Finance

What Is Consumer Finance

Modified: March 1, 2024

Discover the world of consumer finance and gain insights into the various aspects of managing personal finances, budgeting, investing, and more. Empower yourself financially with our comprehensive finance resources.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

- Introduction

- Definition of Consumer Finance

- Importance of Consumer Finance

- Types of Consumer Finance

- Consumer Finance Products

- Role of Consumer Finance in the Economy

- Consumer Finance Regulations

- Consumer Finance Companies

- Advantages and Disadvantages of Consumer Finance

- Consumer Finance Tips and Advice

- Conclusion

Introduction

In today’s fast-paced and consumer-driven world, the concept of consumer finance has become increasingly significant. Consumer finance refers to the management of personal finances by individuals in order to meet their day-to-day expenses, achieve their financial goals, and access necessary financial resources.

Consumer finance plays a crucial role in our daily lives as it provides individuals with the means to afford their immediate needs and aspirations. Whether it is purchasing a new car, buying a home, funding education, or managing unexpected expenses, consumer finance is the backbone that enables people to navigate their financial obligations.

It is essential to have a clear understanding of consumer finance and its intricacies in order to make informed decisions about financial matters. This article will delve deeper into the definition of consumer finance, explore its various types and products, examine its impact on the economy, and provide insights into consumer finance regulations and companies. Additionally, we will discuss the advantages and disadvantages of consumer finance and offer tips and advice to help individuals manage their personal finances effectively.

Consumer finance plays a vital role in fostering economic growth and stability. By providing individuals with access to funds, consumer finance stimulates spending, which in turn boosts demand for goods and services. This, in turn, has a positive impact on businesses and job creation, contributing to overall economic development.

However, it is important to approach consumer finance with caution. Individuals must be aware of the potential risks and pitfalls associated with taking on debt and be responsible borrowers to avoid falling into financial distress. By understanding consumer finance and following prudent financial practices, individuals can harness its benefits while safeguarding their financial well-being.

In the following sections, we will explore the definition, importance, types, products, regulations, and companies associated with consumer finance. Whether you are a consumer looking to make informed financial decisions or a professional in the finance industry, this comprehensive guide will provide you with valuable insights into the world of consumer finance.

Definition of Consumer Finance

Consumer finance is a branch of finance that focuses on the management of personal finances by individuals. It involves the borrowing, lending, and investment activities related to individuals’ financial needs and goals in order to meet their immediate and long-term financial obligations. Consumer finance encompasses a wide range of financial products and services designed to assist individuals in managing their day-to-day expenses and achieving their financial objectives.

At its core, consumer finance involves the borrowing and lending of money. Individuals often require financial assistance to afford high-cost items such as homes, cars, and education. Consumer finance institutions, such as banks, credit unions, and online lenders, offer various loan products to help individuals finance these purchases. These loans can be categorized as secured or unsecured, depending on whether collateral is required to back the loan.

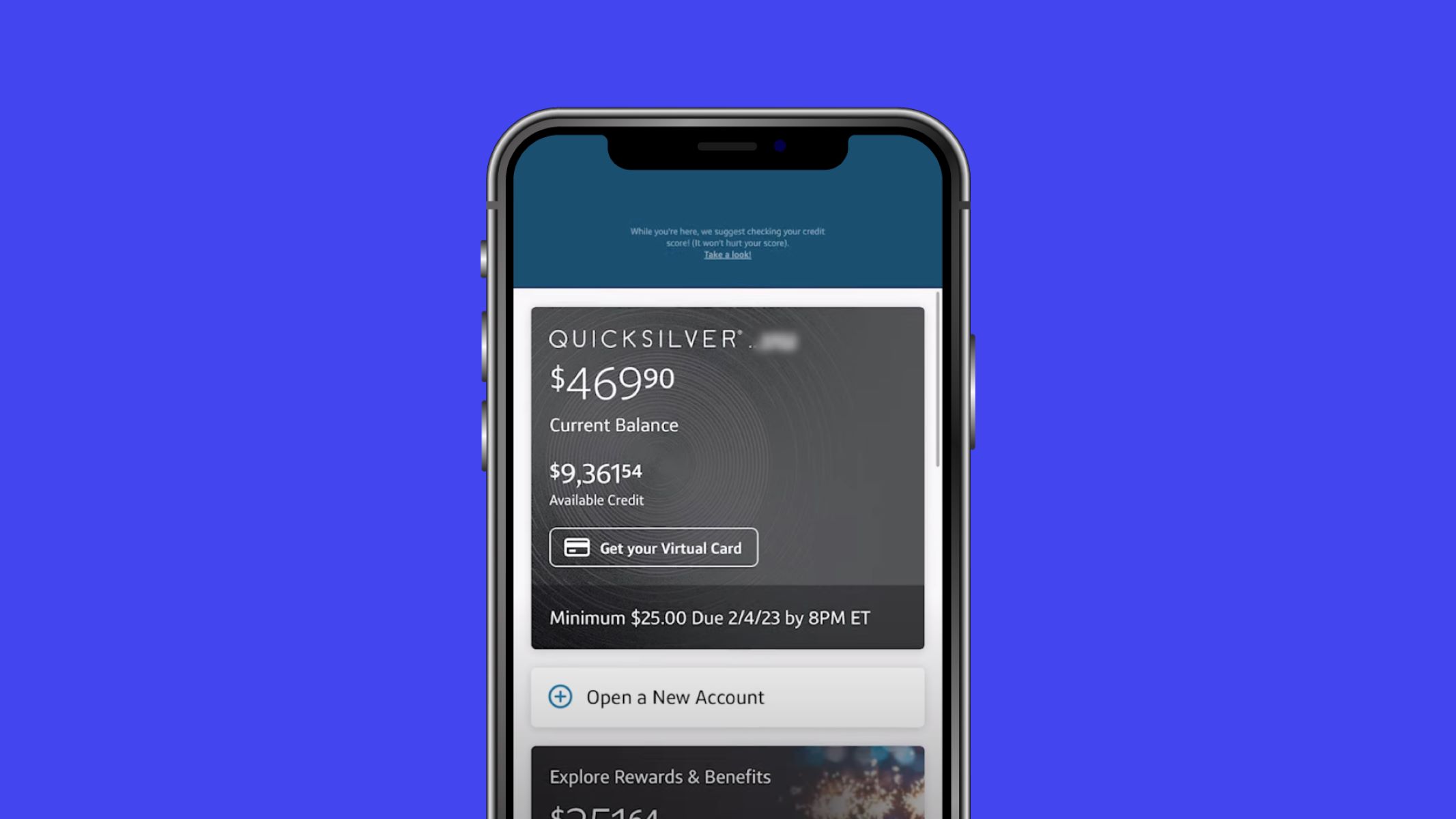

Consumer finance also includes other forms of financial assistance, such as credit cards and lines of credit. These forms of credit allow individuals to make purchases on credit and repay the borrowed amount over time. They provide convenience and flexibility in managing expenses, but it is important to use credit responsibly and avoid accumulating high-interest debt.

Another aspect of consumer finance is investment products. Individuals can invest their money in different financial instruments, such as stocks, bonds, and mutual funds, to grow their wealth and achieve long-term financial goals. Consumer finance institutions often provide investment advice and services to help individuals make informed investment decisions.

Overall, consumer finance involves the management of personal financial resources to meet current and future needs. It encompasses borrowing, lending, and investing activities to fulfill immediate expenses, achieve financial goals, and navigate unexpected financial challenges.

Consumer finance is closely linked to the concept of personal finance, which focuses on individual financial planning, budgeting, saving, and investing. By managing their personal finances effectively, individuals can make informed decisions regarding their financial well-being and achieve financial stability.

Importance of Consumer Finance

Consumer finance plays a vital role in the economic well-being of individuals and the overall health of the economy. It provides individuals with the necessary financial resources to meet their immediate needs, achieve their goals, and navigate through various life stages. Here are some key reasons why consumer finance is important:

- Meeting essential needs: Consumer finance enables individuals to afford basic necessities such as housing, healthcare, education, and transportation. Without access to finance, many people would struggle to meet these fundamental needs, leading to a lower quality of life and limited opportunities.

- Investing in assets: Consumer finance allows individuals to make significant investments in assets such as homes and vehicles. These assets not only provide individuals with shelter and transportation but can also serve as long-term investments that grow in value over time.

- Managing unexpected expenses: Life is full of unexpected events and emergencies that require immediate financial attention. Consumer finance provides individuals with the ability to handle these unexpected expenses, whether it be medical bills, car repairs, or home repairs.

- Supporting economic growth: Consumer spending is a major driver of economic growth. When individuals have access to consumer finance, they can purchase goods and services, which in turn boosts demand and stimulates economic activity. This, in turn, leads to job creation and overall economic development.

- Facilitating entrepreneurship: Consumer finance plays a crucial role in supporting entrepreneurship and small business growth. Entrepreneurs often require access to finance to start or expand their businesses. Consumer finance institutions provide business loans and other financial products to help entrepreneurs fuel their ideas and contribute to economic growth.

- Building credit history: Consumer finance, such as credit cards and loans, offers individuals an opportunity to build their credit history. A strong credit history is essential for gaining access to future credit and financial opportunities, such as mortgages, car loans, and lower interest rates.

Overall, consumer finance is important as it allows individuals to meet their essential needs, invest in assets, navigate through unexpected expenses, contribute to economic growth, support entrepreneurship, and build their credit history. It is a crucial component of personal financial well-being and economic prosperity.

Types of Consumer Finance

Consumer finance encompasses a wide range of financial products and services that cater to the diverse needs and goals of individuals. Here are some of the common types of consumer finance:

- Personal Loans: Personal loans are a common form of consumer finance that allows individuals to borrow a specific amount of money for various purposes. These loans are typically unsecured, meaning no collateral is required, and can be used for anything from consolidating debt to funding a vacation or home renovation.

- Mortgages: Mortgages are loans specifically designed for purchasing real estate, such as a home or property. These loans are typically long-term and secured by the property itself. Mortgages have different interest rates, repayment periods, and down payment requirements, depending on the borrower’s financial situation and the type of mortgage chosen.

- Auto Loans: Auto loans are loans taken out to finance the purchase of a vehicle, whether it is a car, truck, or motorcycle. Like mortgages, auto loans are secured by the vehicle being purchased, and the terms and interest rates can vary based on factors such as credit history, down payment, and the value of the vehicle.

- Credit Cards: Credit cards are a popular form of consumer finance that allows individuals to make purchases on credit. Cardholders can use the credit limit set by the issuer to make purchases and are required to make minimum monthly payments. Credit cards often come with various rewards, perks, and interest rates based on the cardholder’s creditworthiness.

- Lines of Credit: A line of credit is a flexible form of consumer finance that provides individuals with access to a predetermined amount of credit. It allows borrowers to withdraw funds as needed, up to the approved limit, and interest is only incurred on the amount borrowed. Lines of credit can be secured or unsecured and can be used for different purposes, such as home improvements or emergencies.

- Student Loans: Student loans are specifically designed to finance higher education expenses, including tuition, books, and living costs. These loans are available to both undergraduate and graduate students and can be offered by the government or private lenders. Student loans often come with favorable repayment terms and interest rates tailored to students’ needs.

- Payday Loans: Payday loans are short-term, high-interest loans designed to provide individuals with immediate cash before their next paycheck. These loans are intended to be repaid on the borrower’s next payday and typically carry high fees and interest rates. Payday loans are often used by individuals facing financial emergencies, but caution must be exercised due to their high cost.

These are just a few examples of the types of consumer finance available to individuals. Each type of consumer finance serves a specific purpose and comes with its own terms, conditions, and eligibility criteria. It is important for individuals to carefully consider their financial needs and capabilities before selecting the most appropriate form of consumer finance.

Consumer Finance Products

Consumer finance products are designed to meet the diverse financial needs and goals of individuals. These products offer a wide range of solutions to help individuals manage their personal finances effectively. Here are some common consumer finance products:

- Savings Accounts: Savings accounts are one of the most basic and common consumer finance products. They allow individuals to deposit their money and earn interest on their savings. Savings accounts provide a safe place to keep money for emergencies, future goals, and general financial security.

- Checking Accounts: Checking accounts are transactional accounts that enable individuals to deposit and withdraw money for day-to-day expenses. These accounts often come with features like debit cards, check-writing privileges, and online banking options for easy access to funds.

- Certificates of Deposit (CDs): Certificates of Deposit are time deposits that offer higher interest rates than regular savings accounts. They require individuals to keep their funds in the account for a specified period of time, ranging from a few months to several years, in exchange for higher returns.

- Credit Cards: Credit cards are widely used consumer finance products that allow individuals to make purchases on credit. Cardholders can use the card up to a certain credit limit and must repay the borrowed amount, along with any interest or fees, within a designated time frame.

- Debit Cards: Debit cards are linked to a checking account and allow individuals to make purchases using funds available in the account. Unlike credit cards, debit cards withdraw money directly from the account, eliminating the need to repay borrowed funds later.

- Personal Loans: Personal loans provide individuals with a lump sum of money that can be used for various purposes, such as consolidating debt, funding a home renovation, or covering unexpected expenses. These loans have fixed interest rates and repayment terms.

- Auto Loans: Auto loans are specifically designed to finance the purchase of a vehicle. Individuals can obtain auto loans from banks, credit unions, or other lenders to cover the cost of a new or used vehicle. These loans typically have fixed interest rates and repayment periods.

- Mortgages: Mortgages are long-term loans used to finance the purchase of a home or property. These loans are secured by the property itself and often have fixed or adjustable interest rates. Mortgages typically have longer repayment periods, ranging from 15 to 30 years.

- Student Loans: Student loans are intended to help students cover the costs of higher education. They can be provided by the government or private lenders and often come with favorable repayment terms and interest rates, including options for income-based repayment or deferment.

- Investment Products: Consumer finance products also include investment options such as stocks, bonds, mutual funds, and retirement accounts. These products allow individuals to grow their wealth over time and save for future financial goals like retirement or education.

These consumer finance products offer individuals a broad range of options to manage their personal finances effectively, whether it is saving for emergencies, funding large purchases, or investing for the future. It is important for individuals to carefully consider their financial goals, risk tolerance, and long-term plans when choosing the most suitable consumer finance products.

Role of Consumer Finance in the Economy

Consumer finance plays a significant role in driving economic growth and stability. It serves as a catalyst for consumption, investment, and entrepreneurship, contributing to the overall health and development of the economy. Here are the key roles of consumer finance in the economy:

- Stimulating Consumer Spending: Consumer finance provides individuals with access to credit, allowing them to make purchases on installment plans or through credit cards. This stimulates consumer spending, which is a critical component of economic growth. Increased consumer spending leads to higher demand for goods and services, driving production, sales, and job creation.

- Facilitating Economic Development: Consumer finance enables individuals to invest in assets such as homes, cars, and education. These investments not only benefit individuals but also contribute to economic development. The purchase of homes and vehicles stimulates the construction and manufacturing sectors, generating employment and boosting economic activity.

- Supporting Small Businesses: Consumer finance plays a vital role in supporting small businesses and entrepreneurship. Entrepreneurs often require access to financing to start or expand their businesses. Consumer finance institutions provide business loans, lines of credit, and other financial products to support small businesses, which are the backbone of many economies.

- Creating Jobs: The availability of consumer finance leads to increased consumer spending, which drives demand for goods and services. This, in turn, creates job opportunities in various industries, including retail, manufacturing, and services. Job creation is essential for economic growth, income generation, and poverty reduction.

- Promoting Financial Inclusion: Consumer finance plays a crucial role in promoting financial inclusion by providing access to financial products and services for individuals who may have limited or no access to traditional banking systems. This enables underserved populations to participate in the formal economy, build credit history, and improve their financial well-being.

- Encouraging Savings and Investments: Consumer finance institutions offer savings accounts, investment products, and retirement accounts to help individuals save and invest their money. This encourages individuals to accumulate wealth over time and contributes to the capital formation needed for businesses and infrastructure development.

- Managing Risk: Consumer finance allows individuals to manage financial risks by providing insurance products such as life insurance, health insurance, and property insurance. These products offer protection against unforeseen events and help individuals and businesses mitigate potential losses.

- Contributing to Economic Stability: Consumer finance, when managed responsibly, promotes economic stability by providing individuals with the means to meet their financial obligations. Financially stable individuals are less likely to default on loans or go bankrupt, reducing the risk of financial crises and ensuring a healthy and sustainable economy.

Overall, consumer finance plays a critical role in driving economic growth, supporting small businesses, creating jobs, promoting financial inclusion, and encouraging savings and investment. By providing individuals with access to financial resources, consumer finance contributes significantly to the overall well-being and stability of the economy.

Consumer Finance Regulations

Consumer finance is subject to a variety of regulations and laws designed to protect consumers, ensure fair practices, and maintain the stability of the financial system. These regulations aim to promote transparency, prevent fraud and abuse, and provide consumers with adequate rights and safeguards. Here are some key consumer finance regulations:

- Consumer Financial Protection Bureau (CFPB): The CFPB is a regulatory agency responsible for enforcing federal consumer financial laws and protecting consumers in the financial marketplace. It oversees and regulates banks, credit unions, and other financial firms, ensuring fair lending practices, addressing consumer complaints, and promoting financial education.

- Truth in Lending Act (TILA): TILA requires lenders to disclose important terms and costs associated with loan products. It ensures that consumers receive clear and accurate information about interest rates, fees, repayment terms, and other charges before entering into a loan agreement.

- Fair Credit Reporting Act (FCRA): The FCRA regulates the collection, use, and disclosure of consumer credit information. It gives consumers the right to access and dispute their credit reports, protects their privacy, and requires accurate reporting by credit bureaus and data furnishers.

- Equal Credit Opportunity Act (ECOA): ECOA prohibits lenders from discriminating against applicants based on characteristics such as race, religion, sex, age, or marital status. It ensures that all consumers have equal access to credit and are treated fairly in the lending process.

- Fair Debt Collection Practices Act (FDCPA): The FDCPA regulates debt collection practices and prohibits abusive, unfair, or deceptive practices by debt collectors. It outlines guidelines for how debt collectors can communicate with consumers, sets limits on harassment and false representations, and provides consumers with the right to dispute and verify debts.

- Consumer Leasing Act (CLA): The CLA requires lessors to provide clear and consistent lease disclosures to consumers. It ensures that individuals who lease goods or equipment receive comprehensive information about costs, terms, and any potential liabilities before entering into a lease agreement.

- Securities and Exchange Commission (SEC) Regulations: The SEC regulates the sale and trading of securities to protect investors and maintain fair and efficient markets. It requires companies to provide accurate and timely information to investors, prevents insider trading, and ensures compliance with securities laws.

- State-Specific Regulations: In addition to federal regulations, consumer finance is also subject to state-specific laws that vary across jurisdictions. These laws cover areas such as usury limits, foreclosure procedures, licensing requirements, and consumer protection measures.

Consumer finance regulations aim to create a fair and ethical financial marketplace where consumers are protected from deceptive practices, have access to transparent information, and can exercise their rights. Compliance with these regulations is essential for financial institutions, lenders, and other service providers to maintain trust and integrity in their interactions with consumers.

Consumer Finance Companies

Consumer finance companies play a crucial role in providing individuals with access to financial resources and services, contributing to their financial well-being and economic growth. These companies specialize in offering various consumer finance products and services tailored to meet the diverse needs and goals of individuals. Here are some common types of consumer finance companies:

- Banks: Banks are financial institutions that offer a wide range of consumer finance products and services, including savings accounts, checking accounts, credit cards, personal loans, mortgages, and investment options. They provide individuals with access to funds, financial advice, and a secure place to store their money.

- Credit Unions: Credit unions are non-profit financial cooperatives owned and operated by their members. They offer similar consumer finance products as banks, but tend to have lower fees, higher interest rates on savings accounts, and more personalized customer service. Credit unions are often community-based and serve specific geographic regions or industries.

- FinTech Companies: FinTech (Financial Technology) companies leverage technology to innovate and provide consumer finance products and services. These companies offer online lending platforms, peer-to-peer lending, digital wallets, budgeting apps, and investment platforms. FinTech companies often prioritize convenience, efficiency, and user-friendly interfaces.

- Lending Institutions: Lending institutions specialize in providing loans to individuals. This includes traditional banks, credit unions, online lenders, and specialized lending companies. These institutions offer personal loans, auto loans, student loans, and mortgages, among other lending products.

- Credit Card Companies: Credit card companies issue credit cards to individuals, allowing them to make purchases on credit up to a certain limit. These companies provide account management services, rewards programs, and various credit card options tailored to different consumer needs and credit profiles.

- Insurance Companies: Insurance companies offer a variety of consumer finance products, such as life insurance, health insurance, property insurance, and auto insurance. These products provide individuals with financial protection against unforeseen events, giving them peace of mind and financial security.

- Investment Firms: Investment firms, including brokerage houses and asset management companies, help individuals invest their money in various financial instruments such as stocks, bonds, mutual funds, and retirement accounts. These firms provide investment advice, portfolio management, and tailored investment solutions.

Consumer finance companies play a crucial role in providing individuals with the financial tools, products, and services they need to manage their personal finances effectively. They serve as intermediaries between individuals and the financial system, facilitating access to credit, investment opportunities, risk management, and financial advice. It is important for individuals to carefully evaluate the offerings and reputation of consumer finance companies to ensure they are dealing with reputable institutions that align with their financial goals and values.

Advantages and Disadvantages of Consumer Finance

Consumer finance offers individuals various advantages and opportunities to manage their personal finances effectively. However, there are also some potential disadvantages and risks that individuals should be mindful of. Here are the key advantages and disadvantages of consumer finance:

- Advantages:

- Access to funds: Consumer finance provides individuals with access to funds they may not have readily available, allowing them to meet immediate financial needs or pursue desired goals.

- Financial flexibility: Consumer finance offers individuals flexibility in managing their expenses and cash flow. Credit cards, lines of credit, and personal loans can help individuals bridge financial gaps or deal with unexpected expenses.

- Opportunity for growth: Consumer finance, such as mortgages and student loans, can provide individuals with an opportunity for growth by enabling them to invest in assets or pursue higher education that can increase their earning potential.

- Convenience and ease of transactions: Consumer finance products, such as credit cards and online banking, make financial transactions convenient and efficient. They offer features like online bill payments, mobile banking, and rewards programs for added convenience.

- Building credit history: Responsible use of consumer finance products, such as credit cards and loans, can help individuals establish and build a positive credit history. This can lead to better credit scores, lower interest rates, and increased access to financial opportunities in the future.

- Disadvantages:

- Debt accumulation: One of the primary risks of consumer finance is the potential for individuals to accumulate excessive debt if not used responsibly. High-interest rates and uncontrolled spending can lead to financial strain and difficulties in repayment.

- Interest and fees: Consumer finance products often come with interest charges, fees, and penalties. If individuals are not aware of these costs or fail to make timely payments, they can incur additional expenses and end up paying more than the original amount borrowed.

- Risk of financial instability: Relying heavily on consumer finance for day-to-day expenses can leave individuals vulnerable to financial instability. Economic downturns, job loss, or unexpected events can disrupt the ability to repay debts and impact financial well-being.

- Potential for predatory practices: Some consumer finance providers engage in predatory practices, targeting vulnerable individuals with unscrupulous lending terms, hidden fees, and aggressive collection practices. It is essential to be cautious and choose reputable financial institutions.

- Impulsive spending: Access to consumer finance, particularly credit cards, can tempt individuals to make impulsive purchases and overspend beyond their means. This can lead to long-term financial challenges and difficulty in meeting repayment obligations.

It is crucial that individuals weigh the advantages and disadvantages of consumer finance carefully and make informed decisions based on their financial situation, goals, and risk tolerance. Responsible borrowing, budgeting, and understanding the terms and conditions of consumer finance products are key to harnessing the benefits while mitigating potential risks.

Consumer Finance Tips and Advice

Effectively managing consumer finance is essential for individuals to maintain financial stability, achieve goals, and avoid unnecessary debt. Here are some tips and advice to help individuals make informed decisions and handle their consumer finance responsibly:

- Create a budget: Start by creating a monthly budget that outlines your income and expenses. This will help you track your spending, identify areas where you can cut back, and allocate funds towards savings and debt repayment goals.

- Set financial goals: Determine your short-term and long-term financial goals. Whether it’s paying off debt, saving for a down payment, or building an emergency fund, having clear goals will help you stay focused and motivated on your financial journey.

- Understand your credit: Regularly check your credit reports from the major credit bureaus to ensure accuracy and address any discrepancies. Monitor your credit score and understand how it can impact your ability to access credit and the interest rates you may receive.

- Borrow responsibly: Before taking on any form of consumer finance, carefully evaluate your needs and repayment ability. Compare interest rates, terms, and fees from different lenders to ensure you are getting the best deal. Only borrow what you can afford to repay, and avoid excessive debt.

- Pay bills on time: Make it a priority to pay your bills on time to avoid late fees and negative impacts on your credit score. Set up automatic payments or reminders to help you stay organized and ensure timely payment.

- Use credit cards wisely: If you have credit cards, be mindful of your spending and pay off the balance in full each month to avoid interest charges. Limit the number of credit cards you have and keep your credit utilization ratio low, ideally below 30% of your available credit.

- Save for emergencies: Build an emergency fund to cover unexpected expenses, such as medical bills or car repairs. Aim to save three to six months’ worth of living expenses in a separate, easily accessible account.

- Seek financial advice: If you are unsure about your financial situation or need guidance, consider seeking help from a financial advisor or credit counselor. They can provide tailored advice, help you create a financial plan, and assist with debt management strategies.

- Stay informed: Keep yourself updated on financial news, changes in consumer finance regulations, and new products or offers. Being knowledgeable about the financial landscape will empower you to make informed decisions and take advantage of opportunities.

- Practice financial discipline: Cultivate healthy financial habits such as avoiding impulsive purchases, saving regularly, and reviewing your financial goals periodically. Small changes in your daily habits can have a significant impact on your long-term financial well-being.

Remember, everyone’s financial situation is unique, so it is important to tailor these tips to meet your specific needs and circumstances. By practicing responsible consumer finance habits and being proactive in managing your finances, you can achieve greater financial security and work towards your financial goals.

Conclusion

Consumer finance is a crucial aspect of our daily lives and plays a significant role in achieving financial stability, meeting immediate needs, and pursuing long-term goals. It encompasses a wide range of financial products and services that enable individuals to manage their personal finances effectively.

Throughout this article, we have explored the definition of consumer finance, its importance in the economy, various types of consumer finance, common consumer finance products, regulations, consumer finance companies, and the advantages and disadvantages associated with consumer finance. We have also provided tips and advice to help individuals make informed decisions and handle their consumer finance responsibly.

Consumer finance offers numerous advantages, including access to funds, financial flexibility, growth opportunities, convenience in transactions, and the ability to build credit history. However, it also presents potential disadvantages such as debt accumulation, high-interest rates, financial instability risks, predatory practices, and impulsive spending.

To navigate the world of consumer finance successfully, it is crucial to approach it with caution and make informed decisions. This includes understanding your financial goals, evaluating the terms and conditions of consumer finance products, practicing responsible borrowing, and managing your finances wisely.

By creating a budget, setting financial goals, paying bills on time, using credit cards wisely, saving for emergencies, seeking financial advice when needed, and staying informed, individuals can make sound financial decisions and harness the benefits of consumer finance while minimizing the risks.

Consumer finance, when managed responsibly, can provide individuals with the necessary financial resources to meet their immediate needs, pursue their aspirations, and contribute to economic growth. By employing the strategies and tips outlined in this article, individuals can embark on a path towards financial well-being and create a solid foundation for their future.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance