Home>Finance>How To Report PPP Loan Forgiveness On An 1120 Tax Return

Finance

How To Report PPP Loan Forgiveness On An 1120 Tax Return

Published: October 29, 2023

Learn how to properly report PPP loan forgiveness on an 1120 tax return, ensuring compliance with finance regulations. Simplify your filing process with expert guidance.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

- Introduction

- Step 1: Gathering the necessary documents

- Step 2: Calculating the forgiven amount

- Step 3: Reporting the forgiven amount on Schedule K of Form 1120

- Step 4: Completing Form 1099-CAP

- Step 5: Reporting any retained loan amount as income

- Step 6: Submitting the tax return and supporting documentation

- Conclusion

Introduction

The Paycheck Protection Program (PPP) has provided much-needed financial relief to businesses affected by the COVID-19 pandemic. As part of the program, small businesses and eligible organizations were able to apply for loans to cover payroll and other essential expenses. One of the key benefits of the PPP is the potential for loan forgiveness, allowing borrowers to have a portion, or in some cases, the full amount of the loan forgiven. However, it is important for businesses to understand the process of reporting PPP loan forgiveness on their tax returns to ensure compliance with IRS regulations.

In this article, we will guide you through the necessary steps to report PPP loan forgiveness on an 1120 tax return. By following these steps, you can accurately report your forgiven loan amount and fulfill your tax obligations.

Before we delve into the reporting process, it is crucial to note that tax laws and guidance surrounding PPP loans and loan forgiveness are subject to change. It is highly recommended that you consult with a qualified tax professional or reference the most up-to-date IRS guidelines to ensure compliance with current regulations.

Now, let’s get started with Step 1: Gathering the necessary documents.

Step 1: Gathering the necessary documents

Before you begin the process of reporting PPP loan forgiveness on your 1120 tax return, it’s crucial to gather all the required documentation. These documents will provide the necessary evidence to support your loan forgiveness application and accurately report the forgiven amount on your tax return. Here are the key documents you will need:

- PPP loan forgiveness application: Start by obtaining a copy of the PPP loan forgiveness application. This application will provide detailed instructions on how to calculate your forgiven amount and what supporting documentation you need to provide. Each application has a unique form number, so make sure you have the correct application for your loan.

- Payroll records: Gather payroll records for the period covered by the loan. This includes documents such as payroll registers, employee tax forms (W-2 or 1099), and payroll tax filings (Form 941).

- Eligible expense receipts: If you used a portion of the loan for eligible expenses like rent, utilities, and mortgage interest, gather supporting documentation such as receipts, invoices, and lease agreements.

- Bank statements: Collect bank statements for the period covered by the loan. These statements should clearly show the deposits and withdrawals related to the PPP loan.

- Other relevant financial records: Depending on your business’s specific circumstances, you may need additional financial records to support your loan forgiveness application. Examples include utility bills, mortgage statements, and invoices for business-related expenses.

It’s important to ensure that all documents are accurate, complete, and organized. Having a well-organized file containing the necessary documentation will make the reporting process much smoother and reduce the chances of errors or omissions.

Once you have gathered all the required documents, you can proceed to the next step: calculating the forgiven amount.

Step 2: Calculating the forgiven amount

Calculating the forgiven amount is a critical step in reporting PPP loan forgiveness on your 1120 tax return. The forgiven amount represents the portion of the loan that you do not need to repay, and it is determined by several factors outlined in the PPP loan forgiveness application. Here’s how you can calculate the forgiven amount:

- Determine eligible expenses: Review the PPP loan forgiveness application to identify the eligible expenses that qualify for forgiveness. These typically include payroll costs, rent or lease payments, utility payments, and mortgage interest payments.

- Calculate the payroll cost limitation: If you used at least 60% of the loan amount for payroll costs, you can skip this step. However, if less than 60% was used for payroll costs, you will need to calculate the payroll cost limitation. Multiply the total loan amount by 60% to determine the minimum amount that must be used for payroll costs.

- Consider reductions: Take into account any reductions in the forgiven amount due to salary or wage reductions and Full-Time Equivalent (FTE) employee reductions. These reductions can impact the final forgiven amount, so be sure to carefully follow the instructions provided in the forgiveness application.

- Apply the 25% non-payroll cost limitation: If applicable, apply the 25% limitation on non-payroll costs. This means that non-payroll expenses cannot exceed 25% of the total forgiven amount. If your non-payroll costs exceed this limit, the excess amount will not be forgiven.

- Calculate the final forgiven amount: After considering all the factors mentioned above, calculate the final forgiven amount by subtracting any reductions and limitations from the eligible expenses. This will give you the total amount that can be reported as forgiven on your tax return.

It is crucial to carefully follow the guidelines provided in the PPP loan forgiveness application to ensure accurate calculations. If you have any doubts or uncertainties, consult with a qualified tax professional or refer to the most up-to-date IRS guidelines for clarification.

Once you have calculated the forgiven amount, you can move on to Step 3: Reporting the forgiven amount on Schedule K of Form 1120.

Step 3: Reporting the forgiven amount on Schedule K of Form 1120

Once you have calculated the forgiven amount, it’s time to report it on your 1120 tax return. The forgiven amount should be reported on Schedule K, which is used to report the company’s income, deductions, and credits. Here’s how you can report the forgiven amount:

- Complete Schedule K: Start by filling out Schedule K of Form 1120. Schedule K contains several sections, including lines for ordinary business income, deductions, and credits.

- Locate line 11: On Schedule K, locate line 11, which is labeled “Other income (loss) – net.” This is the line where you will report the forgiven amount.

- Enter the forgiven amount: Write the total forgiven amount in parentheses on line 11. This indicates that it is a negative amount and represents a reduction in the company’s income. Include a brief description next to the amount, such as “PPP loan forgiveness.”

- Attach supporting documentation: To support the reporting of the forgiven amount, attach the necessary documentation, such as the PPP loan forgiveness application and any applicable worksheets or calculations, to your tax return. This will serve as evidence to substantiate the reported amount.

Remember to follow the IRS guidelines and instructions for Schedule K to ensure accurate reporting. Double-check all the information entered on the form, and make sure it aligns with your calculated forgiven amount.

After reporting the forgiven amount on Schedule K, you can proceed to Step 4: completing Form 1099-CAP.

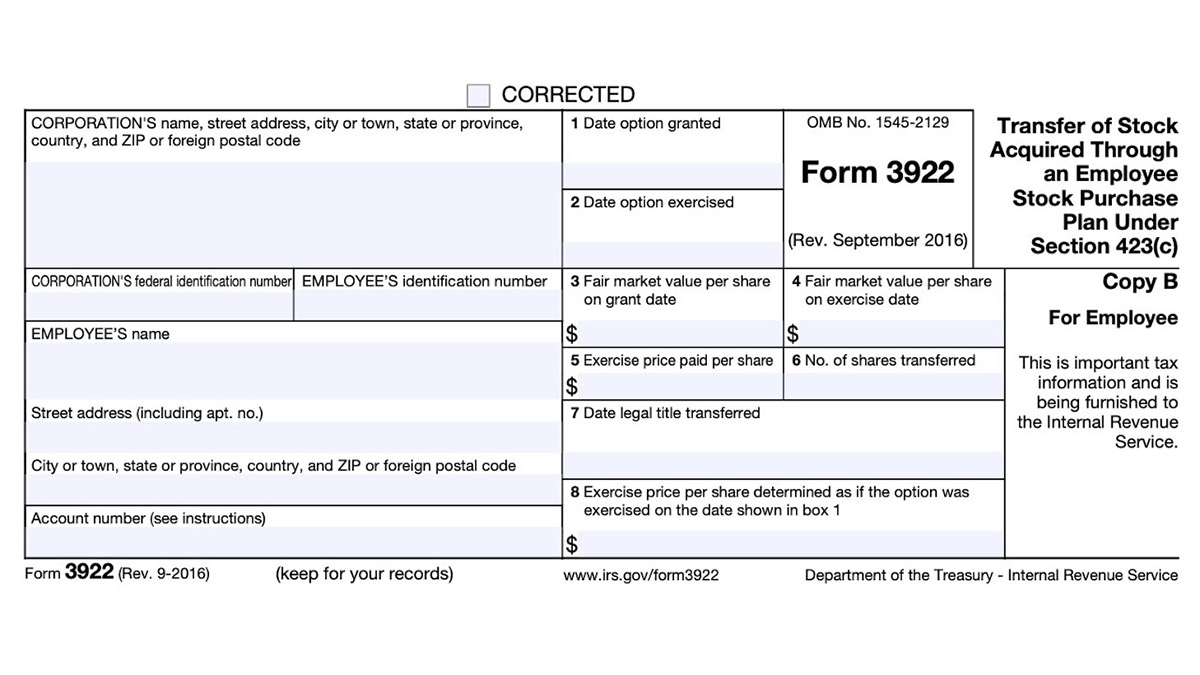

Step 4: Completing Form 1099-CAP

Completing Form 1099-CAP is an important step in the process of reporting PPP loan forgiveness on your 1120 tax return. Form 1099-CAP is used to report changes in corporate control and capital structure, including the cancellation of debt. Here’s how you can complete Form 1099-CAP:

- Obtain Form 1099-CAP: Start by obtaining a copy of Form 1099-CAP from the IRS website or by contacting the IRS directly. Make sure you have the most recent version of the form.

- Provide the necessary information: Fill in the required information on the form, including your business’s name, address, and tax identification number (TIN).

- Enter the creditor’s information: Provide the creditor’s information, including their name, address, and TIN. The creditor in this case would be the lender who provided the PPP loan.

- Report the canceled debt: Report the canceled debt amount in Box 2 of Form 1099-CAP. This is the amount of the PPP loan that has been forgiven and does not need to be repaid.

- Add a description: Include a brief description in Box 3 of Form 1099-CAP, specifying that the canceled debt relates to PPP loan forgiveness.

- Attach supporting documentation: Attach a copy of the PPP loan forgiveness application and any additional documentation requested by the IRS to support the reported forgiven amount.

Remember to carefully review all the information entered on Form 1099-CAP for accuracy. Any errors or omissions could lead to potential issues with your tax return. It’s also recommended to consult with a tax professional or refer to the IRS instructions for Form 1099-CAP to ensure compliance with the latest guidelines.

After completing Form 1099-CAP, you can move on to Step 5: reporting any retained loan amount as income.

Step 5: Reporting any retained loan amount as income

While a portion of your PPP loan may have been forgiven, it’s important to note that any retained loan amount that was not forgiven should be reported as income on your 1120 tax return. Reporting this retained loan amount as income ensures compliance with IRS regulations. Here’s how you can report the retained loan amount:

- Identify the retained loan amount: Calculate the portion of the PPP loan that was not forgiven, also known as the retained loan amount. This is the remaining balance that you must repay.

- Report the retained loan amount: Include the retained loan amount as income on your 1120 tax return. On Schedule K, line 1 (Ordinary business income (loss)), add the retained loan amount in parentheses as a positive value. This indicates that it is an addition to the company’s income.

- Provide supporting documentation: To substantiate the reporting of the retained loan amount as income, attach any relevant documentation, such as bank statements or loan statements, to your tax return. This will serve as evidence of the outstanding loan balance.

It’s important to accurately report the retained loan amount as income to avoid any potential tax penalties or issues with the IRS. If you’re unsure about the reporting process or have questions about tax implications related to the retained loan amount, it’s advisable to consult with a qualified tax professional.

After reporting the retained loan amount as income, you can proceed to Step 6: submitting the tax return and supporting documentation.

Step 6: Submitting the tax return and supporting documentation

After completing all the necessary steps to report PPP loan forgiveness on your 1120 tax return, it’s time to submit your tax return and the supporting documentation. Here’s how you can ensure a smooth submission process:

- Review your tax return: Before submitting your tax return, carefully review all the information entered and make sure it is accurate. Double-check the reported forgiven amount, the retained loan amount reported as income, and any other relevant details.

- Compile supporting documentation: Gather all the required supporting documentation related to PPP loan forgiveness. This includes the PPP loan forgiveness application, Form 1099-CAP, bank statements, payroll records, eligible expense receipts, and any other documentation that supports the calculations and reporting of the forgiven amount and retained loan amount.

- Attach the supporting documentation: Include the necessary supporting documentation with your tax return. Attach copies of the documentation to ensure that you have a complete record of the process and can provide evidence if requested by the IRS.

- File your tax return: Submit your tax return, along with the supporting documentation, by the applicable deadline. Ensure that you are using the correct filing method, whether it’s paper filing or electronic filing, depending on the requirements and options available to you.

It’s crucial to keep a copy of your filed tax return and all supporting documentation for your records. These documents serve as evidence of your compliance with IRS guidelines and can be useful if any questions or audits arise in the future.

Remember that tax rules and regulations are subject to change, so it’s essential to stay updated with any revisions or updates from the IRS. If you have any concerns or questions about the submission process, it’s advisable to consult with a qualified tax professional to ensure accuracy and compliance.

With Step 6 complete, you have successfully reported your PPP loan forgiveness on your 1120 tax return. By following these steps and fulfilling your tax obligations, you can enjoy the benefits of PPP loan forgiveness while complying with IRS guidelines.

Concluding this process, make sure to keep a record of your communication with the IRS and the documents submitted, as they are essential for future reference and potential audits.

Remember to consult with a qualified tax professional for personalized guidance tailored to your specific business circumstances to ensure compliance with current regulations and maximize your tax benefits.

Best of luck with your reporting process!

Conclusion

Reporting PPP loan forgiveness on an 1120 tax return requires careful attention to detail and adherence to IRS guidelines. By following the steps outlined in this article, you can accurately report your forgiven loan amount, retain the necessary documentation, and fulfill your tax obligations.

Remember, tax laws and regulations surrounding PPP loans and loan forgiveness can evolve, so it’s crucial to stay updated with the latest IRS guidance or consult with a qualified tax professional. They can provide personalized advice tailored to your specific business situation and ensure compliance with current regulations.

Gathering the necessary documents, calculating the forgiven amount, reporting it on Schedule K, completing Form 1099-CAP, reporting the retained loan amount as income, and submitting your tax return with supporting documentation are all integral steps in properly reporting PPP loan forgiveness.

By accurately reporting your forgiven loan amount and any retained loan amount as income, you can maintain compliance with IRS regulations and avoid potential penalties or issues with the IRS in the future.

Remember to keep copies of all documentation submitted with your tax return for your records. These records will serve as evidence of your compliance and can be useful in the event of an audit or future questions from the IRS.

As always, if you have any questions or concerns during the reporting process, it’s recommended to consult with a qualified tax professional. They can provide guidance tailored to your unique circumstances and ensure that you navigate the reporting process accurately and in compliance with IRS guidelines.

Reporting PPP loan forgiveness can be a complex process, but with the right knowledge and attention to detail, you can successfully navigate through it and enjoy the benefits of loan forgiveness while managing your tax obligations.

Remember to stay informed about any changes or updates to IRS regulations and guidelines to ensure accurate reporting. With proper reporting, you can confidently move forward in the financial recovery of your business.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance