Finance

What Are Prepaid Expenses In Accounting

Published: October 13, 2023

Learn about prepaid expenses in accounting and how they impact your financial statements. Understand the importance of managing prepaid expenses in your overall finance strategy.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

Introduction

In the realm of accounting, there are various types of expenses that businesses incur to operate smoothly and efficiently. One such type of expense is called “prepaid expenses.” Prepaid expenses are an important aspect of financial management and understanding their nature and accounting treatment is crucial for businesses.

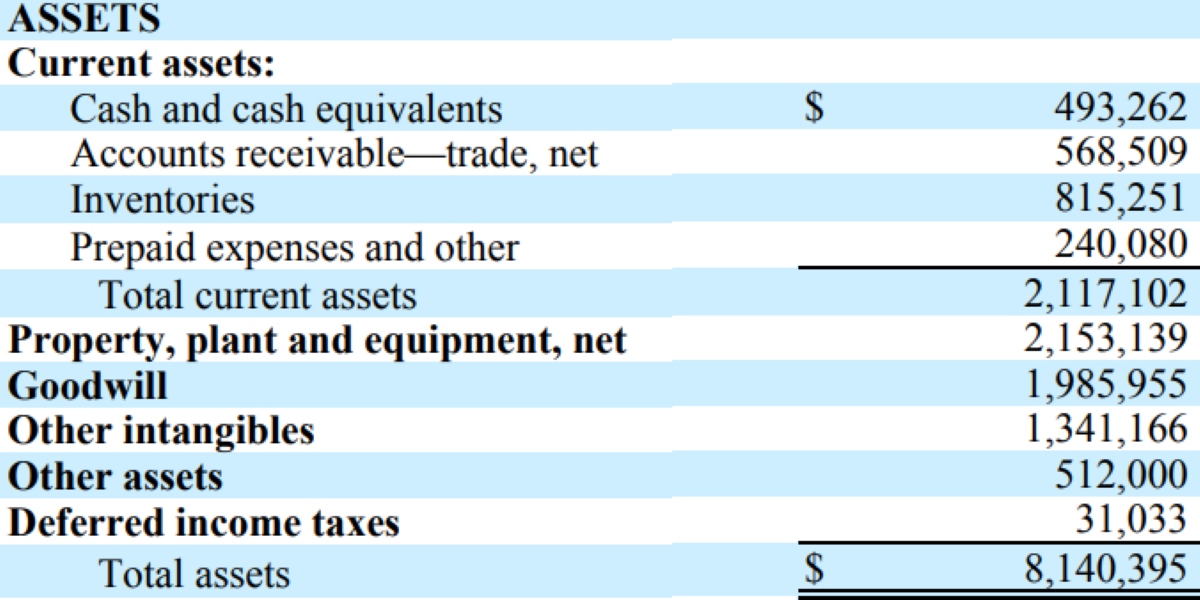

Prepaid expenses are expenses that are paid in advance by a company for goods or services that will be utilized in the future. These expenses are considered assets on the balance sheet because they provide future economic benefits to the company. Prepaid expenses are often incurred for long-term commitments, such as insurance premiums, rent, or maintenance contracts.

Properly recording and accounting for prepaid expenses is essential to accurately represent a company’s financial position. It ensures that expenses are recognized in the appropriate accounting period and aligns with the matching principle of accounting, which states that expenses should be recognized in the same period as the revenue they generate.

In this article, we will delve into the definition and examples of prepaid expenses, explore how they are recognized and accounted for in financial statements, examine the impact on the company’s financial position, and discuss the importance of properly handling prepaid expenses.

Definition of Prepaid Expenses

Prepaid expenses, also known as prepaid assets or unexpired expenses, are expenses that a company pays for in advance but has not yet consumed or received the full benefit of. These expenses are considered assets because they represent future economic benefits that the company will receive.

Prepaid expenses can take various forms depending on the nature of the expense and the industry in which the company operates. Common examples of prepaid expenses include:

- Insurance premiums: Companies often make advance payments for insurance coverage to protect against potential risks and liabilities.

- Rent: Many businesses prepay rent for office space or equipment leases.

- Subscriptions: Companies may pay in advance for subscriptions to magazines, professional memberships, or software services.

- Maintenance contracts: Some businesses enter into contracts for regular maintenance of equipment or facilities and make advanced payments for these services.

- Advertising: Prepayments for advertising campaigns or marketing efforts are also classified as prepaid expenses.

These are just a few examples, but prepaid expenses can encompass a wide range of costs that are paid in advance but not yet utilized. It’s important to note that the duration of the prepaid expense can vary. Some prepaid expenses may cover a short-term period, such as a month or quarter, while others may cover an entire year or even longer.

Recognizing and accounting for prepaid expenses accurately is crucial to ensure the financial statements reflect the true financial position of the company. The treatment of prepaid expenses differs from regular expenses, as they are not immediately recognized as expenses when paid. Instead, they are initially recorded as an asset on the balance sheet and gradually recognized as expenses over the period when the benefit is consumed. This process is known as amortization or expense recognition.

Examples of Prepaid Expenses

Prepaid expenses are a common occurrence in various industries, and their specific examples may vary depending on the nature of the business. Here are some common examples of prepaid expenses:

- Insurance Premiums: Many companies pay their insurance premiums in advance to ensure continuous coverage. These prepaid expenses are typically recognized as assets and gradually expensed over the coverage period.

- Rent: Businesses often prepay rent for office spaces, retail locations, or equipment leases. These prepaid rent expenses are recognized as assets and allocated to the appropriate accounting periods.

- Subscriptions: Companies may subscribe to industry publications, professional memberships, or software services and make upfront payments. These prepaid expenses are amortized over the subscription period.

- Utilities: In some cases, companies might pay utility bills, such as electricity, water, or internet services, in advance. These prepaid utility expenses are recorded as assets and recognized as expenses over the usage period.

- Maintenance Contracts: Businesses often enter into contracts for routine maintenance of equipment or facilities. Prepayments for these maintenance services are considered prepaid expenses and recognized as expenses over the contract period.

- Advertising: Companies might prepay for advertising campaigns, both online and offline, to promote their products or services. These prepaid advertising expenses are recognized as assets and gradually expensed as the advertising campaign unfolds.

- Software Licenses: Many companies pay for software licenses upfront or on an annual basis. These prepaid software expenses are amortized over the license period.

These examples demonstrate the diverse nature of prepaid expenses and emphasize the importance of accurately accounting for them. Properly recognizing and allocating these prepaid expenses to the appropriate accounting periods ensures that the financial statements reflect the true financial position and performance of the company.

Recognition and Accounting for Prepaid Expenses

Recognizing and accounting for prepaid expenses involves several steps to ensure accurate financial reporting. Let’s explore the process:

- Initial Recording: When a company makes a payment for a prepaid expense, it is initially recorded as an asset on the balance sheet. The amount is debited to the prepaid expense account and credited to the cash or accounts payable account, depending on the payment method.

- Expense Recognition: Over time, as the benefit of the prepaid expense is consumed, a portion of the prepaid amount is recognized as an expense. This is typically done on a systematic basis, following the matching principle of accounting.

- Adjusting Entries: At the end of each accounting period, adjusting entries are made to properly reflect the prepaid expense on the income statement and balance sheet. An adjusting entry debits the appropriate expense account and credits the prepaid expense account, reducing the balance of the prepaid asset.

Let’s consider an example to understand the accounting for prepaid expenses. ABC Company pays $12,000 for a one-year insurance policy on January 1st. The monthly insurance expense is $1,000.

On January 1st, ABC Company records the transaction as follows:

Prepaid Insurance 12,000

Cash 12,000

At the end of each month, ABC Company would make the following adjusting entry:

Insurance Expense 1,000

Prepaid Insurance 1,000

This entry reduces the prepaid insurance asset by $1,000 and recognizes the monthly insurance expense of $1,000 on the income statement.

By making adjusting entries at the end of each accounting period, the correct amount of prepaid expense is recognized, ensuring accurate financial reporting. It is important to note that the duration of prepaid expenses may vary, and adjusting entries need to be made accordingly.

Properly recording and tracking prepaid expenses provides a clear picture of the company’s financial performance and helps in making informed financial decisions. Incorrect recognition or failure to account for prepaid expenses can result in inaccurate financial statements and misrepresentation of the company’s financial position.

Adjusting Entries for Prepaid Expenses

Adjusting entries are an important part of the accounting process, and they play a crucial role in properly reflecting prepaid expenses in the financial statements. Adjusting entries are made at the end of each accounting period to ensure that the correct amount of expense is recognized and the prepaid expense balance is accurately reflected on the balance sheet.

When it comes to prepaid expenses, adjusting entries are made to allocate the portion of the prepaid amount that has been consumed as an expense, reducing the prepaid asset balance. The specific adjusting entry depends on the frequency and duration of the prepaid expense.

There are two common methods for adjusting entries for prepaid expenses:

- Time-Based Method: This method is used when the prepaid expense covers a specific time period, such as insurance premiums or rent. The adjustment is made by recognizing the expense over the duration of the prepaid period. For example, if a company pays $12,000 for a one-year insurance premium, and each month represents $1,000 of expense, the adjusting entry at the end of each month would be to debit the related expense account (e.g., Insurance Expense) and credit the prepaid asset account (e.g., Prepaid Insurance) for $1,000.

- Usage-Based Method: This method is used when the prepaid expense is consumed based on usage rather than time, such as utilities or supplies. The adjustment is made by estimating the amount of prepaid expense used during the accounting period. For example, if a company prepayments $1,200 for utilities and estimates that 60% has been consumed at the end of the month, the adjusting entry would be to debit the related expense account (e.g., Utilities Expense) and credit the prepaid asset account (e.g., Prepaid Utilities) for $720 ($1,200 * 60%).

It’s important to note that adjusting entries for prepaid expenses have an impact on both the income statement and the balance sheet. The expense recognized in the adjusting entry reduces net income on the income statement, while the reduction in the prepaid asset balance affects the balance sheet.

By making adjusting entries for prepaid expenses, businesses ensure that the financial statements accurately reflect the expenses incurred during the accounting period and provide a true representation of the company’s financial position. Failure to make these adjustments can lead to distorted financial statements and misrepresentation of the company’s profitability and assets.

Impact on Financial Statements

The recognition and accounting for prepaid expenses have a significant impact on a company’s financial statements. The proper treatment of prepaid expenses ensures the accurate representation of the company’s financial position and performance. Let’s explore the impact on the financial statements:

1. Balance Sheet: Prepaid expenses are initially recorded as assets on the balance sheet. They represent future economic benefits to the company. As the prepaid expense is consumed over time, the balance of the prepaid asset decreases through adjusting entries. This reduction in the prepaid asset balance is reflected as an increase in the corresponding expense category on the income statement.

2. Income Statement: As the prepaid expense is gradually recognized as an expense through adjusting entries, it affects the company’s net income. The recognized expense reduces the net income for the accounting period, thus impacting the profitability of the business. It is important to accurately match the expense recognition with the corresponding revenue generated in the same accounting period, following the matching principle of accounting.

3. Cash Flow Statement: Prepaid expenses do not directly impact cash flow since they involve payments made in advance. However, the recognition of the prepaid expense as an expense in the income statement does affect the operating activities section of the cash flow statement. The cash paid for the prepaid expense is reflected in the cash flow from operating activities, while the expense recognized adjusts the net income to arrive at the cash provided or used by operating activities.

The impact of prepaid expenses on the financial statements is evident primarily through the changes in the balance sheet and income statement. The accurate recognition and accounting for prepaid expenses ensure that the financial statements provide users with a clear understanding of the company’s financial health, performance, and cash flow.

It is essential for businesses to diligently handle prepaid expenses to maintain the integrity of their financial reporting. Failing to properly recognize and account for prepaid expenses can lead to misrepresentation of financial performance, inaccurate calculation of profitability, and poor decision-making based on misleading financial information.

Importance and Benefits of Properly Accounting for Prepaid Expenses

Properly accounting for prepaid expenses is of paramount importance for businesses. It ensures accurate financial reporting, portrays the true financial position of the company, and provides several benefits. Let’s explore the importance and benefits of properly accounting for prepaid expenses:

1. Accurate Financial Statements: Properly accounting for prepaid expenses ensures that the financial statements reflect the true financial position and performance of the company. By recognizing and allocating prepaid expenses to the appropriate accounting periods, the income statement and balance sheet accurately represent the company’s expenses and assets.

2. Matching Principle: Accounting for prepaid expenses follows the matching principle, which states that expenses should be recognized in the same accounting period as the revenue they generate. By properly recognizing and expensing prepaid expenses, the matching principle is upheld, ensuring the accurate calculation of profitability and aligning revenue and expenses in the financial statements.

3. Decision-Making: Accurate accounting for prepaid expenses provides business owners and managers with reliable financial information for decision-making. It allows them to analyze the true costs of operations, identify trends, and make informed decisions regarding budgeting, cash flow management, pricing strategies, and resource allocation.

4. Compliance with Accounting Standards: Properly accounting for prepaid expenses ensures compliance with accounting standards and regulations. It demonstrates transparency and adherence to accounting principles, which is crucial for maintaining the trust of stakeholders, such as investors, lenders, and regulatory bodies.

5. Effective Budgeting and Planning: Having accurate records of prepaid expenses enables businesses to effectively plan and budget for future expenses. By knowing the expected prepaid expenses, businesses can allocate funds appropriately, optimize cash flow management, and avoid unexpected financial strains.

6. Improved Financial Analysis: Accurate accounting for prepaid expenses enhances financial analysis capabilities. It allows for meaningful comparative analysis across different periods, highlighting trends and patterns that can aid in identifying areas for cost savings, efficiency improvements, and strategic decision-making.

In summary, properly accounting for prepaid expenses is crucial for businesses to ensure accurate financial reporting, comply with accounting standards, make informed decisions, and effectively plan for the future. By upholding the matching principle and providing reliable financial information, businesses can enhance their financial analysis capabilities and optimize their financial management processes.

Conclusion

Properly accounting for prepaid expenses is an essential aspect of financial management for businesses. Prepaid expenses represent costs paid in advance for goods or services that will be utilized in the future. By accurately recognizing and accounting for prepaid expenses, businesses can ensure the integrity of their financial statements, comply with accounting standards, and make informed financial decisions.

Throughout this article, we have explored the definition and examples of prepaid expenses, as well as the recognition and accounting process for them. We have seen how prepaid expenses are initially recorded as assets on the balance sheet and gradually recognized as expenses through adjusting entries. This process aligns with the matching principle, ensuring that expenses are recognized in the same period as the revenue they generate.

Understanding and properly accounting for prepaid expenses have numerous benefits. Accurate financial statements provide a true representation of a company’s financial position and performance, enabling informed decision-making and effective budgeting. Compliance with accounting standards and regulations instills trust in stakeholders and ensures transparency in financial reporting. Additionally, proper accounting for prepaid expenses enhances financial analysis capabilities, supporting strategic planning and cost-saving initiatives.

In conclusion, businesses must prioritize the proper recognition and accounting of prepaid expenses to maintain financial accuracy and integrity. By doing so, businesses can navigate the complexities of prepaid expenses, optimize their financial management processes, and support the overall success and sustainability of their operations.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance