Home>Finance>How Do Investment Banks Differ From Commercial Banks?

Finance

How Do Investment Banks Differ From Commercial Banks?

Published: October 18, 2023

Learn the key differences between investment banks and commercial banks in finance, including their roles, services, and regulations.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

How Do Investment Banks Differ From Commercial Banks?

Introduction

When it comes to the world of finance, there are various types of banks that play distinct roles in the economy. Two prominent types are investment banks and commercial banks.

Investment banks and commercial banks might seem similar at first glance, as both entities are involved in financial transactions. However, they serve different purposes and operate in distinct ways. Understanding the differences between investment banks and commercial banks is crucial for individuals looking to navigate the financial landscape and make informed decisions.

Investment banks primarily focus on assisting corporations, governments, and other entities in raising capital by issuing stocks and bonds. They facilitate large-scale financial transactions, such as initial public offerings (IPOs), mergers and acquisitions, and underwriting securities. Investment banks also offer advisory services to clients regarding investment strategies, market analysis, and risk management.

In contrast, commercial banks cater to a broader range of services. They are primarily responsible for accepting deposits from individuals and businesses and providing financial services such as loans, mortgages, and checking accounts. Commercial banks also handle routine banking activities like consumer transactions and managing savings accounts.

While both investment banks and commercial banks deal with money and provide financial services, their core functions and operations set them apart. It is important to delve deeper into each type of bank to understand their unique characteristics, financing activities, risk profiles, and regulatory differences.

Definition of Investment Banks

Investment banks are financial institutions that specialize in offering a range of financial services to corporations, governments, and institutional clients. Unlike commercial banks, which focus on traditional banking activities like accepting deposits and providing loans, investment banks primarily engage in activities related to capital markets and investment banking.

Investment banks play a crucial role in facilitating the issuance of securities, such as stocks and bonds, through underwriting services. They act as intermediaries between issuers of securities and potential investors, helping companies raise capital for expansion, acquisitions, or other financial needs.

Additionally, investment banks provide advisory services to clients. This includes offering expertise on mergers and acquisitions, corporate restructuring, valuations, and strategic financial planning. Investment banks assist companies in making informed financial decisions, maximizing shareholder value, and navigating complex financial transactions.

Furthermore, investment banks engage in proprietary trading, which involves buying and selling financial products on their own behalf to generate profits. They also manage investment portfolios on behalf of clients, providing investment management services and insights into market trends.

The operations of investment banks can vary depending on the size and scope of the institution. Some investment banks operate globally and offer a wide array of financial services, while others specialize in specific sectors or regions. Regardless of their size, investment banks are known for their expertise in capital markets, financial advisory, and their ability to access and analyze market information to make informed investment decisions.

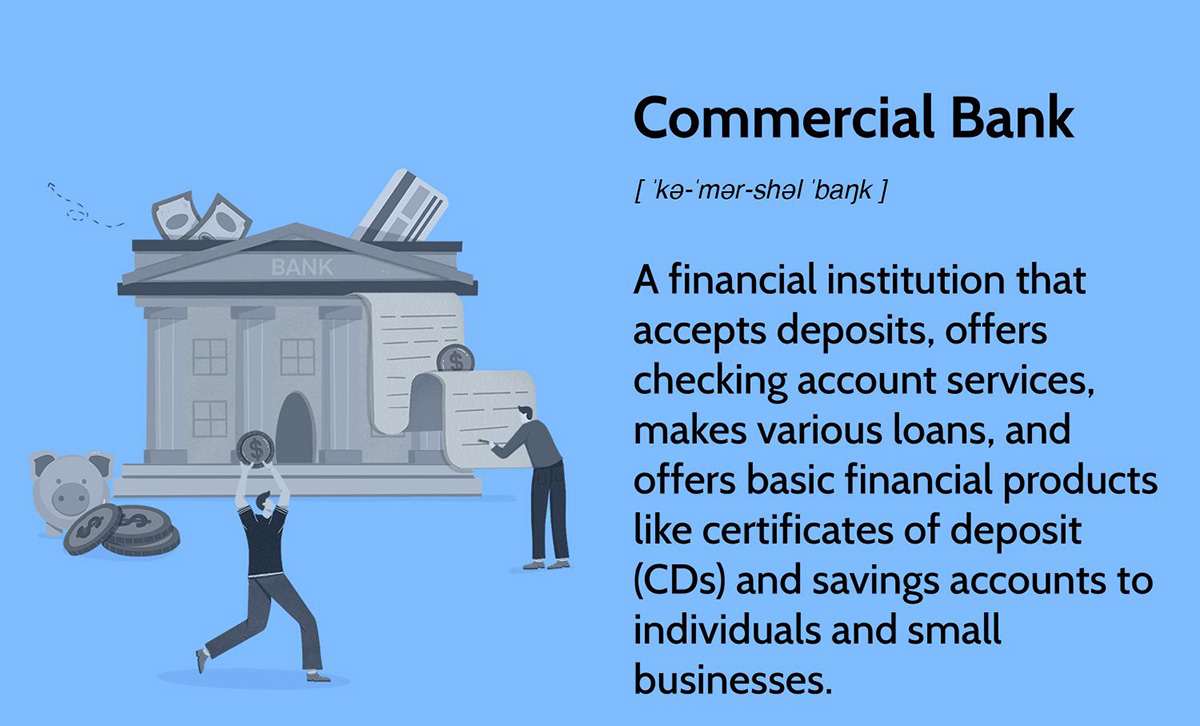

Definition of Commercial Banks

Commercial banks are financial institutions that primarily focus on providing a wide range of services to individual customers, small businesses, and large corporations. They are the most common type of bank that individuals interact with on a daily basis for their banking needs.

One of the primary functions of commercial banks is accepting deposits from individuals and businesses. They offer various types of accounts, such as savings accounts, checking accounts, and certificates of deposit (CDs), which allow customers to securely store their money and earn interest.

In addition to accepting deposits, commercial banks provide loans to individuals and businesses. This includes personal loans, home mortgages, auto loans, and business loans. Commercial banks play a vital role in facilitating economic growth by providing capital to individuals and businesses to meet their financial needs.

Furthermore, commercial banks offer other essential financial services such as money transfers, credit cards, debit cards, and electronic banking facilities. They also provide services like financial advisory, wealth management, and safekeeping of valuable assets in safety deposit boxes.

Another key function of commercial banks is the creation of credit. They have the ability to create credit by lending out more money than they actually have in deposits, relying on the assumption that not all depositors will ask for their money back at once. This credit creation helps stimulate economic activity and contributes to the overall growth of the economy.

Commercial banks are regulated by central banks and government authorities to ensure stability and safety in the financial system. They are required to maintain a certain level of reserve to meet potential demands for withdrawals and adhere to regulatory guidelines to protect the interests of their depositors.

In summary, commercial banks are financial institutions that provide a wide range of banking services to individuals and businesses. They handle deposits, offer loans, facilitate transactions, and play a crucial role in supporting economic activities on both a small and large scale.

Core Functions of Investment Banks

Investment banks serve a distinct role in the financial industry, focusing on specialized services related to capital markets and investment banking. Here are the core functions of investment banks:

- Underwriting and Issuing Securities: One of the primary functions of investment banks is to assist companies, governments, and other entities in issuing securities such as stocks and bonds. Investment banks play a vital role in underwriting these securities, which involves pricing and selling them to potential investors.

- Merger and Acquisition Advisory: Investment banks provide expert advice and assistance to companies engaged in mergers, acquisitions, and other corporate restructuring activities. They help navigate complex transactions, conduct valuations, and ensure that the interests of all parties involved are protected.

- Corporate Finance and Fundraising: Investment banks offer financial advisory services to companies seeking to raise capital for various purposes, such as expansion, research and development, or debt refinancing. They help identify suitable funding sources, develop financing strategies, and structure deals to meet the specific needs of their clients.

- Trading and Market Making: Investment banks engage in proprietary trading, where they trade on their own behalf to generate profits. They also act as market makers, providing liquidity by buying and selling securities, thereby ensuring efficient and smooth market operations.

- Research and Analysis: Investment banks employ teams of research analysts who provide in-depth market research, analysis, and insights. This research helps clients make informed investment decisions, understand market trends, and assess the performance of companies and industries.

- Asset Management: Many investment banks offer asset management services to institutional clients and high-net-worth individuals. They manage investment portfolios, provide investment advice, and help clients achieve their financial goals through proper asset allocation and risk management strategies.

These core functions of investment banks reflect their specialized focus on capital markets, corporate finance, and advisory services. Investment banks play a critical role in facilitating financial transactions, supporting the growth of businesses, and providing valuable insights and expertise to clients in navigating the complexities of the financial landscape.

Core Functions of Commercial Banks

Commercial banks perform a range of essential functions that cater to the banking needs of individuals, small businesses, and corporations. Here are the core functions of commercial banks:

- Accepting Deposits: One of the primary functions of commercial banks is to accept deposits from individuals and businesses. They offer various types of accounts, such as savings accounts, checking accounts, and certificates of deposit (CDs), where customers can securely store their money and earn interest.

- Providing Loans and Credit: Commercial banks lend money to customers and businesses to meet their financial needs. They offer a variety of loan products, including personal loans, home mortgages, auto loans, and business loans. Commercial banks play a vital role in providing capital to individuals and businesses, fostering economic growth.

- Facilitating Transactions: Commercial banks enable customers to make financial transactions. This includes services such as money transfers, wire transfers, cashiers’ checks, and electronic banking facilities. Commercial banks facilitate the movement of funds domestically and internationally, ensuring the efficient and secure transfer of money.

- Credit Card and Debit Card Services: Commercial banks issue credit cards and debit cards to customers, providing them with convenient payment options. These cards enable customers to make purchases and access funds from their accounts, both in-person and online.

- Electronic Banking Services: Commercial banks offer electronic banking services, allowing customers to access and manage their accounts online. This includes features such as online banking, mobile banking applications, and electronic bill payment services. These services provide customers with convenience and flexibility in managing their finances.

- Financial Advisory and Wealth Management: Many commercial banks provide financial advisory services to customers. This includes investment advice, retirement planning, and wealth management services. Commercial banks help individuals and businesses make informed financial decisions and achieve their long-term financial goals.

In addition to these core functions, commercial banks also play a crucial role in creating credit, stimulating economic activity, and contributing to the overall stability of the financial system. They are regulated by central banks and government authorities to ensure the safety and integrity of the banking system.

Overall, commercial banks serve as the backbone of the banking industry, providing a wide range of essential services that meet the diverse banking needs of individuals and businesses.

Differences in Financing Activities

One of the key distinctions between investment banks and commercial banks lies in their financing activities. While both types of banks are involved in financial transactions, the nature and focus of their financing activities differ significantly.

Investment Banks: Investment banks primarily focus on facilitating capital market transactions and providing advisory services to corporations and institutional clients. Their financing activities revolve around raising capital, underwriting securities, and engaging in proprietary trading.

Investment banks assist companies in raising capital by issuing securities such as stocks and bonds. They play a crucial role in underwriting these securities, meaning they assume the risk of purchasing the securities from the issuer and reselling them to investors. By doing so, investment banks enable companies to access funding for various purposes, such as expansion, acquisitions, or debt refinancing.

Additionally, investment banks engage in proprietary trading, where they trade financial products using the bank’s own capital. This activity is aimed at generating profits for the bank and often involves buying and selling securities, commodities, and derivatives.

Commercial Banks: Commercial banks, on the other hand, focus on lending and accepting deposits from individuals and businesses. Their financing activities primarily involve providing loans and credit to customers.

Commercial banks play a critical role in the economy by providing financial assistance to individuals and businesses. They accept deposits from customers, creating a pool of funds that can be lent out to borrowers. Commercial banks offer a variety of loan products, including personal loans, mortgages, business loans, and credit lines. Their financing activities help individuals purchase homes, buy cars, start businesses, and meet various financial needs.

In addition to lending, commercial banks also engage in other financing activities such as issuing credit cards, providing overdraft facilities, and offering trade finance services to support international trade transactions.

Overall, investment banks focus on capital market transactions and raising capital through securities issuance and proprietary trading, while commercial banks concentrate on lending activities and accepting deposits to provide financial support to individuals and businesses.

Differences in Risk Profiles

Investment banks and commercial banks differ in their risk profiles due to the distinct nature of their operations and financial activities. Understanding these differences is essential for assessing the risk exposure of each type of bank.

Investment Banks: Investment banks typically have a higher risk profile compared to commercial banks. This is primarily due to their involvement in capital market activities, proprietary trading, and advisory services.

Investment banks often handle large-scale financial transactions, such as initial public offerings (IPOs), mergers and acquisitions, and underwriting securities. These activities involve a certain level of market risk and sensitivity to external factors, such as economic conditions, market fluctuations, and regulatory changes.

Additionally, investment banks engage in proprietary trading, which entails trading financial products on their own behalf to generate profits. While this activity can be lucrative, it also carries inherent risks associated with market volatility and the bank’s ability to accurately anticipate market movements.

Furthermore, investment banks provide advisory services to clients, which entails offering financial guidance and recommendations. While investment banks strive to provide accurate advice, there is a risk that market conditions or unforeseen events may impact the performance of investments, potentially leading to financial losses and reputational risks.

Commercial Banks: Commercial banks generally have a lower risk profile compared to investment banks. This is primarily due to their focus on traditional banking activities, such as accepting deposits, providing loans, and offering basic financial services.

Commercial banks primarily engage in lending activities, where risks are assessed through credit analysis, collateral requirements, and stringent underwriting processes. Although there is still some credit risk involved, commercial banks have established risk management frameworks to mitigate these risks and ensure the repayment of loans.

Since commercial banks primarily accept deposits from individuals and businesses, they have a stable source of funding in the form of customer deposits. This mitigates liquidity risk and reduces their reliance on external sources of funding. They also have access to central bank facilities and interbank lending to manage potential liquidity concerns.

While commercial banks are exposed to general economic risks and fluctuations, their risk profiles are typically more stable due to their diversified customer base and broad range of banking services.

It is important to note that both investment banks and commercial banks are subject to regulatory oversight and risk management requirements. However, the nature of their operations and the types of risks they face differ, leading to varying risk profiles for each type of bank.

Regulatory Differences

Investment banks and commercial banks are subject to different regulatory frameworks and oversight due to the distinct nature of their operations and the risks they pose to the financial system. These regulatory differences contribute to variations in capital requirements, risk management practices, and reporting obligations.

Investment Banks: Investment banks are typically regulated as part of the broader financial services sector, with oversight from regulatory bodies such as the Securities and Exchange Commission (SEC) in the United States or the Financial Conduct Authority (FCA) in the United Kingdom.

Investment banks are subject to regulations that focus on capital market activities, securities underwriting, and trading activities. The regulatory framework aims to ensure fair and transparent capital market operations, protect the interests of investors, and maintain market stability.

Regulations for investment banks often include requirements related to capital adequacy, risk management, compliance, and disclosure. Investment banks are required to maintain sufficient capital to support their operations and withstand potential market shocks. They are also expected to implement robust risk management practices to identify, assess, and mitigate risks associated with market activities and client engagements.

Furthermore, investment banks are subject to regulations surrounding insider trading, conflicts of interest, and transparency in their dealings. They are required to adhere to strict compliance procedures and regulatory reporting obligations to ensure regulatory compliance and maintain the integrity of the financial system.

Commercial Banks: Commercial banks are subject to a different set of regulatory frameworks that focus on safeguarding customer deposits, maintaining financial stability, and ensuring the safety and soundness of the banking system as a whole.

Commercial banks are typically regulated by banking authorities and central banks, such as the Federal Reserve in the United States or the European Central Bank (ECB) in the Eurozone. These regulatory bodies have oversight over banks’ operations, capital requirements, lending practices, and risk management.

Regulations for commercial banks emphasize factors such as capital adequacy, liquidity management, credit risk assessment, and consumer protection. Commercial banks are required to hold a certain amount of capital to support their lending activities and absorb potential losses. They must also adhere to specific liquidity ratios to ensure they have sufficient reserves to meet customer deposit withdrawals and other financial obligations.

Moreover, commercial banks are subject to regulations surrounding lending practices, interest rates, consumer protection, anti-money laundering measures, and data privacy. These regulations are in place to ensure fairness, transparency, and the protection of customer interests in the banking relationship.

In summary, investment banks and commercial banks operate under different regulatory frameworks that reflect the unique risks associated with their respective business models. Investment banks face regulations that focus on capital market activities and securities trading, while commercial banks adhere to regulations designed to safeguard customer deposits and maintain financial stability.

Conclusion

Investment banks and commercial banks play crucial roles in the financial industry, but they differ significantly in their functions, financing activities, risk profiles, and regulatory oversight.

Investment banks focus on capital market activities, including underwriting securities, advisory services, and proprietary trading. They assist companies in raising capital, facilitate mergers and acquisitions, and provide valuable insights and expertise to clients. Investment banks typically have higher risk profiles due to their exposure to market fluctuations and their involvement in complex financial transactions.

On the other hand, commercial banks primarily engage in traditional banking activities such as accepting deposits and providing loans. They cater to the banking needs of individuals and businesses, offering a wide range of financial services. Commercial banks have lower risk profiles compared to investment banks, as their operations are centered around lending and customer deposits.

The regulatory frameworks for investment banks and commercial banks differ as well. Investment banks are regulated by bodies such as the SEC or FCA, with regulations focusing on capital market activities and securities trading. Commercial banks are regulated by banking authorities and central banks, placing emphasis on customer deposit protection, financial stability, and consumer protection.

Understanding these differences is vital for individuals, businesses, and policymakers in navigating the financial landscape and making informed decisions. Whether it’s raising capital, obtaining a loan, or seeking financial advice, knowing the distinctions between investment banks and commercial banks can help optimize financial strategies and mitigate risks.

In summary, investment banks and commercial banks are essential institutions within the financial sector, each with its own distinct roles, functions, risk profiles, and regulatory frameworks. By recognizing these differences, individuals and businesses can better navigate the financial landscape and make informed decisions tailored to their specific needs and goals.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance