Finance

What Is A Variable Purchase APR?

Published: March 3, 2024

Learn about variable purchase APR in finance. Understand how it affects your credit card interest rates and financial decisions.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

Introduction

In the realm of personal finance, understanding the nuances of annual percentage rates (APR) is crucial for making informed decisions about borrowing and managing debt. One particular type of APR that holds significant relevance for credit cardholders is the Variable Purchase APR. This article aims to demystify the concept of Variable Purchase APR, shedding light on its intricacies, factors influencing it, and strategies for effectively managing it.

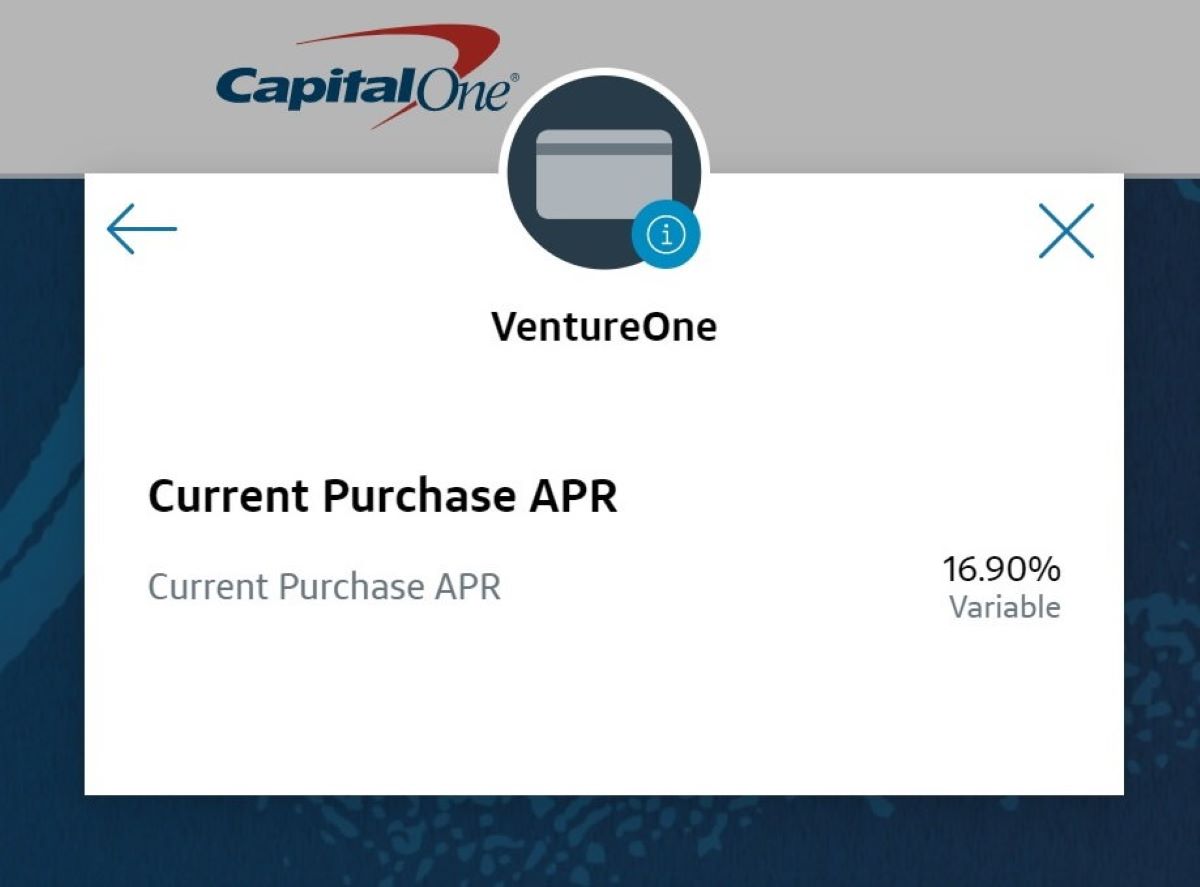

The Variable Purchase APR, often a key feature of credit cards, represents the interest rate applied to outstanding balances resulting from purchases made using the card. Unlike a fixed APR, which remains constant, a variable APR is subject to change in tandem with fluctuations in an underlying index, such as the prime rate. This inherent variability introduces an element of uncertainty, making it essential for cardholders to grasp the dynamics at play.

As we delve deeper into the realm of Variable Purchase APR, we will explore the factors influencing its fluctuations, the potential advantages and drawbacks it presents, and actionable insights for effectively managing this variable interest rate. By gaining a comprehensive understanding of Variable Purchase APR, individuals can make informed financial choices, mitigate risks, and navigate the credit landscape with confidence.

Understanding Variable Purchase APR

Variable Purchase APR is a critical component of credit card agreements, exerting a significant impact on the cost of carrying a balance from month to month. Unlike the fixed APR, which remains constant, the variable nature of this interest rate introduces an element of unpredictability, closely tied to fluctuations in the broader economic landscape.

At its core, the Variable Purchase APR is determined by adding a margin, set by the credit card issuer, to a base index, typically the prime rate. As the prime rate fluctuates in response to changes in the federal funds rate and broader economic conditions, the Variable Purchase APR adjusts accordingly. This dynamic nature makes it essential for cardholders to stay abreast of economic trends and monitor their credit card statements for changes in the APR.

Cardholders should also be mindful of the potential for a lag between changes in the index and the corresponding adjustment in the Variable Purchase APR. This lag can lead to a period of uncertainty and necessitates proactive management of credit card balances to mitigate the impact of potential rate hikes.

Furthermore, it’s crucial for individuals to comprehend the implications of carrying a balance subject to a Variable Purchase APR. Unlike making full, timely payments, carrying a balance accrues interest charges, thereby increasing the overall cost of purchases. This underscores the importance of prudent financial management and the avoidance of unnecessary interest expenses.

By understanding the intricacies of Variable Purchase APR, individuals can make informed decisions regarding credit card usage, debt management, and overall financial planning. This knowledge empowers cardholders to navigate the complexities of variable interest rates, anticipate potential fluctuations, and take proactive measures to mitigate the impact of changing APRs on their financial well-being.

Factors Affecting Variable Purchase APR

The Variable Purchase APR is influenced by a multitude of factors, each playing a pivotal role in determining the interest rate applied to credit card balances. Understanding these factors is essential for cardholders seeking to anticipate potential fluctuations in their APR and effectively manage their financial obligations.

One of the primary determinants of Variable Purchase APR is the underlying index to which it is linked, commonly the prime rate. Fluctuations in the prime rate, which is influenced by changes in the federal funds rate set by the Federal Reserve, directly impact the Variable Purchase APR. Economic conditions, monetary policy decisions, and inflationary pressures can all contribute to shifts in the prime rate, thereby affecting the APR borne by credit card balances.

Additionally, the margin set by the credit card issuer represents another critical factor influencing the Variable Purchase APR. This margin, added to the base index, serves as the card issuer’s profit and risk premium. Cardholders should be aware that variations in the margin can impact the overall APR, making it essential to review the terms and conditions of the credit card agreement to ascertain the margin applied to their account.

Moreover, an individual’s creditworthiness and credit history play a significant role in determining the specific APR they are assigned. Credit card issuers assess the credit risk associated with each cardholder, utilizing credit scores, payment history, and overall credit utilization as key metrics. Cardholders with stronger credit profiles may be eligible for lower APRs, while those with less favorable credit histories may face higher Variable Purchase APRs, reflecting the increased risk perceived by the issuer.

Furthermore, market competition and regulatory changes can impact the Variable Purchase APR landscape. Intense competition among credit card issuers may lead to promotional offers and competitive APRs to attract new customers, while regulatory developments can influence the overall interest rate environment and the terms under which credit is extended to consumers.

By comprehending the multifaceted factors influencing Variable Purchase APR, individuals can gain insight into the dynamics shaping their credit card interest rates. This knowledge empowers cardholders to monitor economic trends, maintain strong credit profiles, and make informed decisions regarding credit card usage and debt management.

Pros and Cons of Variable Purchase APR

Variable Purchase APRs come with a set of advantages and disadvantages that warrant careful consideration for individuals navigating the realm of credit card usage and debt management.

Pros:

- Flexibility: Variable Purchase APRs can potentially decrease, offering cost savings when underlying interest rates decline, thereby reducing the overall interest expense for cardholders.

- Opportunity for Savings: In a climate of decreasing interest rates, cardholders with Variable Purchase APRs may benefit from lower interest charges, translating to reduced costs for carrying credit card balances.

- Competitive Offers: Credit card issuers may leverage variable APRs to introduce enticing promotional offers, providing cardholders with the opportunity to access favorable terms and potentially lower interest rates during promotional periods.

Cons:

- Uncertainty: The variability of Variable Purchase APRs introduces uncertainty, making it challenging for cardholders to predict future interest expenses and plan their financial obligations effectively.

- Risk of Rate Increases: Fluctuations in the underlying index can lead to potential rate hikes, resulting in higher interest charges for cardholders carrying balances subject to Variable Purchase APRs.

- Financial Vulnerability: Individuals with limited financial flexibility may face challenges in managing budgetary constraints when confronted with increased interest expenses stemming from rising Variable Purchase APRs.

It is imperative for cardholders to weigh the potential benefits and drawbacks of Variable Purchase APRs, considering their financial circumstances, risk tolerance, and ability to adapt to changing interest rate environments. By carefully evaluating the pros and cons, individuals can make informed decisions regarding credit card usage, debt management, and the mitigation of interest-related financial risks.

How to Manage Variable Purchase APR

Effectively managing a Variable Purchase APR entails proactive financial planning and a comprehensive understanding of the factors impacting this variable interest rate. By implementing strategic measures, cardholders can mitigate the potential risks associated with fluctuations in the APR and optimize their financial well-being.

Monitor Economic Indicators:

Staying informed about economic indicators, particularly the prime rate and broader monetary policy decisions, empowers cardholders to anticipate potential changes in Variable Purchase APRs. By monitoring these indicators, individuals can gain insight into the prevailing interest rate environment and make informed decisions regarding credit card usage and debt management.

Review Credit Card Statements:

Regularly reviewing credit card statements is essential for identifying changes in the Variable Purchase APR. Being vigilant about any adjustments to the APR allows cardholders to assess the impact on their interest expenses and take appropriate measures to manage their credit card balances effectively.

Opt for Fixed APR Offers:

Some credit card issuers may offer the option to convert a Variable Purchase APR to a fixed APR for a specified duration. This can provide stability and predictability in interest expenses, particularly during periods of economic uncertainty or when anticipating an increase in interest rates.

Focus on Timely Payments:

Maintaining a consistent record of timely payments can positively influence a cardholder’s creditworthiness, potentially leading to opportunities for negotiating lower Variable Purchase APRs or securing more favorable credit card terms in the future.

Consider Balance Transfer Options:

For individuals facing high Variable Purchase APRs, exploring balance transfer offers to credit cards with lower APRs or promotional rates can provide a means of managing interest expenses and consolidating outstanding balances under more favorable terms.

Seek Financial Counseling:

For individuals encountering challenges in managing credit card debt subject to Variable Purchase APRs, seeking guidance from financial counselors or advisors can offer valuable insights and strategies for navigating debt repayment and optimizing financial health.

By implementing these proactive measures and maintaining a vigilant approach to managing Variable Purchase APRs, individuals can navigate the complexities of variable interest rates, mitigate potential risks, and optimize their financial well-being in the realm of credit card usage and debt management.

Conclusion

Variable Purchase APRs represent a dynamic component of credit card agreements, exerting a substantial influence on the cost of carrying balances and the overall financial well-being of cardholders. By comprehending the intricacies of Variable Purchase APRs and the factors shaping their fluctuations, individuals can make informed decisions, mitigate potential risks, and optimize their financial management strategies.

While the variable nature of these interest rates introduces an element of uncertainty, proactive monitoring of economic indicators and credit card statements empowers cardholders to anticipate potential changes in APR and adapt their financial planning accordingly. Additionally, exploring options such as fixed APR offers, balance transfers, and maintaining a strong credit profile can provide avenues for managing Variable Purchase APRs and minimizing interest-related expenses.

It is imperative for individuals to weigh the advantages and drawbacks of Variable Purchase APRs, considering their financial circumstances and risk tolerance. By doing so, they can make informed decisions regarding credit card usage, debt management, and the mitigation of interest-related financial risks.

Ultimately, by implementing strategic measures, such as monitoring economic indicators, exploring alternative credit card offers, and maintaining prudent financial habits, individuals can effectively navigate the complexities of Variable Purchase APRs, mitigate potential risks, and optimize their financial well-being in the realm of credit card usage and debt management.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance