Finance

What Is A Qualified Pension Plan

Modified: February 21, 2024

Learn all about qualified pension plans and their importance in finance. Discover how these plans can help secure your financial future.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

- Introduction

- Definition of a Qualified Pension Plan

- Benefits of a Qualified Pension Plan

- Eligibility Requirements for a Qualified Pension Plan

- Types of Qualified Pension Plans

- Vesting and Participation Rules

- Contribution Limits for Qualified Pension Plans

- Tax Advantages of a Qualified Pension Plan

- Withdrawal and Distribution Options

- Differences Between Qualified and Non-Qualified Pension Plans

- Importance of a Qualified Pension Plan for Retirement Planning

- Conclusion

Introduction

A qualified pension plan is a retirement savings arrangement that is established by an employer and meets specific requirements set by the Internal Revenue Service (IRS). These plans are designed to provide employees with a reliable source of income during their retirement years, helping them maintain their standard of living and financial security.

Participating in a qualified pension plan is an essential component of a comprehensive retirement savings strategy. By contributing a portion of their earnings to the plan, employees can accumulate a substantial retirement nest egg over time, with the added benefit of potential tax advantages.

In this article, we will explore the various aspects of a qualified pension plan, including its definition, benefits, eligibility requirements, types, contribution limits, tax advantages, withdrawal options, and the differences between qualified and non-qualified pension plans. Whether you are an employee considering joining a qualified pension plan or an employer seeking to understand the benefits of offering such a plan to your workforce, this article will provide you with the essential information you need.

So, let’s delve into the world of qualified pension plans and discover how they can play a crucial role in your retirement planning.

Definition of a Qualified Pension Plan

A qualified pension plan, also known as a qualified retirement plan, is a type of retirement savings arrangement established by an employer that adheres to specific rules and regulations set by the IRS. These plans are intended to provide employees with a reliable source of income during their retirement years.

One of the key features of a qualified pension plan is that it offers tax advantages to both the employer and the employee. Through these plans, employees can contribute a portion of their earnings on a pre-tax basis, which means that their contributions are deducted from their taxable income. This allows employees to lower their current tax liabilities while saving for their future.

Employers play a crucial role in qualified pension plans by making contributions to the plan on behalf of their employees. These contributions can take the form of matching contributions, where the employer matches a certain percentage of the employee’s contributions, or non-elective contributions, where the employer contributes a fixed percentage of the employee’s salary regardless of whether the employee makes contributions or not.

Qualified pension plans also have specific rules regarding the management and distribution of the funds. The funds contributed to the plan are typically invested in a variety of financial instruments, such as stocks, bonds, and mutual funds, with the goal of growing the funds over time.

At retirement, employees who have participated in a qualified pension plan are eligible to receive regular payments, often in the form of a monthly annuity, based on their accumulated contributions and investment returns. The amount of the retirement benefit depends on factors such as the employee’s length of service, salary history, and the performance of the investment portfolio.

It is important to note that qualified pension plans are subject to various restrictions and limitations to ensure that they are primarily used for retirement savings and not for short-term financial needs. These restrictions include contribution limits, vesting requirements, and rules for early withdrawal and distribution.

In the next section, we will explore the benefits of participating in a qualified pension plan and how it can contribute to a secure retirement.

Benefits of a Qualified Pension Plan

Participating in a qualified pension plan offers numerous advantages for both employees and employers. These benefits contribute to a secure and fulfilling retirement for employees, while also serving as a valuable employee benefit for employers. Let’s explore some of the key benefits of a qualified pension plan:

- Employer Contributions: One of the biggest advantages of a qualified pension plan is that employers often make contributions on behalf of their employees. These contributions can provide a significant boost to the employee’s retirement savings, helping them accumulate wealth for their golden years.

- Tax Advantages: Qualified pension plans offer tax benefits for both employees and employers. Employees can contribute to their retirement savings on a pre-tax basis, meaning their contributions are deducted from their taxable income, resulting in lower current tax liabilities. Employers may also receive tax deductions for their contributions to the plan.

- Long-Term Savings: Qualified pension plans are designed to be long-term savings vehicles, encouraging employees to save consistently and build a substantial nest egg for retirement. By contributing regularly and taking advantage of employer matching, employees can benefit from compounded growth over time.

- Employer Retention and Attraction: Offering a qualified pension plan can be a valuable tool for employers in attracting and retaining top talent. In a competitive job market, a comprehensive retirement plan can set an employer apart from others and enhance employee loyalty and satisfaction.

- Financial Security: A qualified pension plan provides employees with a reliable source of income during retirement. Knowing that they have a pension plan in place can provide peace of mind and financial security, allowing employees to enjoy their retirement without worrying about running out of funds.

- Social Security Supplement: For employees who may have limited reliance on Social Security benefits, a qualified pension plan can serve as a supplement to their retirement income. This additional income can help fill the gap and ensure a comfortable standard of living in retirement.

Overall, a qualified pension plan offers a range of benefits for both employees and employers. It provides employees with an effective way to save for retirement, enjoy tax advantages, and secure financial stability in their later years. For employers, it serves as a powerful employee benefit that can enhance recruitment efforts, foster employee loyalty, and contribute to a thriving workforce.

Next, let’s explore the eligibility requirements for participating in a qualified pension plan.

Eligibility Requirements for a Qualified Pension Plan

While the specific eligibility requirements for a qualified pension plan can vary from one plan to another, there are some common criteria that employees must meet to participate in these retirement savings arrangements. Let’s take a closer look at the typical eligibility requirements:

- Minimum Age: Many qualified pension plans have a minimum age requirement for participation. This is typically around 21 years old, although some plans may have lower or higher age thresholds.

- Length of Service: Plans often require employees to have worked for the employer for a specific period of time before they become eligible to participate. This could range from a few months to a year, depending on the plan’s provisions.

- Hours Worked: Some plans may have a minimum requirement for the number of hours an employee must work to be eligible. This ensures that only employees who meet a certain level of employment are able to participate.

- Union Membership: In certain industries where unions are prevalent, eligibility for a qualified pension plan may be tied to union membership. Employees who are not part of the union may not be eligible to participate.

- Non-Discrimination Rules: Qualified pension plans must adhere to non-discrimination rules to ensure that all employees are treated fairly. These rules prevent plans from favoring highly compensated employees and must provide benefits to a broad base of employees.

It is important to note that while these eligibility requirements apply to most qualified pension plans, employers have some flexibility in setting their own requirements. Some employers may choose to have more lenient criteria to encourage broader participation, while others may have stricter requirements for specific reasons.

Additionally, employees who do not meet the eligibility criteria for a qualified pension plan may still have access to other retirement savings options, such as Individual Retirement Accounts (IRAs) or non-qualified pension plans offered by their employer.

Now that we have covered the eligibility requirements, let’s explore the different types of qualified pension plans available.

Types of Qualified Pension Plans

Qualified pension plans come in various forms, each with its own features and benefits. Let’s take a closer look at some of the most common types of qualified pension plans:

- Defined Benefit Pension Plans: Also known as traditional pension plans, defined benefit pension plans provide retired employees with a predetermined monthly benefit based on factors such as salary history, years of service, and a formula set by the plan. These plans are funded by employer contributions and aim to provide a stable income stream throughout retirement.

- Defined Contribution Pension Plans: Unlike defined benefit plans, defined contribution pension plans specify the amount of money that both the employer and employee contribute to the plan. The final retirement benefit depends on the investment performance of the contributions made and can vary based on factors such as market fluctuations and investment choices. Popular examples of defined contribution plans include 401(k) plans and 403(b) plans.

- Profit-Sharing Plans: Profit-sharing plans allow employers to make discretionary contributions to an individual account based on the company’s profitability. These contributions are often determined annually and can vary based on the company’s financial performance. Profit-sharing plans can provide employees with an additional source of retirement savings beyond their standard salary and benefits.

- Money Purchase Pension Plans: Money purchase pension plans are similar to defined contribution plans, but the employer is required to make a specific contribution percentage each year. These contributions are typically based on a percentage of the employee’s salary and are vested immediately, meaning employees have full ownership of the contributions and any investment gains.

- Cash Balance Pension Plans: Cash balance pension plans combine features of both defined benefit and defined contribution plans. These plans provide employees with a specific account balance that grows with contributions and interest credits. The account balance can be converted into an annuity or taken as a lump sum at retirement.

Employers have the flexibility to choose the type of qualified pension plan that aligns with their goals and resources. Offering a variety of pension plan options can accommodate the diverse needs and preferences of their workforce.

It is essential for employees to understand the type of pension plan offered by their employer and the specific provisions that govern them. This knowledge enables employees to make informed decisions about their retirement savings and take advantage of the benefits provided by their specific plan.

Next, let’s delve into the vesting and participation rules that govern qualified pension plans.

Vesting and Participation Rules

Vesting and participation rules are important aspects of qualified pension plans that determine when an employee becomes eligible to receive the employer’s contributions and how long they must be employed to maintain all or a portion of those contributions. Let’s explore the key concepts of vesting and participation in qualified pension plans:

Vesting: Vesting refers to the employee’s right to the employer’s contributions made to their pension plan. There are two common vesting schedules:

- Cliff vesting: Under cliff vesting, an employee becomes fully vested in the employer’s contributions after a specific period, typically three to five years. Until the vesting period is complete, the employee does not have rights to any of the employer’s contributions made to the plan.

- Graded vesting: Graded vesting provides a gradual increase in an employee’s vested percentage over time. For example, an employer may grant 20% vesting after two years of service and an additional 20% for each subsequent year until the employee reaches full vesting after six years.

It is important for employees to understand their vesting schedule, as it impacts their ability to retain the employer’s contributions if they leave the company before fully vesting. Once an employee becomes fully vested, they have ownership of the employer’s contributions and any investment earnings and can take the funds with them upon retirement or job change.

Participation: Participation rules determine when an employee becomes eligible to contribute to a qualified pension plan. These rules may vary based on age, length of service, or hours worked. Typically, employees become eligible to participate in a qualified pension plan after meeting specific criteria set by the employer, such as reaching a certain age or completing a certain period of employment.

Participation rules ensure that employees have sufficient time to establish themselves in the workforce before being granted access to retirement savings benefits. Employers may also impose waiting periods before employees can start contributing to the plan, which may range from a few months to a year.

Understanding the vesting and participation rules of a qualified pension plan is crucial for employees. It helps them plan for their retirement and make informed decisions about their employment and career choices to maximize the benefits provided by the plan.

Next, let’s discuss the contribution limits that govern qualified pension plans.

Contribution Limits for Qualified Pension Plans

Qualified pension plans have specific contribution limits that dictate how much employees and employers can contribute to the plan each year. These limits are set by the IRS and are designed to ensure that retirement plans are used primarily for long-term savings and not as a vehicle for excessive tax advantages for high-income individuals. Let’s explore the contribution limits for qualified pension plans:

Employee Contribution Limits: The IRS sets annual limits on how much an employee can contribute to a qualified pension plan. These limits are subject to adjustment each year based on inflation. As of 2021, the maximum employee contribution limit for 401(k) and 403(b) plans is $19,500. For employees aged 50 and older, there is an additional catch-up contribution allowed, which is $6,500 in 2021. These catch-up contributions are designed to help older employees accelerate their retirement savings.

Employer Contribution Limits: Employers also have limits on the amount they can contribute to a qualified pension plan on behalf of their employees. The employer contribution limit is determined by factors such as the type of plan and the employee’s compensation. For example, in a profit-sharing plan, the employer’s total contributions cannot exceed 25% of the employee’s compensation. It is important for employers to consult with their plan administrators to ensure their contributions remain within the allowable limits set by the IRS.

Combined Contribution Limits: The IRS places a total annual contribution limit, which includes both employee and employer contributions, to prevent excessive contributions that disproportionately benefit highly compensated employees. As of 2021, the combined contribution limit for defined contribution plans, such as 401(k) and 403(b) plans, is $58,000 or 100% of the employee’s compensation, whichever is less. This limit may be subject to further restrictions based on the employee’s income and plan design.

It is crucial for both employees and employers to be aware of these contribution limits to ensure compliance with IRS regulations. Exceeding the contribution limits can lead to tax implications and potential penalties.

It is also worth noting that employees have the flexibility to contribute less than the maximum allowed by the IRS. The choice of contribution amount depends on their financial situation, retirement goals, and other financial obligations they may have.

Understanding the contribution limits for qualified pension plans allows employees and employers to make informed decisions about their retirement savings and ensure that their contributions remain within the allowable limits while maximizing the benefits provided by the plan.

Next, let’s explore the tax advantages associated with qualified pension plans.

Tax Advantages of a Qualified Pension Plan

Participating in a qualified pension plan offers several tax advantages for both employees and employers. These tax benefits are designed to incentivize retirement savings and provide individuals with additional financial resources during their working years and in retirement. Let’s explore the tax advantages of a qualified pension plan:

- Pre-Tax Contributions: Qualified pension plans allow employees to contribute a portion of their earnings on a pre-tax basis. This means that the contributions are deducted from the employee’s taxable income, resulting in lower tax liabilities in the year the contributions are made. The contributions and any investment earnings grow tax-deferred until withdrawal during retirement.

- Tax-Deferred Growth: The funds contributed to a qualified pension plan grow on a tax-deferred basis. This means that investment earnings and capital gains generated within the plan are not subject to annual taxes. As a result, the accumulated savings can grow at a potentially faster rate compared to taxable investment accounts.

- Tax Deductions for Employers: Employers can generally deduct their contributions to a qualified pension plan as a business expense. This reduces the employer’s taxable income, resulting in potential tax savings for the company. Offering a qualified pension plan can provide employers with a valuable tax advantage while attracting and retaining top talent.

- Tax-Advantaged Withdrawals: When funds are withdrawn from a qualified pension plan during retirement, they are subject to ordinary income tax. However, since most individuals typically have a lower income in retirement compared to their working years, they may fall into a lower tax bracket, resulting in potentially lower tax rates on their withdrawals.

- Tax Savings during Roth Conversions: In certain cases, qualified pension plans offer the option for Roth conversions. This allows account holders to convert pre-tax funds to after-tax Roth funds within the plan. Although the conversion is taxable in the year it occurs, it provides the opportunity for tax-free growth and tax-free withdrawals in retirement.

It is important to consult with a tax professional or financial advisor to understand the specific tax implications and benefits of participating in a qualified pension plan. They can provide guidance tailored to individual circumstances and help individuals make informed decisions to optimize their tax advantages.

Overall, the tax advantages associated with qualified pension plans make them an attractive retirement savings option for employees and a valuable benefit for employers. Maximizing the tax advantages offered by these plans can significantly enhance the long-term growth and financial security of individuals during their retirement years.

Next, let’s explore the withdrawal and distribution options available within qualified pension plans.

Withdrawal and Distribution Options

Qualified pension plans offer various withdrawal and distribution options to participants when they reach retirement age. These options provide flexibility in how individuals receive their accumulated funds and allow for the best alignment with their financial needs and goals. Let’s explore the withdrawal and distribution options within qualified pension plans:

- Lump Sum Withdrawal: With this option, participants can choose to receive their entire retirement savings in a single lump sum payment. This provides immediate access to the funds, allowing individuals to use the money as they see fit. However, it is important to consider potential tax implications, as a large lump sum withdrawal can push individuals into a higher tax bracket.

- Periodic Payments: Participants can receive their retirement savings in the form of periodic payments, typically monthly. The payments can be structured for a specific period or for the lifetime of the participant. These payments can provide a steady and predictable income stream throughout retirement.

- Annuitization: An annuity is another distribution option where participants convert their retirement savings into a stream of payments that continue for a specified period or for life. Annuities offer the advantage of guaranteed income, ensuring that retirees receive consistent payments regardless of market fluctuations.

- Rollover: Participants may choose to roll over their retirement savings into an Individual Retirement Account (IRA) or another qualified retirement plan if they change jobs or retire. This allows individuals to maintain the tax advantages of the qualified pension plan and continue growing their savings in a new account. Rollovers offer flexibility and control over investment choices and withdrawal timing.

It is essential to carefully consider the withdrawal and distribution options and their potential impact on taxes, cash flow, and long-term financial goals. Participants should evaluate their individual circumstances, risk tolerance, and income needs to select the most suitable option for their retirement planning.

Additionally, participants should familiarize themselves with the rules governing distributions from their specific qualified pension plan. These rules may include minimum distribution requirements, early withdrawal penalties, and restrictions on distribution timing.

It is advisable to consult with a financial advisor or retirement specialist who can provide guidance and assist in making informed decisions regarding the withdrawal and distribution options available within a qualified pension plan.

Next, let’s explore the differences between qualified and non-qualified pension plans.

Differences Between Qualified and Non-Qualified Pension Plans

Qualified and non-qualified pension plans are two distinct types of retirement savings arrangements. While both aim to provide individuals with financial security during their retirement years, there are some key differences between these plans. Let’s explore the differences between qualified and non-qualified pension plans:

- Regulatory Requirements: Qualified pension plans must meet specific requirements set by the IRS to qualify for tax advantages, such as preferential tax treatment of contributions and earnings. On the other hand, non-qualified pension plans are not required to comply with these IRS regulations, allowing for greater flexibility in plan design and customization.

- Participation: Qualified pension plans typically have stricter eligibility requirements, such as age, length of service, and hours worked. Non-qualified plans, however, may offer broader participation, allowing a wider range of employees, including high-ranking executives, to participate without specific eligibility criteria.

- Tax Treatment: Qualified pension plans offer tax advantages, such as pre-tax contributions, tax-deferred growth, and potential tax savings at retirement. Contributions to these plans are deductible for employers and reduce the taxable income for employees. In contrast, contributions to non-qualified plans are typically made with after-tax dollars, and the growth is subject to annual taxation, unlike qualified plans.

- Contribution Limits: Qualified pension plans have annual contribution limits set by the IRS, ensuring that retirement plans are primarily used for long-term savings. Non-qualified plans, however, do not have strict contribution limits and offer more flexibility in terms of contribution amounts and timing.

- Investment Options: Qualified pension plans often have limited investment options, typically offering a selection of mutual funds or target-date funds. In contrast, non-qualified plans may allow participants to invest in a broader range of investment vehicles, including individual stocks and bonds.

- Employer Benefit: Qualified pension plans are generally viewed as an employee benefit and are offered to a broad employee base. Non-qualified plans, on the other hand, are commonly designed to provide additional benefits to high-level executives, key employees, or highly compensated individuals.

- Reporting and Disclosure: Qualified pension plans are subject to various reporting and disclosure requirements, ensuring transparency and oversight. Non-qualified plans, however, are not subject to the same level of reporting and disclosure regulations and offer greater privacy in terms of plan details.

It is important for both employers and employees to understand the differences between qualified and non-qualified pension plans. These distinctions can help individuals make informed decisions about their retirement savings options and align their financial strategies with their specific needs and circumstances.

Next, let’s highlight the importance of a qualified pension plan in retirement planning.

Importance of a Qualified Pension Plan for Retirement Planning

Having a qualified pension plan is of utmost importance when it comes to retirement planning. Retirement can be a significant phase of life, and having a reliable and well-structured pension plan provides individuals with financial security and peace of mind. Let’s explore the importance of a qualified pension plan for retirement planning:

- Long-Term Savings: A qualified pension plan encourages consistent, long-term savings. By contributing to a pension plan throughout their working years, individuals can accumulate a substantial retirement nest egg and mitigate the risk of insufficient funds during retirement.

- Tax Advantages: Qualified pension plans offer attractive tax advantages. Contributions made to these plans are typically made on a pre-tax basis, reducing individuals’ taxable income and potentially lowering their current tax liabilities. The tax-deferred growth within the plan allows savings to grow faster compared to taxable investment accounts, maximizing the potential for a comfortable retirement.

- Employer Contributions: Many qualified pension plans involve employer contributions, which can significantly boost retirement savings. Employer matching programs or non-elective contributions provided by the employer contribute to the overall growth of the retirement fund, increasing the likelihood of achieving retirement goals.

- Financial Security: A qualified pension plan provides a reliable source of income during retirement, supplementing other sources such as Social Security benefits and personal savings. With an adequate pension plan in place, retirees can enjoy their golden years with confidence, knowing that they have a consistent stream of income to cover their essential expenses and maintain their desired lifestyle.

- Controlled Spending: Structured pension plans provide retirees with a regular payment schedule, which helps in budgeting and managing expenses efficiently. Having a predictable income stream allows individuals to plan their financial obligations, ensuring that they can meet their needs without depleting their retirement savings too quickly.

- Retirement Lifestyle: A qualified pension plan offers flexibility and freedom in retirement. It allows retirees to pursue their interests, travel, engage in hobbies, and maintain an active and fulfilling lifestyle without constantly worrying about the financial aspects of retirement. A well-funded pension plan can provide the financial resources necessary to enjoy these experiences.

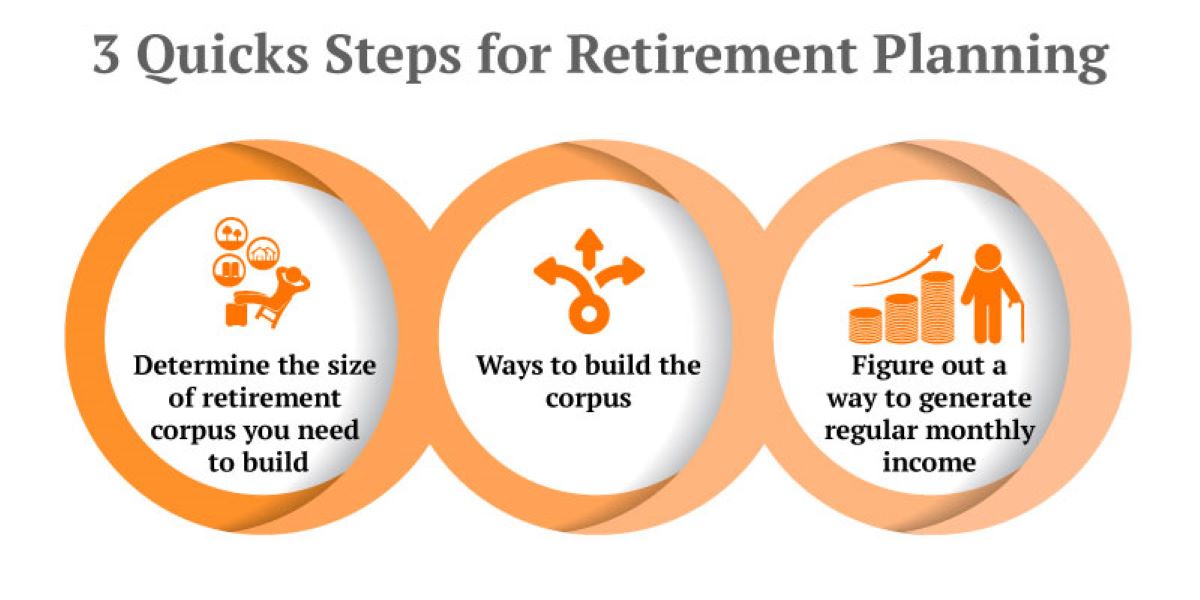

Given the importance of a qualified pension plan in retirement planning, it is crucial for individuals to carefully consider their retirement goals, financial circumstances, and available options. Working with financial advisors or retirement specialists can help navigate the complexities of pension plans and determine the most suitable strategies for achieving a comfortable and secure retirement.

Now that we have explored the significance of a qualified pension plan, let’s conclude our discussion.

Conclusion

A qualified pension plan plays a vital role in retirement planning, offering individuals a pathway to financial security and a comfortable life during their golden years. This comprehensive retirement savings arrangement is designed to provide tax advantages, employer contributions, and a reliable source of income post-retirement.

Throughout this article, we have explored the various aspects of a qualified pension plan, including its definition, benefits, eligibility requirements, types, contribution limits, tax advantages, withdrawal options, and the differences between qualified and non-qualified pension plans.

By participating in a qualified pension plan, employees can benefit from tax savings, employer contributions, and long-term savings growth. These plans offer flexibility in terms of contribution amounts, investment options, and withdrawal methods, allowing individuals to customize their retirement strategies to best meet their needs.

Employers also gain valuable benefits from offering qualified pension plans. They can attract and retain top talent while enjoying tax deductions for their contributions, contributing to a more satisfied and engaged workforce.

In conclusion, a qualified pension plan is an essential component of a well-rounded retirement savings strategy. It provides individuals with the opportunity to save consistently, enjoy tax advantages, and secure a stable income stream during retirement. It is crucial for both employees and employers to understand the specific provisions, rules, and tax advantages associated with their plan and seek professional guidance when needed to maximize the benefits provided.

Whether you are an employee planning for your retirement or an employer considering offering a qualified pension plan, understanding the significance of this type of plan will help you make informed decisions and achieve your retirement goals.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance