Home>Finance>Explain What The Credit Terms Of 2/10 N/30 Mean.

Finance

Explain What The Credit Terms Of 2/10 N/30 Mean.

Published: January 10, 2024

Discover the meaning of the credit terms 2/10 N/30 in the world of finance and learn how it impacts your bottom line.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

Introduction

Welcome to the world of credit terms! When it comes to financial transactions, understanding the language and terminology used is crucial. One such term that often perplexes many is “2/10 N/30.”

In the realm of finance, credit terms refer to the payment conditions established between a buyer and a seller. These terms outline the time frame within which the buyer must make payment, any available discounts, and consequences for late or nonpayment. Essentially, credit terms provide the guidelines for invoicing and payment processes.

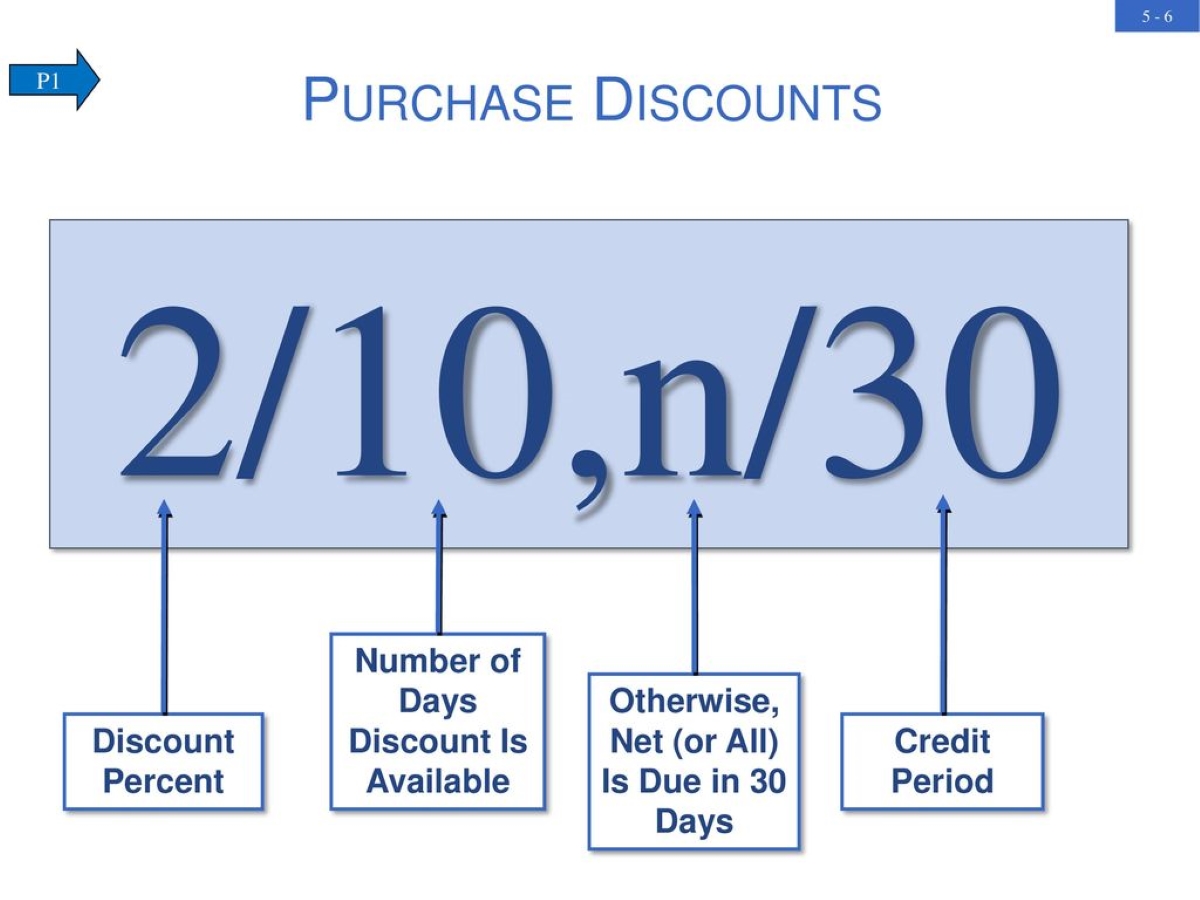

The credit term “2/10 N/30” is a common abbreviation used in the business world. It may seem like a cryptic code, but fear not – allow me to decode it for you.

Essentially, “2/10 N/30” breaks down into two components: the discount and the payment term. The first part, “2/10,” indicates that the buyer is eligible for a 2% discount if payment is made within a specified period of time. The second part, “N/30,” represents the time frame within which the buyer is expected to make payment in full without incurring any penalties.

Now that we have a general understanding of what “2/10 N/30” means, let’s examine each component in more detail to uncover its true significance and implications.

Definition of Credit Terms

In the realm of finance, credit terms refer to the conditions and agreements established between a buyer and a seller regarding the payment of goods or services. These terms serve as a way to outline the expectations and responsibilities of both parties during the transaction process.

Credit terms encompass various factors, including the time frame for payment, any available discounts, and consequences for late or nonpayment. They establish the structure and guidelines for invoicing, collection, and payment processes.

By defining the specific credit terms for a transaction, both the buyer and seller can avoid misunderstandings and ensure a smooth and efficient payment process. These terms provide clarity and accountability, helping to facilitate trust and maintain a healthy business relationship.

In addition to maintaining clear communication and expectations, credit terms also play a crucial role in budgeting and cash flow management for both parties. By establishing payment schedules and discounts, credit terms enable businesses to plan their cash flow effectively and optimize their working capital.

Different industries and companies may have their own variations of credit terms, tailored to their specific needs and circumstances. However, some common credit terms include net 30, net 60, net 90, 2/10 net 30, and 3/15 net 40.

Now that we have a broader understanding of credit terms, let’s delve deeper into the specifics of a popular credit term: “2/10 N/30.”

Explanation of 2/10 N/30

Now, let’s uncover the meaning behind the credit term “2/10 N/30.” As mentioned earlier, this term consists of two components: the discount and the payment term.

The first part, “2/10,” refers to a cash discount available to the buyer. Specifically, it means that the buyer is eligible for a 2% discount if the payment is made within a specified period of time. In this case, the buyer has a window of 10 days to make the payment in order to take advantage of the discount.

The second part, “N/30,” signifies that the buyer is expected to make full payment within 30 days. The “N” stands for “net,” which means the buyer is required to pay the full amount. Failure to do so within the given time frame may result in losing the eligibility for the discount and potentially incurring penalties or interest charges.

In summary, “2/10 N/30” offers a 2% discount if the payment is made within 10 days, with the full payment due within 30 days.

These credit terms are commonly used in the business-to-business (B2B) realm, where sellers often provide incentives in the form of discounts to encourage prompt payments from buyers. The aim is to incentivize early payment and improve the cash flow of the seller while providing cost savings to the buyer.

It’s important to note that the specified time frames for the discount and payment can vary depending on the agreement between the buyer and the seller. While “2/10 N/30” is a common example, other variations such as “1/10 N/45” or “3/10, net 60” may be used based on the specific needs and circumstances of the parties involved.

By understanding the meaning of “2/10 N/30,” both buyers and sellers can navigate the payment process more effectively and take advantage of potential discounts, ultimately benefiting both parties.

The Meaning of “2/10”

Now let’s take a closer look at the first component of the credit term “2/10 N/30” – the “2/10” part. This segment represents the cash discount offered by the seller to the buyer.

In simple terms, “2/10” means that the buyer is entitled to a discount of 2% if payment is made within a specified period of time. In this case, the buyer has a 10-day window to make the payment and take advantage of the discount.

The purpose of offering this cash discount is to incentivize prompt payment from the buyer. By providing a financial incentive, the seller hopes to encourage the buyer to settle the invoice sooner, thereby improving their own cash flow and reducing the risk of delayed payments.

It’s worth noting that the discount percentage can vary depending on the agreement between the buyer and seller. While “2/10” is a commonly used example, other variations may exist, such as “1/10” or “3/10.” The discount percentage is usually determined based on factors such as industry norms, competition, and the financial health of the seller.

These discounted payment terms can be particularly beneficial for buyers who have the financial capability to make early payments. By taking advantage of the cash discount, buyers can save on their purchase costs and improve their own cash flow management.

However, it’s important to evaluate the potential savings against other investment opportunities or cash needs before deciding to take the discount. Sometimes, the opportunity cost of forgoing the discount and utilizing the cash elsewhere may outweigh the benefit of the discount itself.

In summary, the “2/10” component of the credit term “2/10 N/30” signifies a 2% cash discount offered to the buyer if payment is made within 10 days. This discount serves as an incentive for the buyer to settle the invoice promptly and has the potential to enhance cost savings and cash flow management.

The Meaning of “N/30”

Now, let’s delve into the second component of the credit term “2/10 N/30” – the “N/30” part. This part signifies the payment term or the time frame within which the buyer is expected to make full payment.

In this context, “N” stands for “net,” indicating that the buyer is required to pay the full amount without any deductions or discounts. The “30” represents the number of days within which the payment must be made.

Essentially, the term “N/30” means that the buyer is obligated to make full payment within 30 days from the invoice date. Failure to comply with the payment terms may result in consequences such as losing the eligibility for any discounts, incurring penalties, or even damaging the business relationship with the seller.

For sellers, this credit term provides them with a specific timeline for receiving payment. It allows them to manage their cash flow and budget more effectively, as they can expect to receive payment within the specified period.

Buyers, on the other hand, are required to carefully manage their payment obligations and ensure prompt payment within the given timeframe. Adhering to the payment terms is crucial to maintain a good credit standing and foster positive relationships with suppliers.

It’s important for buyers to review their cash flow projections and consider the impact of timely payment on their overall financial position. By making payments within the stipulated time, buyers can demonstrate their reliability and potentially negotiate better terms or discounts in future transactions.

Different variations of the “N/30” term may exist, such as “N/45” or “N/60,” depending on the respective agreement between the buyer and seller. These variations can provide extended payment periods, allowing buyers more time to settle their invoices.

In summary, the term “N/30” in the credit term “2/10 N/30” implies that the buyer is required to make full payment within 30 days without any deductions or discounts. Adhering to the payment terms is essential to maintain a positive business relationship and ensure smooth financial operations.

Implications of 2/10 N/30 Credit Terms

The credit terms “2/10 N/30” have several implications for both buyers and sellers. Let’s explore some of the key implications of these credit terms.

- Prompt Payment Incentive: The availability of a 2% cash discount within 10 days serves as a significant incentive for buyers to make early payments. This encourages prompt payment and helps improve the seller’s cash flow.

- Cost Savings for Buyers: By taking advantage of the cash discount, buyers can lower their purchase costs. This can be particularly beneficial for buyers who have the financial capability to make early payments and can result in significant savings over time.

- Improved Cash Flow for Sellers: The discount offered in “2/10 N/30” incentivizes buyers to settle their invoices earlier, which in turn improves the seller’s cash flow. This steady cash flow allows sellers to meet their own financial obligations and invest in business growth initiatives.

- Potential Strain on Buyer’s Cash Flow: While the discount can be advantageous, buyers need to evaluate their cash flow situation and ensure they can comfortably meet the payment deadline. Neglecting to assess their financial position may cause strain on their cash flow, impacting their ability to fulfill other financial obligations.

- Increased Buyer-Seller Relationship: The credit terms help establish clear expectations for both parties, fostering transparency and trust. By adhering to the agreed-upon terms, buyers and sellers can develop a mutually beneficial relationship built on reliability and promptness.

In summary, the credit terms “2/10 N/30” have implications for both buyers and sellers. These terms encourage prompt payment and provide cost savings for buyers, while improving the cash flow and maintaining steady revenue for sellers. However, buyers must carefully assess their cash flow capabilities to ensure they can meet the payment deadline without placing undue strain on their financial position. Overall, these credit terms can facilitate positive buyer-seller relationships and contribute to the smooth functioning of business transactions.

Benefits of Using 2/10 N/30 Credit Terms

The credit terms “2/10 N/30” offer several benefits for both buyers and sellers. Let’s explore some of the key advantages of using these credit terms.

- Improved Cash Flow Management: For sellers, offering a cash discount for early payment incentivizes buyers to settle their invoices sooner. This results in a more consistent and predictable cash flow, allowing sellers to meet their financial obligations and invest in business growth initiatives.

- Cost Savings for Buyers: Buyers who have the financial capability to make early payments can take advantage of the 2% discount. This reduces their purchase costs and can result in substantial savings over time.

- Enhanced Buyer-Seller Relationship: The credit terms provide a clear framework and expectations for both buyers and sellers. By adhering to the agreed-upon terms, a sense of trust and reliability is fostered between the parties, leading to stronger long-term relationships.

- Incentive for Prompt Payments: The availability of a cash discount encourages buyers to make timely payments to take advantage of the savings. This reduces the risk of delayed or late payments, benefiting both parties involved.

- Better Cash Flow Projection: Within the “2/10 N/30” credit terms, sellers can anticipate a higher likelihood of receiving payment within the discount period. This allows for more accurate cash flow projections, enabling better planning and decision-making.

It’s important to note that the benefits of using “2/10 N/30” credit terms may vary depending on the specific circumstances and financial capabilities of the parties involved. Some buyers may find it financially advantageous to take advantage of the discount, while others may prioritize managing their cash flow differently.

Overall, “2/10 N/30” credit terms offer numerous benefits, including improved cash flow management, cost savings for buyers, strengthened relationships, incentivized prompt payments, and better cash flow projections. These advantages contribute to the smooth flow of transactions and mutually beneficial outcomes for both buyers and sellers.

Drawbacks of Using 2/10 N/30 Credit Terms

While the credit terms “2/10 N/30” offer several benefits, there are also some potential drawbacks to consider. Let’s explore some of the key disadvantages of using these credit terms.

- Potential Revenue Loss for Sellers: Offering a cash discount can result in reduced revenue for sellers, especially if a significant number of buyers take advantage of the discount. This loss in revenue needs to be carefully balanced with the benefits of improved cash flow and customer loyalty.

- Cash Flow Strain for Buyers: Buyers need to assess their cash flow situation before committing to early payment within the discount period. Making a payment ahead of schedule may strain their cash flow and impact their ability to meet other financial obligations.

- Opportunity Cost of Discount: Buyers must weigh the benefit of the cash discount against other investment opportunities or cash needs. In some cases, the opportunity cost of forgoing the discount and utilizing the cash elsewhere may outweigh the benefit gained from the discount itself.

- Potential Misalignment with Buyer’s Payment Cycle: The 10-day discount period may not align with the buyer’s usual payment cycle. Reconfiguring payment schedules to accommodate the discount may require additional administrative work and adjustments.

- Complex Payment Management: Both buyers and sellers need to carefully track and manage the payment process to ensure timely payment within the discount period. This requires efficient invoice management and payment tracking systems to avoid missing out on the discount or incurring penalties.

It’s important to evaluate these drawbacks alongside the potential benefits of using “2/10 N/30” credit terms. Each business should consider its unique circumstances and financial capabilities before deciding whether to implement these payment terms.

Overall, while “2/10 N/30” credit terms offer advantages such as improved cash flow management and cost savings, there are also potential drawbacks to consider, including revenue loss for sellers, cash flow strain for buyers, opportunity cost of the discount, alignment with payment cycles, and payment management complexities. Assessing these drawbacks will enable businesses to make informed decisions regarding the use of these credit terms.

Conclusion

Understanding credit terms is essential for navigating the financial aspects of business transactions. The credit term “2/10 N/30” offers a clear framework for payment conditions, providing a cash discount of 2% if payment is made within 10 days, with full payment due within 30 days.

By offering a cash discount, sellers incentivize prompt payment and improve their cash flow, while buyers have the opportunity to save on their purchase costs. The use of “2/10 N/30” credit terms can also foster strong buyer-seller relationships based on trust and reliability.

However, it is important to consider the potential drawbacks of these credit terms, such as revenue loss for sellers, cash flow strain for buyers, and the need for careful payment management. Businesses must evaluate their financial situations and determine if these credit terms align with their payment capabilities and overall objectives.

Ultimately, the decision to use “2/10 N/30” or any other credit terms should be based on careful consideration of the potential benefits and drawbacks, as well as the specific needs and circumstances of the parties involved.

By understanding and effectively utilizing credit terms, businesses can navigate payment processes, improve cash flow management, and foster positive relationships with their partners. Whether you are a buyer or a seller, being knowledgeable about credit terms is a valuable asset in the world of finance and business.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance