities can be complex, requiring expertise and an understanding of tax laws and accounting standards. Consulting with tax professionals and adhering to applicable accounting standards are crucial for accurate recognition and measurement of deferred tax assets and liabilities.

By recognizing and appropriately accounting for deferred tax assets and liabilities, businesses can ensure compliance with accounting standards, provide transparency to stakeholders, and optimize their tax planning strategies.

Accounting Treatment for Income Tax Expense

The accounting treatment for income tax expense is an essential aspect of income tax expense accounting. It involves the proper recognition, measurement, and reporting of income tax expense in financial statements. Let’s explore the key considerations in the accounting treatment for income tax expense:

- Accrual Basis Accounting: Income tax expense is recognized on an accrual basis, meaning that it is recorded in the period to which it relates rather than when the tax payment is made. This ensures that income tax expense is matched with the corresponding revenues and expenses in the financial statements, providing a more accurate representation of a company’s financial performance.

- Income Statement Presentation: Income tax expense is typically presented as a separate line item in the income statement. It is shown as an expense, reflecting the amount of tax owed based on the taxable income for the period. By highlighting income tax expense separately, financial statements provide transparency and enable stakeholders to assess the impact of taxes on a company’s profitability.

- Deferred Tax Assets and Liabilities: Deferred tax assets and liabilities, as discussed previously, are also accounted for in the balance sheet. Deferred tax assets are classified as non-current assets, while deferred tax liabilities are classified as non-current liabilities. The recognition, measurement, and changes in the values of these assets and liabilities are reported in the income statement as deferred tax expense or income.

- Valuation Allowance: When it is uncertain whether some or all of the benefits of deferred tax assets will be realized, a valuation allowance is created to reduce the carrying amount of the deferred tax assets. This allowance is based on management’s judgment and the likelihood of realizing the future tax benefits. Changes in the valuation allowance are recorded as an adjustment to deferred tax expense.

It is important to note that the accounting treatment for income tax expense is governed by accounting standards such as the Generally Accepted Accounting Principles (GAAP) or the International Financial Reporting Standards (IFRS). These standards provide the framework for accurately recognizing, measuring, and reporting income tax expense in financial statements.

Proper accounting for income tax expense ensures compliance with accounting standards, transparency in financial reporting, and provides stakeholders with valuable information about a company’s tax position and financial performance. It is essential to consult with tax professionals and adhere to the relevant accounting standards to ensure accurate accounting treatment for income tax expense.

Recording Income Tax Expense in Financial Statements

Recording income tax expense in financial statements is a crucial step in accurately reflecting a company’s tax obligations and financial performance. It involves the proper presentation and disclosure of income tax expense in financial statements to provide transparency to stakeholders. Let’s explore the key considerations in recording income tax expense:

- Income Statement Presentation: Income tax expense is typically presented as a separate line item in the income statement, reflecting the amount of tax owed based on the taxable income for the period. This allows stakeholders to understand the impact of taxes on a company’s profitability and assess its financial performance.

- Accrual Basis Accounting: Income tax expense is recorded on an accrual basis, matching it with the corresponding revenues and expenses in the financial statements. This ensures that income tax expense is recognized in the period to which it relates, providing a more accurate representation of the company’s financial performance.

- Disclosure in Footnotes: In addition to reporting income tax expense in the income statement, companies are required to provide additional disclosure in the footnotes of financial statements. This disclosure may include details about the significant components of income tax expense, changes in tax rates, the impact of tax planning strategies, and any uncertainties or risks related to income taxes.

- Deferred Tax Assets and Liabilities: The recognition, measurement, and changes in the values of deferred tax assets and liabilities are also recorded in the financial statements. Deferred tax assets are typically presented as non-current assets, while deferred tax liabilities are presented as non-current liabilities in the balance sheet. The impact of changes in deferred tax assets and liabilities is reflected in the income statement as deferred tax expense or income.

Properly recording income tax expense in financial statements ensures compliance with accounting standards and provides stakeholders with valuable insights into a company’s tax obligations and financial performance. By presenting income tax expense separately and providing appropriate disclosure in the footnotes, financial statements offer transparency and enable informed decision-making.

It is important for companies to adhere to accounting standards such as the Generally Accepted Accounting Principles (GAAP) or the International Financial Reporting Standards (IFRS) when recording income tax expense. These standards provide the guidelines for accurately presenting and disclosing income tax expense in financial statements.

Consulting with tax professionals and having a thorough understanding of the relevant accounting standards are crucial for accurately recording income tax expense and providing transparent financial reporting to stakeholders.

Disclosure Requirements for Income Tax Expense

Disclosure requirements for income tax expense play a crucial role in providing transparency and clarity to stakeholders regarding a company’s tax obligations and the impact of taxes on its financial performance. These requirements ensure that relevant information is disclosed in the financial statements and footnotes to enable stakeholders to make informed decisions. Let’s explore the key disclosure requirements for income tax expense:

- Components of Income Tax Expense: Companies are typically required to disclose the components of income tax expense in the footnotes to the financial statements. This includes providing a breakdown of the current tax expense and deferred tax expense. The disclosure may also include information about any adjustments related to changes in tax rates or tax planning strategies.

- Significant Judgments and Estimates: Companies are required to disclose significant judgments and estimates made in determining income tax expense. This may include judgments related to the recognition of deferred tax assets, the valuation allowance, or uncertain tax positions. The disclosure provides insights into the potential impact of these judgments and estimates on future tax obligations.

- Changes in Tax Laws: If there have been any significant changes in tax laws or regulations that could impact income tax expense, companies are required to disclose these changes, their impact, and any related adjustments made to income tax expense. This disclosure allows stakeholders to understand the potential effects of changes in tax legislation on a company’s financial performance.

- Uncertain Tax Positions: If a company has uncertain tax positions, meaning areas of tax treatment that are open to interpretation or subject to disagreement with tax authorities, these positions must be disclosed. The disclosure should include the nature of the uncertainty, the potential impact on income tax expense, and any related contingent liabilities or provisions.

- Tax Planning and Strategies: Companies may disclose information about their tax planning strategies and any tax planning arrangements they have entered into. These disclosures provide insight into how a company manages its tax obligations and any potential risks or benefits associated with its tax planning strategies.

By complying with the disclosure requirements for income tax expense, companies can provide stakeholders with a comprehensive understanding of their tax obligations, the impact of taxes on financial performance, and any potential risks or uncertainties related to income taxes. This enables stakeholders to make well-informed decisions and assess the overall financial health of the company.

It is important for companies to stay updated on applicable reporting frameworks, such as the Generally Accepted Accounting Principles (GAAP) or the International Financial Reporting Standards (IFRS), to ensure compliance with disclosure requirements for income tax expense. Seeking guidance from tax professionals and conducting thorough documentation and analysis of relevant tax positions are vital for accurate and comprehensive disclosure.

Conclusion

Income tax expense accounting is a critical aspect of financial management for both businesses and individuals. Properly calculating, recognizing, and recording income tax expense ensures compliance with tax laws and provides transparency in financial reporting. By understanding the basics of income tax expense accounting, including taxable income, tax rates, and the calculation process, businesses and individuals can accurately determine their tax obligations and optimize their overall tax position.

The accounting treatment for income tax expense, including the recognition of deferred tax assets and liabilities, requires adherence to accounting standards and proper presentation in financial statements. By following these guidelines, companies can provide clear and transparent information about their tax obligations and the impact of taxes on their financial performance.

Disclosure requirements for income tax expense are crucial in providing stakeholders with an understanding of a company’s tax position and the potential risks and uncertainties related to income taxes. Companies must adhere to these requirements and provide comprehensive disclosures in financial statements and footnotes.

To navigate the intricacies of income tax expense accounting, it is recommended to consult with tax professionals who have in-depth knowledge of tax laws and regulations. Staying updated on changes in tax legislation and accounting standards is essential for accurate financial reporting and compliance.

In conclusion, income tax expense accounting is a complex but essential process that ensures accurate financial reporting and compliance with tax laws. By understanding the fundamentals, adhering to accounting standards, and seeking professional guidance, businesses and individuals can effectively manage their tax obligations and optimize their tax positions.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: Chelsea • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance