Finance

How To Cancel A Secured Card At SDFCU

Published: March 2, 2024

Learn how to cancel a secured card at SDFCU and manage your finances effectively. Follow our step-by-step guide to streamline the process.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

Introduction

Secured credit cards serve as a valuable financial tool for individuals aiming to establish or rebuild their credit. These cards require a cash deposit as collateral, providing a viable option for those with limited or damaged credit history. However, circumstances may arise where cardholders need to cancel their secured cards, and understanding the process is essential.

In this comprehensive guide, we will delve into the specifics of canceling a secured card at SDFCU (State Department Federal Credit Union). Whether you are seeking alternative financial products or have achieved improved credit standing, knowing the steps and considerations involved in cancelling a secured card can empower you to make informed decisions about your financial future.

Understanding the nuances of secured cards and the implications of cancellation is crucial. We will explore the reasons behind cancelling a secured card, the step-by-step process for doing so at SDFCU, and the essential considerations to bear in mind before finalizing the decision. By the end of this guide, you will have a clear understanding of the necessary steps and factors to consider when contemplating the cancellation of a secured card at SDFCU.

Understanding Secured Cards

Secured credit cards are designed to provide individuals with limited or damaged credit histories an opportunity to build or rebuild their credit. Unlike traditional credit cards, secured cards require a cash deposit, which serves as collateral and determines the card’s credit limit. This deposit mitigates the risk for the card issuer, making secured cards accessible to individuals who may not qualify for unsecured credit cards.

When a cardholder makes purchases using a secured card, the available credit is reduced by the amount of the purchase, just like with a traditional credit card. Monthly payments are required, and the cardholder’s payment history is reported to credit bureaus, thereby contributing to their credit profile.

It’s important to note that while secured cards offer a pathway to building credit, they often come with higher interest rates and fees compared to traditional credit cards. However, responsible use of a secured card can lead to improved credit scores over time, opening doors to better financial opportunities.

Understanding the mechanics of secured cards is crucial for individuals considering the cancellation of their SDFCU secured card. By comprehending the role of secured cards in credit-building and the impact of cancellation, cardholders can make informed decisions about their financial strategies.

Reasons for Cancelling a Secured Card

Cancelling a secured card is a significant decision that should be made thoughtfully and with a clear understanding of the potential implications. Several reasons may prompt individuals to consider cancelling their secured card, including:

- Improved Credit Standing: As individuals work diligently to improve their credit, they may become eligible for unsecured credit cards with more favorable terms. In such cases, cancelling the secured card can be a strategic move to transition to a traditional credit card without the need for a security deposit.

- Transition to Better Financial Products: With an enhanced credit profile, individuals may seek access to financial products offering superior rewards, lower interest rates, or higher credit limits. Cancelling the secured card can pave the way for obtaining these more advantageous products.

- Reducing Fees and Interest Rates: Secured cards often entail higher fees and interest rates compared to unsecured cards. Once a cardholder’s credit has improved, they may wish to cancel their secured card to escape these less favorable terms.

- Changing Financial Goals: As individuals’ financial goals evolve, they may find that the features and benefits of their secured card no longer align with their current objectives. Cancelling the secured card can signify a shift in financial strategy.

- Financial Hardship: In some cases, unforeseen financial challenges may necessitate the cancellation of a secured card. Whether due to job loss, medical expenses, or other financial hardships, individuals may need to close their secured card to alleviate financial burdens.

Understanding the reasons behind cancelling a secured card is essential for individuals evaluating their financial needs and goals. By recognizing the factors that may prompt card cancellation, individuals can make informed decisions aligned with their evolving financial circumstances and aspirations.

Steps to Cancel a Secured Card at SDFCU

Cancelling a secured card at SDFCU involves a series of specific steps to ensure a seamless and well-executed process. By following the outlined procedure, cardholders can effectively close their secured card account. Here are the essential steps to cancel a secured card at SDFCU:

- Review the Terms and Conditions: Before initiating the cancellation process, carefully review the terms and conditions of your secured card agreement with SDFCU. Understanding any potential fees, outstanding balances, or specific cancellation requirements is crucial.

- Pay off the Balance: If there is an outstanding balance on the secured card, ensure that it is paid off in full. This step is essential to close the account and prevent any lingering financial obligations.

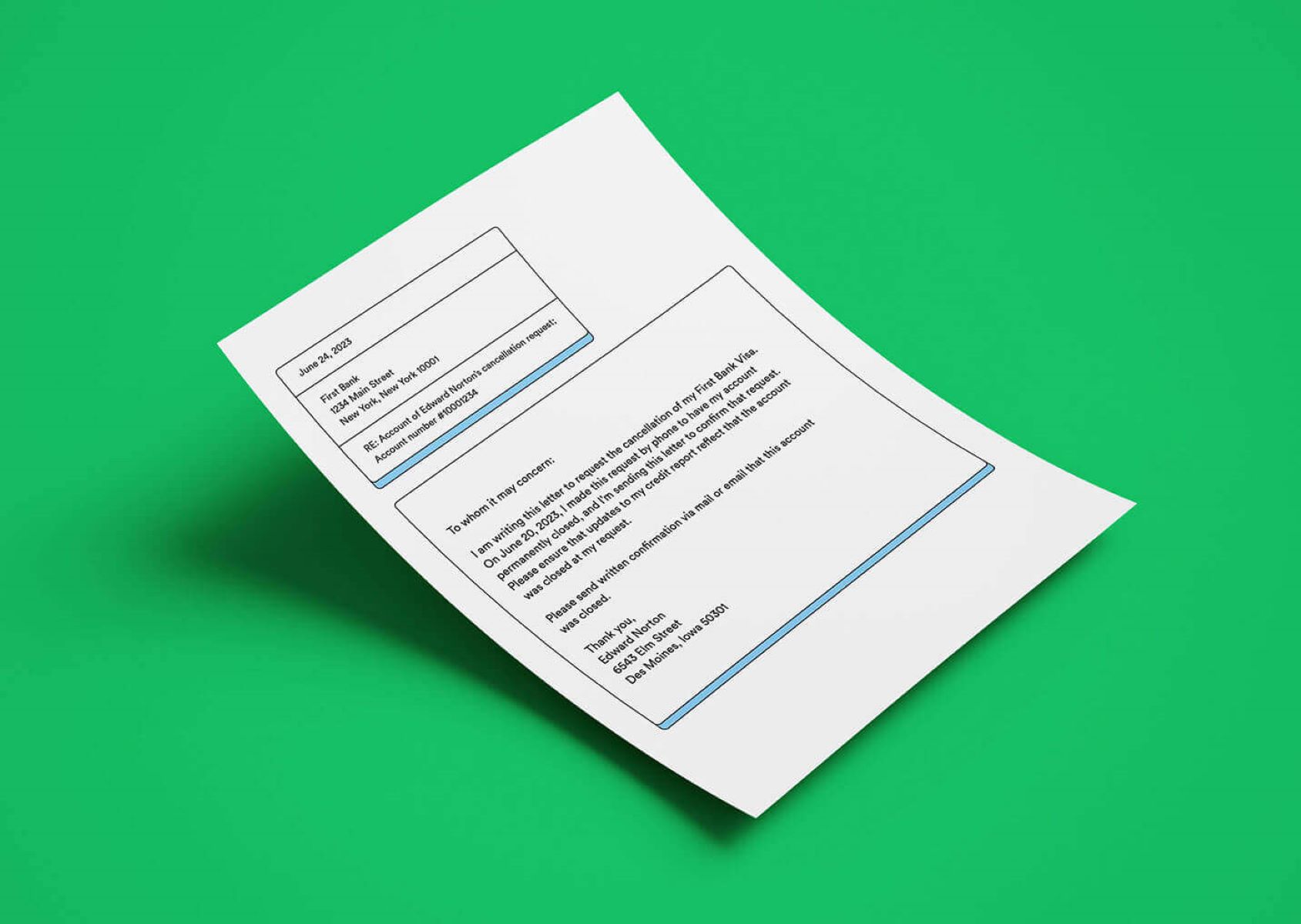

- Contact SDFCU Customer Service: Reach out to SDFCU’s customer service department via phone or secure message through the online banking portal. Inform them of your intention to cancel the secured card and inquire about any specific procedures or documentation required.

- Follow SDFCU’s Cancellation Instructions: SDFCU may have a formal process for cancelling a secured card. Adhere to their instructions, which may include submitting a written request or completing a cancellation form.

- Destroy the Secured Card: Once the cancellation is confirmed, safely destroy the physical card to prevent any unauthorized usage. Shredding or cutting the card into pieces is recommended.

- Monitor Your Credit Report: After cancelling the secured card, monitor your credit report to ensure that the account is reported as closed. Verifying this information can help safeguard your credit standing.

- Dispose of the Security Deposit: If the security deposit is refundable, confirm the process for its return. SDFCU may issue a refund for the deposit, typically via check or direct deposit.

By diligently following these steps, individuals can effectively navigate the process of cancelling a secured card at SDFCU, ensuring that the account closure is executed smoothly and in compliance with the institution’s policies.

Considerations Before Cancelling

Before proceeding with the cancellation of a secured card at SDFCU, it is crucial to carefully consider several important factors to make an informed decision. These considerations can significantly impact your financial standing and credit profile. Here are the key aspects to contemplate before cancelling a secured card:

- Credit Impact: Closing a credit account, even a secured card, can affect your credit score. If the secured card has been managed responsibly and maintained a positive payment history, its closure may impact the length of your credit history and credit utilization ratio.

- Alternative Options: Evaluate alternative options within SDFCU, such as transitioning to an unsecured card or exploring other credit products offered by the institution. This can help maintain your relationship with the credit union while potentially accessing more favorable financial products.

- Refundable Deposit: If your secured card required a security deposit, confirm the process for the return of the deposit upon account closure. Understanding the timeline and method for receiving the deposit refund is essential.

- Outstanding Balances or Fees: Ensure that all outstanding balances, including interest and fees, are settled before closing the secured card. This proactive approach can prevent any lingering financial obligations and ensure a clean closure of the account.

- Future Credit Needs: Consider your future credit needs and how the cancellation of the secured card may impact your access to credit. If you plan to apply for new credit in the near future, the closure of the secured card can influence your overall credit profile.

- Communication with SDFCU: If you have specific concerns or reasons for cancelling the secured card, consider communicating with SDFCU to explore potential solutions or accommodations. The credit union may offer guidance or alternative options based on your circumstances.

By carefully weighing these considerations and their potential implications, individuals can make an informed choice regarding the cancellation of their secured card at SDFCU. Taking a proactive and thoughtful approach can help mitigate any adverse effects and pave the way for a smooth transition in your financial journey.

Conclusion

Cancelling a secured card at SDFCU is a significant financial decision that warrants careful consideration and a clear understanding of the associated processes and implications. Throughout this guide, we have explored the fundamental aspects of secured cards, the reasons that may prompt individuals to cancel their secured cards, the step-by-step process for cancelling a secured card at SDFCU, and the essential considerations to ponder before finalizing the decision.

Understanding the role of secured cards in credit-building, the potential impact of cancellation on credit standing, and the importance of evaluating alternative options within SDFCU are crucial elements in the decision-making process. By meticulously following the steps for cancellation and considering the broader financial implications, individuals can navigate the closure of their secured card account with confidence and prudence.

Ultimately, the decision to cancel a secured card at SDFCU should align with your evolving financial goals, credit needs, and overall financial well-being. By approaching the cancellation process thoughtfully and proactively, you can position yourself for a seamless transition and continued progress in your financial journey.

It is recommended to consult with SDFCU’s customer service representatives or financial advisors if you have specific inquiries or require personalized guidance regarding the cancellation of your secured card. Their expertise and insights can provide valuable clarity as you navigate this important financial milestone.

By leveraging the knowledge and considerations outlined in this guide, individuals can confidently navigate the process of cancelling a secured card at SDFCU, empowering them to make informed decisions that align with their financial aspirations and contribute to their long-term financial success.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: Rachel Chua • Finance