Finance

What Is A Draft In Banking

Modified: February 21, 2024

Learn what a draft in banking is and how it relates to finance. Discover key concepts and uses of drafts in the financial sector.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

Introduction

In the world of banking and finance, various instruments are used to facilitate transactions, one of which is a draft. A draft is a widely accepted method of payment that allows one party to send funds to another party, typically for goods or services rendered.

In simple terms, a draft is a written order issued by a person or entity instructing a bank or financial institution to pay a specific amount of money to a named recipient. It serves as a legal document that guarantees the payment and acts as an official proof of obligation.

Drafts have been used in banking for centuries and continue to be a popular choice due to their convenience and security features. They offer a flexible and reliable payment solution, especially for large transactions involving parties who may not have a direct financial relationship.

This article will delve into the details of drafts in banking, including their definition, types, how they work, advantages, disadvantages, and the security features that make them a preferred choice for many financial transactions.

Definition of a Draft in Banking

In the banking industry, a draft refers to a negotiable instrument that serves as a form of payment. It is commonly used for domestic and international transactions, allowing individuals and businesses to transfer funds securely and efficiently.

A draft functions as an order from the payer, also known as the drawer, to the payee, instructing a bank or financial institution to make a payment to a designated recipient, referred to as the drawee. The drawee can be an individual, a company, or even another bank.

Essentially, a draft is a written contract where the drawer authorizes the drawee to deduct a specified amount from their account and pay it to the payee. The draft includes essential information such as the amount to be paid, the name of the payee and drawee, and any relevant instructions or conditions.

One of the distinguishing features of a draft is that it can be transferable. This means that the payee, instead of receiving the funds directly, can endorse the draft to a third party, effectively transferring the payment obligation to them. This transferability makes drafts a versatile instrument in conducting business transactions.

Drafts can be categorized into two main types: sight drafts and time drafts. A sight draft is payable as soon as it is presented to the drawee or their financial institution. In contrast, a time draft specifies a future payment date, allowing for a delayed payment. Time drafts are often accompanied by a document known as a bill of exchange or a promissory note, further outlining the terms and conditions of the payment.

It is important to note that drafts should not be confused with checks. While both documents serve as payment instruments, their underlying mechanisms and legal implications differ. Checks typically draw funds directly from the drawer’s account, while drafts may involve different parties and financial institutions in the payment process.

Understanding the definition and types of drafts is crucial for anyone involved in banking or financial transactions. With this knowledge, individuals and businesses can utilize drafts effectively to facilitate secure and timely payments.

Types of Drafts

There are various types of drafts used in banking, each with its own characteristics and purpose. Understanding the different types of drafts can help individuals and businesses choose the most suitable payment instrument for their specific needs. Here are some common types:

- Sight Draft: A sight draft, as the name suggests, is payable upon presentation. This means that the drawee is obligated to make the payment as soon as they receive the draft. Sight drafts are commonly used in transactions where immediate payment is necessary or preferred.

- Time Draft: Unlike a sight draft, a time draft specifies a future payment date. The drawee is not required to make the payment until the specified date. This type of draft allows for a delay in payment, providing more flexibility for both the payer and payee.

- Trade Draft: A trade draft is specifically designed for business transactions involving the purchase or sale of goods and services. It typically includes detailed information about the transaction, such as the terms of the sale, shipment details, and payment instructions. Trade drafts are widely used in domestic and international trade to ensure secure and transparent transactions.

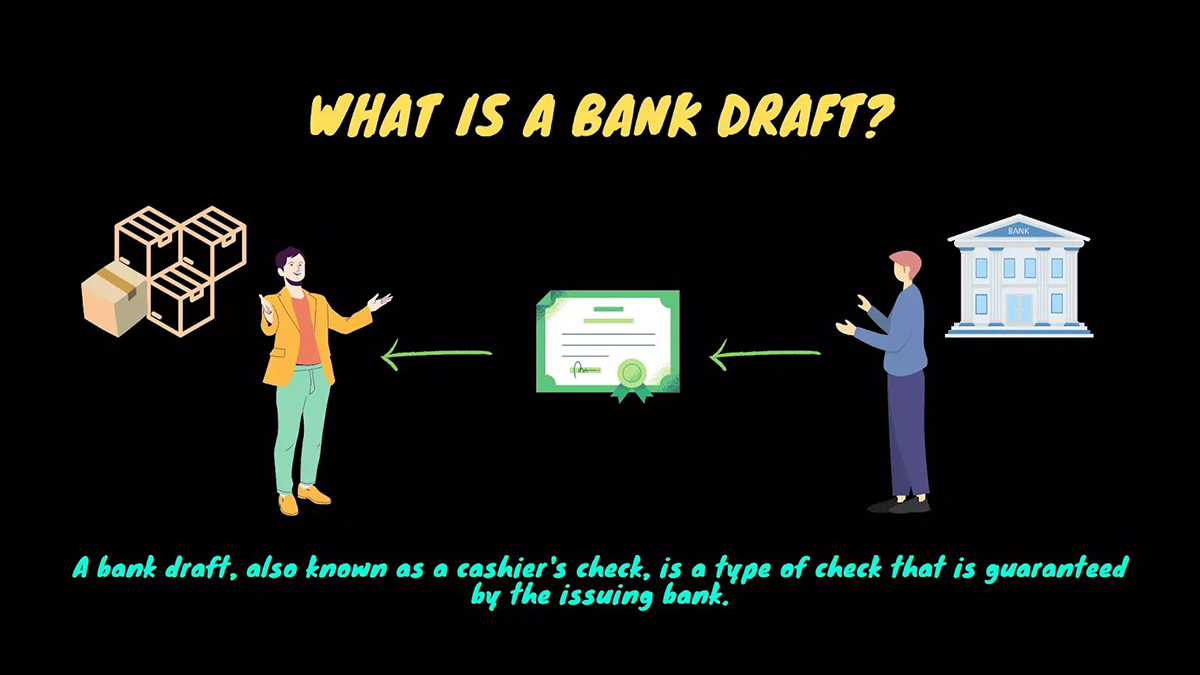

- Bank Draft: A bank draft, also known as a cashier’s check, is a type of draft issued by a bank or financial institution. It guarantees the payment as the bank acts as the drawer and also provides the funds. Bank drafts are considered a safe and widely accepted form of payment, especially for large transactions or when a higher level of security is required.

- Traveler’s Cheque: Although not strictly a draft, traveler’s cheques operate on a similar principle. They are preprinted, fixed-denomination checks that can be used as a form of payment while traveling. Traveler’s cheques offer convenience and security as they can be replaced if lost or stolen.

These are just a few examples of the types of drafts that exist in banking. It’s essential to understand the nuances of each type and choose the one that best suits the specific transaction and payment requirements.

How Drafts Work

Understanding how drafts work is crucial in comprehending the payment process involved in using this form of instrument in banking transactions. Here is a simplified explanation of how drafts work:

- Creation: The process begins with the creation of a draft by the payer, also known as the drawer. The drawer fills out the necessary details on the draft, including the amount to be paid, the name of the payee, and any specific instructions or conditions.

- Presentation: Once the draft is created, the drawer presents it to their bank or financial institution. The bank verifies the authenticity of the draft and ensures that there are sufficient funds in the drawer’s account to cover the payment.

- Payment Authorization: After the bank verifies the draft, it authorizes the payment by debiting the drawer’s account for the specified amount. The bank then becomes the drawee and is responsible for making the payment to the payee.

- Payment Process: The draft is sent to the payee’s bank or financial institution for payment. The payee’s bank verifies the authenticity of the draft and compares the details on the draft with their records. If everything is in order, the payee’s bank credits the payee’s account with the specified amount.

- Transferability: In some cases, the payee may choose to transfer the draft to a third party. This is done by endorsing the draft, effectively transferring the payment obligation to the third party. Endorsements may be made on the back of the draft.

- Presentation to Drawee: If the draft is transferable, the new holder of the draft can present it directly to the drawee’s bank for payment. The drawee’s bank verifies the authenticity of the draft and, upon confirmation, makes the payment to the new holder.

- Payment Completion: Once the payment is made, the draft is considered fulfilled, and the transaction is completed. The payee or new holder can access the funds transferred through the draft, and the drawer’s obligation is settled.

It’s important to note that the specific processes and requirements for drafts may vary depending on the country, financial institution, and the type of draft used. However, the underlying principle of a draft as an order for payment remains consistent throughout.

By understanding how drafts work, individuals and businesses can effectively utilize this payment instrument to carry out secure and reliable financial transactions.

Advantages of Using Drafts in Banking

Using drafts in banking transactions offers several advantages that make them a popular method of payment for individuals and businesses alike. Let’s delve into some of the key advantages of using drafts:

- Secure Payment: Drafts provide a high level of security for both the payer and payee. Since the payment is guaranteed by the drawer’s bank, there is a reduced risk of fraud or non-payment. This makes drafts a preferred option for transactions involving large sums of money or when dealing with unfamiliar parties.

- Flexibility: Drafts offer flexibility in terms of payment options. The payee can choose to receive immediate payment by presenting a sight draft or opt for a time draft, allowing for a delay in payment. This flexibility allows for better financial management and ensures that both parties have control over the payment process.

- Transferability: Drafts can be transferred to third parties through endorsement. This transferability allows for greater flexibility in financial transactions. The payee may choose to use the draft as a form of payment to another party, effectively passing on the payment obligation. This feature makes drafts a convenient instrument for business transactions, particularly in complex supply chains.

- Accepted Worldwide: Drafts are widely recognized and accepted globally. They are a trusted form of payment, making them valuable in domestic and international transactions. This acceptance ensures that drafts can be utilized in various industries and business environments, facilitating smoother financial transactions.

- Clear Documentation: With drafts, there is clear documentation of the payment process. The draft itself serves as a legally binding contract between the payer, payee, and financial institutions involved. This documentation provides transparency and reduces the chances of disputes or misunderstandings regarding the payment terms and obligations.

- Effective Cash Management: Drafts enable efficient cash management for businesses. They allow for controlled payment scheduling, ensuring that funds are disbursed when required while maintaining the visibility of cash flows. This helps businesses maintain strong financial discipline and liquidity.

The use of drafts in banking transactions offers numerous advantages, including secure payments, flexibility, transferability, global acceptance, clear documentation, and effective cash management. These benefits contribute to the continued popularity of drafts as a reliable and convenient payment instrument in the world of finance.

Disadvantages of Using Drafts in Banking

While drafts have various advantages, it’s important to consider the potential disadvantages that come with their use in banking transactions. Here are a few drawbacks to using drafts:

- Lengthy Processing Time: Depending on the banks and financial institutions involved, the processing time for drafts can be longer compared to other payment methods. The verification and clearance process may take several days, which can delay the payment and impact the liquidity of the parties involved.

- Potential for Fraud: Although drafts are generally considered secure, there is still a risk of fraudulent activity. Forgery, alteration, or counterfeit drafts can lead to financial losses for both the payer and payee. It is essential to exercise caution and ensure the authenticity of the draft before accepting it as a form of payment.

- Higher Costs: Using drafts can come with additional costs. Banks may charge fees for issuing, processing, and handling drafts, which can increase the overall transaction expenses. Additionally, international drafts may involve currency conversion fees, further adding to the cost.

- Dependence on Banking Systems: Drafts rely on the efficiency and reliability of the banking systems involved. In case of any issues with the banks or their infrastructure, such as system outages or delays, the processing and clearance of drafts can be affected. This dependence on third-party entities can introduce unforeseen risks and delays.

- Potential Payment Dishonor: There is a slight risk of payment dishonor when using drafts. If the drawer’s account does not have sufficient funds or if the drawer places a stop payment on the draft, the payment may be rejected or delayed. This can cause inconvenience and disrupt the payment process for the payee.

- Complexity for Endorsement: While the transferability of drafts is an advantage, it can add complexity to the payment process. Proper endorsement procedures and documentation must be followed to ensure that the transfer of payment obligation is valid. Failure to comply with endorsement requirements can invalidate the draft and result in payment disputes.

It is important to weigh the advantages against the disadvantages when considering the use of drafts in banking transactions. Understanding these potential drawbacks and taking necessary precautions can help mitigate risks and ensure a smooth payment experience when utilizing drafts.

Security Features of Drafts

Security is paramount in banking transactions, and drafts are designed with several features to ensure the integrity and authenticity of the instrument. These security measures help prevent fraud and provide peace of mind to both the payer and the payee. Here are some common security features of drafts:

- Unique Design and Paper: Drafts are typically printed on high-quality, specialized paper with unique textures, watermarks, and other distinctive features. These design elements make it difficult to replicate or counterfeit the draft, enhancing its security.

- Use of Security Inks: Drafts utilize special inks that are resistant to alteration and tampering. These inks have specific properties that make it difficult to erase or modify the information on the draft without leaving visible evidence of tampering.

- Microprinting: Microprinting is a security feature that involves printing extremely small text or images on the draft. These microscopic details are difficult to replicate accurately, adding an additional layer of security and authenticity.

- Holograms and Foil Stamps: Some drafts may incorporate holograms or foil stamps as security features. These elements are unique and difficult to reproduce, making it easier to identify genuine drafts and distinguishing them from counterfeit ones.

- Machine-readable Codes: Many drafts contain machine-readable codes, such as barcodes or QR codes. These codes allow for easy verification and validation of the draft’s authenticity, reducing the risk of accepting fraudulent drafts.

- Security Envelopes: In some cases, drafts are issued in secure envelopes with tamper-evident seals. These envelopes provide an added layer of protection, ensuring that the draft remains secure until it reaches the intended recipient.

- Advanced Encryption: With the increasing digitalization of banking transactions, drafts may include advanced encryption technology to protect the information and ensure secure transmission between financial institutions. This encryption adds an extra level of security and confidentiality to the draft.

- Unique Serial Numbers: Each draft is assigned a unique serial number, enabling easy identification and tracking of the instrument. Serial numbers are crucial for audit purposes and can help detect any discrepancies or fraudulent activity associated with the draft.

These security features work together to make drafts a trusted and secure method of payment in banking. By incorporating these measures, drafts help safeguard the payment process and minimize the risk of fraud and unauthorized alterations.

Differences between Drafts and Cashier’s Checks

While both drafts and cashier’s checks are widely used payment instruments in banking, there are distinct differences between the two. Understanding these differences is crucial for individuals and businesses when choosing the most appropriate form of payment. Here are the key distinctions between drafts and cashier’s checks:

- Issuer: One of the main differences lies in the issuer of the instrument. Drafts are typically issued by individuals or businesses who have an account with a bank, whereas cashier’s checks are issued by the bank itself. The bank guarantees payment for a cashier’s check, whereas a draft relies on the funds available in the drawer’s account.

- Payment Obligation: In a draft, the payment obligation rests primarily with the drawer, who instructs the drawee (bank or financial institution) to pay a specific amount to the payee. The funds for the payment are drawn from the drawer’s account. In contrast, with a cashier’s check, the bank itself becomes the payer and assumes the obligation to make the payment to the payee.

- Security: Cashier’s checks are often considered more secure compared to drafts. Since they are issued by the bank and backed by the bank’s funds, the risk of the payment not being honored is minimal. Cashier’s checks have built-in security features, such as watermarks and unique paper, to deter counterfeiting. On the other hand, drafts rely on the drawer’s account balance, which can introduce a slight element of risk if the funds are insufficient or not available.

- Clearance Process: Generally, cashier’s checks have a smoother and faster clearance process compared to drafts. As a bank-issued instrument, cashier’s checks are quickly verified and accepted by other financial institutions. Drafts, however, may require additional verification and clearance steps, especially if they involve parties or banks that do not have an established relationship.

- Transferability: While both drafts and cashier’s checks can be transferable, drafts are typically more versatile in terms of transferability. The payee can endorse a draft to a third party, effectively transferring the payment obligation. Cashier’s checks, on the other hand, may have more restrictions and limitations when it comes to transferability and endorsement.

- Costs: The costs associated with drafts and cashier’s checks can vary. Generally, the fees for purchasing a cashier’s check tend to be higher compared to the fees for issuing a draft. The exact charges may vary depending on the bank, the amount involved, and the specific circumstances of the transaction.

Considering these differences is crucial when deciding between using a draft or a cashier’s check as a payment instrument. The choice will depend on factors such as the level of security required, the issuing party’s relationship with the bank, the clearance time, and any limitations on transferability.

Conclusion

Drafts play a vital role in the world of banking, providing a secure and reliable method for conducting financial transactions. With their defined payment obligations and various types, drafts offer flexibility and convenience for both individuals and businesses.

Throughout this article, we have explored the definition of a draft in banking, the different types of drafts available, how they work, and their advantages and disadvantages. We have also highlighted the importance of security features in drafts, which ensure the integrity and authenticity of these payment instruments.

While drafts offer benefits such as secure payment, flexibility, and transferability, they do come with some drawbacks, including potential delays, higher costs, and a reliance on banking systems. It is important for users to assess these factors and consider their specific requirements before utilizing drafts for their transactions.

Lastly, understanding the distinctions between drafts and cashier’s checks is essential. While drafts rely on the drawer’s account balance and payment instructions, cashier’s checks are issued by banks and carry a higher level of security and assurance.

In conclusion, drafts are a valuable tool in the banking industry, providing a reliable and secure means of payment for various financial transactions. By utilizing the appropriate security measures and understanding the nuances of drafts, individuals and businesses can conduct their transactions confidently and efficiently.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance