Home>Finance>How Is A Mutual Savings Bank Different From A Commercial Bank

Finance

How Is A Mutual Savings Bank Different From A Commercial Bank

Modified: February 21, 2024

Discover the key differences between mutual savings banks and commercial banks in the finance sector. Gain insights into their unique features and functions.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

Introduction

In the world of banking and finance, there are various types of institutions that cater to the needs of individuals and businesses. Among these institutions, two prominent ones are mutual savings banks and commercial banks. While they both serve the purpose of accepting deposits and providing loans, there are several key differences that set them apart.

In this article, we will delve into the definitions of mutual savings banks and commercial banks, explore their ownership structures, examine their purposes and missions, analyze their customer ownership models, investigate their profit distribution methods, discuss the types of services they provide, highlight their regulatory oversight, and explore their funding sources.

Understanding the distinctions between mutual savings banks and commercial banks is crucial for individuals and businesses alike. By gaining this knowledge, you can make more informed decisions when it comes to choosing the right banking institution for your financial needs.

So, let’s dive in and explore the fascinating world of mutual savings banks and commercial banks, and uncover what makes them unique.

Definition of a Mutual Savings Bank

A mutual savings bank is a type of financial institution that operates as a community-based, depositor-owned organization. Unlike traditional banks, which are typically owned by shareholders and operate with a profit-driven mindset, mutual savings banks are driven by the interests and needs of their depositors.

Mutual savings banks are rooted in a cooperative model where the depositors, also known as members, have a say in the bank’s operations. This means that individuals who have accounts with a mutual savings bank automatically become members and have the ability to vote on matters such as electing the bank’s board of directors and influencing its policies.

One key feature of mutual savings banks is their focus on providing services to individuals and communities. They often have a strong community presence and emphasize relationships with their customers. Mutual savings banks typically offer a range of services, including savings accounts, checking accounts, mortgages, personal loans, and small business loans.

Another defining aspect of mutual savings banks is their commitment to safety and stability. They are closely regulated by state or federal authorities to ensure the security of customer deposits and adherence to sound financial practices. This oversight aims to protect depositors from potential risks and ensure the long-term viability of the institution.

Due to their depositor-owned structure, mutual savings banks are driven by the interests of their members rather than maximizing profits for shareholders. As a result, they may be more focused on providing competitive interest rates, lower fees, and personalized customer service.

Overall, mutual savings banks stand out for their community focus, member-centric approach, and dedication to providing reliable financial services. As we move forward, let’s explore the characteristics and functions of commercial banks to gain a comprehensive understanding of the banking landscape.

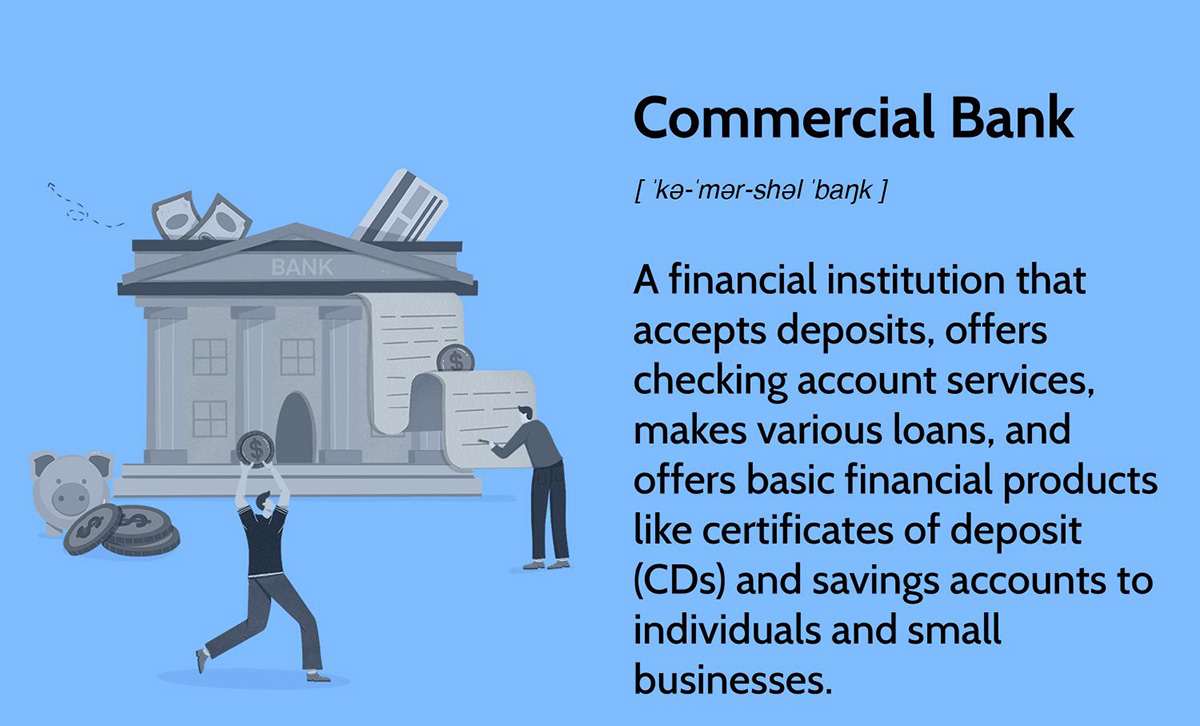

Definition of a Commercial Bank

A commercial bank is a financial institution that operates with the primary objective of making a profit by providing a wide range of financial services to individuals, businesses, and other organizations. Unlike mutual savings banks, which are depositor-owned, commercial banks are typically owned by shareholders and are driven by profit maximization.

Commercial banks play a crucial role in the economy by facilitating economic growth, supporting businesses, and providing essential banking services. They offer a wide array of products and services, including savings and checking accounts, loans, credit cards, investment services, and wealth management.

One distinguishing characteristic of commercial banks is their ability to create credit. They are authorized to accept deposits from customers and use a portion of those funds to provide loans and credit to other individuals and businesses. This process of creating credit plays a vital role in stimulating economic activity and investing in various sectors of the economy.

Commercial banks also play a significant role as intermediaries between savers and borrowers. They gather deposits from individuals and businesses and use those funds to provide loans and credit to borrowers who need capital for various purposes, such as expanding their businesses or purchasing properties.

Unlike mutual savings banks, commercial banks are profit-driven institutions that strive to generate revenue and increase shareholder value. Their primary sources of income include interest earned from loans and investments, fees and charges for services provided, and commissions from financial transactions.

Commercial banks operate in a highly regulated environment to ensure the stability and integrity of the financial system. They are subject to oversight from governmental authorities, such as central banks and banking regulators, which set prudential regulations and standards to safeguard the interests of depositors and ensure the overall soundness of the banking sector.

With their profit-oriented approach, extensive banking services, and role in credit creation and economic growth, commercial banks play a vital role in the financial system and serve as a cornerstone of modern economies.

Now that we have explored the definitions of mutual savings banks and commercial banks, let’s move on to understanding their ownership structures in more detail.

Ownership Structure

The ownership structures of mutual savings banks and commercial banks differ significantly, reflecting their distinct business models and objectives.

In the case of mutual savings banks, they are primarily owned by their depositors who hold accounts with the institution. These depositors are considered members of the bank and have certain rights, such as the ability to vote on important decisions affecting the bank’s operations, including the election of board members. This ownership structure creates a sense of community and involvement among depositors, with the mutual savings bank operating for the benefit of its members rather than shareholders seeking profits.

On the other hand, commercial banks operate under a shareholder ownership structure. This means that the bank is owned by individuals, corporations, or other financial institutions that hold shares of stock in the bank. The ownership stakes give these shareholders the right to participate in the bank’s decision-making processes, including the appointment of board members. The primary motive for shareholders in a commercial bank is to earn a return on their investment through dividend payments and an appreciation in the value of the bank’s stock.

This distinction in ownership structure has implications for how these banks prioritize their objectives and make decisions. Mutual savings banks, being owned by their depositors, tend to have a stronger focus on customer relationships and community impact rather than solely pursuing profit maximization. They are often deeply rooted in the communities they serve and may prioritize lending to local businesses and individuals to support economic development.

Commercial banks, as profit-driven institutions, prioritize generating returns for their shareholders. While they also provide essential banking services, their overarching goal is to maximize profitability and shareholder value. This may lead commercial banks to pursue strategies that optimize revenue generation and cost management, sometimes at the expense of personalized customer service or community engagement.

In summary, mutual savings banks are owned by their depositors, fostering a sense of community and customer-centric approach, while commercial banks are shareholder-owned and prioritize profit maximization. The ownership structure is a fundamental aspect that influences the direction and decision-making of these banks.

Next, we will explore the purpose and mission of mutual savings banks and commercial banks to understand their core objectives.

Purpose and Mission

The purpose and mission of mutual savings banks and commercial banks are driven by their distinct ownership structures and objectives.

Mutual savings banks have a strong focus on serving the needs of their depositors and the communities they operate in. They typically have a mission of providing accessible and affordable financial services to individuals and businesses, with an emphasis on local economic development. Mutual savings banks often prioritize building long-term relationships with their customers and promoting financial literacy and education within their communities.

Since mutual savings banks are depositor-owned institutions, their purpose is to benefit their members rather than shareholders. This can be seen in their commitment to customer satisfaction and offering competitive interest rates and fees. They may also have a mission of reinvesting a portion of their profits back into the community through social initiatives or charitable contributions.

On the other hand, commercial banks have a mission of maximizing profits for their shareholders. They are driven by the need to generate revenue, manage risk, and deliver competitive returns on investment. Commercial banks strive to achieve growth through expanding their customer base, increasing market share, and offering a wide range of financial products and services to attract customers.

The purpose and mission of commercial banks align with their profit-oriented ownership structure. They aim to optimize their operations, control costs, and enhance efficiency to generate higher profits. Commercial banks often emphasize innovation, technology, and market competition to gain a competitive edge in the financial industry.

While both mutual savings banks and commercial banks fulfill a critical role in the banking sector, their purposes and missions differ based on their ownership structures and primary objectives. Mutual savings banks focus on community involvement, customer satisfaction, and the well-being of their members, while commercial banks prioritize shareholder returns, profitability, and market competitiveness.

In the next section, we will discuss the customer ownership models of mutual savings banks and commercial banks.

Customer Ownership

The concept of customer ownership varies between mutual savings banks and commercial banks, reflecting the different ownership structures and priorities of these institutions.

In the case of mutual savings banks, the customers themselves, in the form of depositors, own the institution. When individuals open an account with a mutual savings bank, they become members of the bank, which grants them certain ownership rights and privileges. These rights typically include the ability to vote on major decisions, such as electing the bank’s board of directors and influencing the bank’s policies and practices.

This customer ownership model in mutual savings banks fosters a sense of community and involvement. The depositors have a stake in the institution and their interests align with the overall well-being and success of the bank. This can lead to a greater focus on meeting customer needs, delivering personalized service, and prioritizing the interests of the community in which the bank operates.

On the other hand, commercial banks operate under a different customer ownership model. While customers play a vital role by providing deposits and utilizing the bank’s services, they do not have an ownership stake in the institution. Instead, commercial banks are primarily owned by shareholders who hold shares of stock in the bank.

Customers of commercial banks have a different relationship with the institution. They are valued as customers and may influence the bank’s success through their choice to continue using the bank’s services, but they do not participate in decision-making or have voting rights. Commercial banks prioritize customer satisfaction to retain and attract customers, but the primary focus remains on generating profits for shareholders.

While the customer ownership model in mutual savings banks creates a sense of shared responsibility and alignment of interests, the model in commercial banks can lead to a more transactional relationship between the bank and its customers. The bank seeks to meet the needs of customers while maintaining profitability to satisfy shareholder expectations.

In summary, mutual savings banks have a customer ownership model where depositors become members with voting rights, allowing for a greater sense of community and involvement. Commercial banks, however, operate under a shareholder ownership model, where customers have a transactional relationship with the bank without ownership rights. Understanding these customer ownership models can shed light on the different priorities and dynamics present in mutual savings banks and commercial banks.

In the next section, we will explore the profit distribution methods employed by mutual savings banks and commercial banks.

Profit Distribution

The distribution of profits differs between mutual savings banks and commercial banks due to their distinct ownership structures and objectives.

In mutual savings banks, the depositors who are the members and owners of the institution play a central role in profit distribution. When the bank generates profits, it has several options for distributing them. One common approach is to reinvest the profits back into the institution to strengthen its capital base or expand its operations. This reinvestment can benefit depositors by enhancing the financial stability and growth prospects of the mutual savings bank.

Another method of profit distribution in mutual savings banks is in the form of patronage dividends. Instead of distributing the profits to shareholders, the bank may allocate a portion of the earnings to depositors based on their account activity, such as the amount of interest earned or fees paid. This approach rewards loyal depositors and incentivizes them to continue banking with the institution.

On the other hand, commercial banks have a different profit distribution model. As shareholder-owned entities, the primary objective of commercial banks is to generate profits for their shareholders. When a commercial bank earns profits, it typically allocates a portion of these earnings as dividends to the shareholders. Dividends represent a return on the shareholders’ investments and are distributed in proportion to their ownership stakes in the bank.

In addition to dividends, commercial banks may also allocate a portion of their earnings for reinvestment in the institution, such as for expanding operations, improving technology infrastructure, or pursuing strategic acquisitions. These reinvestments aim to enhance the bank’s profitability and long-term sustainability.

Profit distribution is a significant factor that distinguishes the objectives of mutual savings banks and commercial banks. Mutual savings banks prioritize the interests of their depositor-members, aiming to strengthen the institution and provide direct benefits to the depositors. In contrast, commercial banks focus on maximizing returns for their shareholders and maintaining long-term profitability.

It’s important to note that the specific profit distribution practices may vary among individual banks, depending on their policies, financial performance, and regulatory requirements. Nevertheless, comprehending the general patterns of profit distribution can provide insight into the alignment of interests and objectives in mutual savings banks and commercial banks.

In the next section, we will examine the types of services provided by both mutual savings banks and commercial banks.

Types of Services Provided

Mutual savings banks and commercial banks offer a wide range of financial services to meet the needs of individuals, businesses, and organizations. While there are some similarities in the services provided, there are also notable differences reflecting the diverse objectives and customer bases of these institutions.

Mutual savings banks typically offer traditional banking services, such as savings accounts, checking accounts, certificates of deposit (CDs), and individual retirement accounts (IRAs). These accounts provide a safe and convenient way for individuals to save money, earn interest, and manage their day-to-day finances.

They also provide lending services, including personal loans, home mortgages, and small business loans. Mutual savings banks often specialize in mortgage lending, offering competitive interest rates and personalized service to help individuals achieve their dream of homeownership. They may also have a focus on lending to local businesses, supporting economic growth and development in their communities.

Moreover, mutual savings banks may offer investment services and products, such as mutual funds, annuities, and brokerage services. These services aim to provide individuals with opportunities to grow and diversify their investments and plan for long-term financial goals.

Commercial banks, in addition to offering traditional banking services like savings and checking accounts, also provide extensive lending services to individuals and businesses. They offer a variety of loans, including personal loans, auto loans, home mortgages, commercial real estate loans, and lines of credit. Commercial banks often have specialized departments that cater to the specific needs of businesses, such as offering business lines of credit, equipment financing, and working capital loans.

Commercial banks excel in trade finance, providing services such as letters of credit, trade guarantees, and foreign exchange transactions to facilitate international trade. They also offer treasury services, helping businesses manage their cash flow, liquidity, and risk through services like cash management, online banking, and merchant services.

Furthermore, commercial banks have a strong presence in the investment realm, offering brokerage services, wealth management, retirement planning, and other investment advisory services. They provide access to a wide range of investment products, including stocks, bonds, mutual funds, and various managed portfolios.

It is important to note that the specific types of services offered may vary among individual banks, as they tailor their offerings to meet the demands of their target customer base and market segment.

Summing up, while both mutual savings banks and commercial banks provide essential banking services, mutual savings banks often emphasize community-focused lending and customer-oriented services, while commercial banks excel in a broader range of offerings, including specialized business services and investment products. Understanding the types of services provided by these institutions is crucial in selecting the right banking partner that aligns with your financial needs and goals.

In the next section, we will discuss the regulation and oversight of mutual savings banks and commercial banks.

Regulation and Oversight

The regulation and oversight of mutual savings banks and commercial banks ensure the stability, safety, and integrity of the banking industry, providing confidence to depositors and maintaining the overall financial system.

Mutual savings banks, like all banks, are subject to stringent regulation and supervision by relevant banking authorities, which can be either state or federal, depending on the jurisdiction. These regulatory bodies set specific guidelines and standards that mutual savings banks must adhere to in areas such as capital adequacy, liquidity, risk management, and consumer protection.

The regulatory framework for mutual savings banks ensures that these institutions operate in a financially sound manner, protecting the interests of depositors and maintaining the deposit insurance coverage provided by entities such as the Federal Deposit Insurance Corporation (FDIC). This coverage protects depositors’ funds up to a certain limit in case of a bank failure.

In addition to regulations specific to banking, mutual savings banks may also be subject to community reinvestment requirements. These requirements encourage the banks to meet the credit needs of their communities, particularly in underserved areas, by providing loans and financial services to support community development and affordable housing initiatives.

Similarly, commercial banks are subject to comprehensive regulation and oversight by governmental authorities, such as central banks and banking regulators. These oversight agencies establish prudential regulations and standards to ensure the stability and integrity of the banking system.

Commercial banks are required to meet capital adequacy requirements, manage liquidity risks effectively, and implement robust risk management practices. They are also subject to regulations related to anti-money laundering (AML) and combating the financing of terrorism (CFT) to prevent illicit financial activities.

Commercial banks are often subject to additional regulations due to their broader range of services and activities. For example, banks that engage in investment banking, securities trading, or wealth management services are subject to regulations specific to those activities, including securities laws and regulations imposed by entities such as the Securities and Exchange Commission (SEC).

The regulatory oversight of mutual savings banks and commercial banks aims to protect depositors, maintain the stability of the financial system, and ensure fair and transparent banking practices. Compliance with these regulations is crucial for both types of institutions to operate responsibly and maintain the trust of their customers and stakeholders.

In the next section, we will explore the funding sources of mutual savings banks and commercial banks.

Funding Sources

Mutual savings banks and commercial banks rely on different funding sources to support their operations and meet the deposit and lending needs of their customers.

Mutual savings banks primarily rely on customer deposits as their main source of funding. When individuals open savings accounts, checking accounts, or other deposit accounts with a mutual savings bank, the funds deposited by customers serve as a crucial source of liquidity for the institution. These deposits provide the base upon which the bank can lend to individuals and businesses.

Customer deposits are vital for mutual savings banks because they represent a stable and cost-effective funding source. Depositors entrust their money to the bank, which, in turn, utilizes those funds to provide loans and other financial services to customers. Mutual savings banks aim to attract and retain depositors by offering competitive interest rates, personalized service, and a local community focus.

Commercial banks, in addition to customer deposits, have access to a wider range of funding sources. While customer deposits remain a significant component of their funding, commercial banks can also raise capital through other means. This includes borrowing from other financial institutions, issuing debt securities such as bonds, or raising equity capital by issuing shares of stock to investors.

Furthermore, commercial banks can access funding from interbank markets, where banks lend to and borrow from each other to manage short-term liquidity needs. They can also seek funding from central banks through various facilities to maintain liquidity and manage any cash flow imbalances.

Commercial banks have more flexibility in diversifying their funding sources due to their business model and wider range of activities. This allows them to tap into different funding options, including wholesale funding from institutional investors, securitization of loan portfolios, and engaging in repurchase agreements and money market operations.

It’s worth noting that the ability to tap into various funding sources comes with additional scrutiny and regulatory requirements for commercial banks. These regulations aim to ensure the stability and solvency of the institution and the overall financial system.

In summary, mutual savings banks primarily rely on customer deposits as their primary funding source, while commercial banks have access to a broader range of funding options, including customer deposits, borrowing from other financial institutions, issuing debt securities, and raising equity capital. Understanding the funding sources of these banks provides insights into their financial stability, growth potential, and ability to meet the borrowing and lending needs of their customers.

Now that we have explored the various aspects of mutual savings banks and commercial banks, let’s conclude our discussion.

Conclusion

From understanding the definitions to exploring the ownership structures, purposes, customer ownership models, profit distribution methods, types of services provided, regulation and oversight, and funding sources, we have gained a comprehensive understanding of the differences between mutual savings banks and commercial banks.

Mutual savings banks, with their depositor-owned structure, emphasize community involvement, customer satisfaction, and community impact. They prioritize the interests of their members and often have a strong presence in the communities they serve.

On the other hand, commercial banks, being shareholder-owned institutions, prioritize profit maximization and shareholder returns. They offer a broader range of services, have a wider scope of activities, and focus on market competitiveness and efficiency.

While both types of banks provide essential financial services such as savings and checking accounts, loans, and investment products, the emphasis may differ. Mutual savings banks may have a community-focused lending approach and a commitment to financial education, while commercial banks may offer specialized business services and a more extensive range of investment options.

The regulation and oversight of both types of banks ensure the stability, safety, and fairness of the banking industry. Regulations are in place to protect depositors, manage risks, prevent money laundering, and maintain the integrity of the financial system.

In terms of funding, mutual savings banks primarily rely on customer deposits, while commercial banks have access to a wider range of funding sources, including customer deposits, interbank borrowing, debt securities, and equity capital.

Understanding these differences allows individuals and businesses to make informed choices when selecting a banking partner. Consider factors such as community involvement, customer service, specialization, profitability, and the specific financial needs and goals to make the best decision.

In conclusion, mutual savings banks and commercial banks operate with distinct models, ownership structures, and objectives. Both play significant roles in the financial industry, serving the needs of individuals, businesses, and communities, albeit with different emphases and priorities. By understanding these differences, individuals and organizations can make informed decisions to meet their financial needs and goals effectively.

What's Hot

Latest Articles

Related Post

By: Chelsea • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance