Finance

Retirement Planning: How Much Do I Need

Published: January 21, 2024

Discover how to plan for retirement and determine how much money you need. Get expert finance advice to ensure a secure future.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

- Introduction

- Importance of Retirement Planning

- Factors to Consider in Retirement Planning

- Estimating Your Retirement Expenses

- Determining Your Retirement Income

- Calculating Your Retirement Savings Goal

- Strategies for Achieving Your Retirement Savings Goal

- Understanding Different Retirement Accounts

- Adjusting for Inflation and Longevity

- Evaluating Your Retirement Plan Regularly

- Conclusion

Introduction

Retirement is a significant phase of life that requires careful planning to ensure financial security and stability. However, many individuals often underestimate the importance of retirement planning or delay starting the process. By taking the time to create a comprehensive retirement plan, you can have peace of mind knowing that your future is secured.

Retirement planning involves assessing your future financial needs, estimating expenses, determining sources of income, and setting a savings goal to achieve your desired lifestyle after retirement. While it may seem daunting, proper planning can provide you with the freedom to enjoy your retirement years without financial stress.

In this article, we will explore the key factors to consider in retirement planning, including estimating your retirement expenses, determining your retirement income, calculating your savings goal, and implementing strategies to achieve it. We will also discuss different retirement accounts, considerations for inflation and longevity, and the importance of regularly evaluating and adjusting your retirement plan.

Whether you are just starting your career or approaching retirement age, it’s never too early or too late to start planning for your retirement. The sooner you begin, the more time you have to build a solid financial foundation and make the necessary adjustments along the way.

So, let’s delve into the world of retirement planning and explore the steps you can take to secure a financially stable and fulfilling retirement.

Importance of Retirement Planning

Retirement planning is an essential aspect of financial management that ensures a comfortable and worry-free post-work life. It involves making strategic decisions and taking necessary actions to secure adequate funds to cover living expenses and achieve personal goals during retirement.

One of the primary reasons retirement planning is crucial is the changing landscape of pension systems. Traditional pension plans provided by employers are becoming less common, placing the responsibility of retirement savings squarely on the individual’s shoulders. Without proper planning and proactiveness, individuals risk facing financial hardships during their later years.

Moreover, as life expectancies continue to rise, retirement periods are getting longer, increasing the need for sufficient savings to maintain a desired lifestyle. It’s not uncommon for individuals to spend 20-30 years or more in retirement, requiring a substantial nest egg to support their living expenses over such an extended duration.

Retirement planning also enables individuals to maintain their independence and freedom. By securing adequate savings, individuals can choose to retire at the desired age and pursue activities that bring them joy and fulfillment. It provides the opportunity to travel, spend time with loved ones, engage in hobbies, or even start a new business venture without financial constraints.

Another important aspect of retirement planning is safeguarding against unforeseen circumstances. Life is unpredictable, and unexpected events such as health issues, accidents, or economic downturns can significantly impact an individual’s finances. By having a retirement plan in place, individuals can better navigate these challenges and ensure they have a safety net to fall back on.

Additionally, retirement planning enables individuals to leave a legacy for their loved ones. By carefully managing their finances and assets, individuals can plan for the distribution of their wealth, ensuring that their heirs are taken care of and their wishes are upheld.

By prioritizing retirement planning, individuals can make informed financial decisions throughout their lives, ensuring that their hard-earned money is working for them. It provides a roadmap for achieving financial security and peace of mind during the retirement years.

In the following sections, we will delve into the factors to consider when planning for retirement, helping you make informed decisions and set realistic goals to achieve a comfortable and fulfilling retirement lifestyle.

Factors to Consider in Retirement Planning

Retirement planning involves a careful evaluation of various factors that can impact your financial well-being during your post-work years. By considering these factors, you can make informed decisions and create a solid retirement plan. Here are some key factors to consider:

- Age of Retirement: The age at which you plan to retire plays a crucial role in determining your retirement savings goal. Starting early allows you to take advantage of compounding interest and build a larger nest egg. However, if you plan to retire earlier, you may need to save more aggressively to account for the shorter time frame.

- Life Expectancy: Estimating your life expectancy is essential in determining how long your retirement savings need to last. Factors such as family history, lifestyle, and overall health can influence your projected lifespan. It’s wise to plan for a longer retirement period to ensure you have enough funds to sustain your lifestyle.

- Current Expenses: Analyzing your current expenses is a critical step in estimating your future retirement expenses. Take into account your housing costs, healthcare expenses, insurance premiums, transportation, groceries, and any other regular expenditures. It’s essential to be realistic and factor in potential changes in expenses during retirement.

- Inflation: Inflation erodes the purchasing power of money over time. When planning for retirement, it’s important to consider inflation and its potential impact on your expenses. Assume a conservative inflation rate to ensure your savings can keep up with the rising cost of living.

- Healthcare Costs: Healthcare expenses tend to increase as individuals age. Factoring in potential healthcare costs, including insurance premiums, prescription medications, and long-term care, is essential to avoid financial strain in retirement. Consider the potential need for Medicare or supplementary health insurance.

- Social Security Benefits: Understand how Social Security benefits will contribute to your retirement income. Familiarize yourself with the eligibility criteria, projected benefits based on your earnings history, and the potential impact of claiming benefits early or delaying them. Incorporate these benefits into your retirement income plan.

- Investment Strategy: Your investment strategy can significantly impact the growth and sustainability of your retirement savings. Consider your risk tolerance, diversification, asset allocation, and investment vehicles such as Individual Retirement Accounts (IRAs) or 401(k)s. A well-balanced and diversified investment portfolio can help mitigate risks and maximize returns.

- Debt Management: Managing and reducing debt before retirement is crucial. High-interest debt, such as credit cards or personal loans, can strain your retirement income. Prioritize paying off debts and consider strategies to minimize or eliminate debt before entering retirement.

These factors provide a foundation for retirement planning and highlight the importance of considering various aspects of your financial situation. By addressing these factors, you can create a more accurate retirement plan and set achievable goals that align with your desired lifestyle.

Estimating Your Retirement Expenses

When planning for retirement, it is crucial to have a clear understanding of your estimated expenses during your post-work years. By accurately estimating your retirement expenses, you can determine the amount of savings required to maintain your desired lifestyle. Here are some key factors to consider when estimating your retirement expenses:

- Basic Living Expenses: Start by calculating the essential expenses you need to cover in retirement. This includes housing costs (mortgage/rent, property taxes, utilities), food, transportation, healthcare, and insurance premiums. Take into account any changes in these expenses, such as downsizing your home or reducing transportation costs.

- Healthcare Costs: Healthcare expenses tend to increase with age, making them a significant consideration in retirement planning. Research the potential costs of Medicare premiums, deductibles, and copayments, as well as the need for supplemental health insurance. Consider long-term care insurance, as the need for assisted living or nursing care can be financially draining.

- Travel and Leisure: Retirement is often a time when individuals want to enjoy their freedom and pursue travel and leisure activities. Consider the cost of vacations, hobbies, dining out, and entertainment. Factor in any bucket-list experiences or special events you wish to participate in during retirement.

- Debts and Loans: Ideally, you should aim to pay off high-interest debts, such as credit cards or personal loans, before entering retirement. However, if you have ongoing debts, determine the monthly payments and include them in your estimate. Be mindful of loan terms and interest rates that may affect your retirement budget.

- Home Maintenance and Repairs: As a homeowner, it’s important to consider the cost of ongoing maintenance and repairs for your property. Budget for routine maintenance, such as landscaping or appliance replacements, as well as unexpected repairs that may arise.

- Charitable and Family Support: If contributing to charitable causes or providing financial assistance to family members is important to you, allocate funds in your retirement budget. Consider any regular or one-time contributions you wish to make and plan accordingly.

- Inflation: Inflation erodes the purchasing power of money over time. Factor in a reasonable inflation rate when estimating your expenses to ensure that your retirement savings can keep pace with the rising cost of living.

Estimating your retirement expenses may require some research and careful evaluation of your current lifestyle and anticipated future needs. It’s essential to be thorough and realistic in order to create a comprehensive retirement budget. Consider consulting with a financial advisor who specializes in retirement planning to ensure all aspects of your expenses are adequately accounted for.

By accurately estimating your retirement expenses, you can develop a realistic savings goal to work towards and make informed decisions regarding your retirement income sources and investment strategies.

Determining Your Retirement Income

When planning for retirement, one of the crucial steps is determining your sources of income during your post-work years. Having a clear understanding of your retirement income can help you create a sustainable financial plan. Here are some key factors to consider when determining your retirement income:

- Social Security: Social Security benefits can be a significant source of income for retirees. To determine your estimated Social Security income, review your earnings history and consult the Social Security Administration’s website or speak with a representative. Consider the impact of claiming benefits early versus delaying them to maximize your monthly payments.

- Pension Plans: If you are fortunate enough to have an employer-sponsored pension plan, determine the amount you will receive in retirement. Review your pension plan documents or consult with your employer’s HR department for specific details. Take into account factors such as years of service and retirement age eligibility.

- Investment Income: Evaluate the income generated from your investment portfolio. This can include dividends from stocks, interest from bonds or savings accounts, and rental income from real estate investments. Consider working with a financial advisor to assess the potential income your investments can generate in retirement.

- Retirement Accounts: Determine the income you can expect from your retirement accounts, such as Individual Retirement Accounts (IRAs) or 401(k)s. Calculate the required minimum distributions (RMDs) as mandated by the IRS once you reach a certain age. Assess the withdrawal strategies that align with your financial goals and tax considerations.

- Part-Time Work: Consider the option of working part-time during retirement to supplement your income. Assess the potential income you can earn from part-time work and factor it into your overall retirement income plan. Plan for flexibility in case you decide to continue working on a part-time basis.

- Income from Other Sources: Assess any additional sources of income you may have, such as rental properties, royalties, or annuities. Factor in any expected income from inheritances or the sale of assets to determine how they contribute to your retirement income.

When determining your retirement income, it is important to be realistic and conservative in your estimates. Consider potential market fluctuations, tax implications, and any changes that may occur in your circumstances. It may be helpful to consult with a financial advisor to ensure all sources of income are accurately assessed and optimized.

By gainfully understanding your retirement income sources, you can develop a comprehensive retirement plan that balances your expenses, savings goals, and desired lifestyle. This will provide you with the financial security and peace of mind to enjoy your retirement years to the fullest.

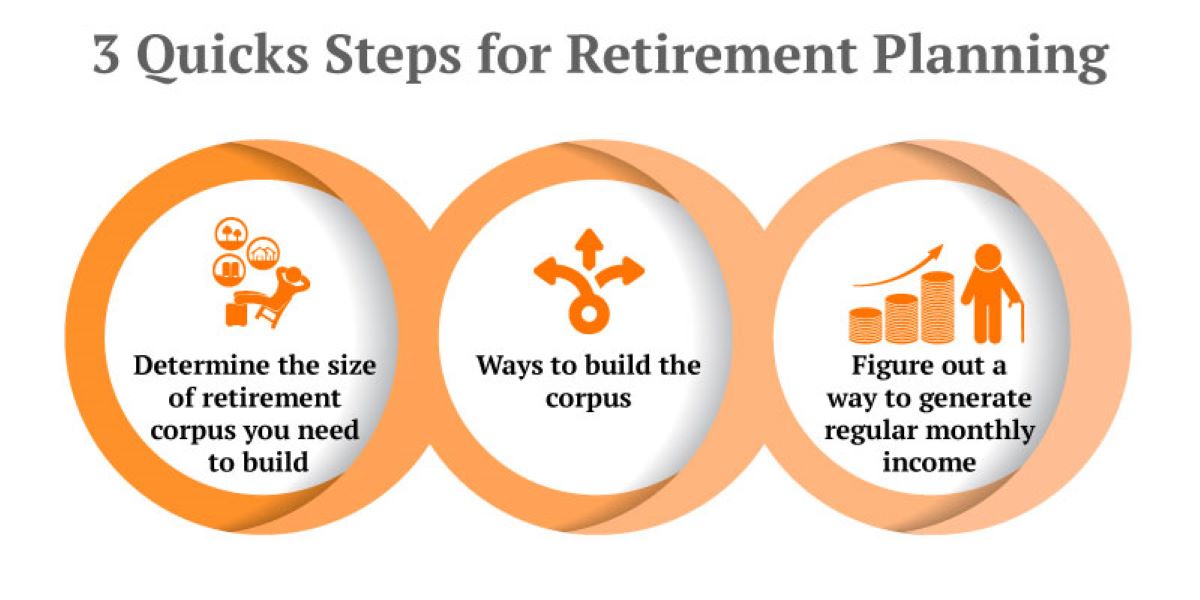

Calculating Your Retirement Savings Goal

Calculating your retirement savings goal is a critical step in retirement planning, as it helps determine the amount of money you need to save to maintain your desired lifestyle throughout your post-work years. While the specific formula can vary based on individual circumstances, here are some key factors to consider when calculating your retirement savings goal:

- Estimate Your Retirement Expenses: Begin by estimating your retirement expenses, as we discussed in a previous section. Consider your current expenses, potential changes in expenses during retirement, and any specific goals or aspirations you have for your retirement lifestyle.

- Consider Your Retirement Age: Determine the age at which you plan to retire. This will affect the number of years you will need to rely on your retirement savings and the potential growth or depletion of those savings over time.

- Factor in Life Expectancy: Estimate your life expectancy to ensure your retirement savings will last throughout your post-work years. Consider your family history, current health, and lifestyle factors that may impact your projected lifespan.

- Account for Inflation: Factor in the impact of inflation on your retirement expenses. Assume a conservative inflation rate to ensure your savings can keep up with the rising cost of living over time.

- Evaluate Potential Income Sources: Assess the potential income you will receive from sources such as Social Security benefits, pension plans, and investment income. This will help determine the gap between your estimated expenses and your available income.

- Calculate the Savings Gap: Subtract your estimated retirement income from your projected retirement expenses to determine the amount of savings you need to accumulate. This is often referred to as the savings gap or the shortfall you need to fill with your own savings.

- Consider Investment Returns: Take into account the potential returns on your investments. Assess the growth rate and risk tolerance of your portfolio to determine a reasonable rate of return. This will help you determine how much you need to save each year to achieve your retirement savings goal.

- Implement Regular Contributions: Determine the amount you can contribute on a regular basis to your retirement savings. Set up a budget that allows for consistent contributions to gradually build your nest egg over time.

- Reevaluate and Adjust: Regularly review and adjust your retirement savings goal as your circumstances change. Factors such as unexpected expenses, changes in income, or shifting market conditions may require reassessment and modification of your savings strategy.

It’s important to note that calculating your retirement savings goal is not an exact science, and future needs and circumstances can be unpredictable. Working with a financial advisor can provide valuable insights and guidance in determining a realistic savings goal and developing a customized retirement plan.

By calculating your retirement savings goal, you can set tangible objectives, make informed decisions, and work towards building a robust financial foundation for a secure and fulfilling retirement.

Strategies for Achieving Your Retirement Savings Goal

Once you have calculated your retirement savings goal, the next step is to implement strategies to help you achieve it. Here are some effective strategies to consider:

- Start Saving Early: The power of compounding interest means that the earlier you start saving for retirement, the more time your money has to grow. Even small contributions made consistently over a long period can accumulate into a significant retirement fund.

- Set a Realistic Budget: Create a budget that focuses on your retirement savings goal. Identify areas where you can cut back on unnecessary expenses and redirect those funds towards your retirement savings. Be disciplined with your spending and prioritize long-term financial security over short-term gratification.

- Maximize Retirement Account Contributions: Take full advantage of tax-advantaged retirement accounts, such as IRAs and 401(k)s. Contribute as much as you can, aiming to maximize your annual contributions. These accounts offer tax benefits and can help accelerate your savings growth.

- Consider Employer Matching Contributions: If your employer offers a matching contribution on your retirement plan, make sure you contribute enough to receive the maximum match. This is essentially free money that can significantly boost your retirement savings.

- Automate Your Savings: Set up automatic contributions to your retirement accounts. By automating your savings, you ensure consistent contributions without relying on manual effort or discipline. Treat your retirement savings as a non-negotiable expense each month.

- Diversify Your Investments: Diversification is key to managing risk and maximizing returns. Spread your investments across different asset classes, such as stocks, bonds, and real estate. This can help protect your savings from market volatility and potentially increase your long-term gains.

- Monitor and Rebalance Your Portfolio: Regularly review your investment portfolio to ensure it aligns with your goals and risk tolerance. Rebalance as necessary to maintain an appropriate asset allocation. Consult with a financial advisor if needed to optimize your investment strategy.

- Consider Delaying Retirement: If possible, consider delaying your retirement age. Working for a few extra years can provide additional time to save, maximize Social Security benefits, and reduce the number of years your savings need to support your retirement lifestyle.

- Manage Debt: Prioritize debt management and aim to pay off high-interest debts as soon as possible. Reducing or eliminating debt before entering retirement can free up more funds to allocate towards your retirement savings.

- Stay Informed and Educated: Stay updated on retirement planning strategies, tax laws, and investment practices. Attend workshops, read books or articles, and consult with financial professionals to ensure you are making informed decisions and staying on track with your retirement savings goals.

Adopting these strategies and maintaining consistency and discipline will position you for success in achieving your retirement savings goal. Remember, it’s never too late to start saving for retirement, so take action today and create a roadmap towards a financially secure future.

Understanding Different Retirement Accounts

When planning for retirement, it’s important to have a good understanding of the different types of retirement accounts available to you. These accounts provide various tax advantages and investment options that can help you grow and manage your retirement savings. Here are some common retirement accounts to consider:

- Individual Retirement Accounts (IRAs): IRAs are personal retirement accounts that allow individuals to make tax-deductible contributions (in the case of Traditional IRAs) or contribute after-tax income (in the case of Roth IRAs). Earnings in these accounts grow tax-deferred or tax-free, respectively, and withdrawals are generally subject to income tax in retirement.

- 401(k) Plans: These employer-sponsored retirement plans allow employees to contribute a portion of their salary to a retirement account on a pre-tax basis. Some employers also offer matching contributions. Contributions to a 401(k) are tax-deferred until withdrawn, typically in retirement.

- 403(b) Plans: Similar to 401(k) plans, 403(b) plans are retirement accounts available to employees of certain nonprofit organizations, schools, and government organizations. Contributions are made on a pre-tax basis, and earnings grow tax-deferred until withdrawal.

- 457 Plans: These retirement plans are available to employees of state and local governments and certain nonprofit organizations. Contributions to 457 plans can be made on a pre-tax or post-tax basis, and the earnings grow tax-deferred until withdrawal.

- SIMPLE IRA: The Savings Incentive Match Plan for Employees (SIMPLE) IRA is an employer-sponsored retirement plan for small businesses with 100 or fewer employees. Employers contribute to their employees’ accounts, and employees can make their own contributions on a pre-tax basis.

- Solo 401(k): Designed for self-employed individuals or small business owners with no employees other than their spouse, a Solo 401(k) allows higher contribution limits than traditional 401(k)s. It offers both employer and employee contributions.

- SEP IRA: The Simplified Employee Pension (SEP) IRA is a retirement plan for self-employed individuals and small business owners. Contributions are made by the employer only and are tax-deductible.

Each type of retirement account has its own set of eligibility requirements, contribution limits, and withdrawal rules. It’s essential to familiarize yourself with the specifics of each account and determine which ones align with your financial goals and circumstances. Consider consulting with a financial advisor or tax professional who can provide guidance tailored to your specific needs.

Understanding the different retirement accounts available to you enables you to take advantage of their tax benefits, maximize contributions, and make informed decisions when it comes to managing and investing your retirement savings.

Adjusting for Inflation and Longevity

When planning for retirement, it’s crucial to account for inflation and longevity to ensure that your savings will be sufficient to cover your expenses throughout your post-work years. Failing to consider these factors can result in a significant erosion of purchasing power and a potential shortfall in your retirement funds. Here’s what you need to know:

Inflation:

Inflation refers to the gradual increase in the cost of goods and services over time. As inflation occurs, the purchasing power of your money decreases. To adjust your retirement savings for inflation, it’s important to assume a reasonable rate of inflation and factor it into your financial projections. While it is impossible to predict future inflation rates, a common rule of thumb is to assume an average annual inflation rate of around 2-3%. By accounting for inflation, you can ensure that your savings will be able to handle the rising cost of living during your retirement years.

Longevity:

Life expectancies have been steadily increasing, which means that planning for a longer retirement period has become increasingly important. When estimating how long your retirement savings need to last, it’s essential to consider your individual life expectancy. Factors such as family history, lifestyle choices, and overall health can influence your longevity. It’s prudent to plan for a longer retirement duration than expected to avoid outliving your savings. By being prepared for a longer retirement, you can ensure that your funds will be sufficient to cover your living expenses throughout your post-work years.

Strategies to Adjust for Inflation and Longevity:

- Invest in assets that have historically outpaced inflation, such as stocks or real estate. These investments have the potential to provide higher returns over the long term and can act as a hedge against inflation.

- Consider purchasing inflation-protected securities like Treasury Inflation-Protected Securities (TIPS) to help safeguard your retirement savings from inflationary pressures.

- Regularly review and adjust your retirement plan to account for changes in living expenses, inflation rates, and investment performance.

- Consider purchasing longevity insurance, an annuity product that provides guaranteed income starting at a predetermined age to protect against the risk of outliving your savings.

- Stay informed about economic trends, market conditions, and retirement planning strategies to proactively manage your retirement savings and adjust your plans as needed.

By adjusting for inflation and longevity, you can ensure that your retirement savings are protected against the impact of rising prices and provide for a longer retirement period. Remember, it’s essential to regularly review and adjust your retirement plan to keep it in line with your evolving financial situation and goals.

Evaluating Your Retirement Plan Regularly

Creating a retirement plan is not a one-time activity; it requires regular evaluation and adjustments to ensure that it remains on track to meet your financial goals. Evaluating your retirement plan regularly allows you to assess the progress you’ve made, make necessary tweaks, and stay proactive in your financial management. Here are some key reasons why regular evaluation is crucial:

Monitoring Progress:

By evaluating your retirement plan regularly, you can track the progress you’ve made towards your savings goals. This includes reviewing the growth of your investments, contributions to retirement accounts, and any adjustments you’ve made to your savings strategy. Regular monitoring helps you stay aware of your financial status and motivates you to stay on track with your retirement savings.

Responding to Life Changes:

Life is full of unexpected events and changes, such as marriage, having children, career advancements, or health issues. Regularly evaluating your retirement plan allows you to reassess and adjust your savings and investment strategy to accommodate these changes. This ensures that your plan remains aligned with your evolving circumstances and helps you make the necessary adjustments to stay on course for your retirement goals.

Investment Performance:

Regular evaluation of your retirement plan provides an opportunity to assess the performance of your investment portfolio. Analyze the performance of your individual investments, asset allocation, and overall return on investment. Consider rebalancing your portfolio if it deviates significantly from your target asset allocation or if certain investments underperform. This allows you to optimize your investments and potentially maximize your returns.

Adjusting for Economic Conditions:

The economic landscape is constantly changing, with fluctuations in interest rates, inflation rates, and market conditions. Regular evaluation of your retirement plan allows you to take into account these economic factors and adjust your strategies accordingly. For instance, during periods of high inflation, you may need to increase your savings goal or explore different investment options to protect your purchasing power.

Retirement Lifestyle Considerations:

As you approach retirement, your desired lifestyle and goals may change. Regular evaluation enables you to align your retirement plan with your evolving aspirations. Assess whether your savings and investment strategies can support the retirement lifestyle you envision. Consider any adjustments needed to ensure you have enough funds to fulfill your retirement dreams.

To conduct a comprehensive evaluation of your retirement plan:

- Review your savings progress and compare it with your intended goals.

- Assess the performance of your investment portfolio and consider rebalancing if needed.

- Consider any life changes, such as job changes, marital status changes, or health-related factors that may require adjustments to your plan.

- Revisit your retirement expenses and adjust if necessary based on changes in your lifestyle or economic conditions.

- Consult with a financial advisor if needed to receive professional guidance on your retirement plan and investment strategy.

By regularly evaluating your retirement plan, you have the opportunity to make informed decisions, adapt to changing circumstances, and ensure that you are on track to meet your financial objectives. Stay proactive and make adjustments as necessary to maintain a solid financial foundation for your retirement years.

Conclusion

Retirement planning is an essential aspect of ensuring a secure and fulfilling post-work life. By considering factors such as estimating retirement expenses, determining retirement income sources, and calculating savings goals, individuals can create a roadmap to financial security during their retirement years.

Understanding the importance of retirement planning is the first step towards taking control of your financial future. By starting early, setting realistic goals, and implementing effective strategies, you can build a substantial retirement nest egg. Regularly evaluating and adjusting your retirement plan allows you to stay on track, respond to life changes, and make informed financial decisions.

Factors such as inflation and longevity must be taken into account to protect your savings and ensure they last throughout your retirement years. Adjusting for inflation helps maintain your purchasing power, while considering increasing life expectancies helps manage the risk of outliving your savings.

Additionally, understanding the various retirement accounts available, such as IRAs, 401(k)s, and pensions, allows you to optimize your savings and take advantage of the tax benefits they offer.

Retirement planning is a dynamic process that requires ongoing attention and adjustment. By staying informed, regularly reviewing your retirement plan, and consulting with financial professionals, you can adapt to changing circumstances and stay on track towards your retirement goals.

Remember, it’s never too early or too late to start planning for retirement. The earlier you begin, the more time you have to save and grow your investments. But even if you’re starting later in life, taking action now can still make a significant difference in ensuring a financially secure future.

So don’t delay, take the necessary steps to design and implement your retirement plan today. With careful planning, proactive decision-making, and a commitment to regular evaluation, you can achieve the retirement lifestyle you desire and deserve.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance