Finance

How To Cash Savings Bonds Of Deceased

Published: January 16, 2024

Learn how to cash savings bonds of a deceased person and manage their finances effortlessly. Gain valuable insights into finance and estate planning.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

Introduction

When a loved one passes away, there are numerous administrative tasks that need to be addressed, and one of them is dealing with their financial assets. If your deceased family member had savings bonds, it’s important to understand the process of cashing them in. Savings bonds are a popular investment option because they provide a safe and reliable way to grow savings over time.

In this article, we will guide you through the process of cashing savings bonds of a deceased individual. We will cover the necessary steps, documentation, and procedures to ensure a smooth and successful completion of the process. By following this guide, you’ll be equipped with the information needed to navigate this potentially complex situation and access the funds tied up in the savings bonds.

Before diving into the details, it’s important to have a basic understanding of what savings bonds are and how they work.

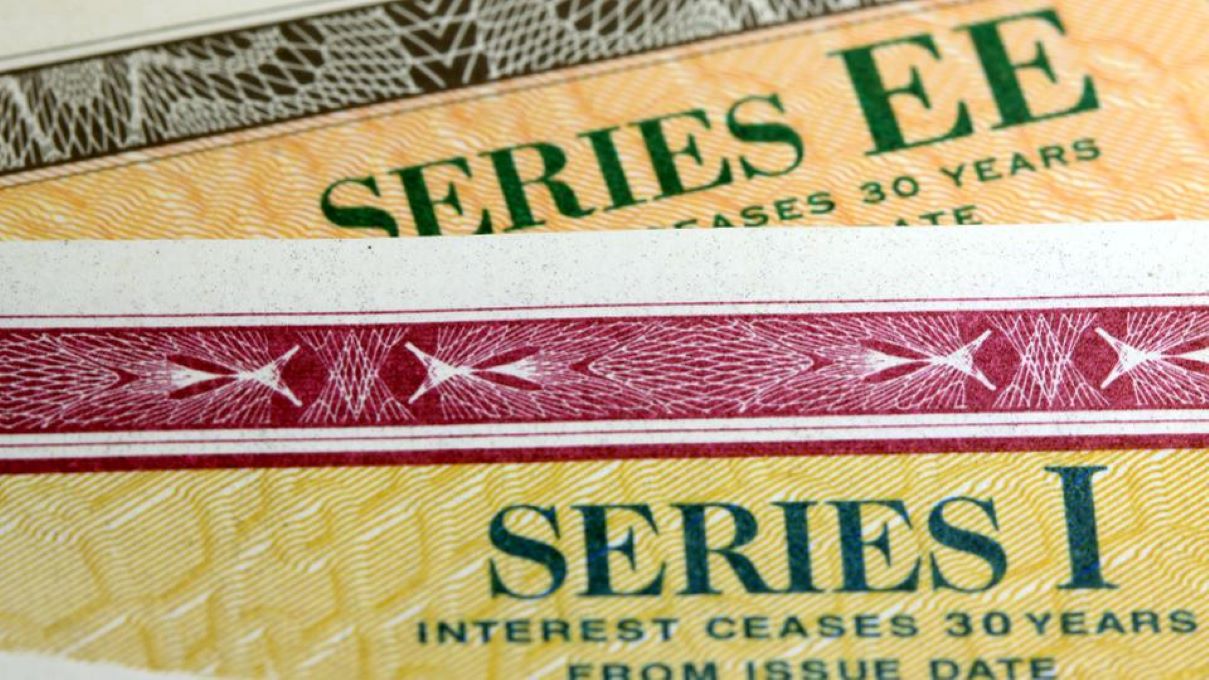

Savings bonds are debt securities issued by the U.S. Department of the Treasury. They are considered one of the safest and most secure forms of investment available. These bonds are a way for individuals to lend money to the government, which in turn pays interest on the principal investment. The interest accrues over a specified period, typically 30 years, and can be redeemed by the bondholder after a minimum holding period of 12 months. Savings bonds come in different series, including the EE, I, and H bonds, each with its own set of features and benefits.

In the unfortunate event of a loved one passing away, you may find yourself in a situation where you need to determine ownership of their savings bonds.

Understanding Savings Bonds

Savings bonds are a type of investment issued by the U.S. Department of the Treasury. They are considered a safe and reliable way to save money and earn interest over time. Understanding how savings bonds work is crucial when it comes to cashing them in after the death of a bondholder.

There are several types of savings bonds available, including Series EE, Series I, and Series H bonds. Series EE bonds are typically purchased at half their face value and earn a fixed rate of interest. These bonds have a maturity period of 30 years, but they can be cashed in after holding them for at least 12 months. Series I bonds, on the other hand, have a variable interest rate that is adjusted for inflation. They can be cashed in after holding them for at least 12 months as well. Series H bonds are no longer available for purchase, but if your deceased loved one has this type of bond, it can still be cashed in.

When it comes to cashing in savings bonds after a person’s death, it’s important to determine the ownership of the bonds. If the bonds were registered solely in the deceased person’s name, they will need to go through the probate process. However, if the bonds are held jointly with another person, it may be possible for the surviving co-owner to redeem them without going through probate.

It’s also important to note that savings bonds are subject to federal estate tax. If the total value of the deceased person’s estate, including the bonds, exceeds the estate tax exemption threshold, the estate may be subject to tax. It’s recommended to consult with a tax professional to understand and navigate the tax implications.

In the next sections, we will dive into the specific steps and documentation required to cash savings bonds of a deceased individual.

Determining Ownership of Bonds

Before you can proceed with cashing in savings bonds of a deceased individual, it is important to determine the ownership of the bonds. This step is crucial as it will determine the next course of action and the documentation required for redemption.

If the savings bonds were registered solely in the name of the deceased individual, the bonds may need to go through the probate process. Probate is a legal process through which the court oversees the distribution of a deceased person’s assets. The court will appoint an executor or personal representative who will be responsible for handling the deceased individual’s estate, including the savings bonds.

If the savings bonds were registered jointly with another individual, such as a spouse or child, the surviving co-owner may be able to redeem the bonds without going through probate. However, it is important to gather the necessary documentation to establish ownership and prove the relationship to the deceased individual.

To determine ownership of the savings bonds, the following steps can be taken:

- Locate the physical bonds: Start by locating the physical savings bonds. They may be stored in a safe deposit box, a personal safe, or any other secure location.

- Check the registration: Look closely at the bonds to identify the registration. The registration will indicate how the bonds are titled and who the owners are.

- Review beneficiary designations: In some cases, the deceased individual may have designated a beneficiary for the savings bonds. Check if there is a designated beneficiary and gather the necessary documentation to establish their relationship to the deceased.

- Consult with an attorney: If there is uncertainty or complexity in determining ownership, it is advisable to consult with an attorney who specializes in estate planning and probate. They can provide legal guidance and assist in navigating the process.

Once you have determined the ownership of the savings bonds, you can proceed with the necessary steps to cash them in. In the following sections, we will explore the required documentation and the process of notifying the Treasury Department to initiate the redemption process.

Required Documentation

When cashing in savings bonds of a deceased individual, it is essential to gather the necessary documentation to prove eligibility and ownership. The required documentation may vary depending on the circumstances, such as whether the bonds were registered solely in the deceased person’s name or held jointly with another individual. Below is a list of common documents that may be required:

- Death certificate: A certified copy of the death certificate is typically required to establish the death of the bondholder. The death certificate can be obtained from the vital records office in the state where the individual passed away.

- Proof of identity: To ensure that you are authorized to cash in the savings bonds, you will need to provide proof of your own identity. This may include a valid government-issued identification document such as a driver’s license or passport.

- Proof of relationship to the deceased: If you are the surviving co-owner or designated beneficiary of the savings bonds, you may need to provide documentation to establish your relationship to the deceased individual. This can be in the form of a marriage certificate, birth certificate, or other legal documents.

- Probate documents: If the savings bonds are solely in the name of the deceased individual and need to go through probate, you will likely need to provide relevant probate documents. These may include the letters testamentary or letters of administration, which are issued by the court to authorize the executor or personal representative to act on behalf of the estate.

- Power of attorney documents: If you are acting as an attorney-in-fact or have power of attorney for the deceased individual, you will need to provide the appropriate legal documentation to establish your authority to redeem the savings bonds.

It is important to note that the above list is not exhaustive, and additional documentation may be required based on the specific circumstances and the policies of the Treasury Department or financial institution where the bonds are held. It is recommended to contact the relevant institution or consult with a financial advisor to ensure that you have all the necessary documents before proceeding with the redemption process.

Once you have gathered the required documentation, you can proceed with notifying the Treasury Department of the bondholder’s death and initiating the redemption process. The next section will guide you through the steps of notifying the Treasury Department and completing the claim form.

Notifying the Treasury Department

After gathering the necessary documentation and determining the ownership of the savings bonds, the next step is to notify the Treasury Department of the bondholder’s death. Notifying the Treasury Department is important as it will initiate the process of redeeming the savings bonds and transferring the funds to the rightful beneficiaries.

To notify the Treasury Department, you will need to follow these steps:

- Contact the Bureau of the Fiscal Service: The Bureau of the Fiscal Service is responsible for handling savings bond transactions. You can contact them by phone or email to inform them about the bondholder’s death. They will guide you through the necessary procedures and provide instructions on how to proceed.

- Provide the required information: The Treasury Department will need specific information about the deceased individual and the savings bonds. This may include the bond serial numbers, issue dates, denominations, and any relevant account numbers associated with the bonds. Be prepared to provide accurate and detailed information to facilitate the redemption process.

- Submit the necessary documentation: Along with the information about the bonds, you will need to submit the required documentation, such as the death certificate and any other supporting documents that establish your eligibility to redeem the savings bonds. Make sure to follow the Treasury Department’s guidelines for document submission.

- Follow up on the notification: After notifying the Treasury Department, it is important to maintain regular communication and follow up on the status of your claim. Keep records of all correspondence and make note of the names and contact information of the people you speak with at the Treasury Department.

It is crucial to notify the Treasury Department as soon as possible after the bondholder’s death to avoid any potential issues or delays in redeeming the savings bonds. By following the proper notification procedures and providing the required information and documentation, you can ensure a smooth and efficient transfer of funds.

Once you have notified the Treasury Department, you can proceed with completing the claim form, which is the next step in the process. The following section will guide you through the steps of completing the claim form for cashing in the savings bonds.

Completing the Claim Form

After notifying the Treasury Department of the bondholder’s death and providing the necessary information, the next step is to complete the claim form. The claim form is required to officially request the redemption of the savings bonds and transfer the funds to the designated beneficiaries.

To complete the claim form, follow these steps:

- Obtain the appropriate form: The specific claim form required to cash in the savings bonds will depend on the type of bonds and the ownership structure. You can obtain the form from the Treasury Department’s website or by contacting the Bureau of the Fiscal Service.

- Fill in the necessary information: The claim form will ask for essential details about the bondholder, the bonds being redeemed, and the beneficiaries. Provide accurate information such as the bondholder’s name, social security number, bond serial numbers, denominations, issue dates, and the names and contact information of the beneficiaries.

- Submit supporting documents: Along with the completed claim form, you may need to attach the required supporting documents. This may include the death certificate, proof of ownership, proof of relationship to the deceased, and any other documentation specified by the Treasury Department.

- Review and sign the form: Carefully review the claim form and ensure that all the information provided is accurate and complete. Sign the form according to the instructions provided.

It is important to fill out the claim form accurately and provide all the necessary documentation to avoid any potential delays or complications in the redemption process. Keep copies of the completed claim form and supporting documents for your records.

Once you have completed the claim form, you can proceed with submitting it to the Treasury Department for processing. The next section will provide guidance on how to submit the claim form and what to expect in terms of receiving the funds from the redeemed savings bonds.

Submitting the Claim Form

After completing the claim form for cashing in the savings bonds of a deceased individual, the next step is to submit the form to the Treasury Department for processing. Submitting the claim form properly is crucial to ensure that the redemption process proceeds smoothly and efficiently.

Here are the steps to submit the claim form:

- Make copies of the claim form and supporting documents: Before submitting the claim form, make copies of the completed form and all the supporting documents. This will serve as a backup in case any issues arise during the submission process.

- Follow the submission instructions: The claim form will have specific instructions on how to submit it. This may include mailing the form to a specific address or submitting it electronically through the Treasury Department’s website.

- Include additional required documents: Along with the claim form, double-check that you have included all the necessary supporting documents as outlined in the instructions. This may include the death certificate, proof of ownership, and any other documentation specified.

- Send the claim form by certified mail: When submitting the claim form by mail, consider sending it via certified mail with a return receipt requested. This will provide proof of delivery and ensure that it reaches the Treasury Department safely.

- Keep track of the submission: Keep a record of the date and method of submission, such as the tracking number if using certified mail. This will allow you to track the progress of your claim and follow up if necessary.

After submitting the claim form, it may take some time for the Treasury Department to process the request and redeem the savings bonds. It is essential to be patient during this time and to keep track of any communication or updates received from the department.

Once the claim form has been processed and approved, the Treasury Department will transfer the funds to the designated beneficiaries. The next section will provide information on how the funds are typically received and what to expect in terms of timelines.

Receiving the Funds

After the Treasury Department processes the claim form for cashing in the savings bonds of a deceased individual, the next step is to receive the funds. It is important to understand how the funds are typically disbursed and have an idea of what to expect in terms of timelines.

Here’s what you need to know about receiving the funds:

- Method of payment: The Treasury Department typically offers two options for receiving the funds – electronic deposit or a paper check. Electronic deposit, also known as direct deposit, is the faster and more convenient option. The funds are directly deposited into the bank account specified on the claim form. If you opt for a paper check, it will be mailed to the address provided on the claim form.

- Timeline: The timeline for receiving the funds can vary. It typically takes a few weeks for the Treasury Department to process the claim form and verify the documentation. Once approved, electronic deposit payments are usually received within 1-2 business days. Paper checks may take longer to arrive, depending on the postal service. It’s important to be patient and allow sufficient time for the funds to be disbursed.

- Post-redemption taxes: It’s crucial to note that taxes may be applicable on the redeemed savings bonds. The interest earned on the savings bonds is subject to federal income tax, but not to state or local income tax. You may receive a Form 1099-INT from the Treasury Department, which will provide information on the taxable interest. It is recommended to consult with a tax professional to understand and fulfill any tax obligations.

- Retain records: After receiving the funds, it is important to retain the records of the redeemed savings bonds and related documents for your financial records. These records may be needed for tax purposes or future reference.

Remember to keep track of any correspondence or communication received from the Treasury Department regarding the redemption of the savings bonds. This will help ensure that the process goes smoothly and you have a clear record of the transaction.

By following these steps and being aware of the disbursement process, you can successfully receive the funds from the redeemed savings bonds of the deceased individual.

Before we conclude, let’s recap the important steps covered in this article to cash savings bonds of a deceased individual.

Conclusion

Cashing in savings bonds of a deceased individual can be a complex process that requires careful attention and proper documentation. By following the necessary steps outlined in this guide, you can navigate through the process with ease and ensure a successful redemption of the savings bonds.

Understanding the basics of savings bonds and determining ownership are crucial initial steps. It’s important to gather the required documentation, such as the death certificate and proof of ownership, to establish eligibility for redemption. Notifying the Treasury Department of the bondholder’s death is essential to initiate the process.

Completing the claim form accurately and supplying the necessary supporting documents is vital to ensure a smooth transaction. The claim form can be submitted either by mail or electronically, following the specific instructions provided by the Treasury Department. Once the claim form is processed and approved, you can expect to receive the funds through electronic deposit or a paper check.

It’s important to be aware of any post-redemption tax obligations and consult with a tax professional as needed. Keeping records of the redeemed savings bonds and related documents is crucial for future reference and tax purposes.

Dealing with the financial matters of a deceased loved one can be challenging, but with the right knowledge and guidance, you can successfully navigate the process of cashing in their savings bonds and access the funds they have accumulated over time.

If you have specific questions or need further assistance, it is always recommended to reach out to the Treasury Department or consult with a financial advisor who can provide personalized advice based on your unique circumstances.

Remember, this article serves as a general guide, and it’s important to stay informed about any updates or changes in policies and procedures that may affect cashing in savings bonds.

With proper understanding and careful execution of the steps outlined in this guide, you’ll be equipped to handle the process of cashing in savings bonds of a deceased individual with confidence and efficiency.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance