Finance

What Is Another Name For Balance Sheet

Published: December 27, 2023

Discover the alternate term for a balance sheet in the world of finance. Explore the significance and functions of this essential financial statement.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

Introduction

When it comes to understanding the financial health and performance of a company, one of the essential tools investors and analysts rely on is the balance sheet. The balance sheet provides a snapshot of a company’s financial position at a specific point in time, showcasing its assets, liabilities, and shareholders’ equity.

It is crucial for investors and stakeholders to have a clear understanding of a company’s financial standing, as it enables them to assess its liquidity, solvency, and overall stability. Being able to interpret and analyze a balance sheet is a fundamental skill in the world of finance and business.

In this article, we will explore the concept of a balance sheet, its purpose, and the components that make it up. In addition, we will also delve into the alternative term used to refer to a balance sheet, shedding light on common synonyms that you may come across in financial discussions.

Whether you are a seasoned investor, a finance professional, or simply someone looking to broaden their knowledge of finance, this article will provide you with valuable insights into the intricacies of a balance sheet and its alternative names.

Definition of Balance Sheet

A balance sheet is a financial statement that provides a snapshot of a company’s financial position at a given point in time. It is one of the key financial statements used by businesses to assess their financial health and make informed decisions.

The balance sheet follows a basic accounting equation: assets = liabilities + shareholders’ equity. This equation reflects the fundamental principle that a company’s assets are financed by either debt or equity.

The balance sheet is divided into three main sections: assets, liabilities, and shareholders’ equity. Let’s take a closer look at each of these sections:

- Assets: Assets represent what a company owns and includes both tangible and intangible items. Tangible assets may include cash, inventory, property, and equipment, while intangible assets can include patents, trademarks, and goodwill. Assets are usually categorized as current assets (expected to be converted into cash within a year) or non-current assets (held for longer periods).

- Liabilities: Liabilities represent what a company owes to its creditors. This includes both short-term liabilities, such as accounts payable and short-term loans, and long-term liabilities, such as mortgages and bonds. Liabilities are obligations that the company must settle in the future.

- Shareholders’ Equity: Shareholders’ equity represents the residual interest in the company’s assets after deducting its liabilities. It is the ownership interest of the shareholders and includes the initial investment plus retained earnings. It shows how much of the company’s assets are funded by equity.

The balance sheet provides crucial information about a company’s financial position, including its liquidity, solvency, and ability to meet its financial obligations. By analyzing the balance sheet, investors can assess the company’s financial stability, evaluate its risk profile, and make informed investment decisions.

Purpose of a Balance Sheet

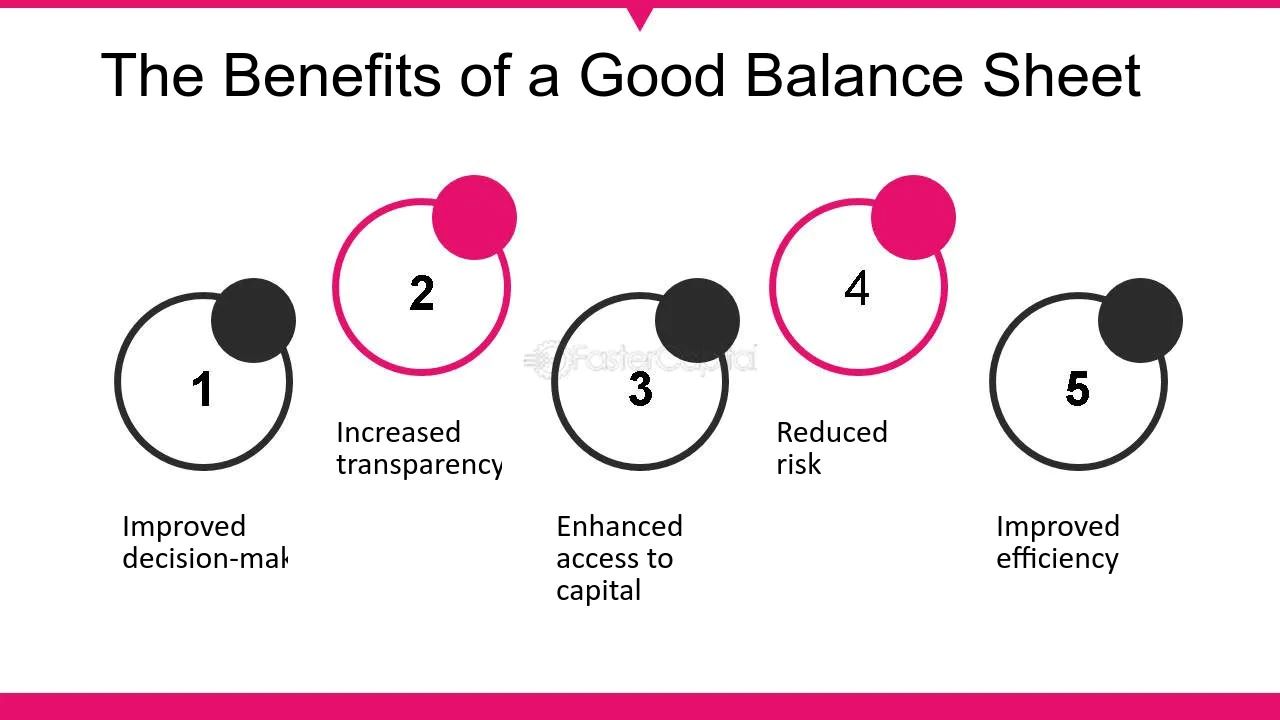

The balance sheet serves several important purposes in providing valuable insights into the financial health and performance of a company. Let’s explore some of the key purposes of a balance sheet:

- Financial Analysis: The primary purpose of a balance sheet is to enable financial analysis. By examining the assets, liabilities, and shareholders’ equity, investors and analysts can evaluate a company’s financial position and performance. It helps assess the company’s ability to generate profits, manage its debts, and allocate its resources effectively.

- Assessing Liquidity: The balance sheet provides information about a company’s liquidity, which refers to its ability to meet short-term obligations. By analyzing the ratio of current assets to current liabilities, investors can assess how easily a company can convert its assets into cash to settle its debts. This information is crucial in evaluating a company’s short-term financial health and ability to navigate through economic downturns.

- Evaluating Solvency: Solvency is the ability of a company to meet its long-term financial obligations. By examining the proportion of long-term liabilities to shareholders’ equity, investors can assess a company’s solvency and its ability to generate sufficient cash flows to repay its long-term debts.

- Assessing Financial Stability: The balance sheet helps investors gauge the overall financial stability of a company. By evaluating various financial ratios, such as the debt-to-equity ratio and the current ratio, investors can identify potential risks and assess the company’s ability to withstand financial shocks. A strong and stable balance sheet is indicative of a company’s financial health and resilience.

- Decision-Making: The balance sheet acts as a valuable tool for decision-making. Whether it’s assessing the financial feasibility of a new project, making investment decisions, or evaluating the financial health of potential business partners, the balance sheet provides crucial information to support informed decision-making.

Overall, the purpose of a balance sheet is to provide stakeholders with a comprehensive view of a company’s financial position and performance. It helps investors, lenders, and other stakeholders assess the company’s financial health, make informed decisions, and monitor its progress over time.

Components of a Balance Sheet

A balance sheet is composed of three main components: assets, liabilities, and shareholders’ equity. Each component provides a unique perspective on a company’s financial position and performance. Let’s explore these components in more detail:

- Assets: Assets represent what a company owns and include both tangible and intangible items. Tangible assets can include cash, inventory, property, and equipment, while intangible assets may include patents, trademarks, and goodwill. Assets are typically listed in order of liquidity, with the most liquid assets appearing first. This allows stakeholders to understand the company’s available resources and their ability to generate cash flows.

- Liabilities: Liabilities represent what a company owes to its creditors and are categorized as either current or non-current liabilities. Current liabilities are obligations that are expected to be settled within one year, such as accounts payable and short-term loans. Non-current liabilities, on the other hand, are long-term obligations, like mortgages and bonds, which are due beyond one year. Liabilities indicate the company’s financial obligations and its ability to meet them.

- Shareholders’ Equity: Shareholders’ equity represents the residual interest in the company’s assets after deducting its liabilities. It includes the initial investment made by shareholders as well as retained earnings. Retained earnings are accumulated profits that have not been distributed to the shareholders as dividends. Shareholders’ equity reflects the ownership stake of the shareholders and indicates the value that remains with them after satisfying the company’s liabilities.

Together, these components interact to maintain the balance sheet equation, where the total value of assets equals the total value of liabilities plus shareholders’ equity. This equation ensures that the accounting equation remains in balance, providing a reliable representation of a company’s financial position.

Moreover, the balance sheet allows stakeholders to assess the company’s financial position and make informed judgments about its liquidity, solvency, and overall stability. By analyzing the components of the balance sheet, investors and analysts can gain valuable insights into the company’s financial health, performance, and ability to generate returns.

Another Term for Balance Sheet

While the term “balance sheet” is widely used to refer to the financial statement that presents a company’s financial position, there are a few alternative terms that are occasionally used in financial discussions. These terms are often region-specific or are utilized in specific industries. Let’s explore some of the common alternate terms for a balance sheet:

- Statement of Financial Position: This term is commonly used in international accounting standards, such as International Financial Reporting Standards (IFRS). It represents a more descriptive name for the balance sheet, emphasizing its purpose of presenting the financial position of a company at a given point in time. The term “statement of financial position” is often favored in countries that have adopted IFRS.

- Position Statement: In some contexts, particularly within certain industries or professional circles, the term “position statement” may be used interchangeably with “balance sheet.” This term highlights the fact that the statement presents the financial position of a company, summarizing its assets, liabilities, and shareholders’ equity.

- Statement of Financial Condition: Similar to the statement of financial position, the term “statement of financial condition” emphasizes the purpose of the balance sheet, which is to provide an overview of a company’s financial status. This term is more commonly used in the United States.

- Statement of Assets and Liabilities: This term highlights the primary elements of a balance sheet – assets and liabilities. While it may be less commonly used, it accurately describes the content and purpose of the balance sheet by emphasizing the presentation of a company’s assets and liabilities.

It is important to note that while these alternate terms are occasionally used, “balance sheet” remains the most widely recognized and commonly used term across the finance and accounting industry. Regardless of the term used, the purpose and content of the financial statement remain the same – to provide a snapshot of a company’s financial position at a specific point in time.

Understanding these alternate terms can be helpful when reading financial reports or engaging in industry-specific discussions where these terms may be used interchangeably. However, it is crucial to have a solid grasp of the underlying concepts and components of a balance sheet to effectively interpret and analyze financial information.

Conclusion

In conclusion, the balance sheet is a vital financial statement that provides a snapshot of a company’s financial position at a specific point in time. It consists of three main components – assets, liabilities, and shareholders’ equity – which collectively represent the financial health and performance of the company.

The balance sheet serves several important purposes, including financial analysis, assessing liquidity and solvency, evaluating financial stability, and supporting decision-making. It helps investors and stakeholders gain a comprehensive understanding of a company’s financial status and make informed decisions.

While the term “balance sheet” is the most commonly used term worldwide, alternate terms like “statement of financial position,” “position statement,” “statement of financial condition,” and “statement of assets and liabilities” are occasionally used in specific contexts or industries.

Having a solid understanding of the balance sheet and its components is crucial for investors, analysts, and finance professionals. It enables them to assess a company’s financial health, evaluate its performance, and make informed decisions regarding investments, loans, and partnerships.

By being familiar with the alternative terms for a balance sheet, individuals can engage in discussions, understand various reporting standards, and effectively interpret financial information from different sources.

In conclusion, the balance sheet remains a cornerstone in financial reporting, providing valuable insights into a company’s financial position and enabling stakeholders to make well-informed decisions based on a comprehensive understanding of its financial health.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance