Finance

What Are Merchant Fees?

Published: February 24, 2024

Learn about merchant fees and how they impact your finances. Understand the costs and make informed decisions to manage your finances effectively.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

Introduction

Navigating the world of finance can be daunting, especially when it comes to understanding the various fees associated with transactions. One such fee that businesses encounter is the merchant fee. Whether you're a small business owner or a consumer, comprehending merchant fees is crucial in managing financial transactions effectively.

Merchant fees, also known as credit card processing fees, are charges incurred by businesses when they accept electronic payments from customers. These fees are levied by payment processors, such as banks or financial institutions, for facilitating the transaction process. Understanding the intricacies of merchant fees is essential for businesses to make informed decisions and optimize their financial operations.

In this article, we'll delve into the nuances of merchant fees, exploring their types, factors influencing their costs, and strategies for minimizing them. By the end, you'll have a comprehensive understanding of merchant fees, empowering you to make informed choices that benefit your business's financial health. Let's embark on this journey to unravel the world of merchant fees and equip ourselves with the knowledge to navigate the financial landscape more effectively.

Understanding Merchant Fees

Merchant fees are a fundamental aspect of the modern financial ecosystem, playing a pivotal role in the seamless processing of electronic payments. When a customer makes a purchase using a credit or debit card, the merchant incurs a fee for processing that transaction. This fee is typically calculated as a percentage of the transaction amount, along with a flat fee for each transaction. It’s important to note that these fees are not set by the business itself but are determined by the payment processor or acquiring bank.

Payment processors act as intermediaries between the merchant, the customer, and the financial institutions involved in the transaction. They provide the technology and infrastructure necessary to authorize and facilitate electronic payments. In return for these services, payment processors charge merchant fees, which contribute to their revenue and cover the costs of maintaining secure and efficient payment processing systems.

Understanding the components of merchant fees is crucial for businesses to gauge the impact of these costs on their bottom line. The percentage-based fee, often referred to as the discount rate, is a percentage of the transaction amount that the payment processor retains. Additionally, a flat fee, known as the transaction fee, is charged for each transaction processed. These fees collectively constitute the merchant discount fee, which is deducted from the total transaction amount before the funds are deposited into the merchant’s account.

By comprehending the mechanics of merchant fees, businesses can make informed decisions regarding pricing strategies, product offerings, and the acceptance of different payment methods. Moreover, this understanding empowers businesses to evaluate the competitiveness of various payment processors and negotiate favorable terms that align with their operational needs.

Types of Merchant Fees

Merchant fees encompass a variety of charges that businesses encounter when processing electronic payments. Understanding the different types of merchant fees is essential for businesses to accurately assess the overall cost of accepting electronic transactions. Here are the primary types of merchant fees:

- Interchange Fees: These fees are paid by the merchant’s bank to the customer’s bank for each transaction and are set by the card networks, such as Visa and Mastercard. The interchange fee is determined based on factors like the type of card used, the nature of the transaction, and the industry of the merchant.

- Assessment Fees: Charged by the card networks, assessment fees are a fixed percentage of the transaction value. These fees contribute to the operational costs and profitability of the card networks.

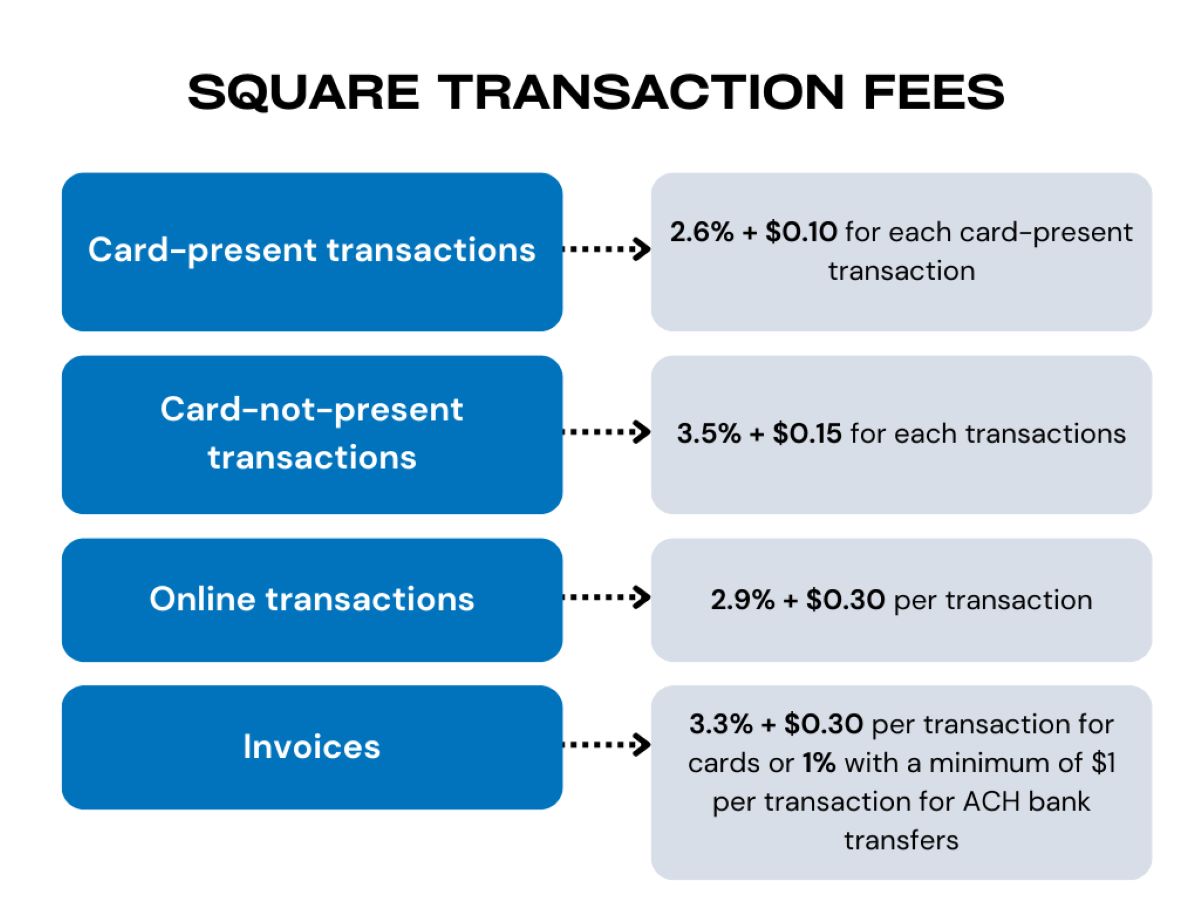

- Payment Processor Fees: Payment processors levy fees for their services, including transaction processing, authorization, and settlement. These fees often comprise a combination of a percentage of the transaction amount and a flat fee per transaction.

- Incidental Fees: These fees encompass various additional charges, such as chargeback fees, retrieval request fees, and batch processing fees. Chargeback fees are incurred when a customer disputes a transaction, leading to a reversal of funds, while retrieval request fees are charged for providing transaction documentation in response to a customer’s inquiry.

By understanding the distinct types of merchant fees, businesses can discern the breakdown of costs associated with processing electronic payments. This knowledge enables businesses to evaluate the impact of these fees on their profitability and make informed decisions when selecting payment processing partners and devising pricing strategies.

Factors Affecting Merchant Fees

Merchant fees are influenced by various factors that can significantly impact the overall cost of processing electronic payments. Understanding these factors is crucial for businesses to anticipate and manage their expenses effectively. Here are the key elements that influence merchant fees:

- Business Type and Industry: The nature of the business and the industry it operates in can influence the risk associated with processing electronic payments. For instance, businesses categorized as high-risk, such as those in the travel or subscription-based sectors, may face higher merchant fees due to the elevated potential for chargebacks and fraud.

- Transaction Volume: The volume of transactions processed by a business can impact the merchant fees. Typically, businesses that handle a higher volume of transactions may negotiate lower fees with payment processors due to the potential for a consistent influx of revenue for the processor.

- Average Transaction Value: The average value of transactions can affect the merchant discount rate. Higher-value transactions may result in lower percentage-based fees, while lower-value transactions could incur relatively higher fees as a percentage of the transaction amount.

- Payment Processing Method: The method through which transactions are processed, such as in-store, online, or mobile payments, can influence the associated fees. Online and mobile transactions may involve higher security risks, potentially leading to varied fee structures.

- Card Type: Different card types, such as rewards cards or corporate cards, may carry higher interchange fees, impacting the overall merchant fees for businesses that accept these cards.

- Payment Processor and Service Agreements: The choice of payment processor and the terms outlined in the service agreements can significantly affect the merchant fees. Businesses can negotiate pricing structures and terms based on their transaction volume, industry, and operational requirements.

By recognizing the factors that influence merchant fees, businesses can tailor their operational strategies to mitigate costs effectively. Engaging in strategic negotiations with payment processors, optimizing transaction processes, and implementing robust fraud prevention measures are among the approaches that businesses can adopt to manage and minimize the impact of these factors on their merchant fees.

How to Minimize Merchant Fees

Minimizing merchant fees is a priority for businesses seeking to optimize their financial operations and enhance profitability. While these fees are an inherent aspect of accepting electronic payments, there are several strategies that businesses can employ to mitigate their impact. Here are effective approaches to minimize merchant fees:

- Compare Payment Processors: Conduct thorough research and compare the fee structures and service offerings of different payment processors. Look for transparent pricing models, competitive rates, and favorable terms that align with your business’s needs.

- Negotiate Fee Structures: Engage in negotiations with payment processors to secure customized fee structures based on your business’s transaction volume, industry, and specific requirements. Leverage competing offers to advocate for more favorable terms.

- Optimize Payment Processing Systems: Implement efficient payment processing systems that streamline transaction authorization, settlement, and reconciliation. This can reduce operational costs and potentially lead to lower fees.

- Enhance Fraud Prevention Measures: Robust fraud prevention and risk management practices can minimize the occurrence of chargebacks and fraudulent transactions, consequently reducing the associated fees and mitigating financial losses.

- Encourage Cost-Effective Payment Methods: Promote the use of cost-effective payment methods, such as ACH transfers or debit cards, which typically incur lower processing fees compared to credit cards.

- Monitor and Analyze Fee Statements: Regularly review and analyze merchant fee statements to identify any discrepancies or unexpected charges. This proactive approach can help rectify errors and ensure that you are not overpaying for processing fees.

- Stay Informed About Regulatory Changes: Stay abreast of regulatory developments and changes in the payment processing industry. Understanding evolving regulations and compliance requirements can help businesses adapt their strategies to minimize the impact of regulatory-driven fee adjustments.

By implementing these proactive measures, businesses can navigate the landscape of merchant fees more effectively, optimize their financial performance, and bolster their competitiveness in the market. Strategic management of merchant fees contributes to improved cost-efficiency and supports sustainable business growth.

Conclusion

Merchant fees are an integral aspect of conducting business in today’s digital economy. Understanding the nuances of these fees empowers businesses to make informed decisions, optimize their financial strategies, and enhance their overall operational efficiency. By comprehending the types of merchant fees, the factors influencing their costs, and effective strategies to minimize their impact, businesses can navigate the complexities of electronic payment processing with confidence.

It is imperative for businesses to proactively manage their merchant fees by leveraging competitive pricing models, negotiating favorable terms with payment processors, and implementing streamlined payment processing systems. Additionally, prioritizing fraud prevention measures and promoting cost-effective payment methods can contribute to mitigating the impact of merchant fees on the bottom line.

As the financial landscape continues to evolve, staying informed about regulatory changes and industry developments is crucial for businesses to adapt their strategies and minimize the impact of fee adjustments. By adopting a proactive and informed approach to managing merchant fees, businesses can optimize their financial performance, bolster their competitiveness, and position themselves for sustained success in the dynamic marketplace.

Ultimately, a comprehensive understanding of merchant fees empowers businesses to make strategic decisions that align with their operational objectives, enhance customer experiences, and drive sustainable growth. By navigating the realm of merchant fees with astuteness and agility, businesses can harness the full potential of electronic payment processing while optimizing their financial resources for long-term success.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance