Finance

Why Commercial Banking

Published: October 11, 2023

Discover the importance of commercial banking in the world of finance. Learn how it plays a vital role in supporting businesses and driving economic growth.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

Introduction

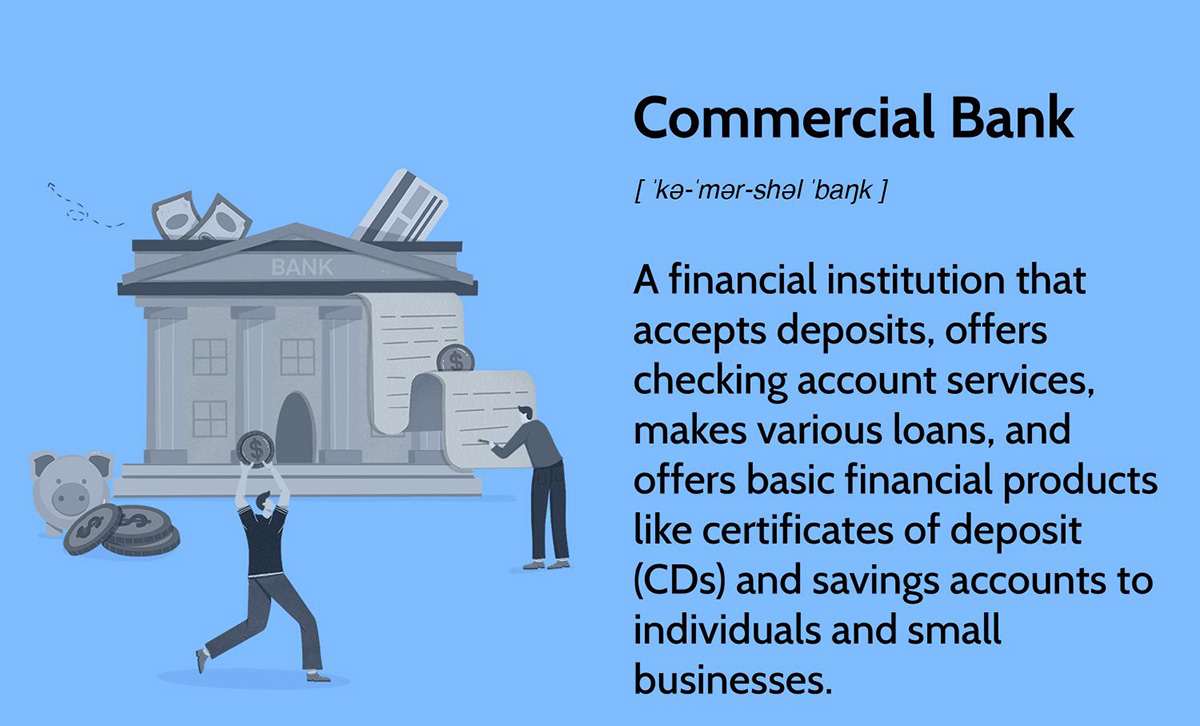

Commercial banks play a crucial role in the functioning of an economy. They are the backbone of the financial system, providing a wide range of services to individuals, businesses, and other entities. From accepting deposits to offering loans and facilitating payment transactions, commercial banks are instrumental in promoting economic growth and stability.

In this article, we will explore the significance of commercial banking and its impact on the economy. We will delve into the various services provided by commercial banks, the sources of their revenue, the regulatory framework that governs their operations, and the challenges they face in an ever-evolving financial landscape. Lastly, we will discuss the future outlook for commercial banking and how it continues to adapt to the changing needs of society.

Commercial banks serve as intermediaries between depositors and borrowers. They collect funds through deposits from individuals, businesses, and institutions and use these funds to provide loans and make investments. This process allows them to mobilize savings, allocate capital, and facilitate economic activity.

The stability and efficiency of the commercial banking sector directly influence the overall health of the economy. A well-functioning banking system promotes financial intermediation, which encourages investment and fosters economic growth. By providing credit to businesses, commercial banks fuel innovation, job creation, and entrepreneurship, thereby contributing to regional and national development.

Furthermore, commercial banks play a crucial role in facilitating payment systems. Through various instruments such as debit cards, credit cards, checks, and electronic fund transfers, they enable seamless and secure financial transactions. This not only enhances convenience for individuals and businesses but also stimulates economic activity by promoting consumer spending and trade.

Role of Commercial Banks in the Economy

Commercial banks play a vital role in the functioning of an economy by performing various functions that are crucial for economic development and stability. Let’s explore some of the key roles played by commercial banks:

- Financial Intermediation: One of the primary roles of commercial banks is to act as financial intermediaries. They mobilize funds through deposits from individuals, businesses, and institutions, and then allocate these funds to borrowers in the form of loans. This process facilitates the flow of capital in the economy, allowing businesses to invest and expand, and individuals to finance their needs and aspirations.

- Payment Processing: Commercial banks offer a range of services to facilitate payment transactions. They provide checking accounts, debit cards, credit cards, and online banking facilities, making it convenient for individuals and businesses to make payments and transfer funds. By providing efficient and secure payment systems, commercial banks support economic activity, promote trade, and contribute to the overall efficiency of the financial system.

- Safekeeping and Custodian Services: Commercial banks offer safekeeping services, where individuals and businesses can store their valuables such as jewelry, important documents, and other assets in secure vaults. Additionally, commercial banks act as custodians for securities and other financial assets, ensuring their safekeeping and facilitating transactions in the capital markets.

- Foreign Exchange Services: Commercial banks facilitate foreign exchange transactions, allowing individuals and businesses to convert currencies and engage in international trade. They provide services such as currency exchange, wire transfers, and foreign currency accounts, making it easier for businesses to engage in cross-border transactions and expand their global presence.

- Financial Advisory Services: Many commercial banks provide financial advisory services to individuals and businesses. They offer expertise on investment options, retirement planning, risk management, and other financial matters. Through these services, commercial banks assist individuals and businesses in making informed financial decisions and achieving their financial goals.

The role of commercial banks in the economy cannot be overstated. They are instrumental in promoting economic growth, stability, and financial inclusion. By mobilizing savings, allocating capital, facilitating payments, and providing various financial services, commercial banks contribute to the overall development and prosperity of a country.

Importance of Commercial Banking

Commercial banking plays a crucial role in the economy by serving as the primary financial intermediary between savers and borrowers. The importance of commercial banking can be understood through the following key aspects:

- Capital Mobilization: Commercial banks play a vital role in mobilizing savings from individuals, businesses, and institutions. They provide a secure and trusted platform for people to deposit their money and earn interest. By aggregating these funds, commercial banks are able to allocate capital for various purposes such as granting loans to individuals and businesses, which in turn fuels investment and economic growth.

- Facilitating Economic Growth: Commercial banks are essential in promoting economic growth. By providing financial resources to businesses, they enable them to expand their operations, invest in new projects, and create job opportunities. These financial resources facilitate innovation, entrepreneurship, and productivity, all of which are critical factors contributing to economic development.

- Supporting Small and Medium-sized Enterprises (SMEs): Commercial banks are often the main source of funding for small and medium-sized enterprises (SMEs) that lack easy access to capital markets. They provide loans to SMEs, allowing them to launch new ventures, expand their operations, and contribute to job creation. This support to SMEs is vital for fostering economic inclusivity and reducing income inequalities.

- Stabilizing the Financial System: Commercial banks play a pivotal role in maintaining the stability of the financial system. They act as intermediaries by transforming short-term deposits into long-term loans. This maturity transformation helps to manage liquidity risks and mitigate potential disruptions in the financial system. Furthermore, commercial banks are subject to regulatory oversight and capital adequacy requirements, which ensure their financial soundness and resilience against economic shocks.

- Promoting Financial Inclusion: Commercial banks play an important role in promoting financial inclusion by providing basic banking services to individuals who would otherwise be excluded from the formal financial system. Through the provision of savings accounts, payment services, and access to credit, commercial banks empower individuals to save, transact, and build financial stability.

The importance of commercial banking extends beyond its primary role as a financial intermediary. It is an essential pillar of the economy that fuels growth, supports businesses, fosters financial stability, and promotes inclusive development. Without the services and functions provided by commercial banks, the economy would lack the necessary financial infrastructure to sustain economic activity and progress.

Services Provided by Commercial Banks

Commercial banks offer a wide range of services to meet the financial needs of individuals, businesses, and other entities. These services are designed to facilitate banking transactions, promote savings, support borrowing activities, and provide various financial solutions. Let’s explore some of the key services provided by commercial banks:

- Deposit Accounts: Commercial banks offer various types of deposit accounts, such as savings accounts, current accounts, and fixed deposit accounts. These accounts provide individuals and businesses with a safe place to store their money, earn interest on their deposits, and have easy access to their funds through checks, debit cards, and online transfers.

- Lending Services: Commercial banks are known for their lending activities. They offer different types of loans, including personal loans, home loans, education loans, and business loans. These loans provide individuals and businesses with the necessary financial resources to meet their various needs, such as purchasing a home, funding education expenses, or expanding their business operations.

- Payment Services: Commercial banks facilitate payment transactions through various channels. They provide services such as checkbooks, debit cards, credit cards, and online banking platforms that enable individuals and businesses to make payments and transfer funds conveniently and securely. Commercial banks also participate in national and international payment networks, ensuring seamless and efficient payment processing.

- Foreign Exchange Services: Commercial banks offer foreign exchange services to individuals and businesses engaged in international trade or travel. They facilitate currency exchange, provide foreign currency accounts, issue travel cards, and assist in international money transfers, enabling customers to transact and convert currencies with ease.

- Investment Services: Many commercial banks have investment departments that offer investment advisory services and facilitate investment transactions. They provide guidance on investment options, assist in stock trading, offer mutual fund investments, and provide access to other investment opportunities, helping individuals and businesses grow their wealth.

- Wealth Management Services: Commercial banks also provide wealth management services to high-net-worth individuals and businesses. These services include portfolio management, estate planning, tax planning, and other personalized financial solutions aimed at preserving and growing wealth.

- Risk Management and Insurance: Commercial banks often have insurance subsidiaries that offer various insurance products, such as life insurance, health insurance, property insurance, and liability insurance. These insurance products help individuals and businesses mitigate potential risks and protect their assets.

These are just a few examples of the services provided by commercial banks. Overall, commercial banks play a vital role in meeting the diverse financial needs of individuals, businesses, and institutions, supporting economic activities, and fostering financial well-being.

Sources of Revenue for Commercial Banks

Commercial banks generate revenue through various channels and sources, which enable them to cover their operating costs, generate profits, and maintain financial stability. These revenue sources are essential for the sustainable operation of commercial banks. Let’s explore some of the key sources of revenue for commercial banks:

- Interest Income: The primary source of revenue for commercial banks is interest income. Banks earn interest on the loans they provide to individuals and businesses. The interest charged on loans is higher than the interest paid to depositors, allowing banks to generate a spread called the “net interest margin.”

- Non-Interest Income: Commercial banks also generate revenue through non-interest income, which includes fees and commissions charged for various services. These services may include account maintenance fees, transaction fees, fees for wire transfers, fees for issuing credit or debit cards, fees for processing loan applications, and fees for wealth management and investment services.

- Investment Income: Banks invest a portion of their funds in various financial instruments such as government securities, corporate bonds, and equities. The income generated from these investments, including dividends and capital gains, contributes to the overall revenue of commercial banks.

- Foreign Exchange Operations: Commercial banks earn revenue from foreign exchange operations. They facilitate currency exchange for individuals and businesses, charging fees or earning a spread on the exchange rates. Additionally, banks generate revenue by providing foreign currency services and participating in the forex market.

- Asset Management: Many commercial banks manage investment portfolios on behalf of their clients. They earn fees for providing asset management services and for the performance of the investment portfolios they manage. These fees contribute to the overall revenue of commercial banks.

- Loan Origination Fees: Commercial banks charge loan origination fees when disbursing loans to borrowers. These fees are typically a percentage of the loan amount and are non-refundable. Loan origination fees help cover the administrative costs associated with loan processing and contribute to the revenue of commercial banks.

- Trading and Market Activities: Commercial banks engage in trading and market activities, such as buying and selling financial securities, currencies, and derivatives. Profits generated from these trading activities contribute to the revenue of commercial banks.

- Other Services: Commercial banks offer a wide range of specialized financial services, including insurance products, wealth management services, and investment banking services. Revenue generated from these additional services adds to the overall income of commercial banks.

It is worth noting that the revenue structure of commercial banks can vary based on factors such as the size of the bank, geographical location, regulatory environment, and the specific services offered. Diversification of revenue sources is essential for banks to mitigate risks, maintain profitability, and support sustainable operations.

Regulatory Framework for Commercial Banks

Commercial banks operate within a robust regulatory framework designed to ensure the stability, integrity, and soundness of the financial system. Regulatory bodies and regulations govern various aspects of commercial banking activities, aiming to protect depositors, borrowers, and other stakeholders. Let’s explore the key components of the regulatory framework for commercial banks:

- Central Banks: Central banks play a crucial role in regulating commercial banks. They are responsible for monetary policy, maintaining financial stability, and overseeing the overall functioning of the banking system. Central banks often set minimum reserve requirements that commercial banks must maintain to ensure liquidity and stability.

- Prudential Regulations: Prudential regulations focus on ensuring the safety and soundness of commercial banks. These regulations include capital adequacy requirements, which mandate that banks maintain a minimum level of capital to absorb potential losses. Other prudential regulations may cover risk management, asset quality, liquidity management, and corporate governance practices.

- Deposit Insurance: Many countries have deposit insurance schemes to protect depositors in the event of bank failures. These schemes provide a guarantee to depositors that their funds, up to a certain limit, will be reimbursed even if the bank fails. Deposit insurance helps maintain public confidence in the banking system and promotes financial stability.

- Anti-Money Laundering (AML) and Counter-Terrorist Financing (CTF) Regulations: Commercial banks are subject to strict anti-money laundering and counter-terrorist financing regulations. These regulations require banks to implement comprehensive customer due diligence measures, monitor transactions for suspicious activities, and report any suspicious transactions to the relevant authorities. These regulations aim to combat financial crimes and protect the integrity of the financial system.

- Consumer Protection Regulations: Commercial banks are required to comply with consumer protection regulations to ensure fair and transparent treatment of customers. These regulations govern areas such as disclosure of terms and conditions, handling of complaints, protection of consumer rights, and fair lending practices. The goal is to safeguard customers’ interests and promote a level playing field.

- Supervision and Oversight: Regulatory bodies, such as banking supervisory authorities, are responsible for supervising and overseeing the operations and activities of commercial banks. They conduct regular on-site and off-site inspections to assess banks’ financial health, compliance with regulations, risk management practices, and overall governance. Supervisors also have the authority to take corrective actions or impose penalties in case of non-compliance.

- International Regulations: Commercial banks operating across borders are subject to international regulations and standards set by organizations such as the Basel Committee on Banking Supervision (BCBS). These regulations aim to promote consistency and stability in the global banking system, addressing areas such as capital adequacy, risk management, and liquidity requirements.

The regulatory framework for commercial banks is dynamic and continuously evolving to adapt to changing market conditions, emerging risks, and technological advancements. The goal is to strike a balance between facilitating innovation, promoting financial inclusion, and maintaining the safety and stability of the banking system.

Challenges Faced by Commercial Banks

Commercial banks operate in a dynamic and complex environment, facing various challenges that impact their profitability, sustainability, and ability to meet the evolving needs of their customers. Let’s explore some of the key challenges faced by commercial banks:

- Regulatory Compliance: The regulatory landscape for commercial banks is constantly evolving, with new rules and regulations being introduced to address emerging risks and ensure financial stability. Banks must invest significant resources in compliance processes, systems, and staff training to meet regulatory requirements. Keeping up with changing regulations can be challenging, especially for smaller banks with limited resources.

- Cybersecurity Risks: Commercial banks are increasingly vulnerable to cyber threats, such as data breaches, phishing attacks, and ransomware. Cybercriminals are continually devising sophisticated methods to exploit weaknesses in banks’ systems and networks. Implementing robust cybersecurity measures and staying ahead of evolving threats is a constant challenge for banks.

- Technological Disruption: Technological advancements, such as digital banking, fintech innovations, and blockchain technology, are reshaping the banking industry. Commercial banks must adapt to these changes and invest in new technologies to remain competitive. However, integrating new technologies while maintaining legacy systems and addressing data privacy and security concerns can be a significant challenge.

- Low Interest Rate Environment: Persistently low interest rates pose challenges for commercial banks, especially in economies with sluggish growth. Low interest rates compress net interest margins, reducing the profitability of traditional banking activities such as lending. Banks must explore alternative revenue streams and adopt efficient cost management strategies to navigate this challenge.

- Risk Management: Managing risks, such as credit risk, market risk, and operational risk, is a critical challenge for commercial banks. Assessing and mitigating risks in an increasingly complex and interconnected financial system requires sophisticated risk management frameworks and skilled personnel. Failure to effectively manage risks can lead to financial losses and damage banks’ reputation.

- Changing Customer Expectations: Customers’ expectations and preferences are continually evolving, driven by advancements in technology and changing demographics. Commercial banks must adapt to meet the demands of tech-savvy customers who expect seamless digital experiences, personalized services, and convenient access to banking services. Keeping up with changing customer expectations can be a challenge for traditional brick-and-mortar banks.

- Competition from Non-Traditional Financial Institutions: Commercial banks face competition from non-traditional financial institutions, such as fintech companies and big tech firms. These entities often leverage technology to offer innovative financial products and services, attracting customers with faster, more convenient, and lower-cost solutions. Commercial banks must embrace innovation and collaborate with fintech companies to stay competitive.

- Economic Uncertainty: Economic volatility and uncertainties, such as recessions, geopolitical events, and regulatory changes, can impact the financial health and stability of commercial banks. Economic downturns can lead to higher loan defaults and reduced business activities, resulting in lower profitability and increased credit risks for banks.

Commercial banks must proactively address these challenges to thrive in a dynamic and competitive banking landscape. Embracing innovation, enhancing risk management capabilities, investing in cybersecurity measures, and adapting to changing customer expectations are essential for commercial banks to remain resilient and sustainable in the face of these challenges.

Future Outlook of Commercial Banking

The commercial banking industry is evolving rapidly, driven by technological advancements, changing customer preferences, and regulatory developments. In the face of these changes, commercial banks must adapt and innovate to remain competitive and relevant. Let’s explore the future outlook of commercial banking:

- Digital Transformation: The future of commercial banking lies in embracing digital transformation. Banks are increasingly investing in digital platforms, mobile banking applications, and advanced technologies like artificial intelligence and data analytics. This shift toward digitalization aims to provide customers with seamless, personalized experiences and improve efficiency in banking operations.

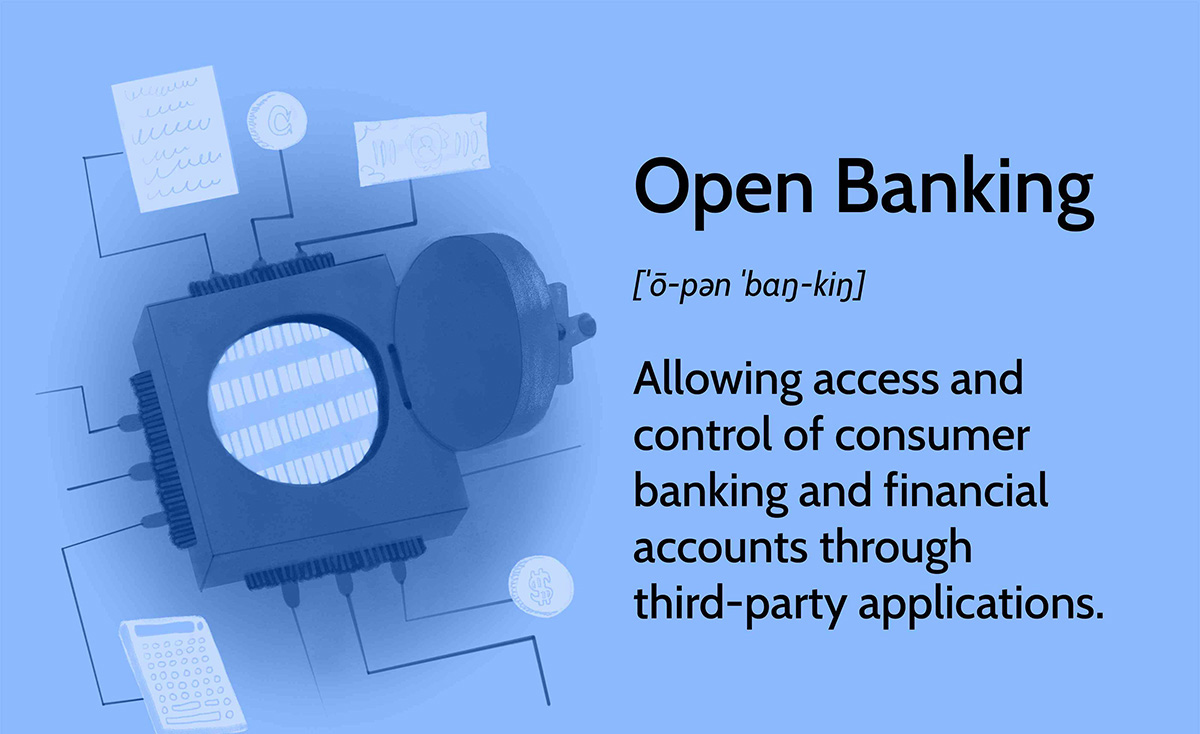

- Open Banking and Collaboration: Open banking, enabled by application programming interfaces (APIs) and data sharing, is a growing trend in the banking industry. Commercial banks are collaborating with fintech companies and other third-party providers to offer innovative services, such as account aggregation, personalized financial advice, and enhanced payment solutions. This collaboration allows banks to leverage the expertise and agility of fintech firms while maintaining customer trust and regulatory compliance.

- Enhanced Risk Management: As the banking landscape becomes increasingly complex, risk management will be paramount for commercial banks. Banks will focus on enhancing their risk management frameworks by leveraging advanced analytics, artificial intelligence, and machine learning algorithms to identify and mitigate risks more effectively. Incorporating robust risk management practices will ensure the financial stability and resilience of commercial banks.

- Focus on Customer Experience: Customer expectations are evolving, and commercial banks must prioritize delivering exceptional customer experiences. Banks will continue to invest in user-friendly interfaces, personalized services, and streamlined processes. Combining technology with human touchpoints will create a seamless and customer-centric banking experience.

- Sustainable Finance: Commercial banks have a critical role to play in promoting sustainable finance and addressing environmental and social challenges. They will increasingly focus on incorporating environmental, social, and governance (ESG) factors into their decision-making processes. Sustainable finance initiatives, such as green lending, socially responsible investments, and sustainable product offerings, will gain momentum in the future.

- Regulatory Compliance and Security: Regulatory requirements will continue to shape the commercial banking industry. Banks will need to stay abreast of evolving regulations related to cybersecurity, data privacy, anti-money laundering, and consumer protection. Investing in robust cybersecurity measures and ensuring compliance with regulatory standards will be crucial to maintain the trust and confidence of customers and regulators.

- Financial Inclusion: Commercial banks will have an ongoing commitment to promoting financial inclusion. They will work towards providing accessible and affordable banking services to underserved populations, leveraging technology to extend their reach and support financial literacy programs. This focus on financial inclusion will contribute to economic development and reduce inequalities.

The future of commercial banking holds both opportunities and challenges. By embracing technological advancements, prioritizing customer experience, strengthening risk management practices, and promoting sustainability, commercial banks can position themselves for long-term success in a rapidly evolving financial landscape.

Conclusion

Commercial banking plays a vital role in the economy as the backbone of the financial system. It serves as a financial intermediary, mobilizing savings, allocating capital, facilitating payments, and providing a range of services to individuals, businesses, and other entities. The importance of commercial banking is evident in its contribution to economic growth, stability, and financial inclusion. By promoting investment, entrepreneurship, and innovation, commercial banks fuel economic development, create job opportunities, and support businesses.

Commercial banks offer various services, including deposit accounts, lending facilities, payment processing, foreign exchange, investment advisory, and wealth management. These services cater to the diverse financial needs of customers and enable them to manage their finances effectively.

However, commercial banks also face challenges in an ever-changing landscape. They must adapt to technological advancements, enhance risk management capabilities, comply with evolving regulations, and meet the changing expectations of customers. The future of commercial banking lies in digital transformation, open banking collaboration, enhanced risk management, customer-centric approaches, sustainable finance initiatives, regulatory compliance, and financial inclusion.

In conclusion, commercial banking will continue to play a critical role in driving economic growth, promoting financial stability, and meeting the needs of individuals and businesses. By embracing innovation, adapting to changing market dynamics, and focusing on customer satisfaction and financial inclusion, commercial banks can navigate the challenges and seize the opportunities that lie ahead. Through their essential services and commitment to excellence, commercial banks will remain steadfast in supporting the growth and prosperity of the economy.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance