Finance

What Is Meant By “2/10, N/30” Credit Terms?

Published: January 7, 2024

Understand the meaning of "2/10, N/30" credit terms in finance. Learn how this payment discount and due date structure is used in business transactions.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

Introduction

When it comes to conducting business transactions, credit terms play a crucial role. One commonly used credit term is “2/10, N/30.” But what exactly does this term mean? In this article, we will dive into the world of credit terms and explore the meaning behind “2/10, N/30.”

Understanding credit terms is essential for both businesses and individuals involved in financial transactions. These terms define the payment conditions and deadlines and dictate how a buyer and seller will settle their financial obligations.

“2/10, N/30” is a shorthand representation of a specific credit term that refers to the discount and payment terms offered by a seller to a buyer. In simple terms, it states that if the buyer pays within a specified time frame, they are entitled to a discount.

As a business owner or individual making a purchase, it is crucial to grasp the meaning of this credit term to determine the financial implications it may have on your transactions. In the following sections, we will break down the various components of “2/10, N/30” and outline how to interpret and calculate its benefits.

Understanding Credit Terms

Before delving into the specifics of “2/10, N/30,” let’s first establish a basic understanding of credit terms.

Credit terms are the conditions agreed upon between a buyer and seller regarding the payment for goods or services rendered. These terms outline the timeframe in which the buyer is expected to settle the invoice and may also include any discounts or incentives for early payment. By setting clear credit terms, both parties can establish a mutually beneficial agreement and maintain a healthy cash flow.

There are various types of credit terms that businesses and individuals may encounter, and they can vary depending on the industry, the relationship between the parties, and other factors. Some common credit terms include Net 30, Net 60, and 2/10, Net 30.

Net 30, for instance, signifies that the buyer must make the full payment within 30 days from the invoice date. On the other hand, a credit term like 2/10, Net 30 provides an additional incentive, offering a discount to the buyer if payment is made within a specified period.

It is important to note that credit terms are negotiable, and businesses may offer different terms based on factors such as the buyer’s creditworthiness, the volume of the transaction, and the nature of the relationship between the parties. Understanding these credit terms is vital for effective financial management and maintaining positive supplier relationships.

Now that we have a general understanding of credit terms, let’s explore the specific meaning behind “2/10, N/30” and how it can impact your financial transactions.

The Meaning of “2/10, N/30”

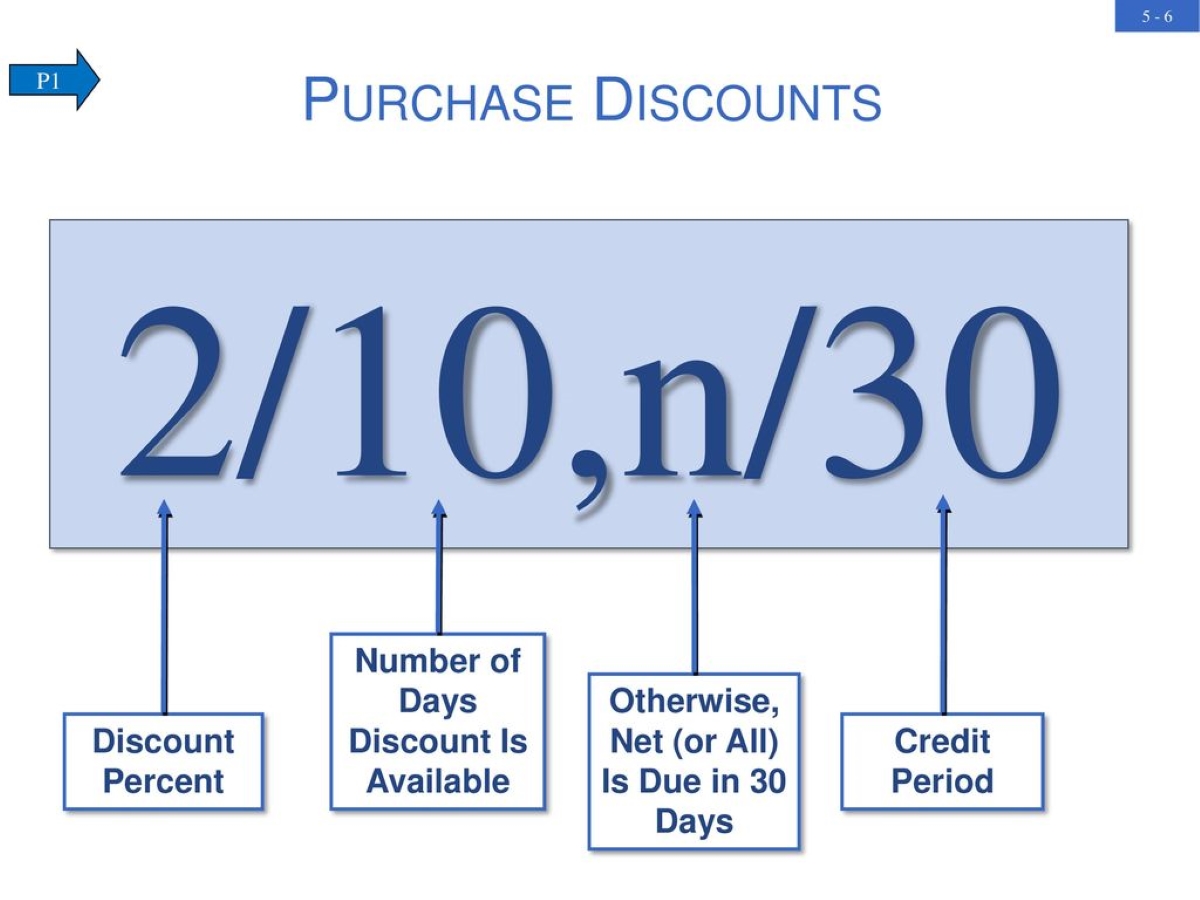

Within the realm of credit terms, “2/10, N/30” is a widely used term that specifies the terms of payment and potential discounts extended by a seller to a buyer. Let’s break down the components of this credit term to understand its meaning:

- 2: The first number in “2/10” indicates the discount percentage offered by the seller. In this case, it signifies a 2% discount.

- 10: The second number in “2/10” represents the time frame in which the buyer can make the payment to qualify for the discount. In this example, the buyer has 10 days from the invoice date to settle the payment.

- N: The letter “N” in “N/30” stands for “Net,” which means that the buyer must pay the full invoice amount.

- 30: The number “30” in “N/30” indicates the number of days within which the buyer must pay the invoice in full.

So, combining all the components, “2/10, N/30” means that the buyer is eligible for a 2% discount if they settle the invoice within 10 days. If the buyer does not take advantage of the early payment discount, they must pay the full invoice amount within 30 days.

It’s important to note that these credit terms are not set in stone and can be subject to negotiation between the buyer and seller. Depending on the specific circumstances, a seller may offer different discount percentages or timeframes for payment.

Next, let’s explore how to interpret and calculate the benefits of “2/10, N/30” using some examples.

Breaking Down the Credit Terms

Now that we understand the meaning of “2/10, N/30,” let’s break down the credit terms further to gain a comprehensive understanding of how they function.

The credit term “2/10, N/30” presents two distinct aspects: the discount and the payment deadline.

The first component, the discount, indicates that the buyer is offered a 2% reduction in the invoice amount if payment is made within the specified time frame. This discount serves as an incentive for prompt payment and is a benefit provided by the seller.

The second component is the payment deadline. Suppose the buyer chooses not to take advantage of the early payment discount. In that case, they must pay the full invoice amount within 30 days, indicating “Net 30” terms. This means that there are no additional discounts available, and the full payment is expected by the stated due date.

By offering a discount for early payment, sellers can encourage their customers to settle invoices promptly, thereby improving cash flow and reducing the risk of late or non-payments. On the other hand, buyers can benefit from the discount by leveraging their cash flow and potentially saving money on their purchases.

It’s important to note that not all businesses or sellers may offer “2/10, N/30” credit terms. Each seller has the flexibility to define their own credit terms based on their financial needs, industry standards, and customer preferences.

In the next section, we will explore examples to illustrate how to interpret and calculate the benefits of “2/10, N/30.”

Interpreting the Numbers

The numbers in “2/10, N/30” represent key aspects of the credit terms. Let’s dive deeper into interpreting these numbers and understand their implications.

The first number, “2,” indicates the discount percentage offered by the seller. In this case, it represents a 2% discount. This means that if the buyer pays within the specified time frame, they can deduct 2% from the total invoice amount as a discount.

The second number, “10,” signifies the time frame within which the buyer must make the payment to qualify for the discount. In the case of “2/10, N/30,” the buyer has 10 days from the date of the invoice to make the payment and avail the discount.

The letter “N” represents “Net,” meaning that if the buyer does not take advantage of the early payment discount, they must pay the full invoice amount.

The final number, “30,” states the number of days within which the buyer must pay the invoice in full. In this case, the buyer has 30 days from the invoice date to settle the payment if they choose not to avail of the discount offered.

Interpreting the numbers in “2/10, N/30” allows both the buyer and seller to understand the financial implications of the credit terms. The buyer can assess the potential savings through the early payment discount, while the seller can encourage prompt payments through the offered discount.

In the following section, we will provide examples to help visualize how to calculate the benefits of “2/10, N/30.”

Calculation Examples

To better understand the benefits of “2/10, N/30,” let’s consider a couple of calculation examples:

Example 1:

Imagine a buyer receives an invoice for $1,000 with credit terms of “2/10, N/30.” If the buyer chooses to take advantage of the early payment discount, they can deduct 2% from the invoice amount. In this case, the discount would be $1,000 x 2% = $20. Therefore, the buyer can pay only $980 if payment is made within 10 days.

If the buyer does not pay within the discount period, they would need to pay the full invoice amount of $1,000 within the 30-day payment deadline.

Example 2:

Let’s consider another scenario where the buyer receives an invoice for $5,000 with the same credit terms of “2/10, N/30.” If the buyer chooses to make the payment within the discount period, they can enjoy a discount of 2% off the total invoice amount. In this case, the discount would amount to $5,000 x 2% = $100. Hence, the buyer can pay only $4,900 if payment is made within 10 days.

If the buyer misses the discount period, they would be required to pay the full invoice amount of $5,000 within the 30-day payment deadline.

These examples illustrate the potential savings that buyers can achieve by availing of the early payment discount. It’s important for both buyers and sellers to be aware of these calculations to make informed decisions regarding payments and cash flow management.

In the next section, we will explore the pros and cons of “2/10, N/30” credit terms.

Pros and Cons of “2/10, N/30”

Like any credit terms, “2/10, N/30” has its own set of advantages and disadvantages that both buyers and sellers should consider. Let’s explore the pros and cons of these credit terms:

Pros:

- Discount Incentive: The early payment discount of 2% offered in “2/10, N/30” can provide significant cost savings for buyers. Taking advantage of the discount allows buyers to reduce their overall expenses and improve their profit margins.

- Improved Cash Flow: By offering a discount for early payment, sellers can encourage prompt payment from their customers. This, in turn, can improve their cash flow and reduce the risk of late or non-payments.

- Stronger Supplier Relationships: Prompt payment through “2/10, N/30” credit terms can foster stronger relationships between buyers and sellers. Timely payments can enhance trust and reliability, leading to better long-term business partnerships.

Cons:

- Tight Payment Deadlines: The 10-day payment period can impose a sense of urgency on buyers to meet the discount deadline. This may require efficient cash flow management and coordination to ensure payments are made on time.

- Limited Discount Percentage: The 2% discount offered in “2/10, N/30” may not always be substantial enough to outweigh the benefits of lengthening payment terms. Buyers must evaluate whether the discount justifies the potential strain on their cash flow.

- Need for Financial Resources: To take advantage of the discount, buyers must have the necessary financial resources available within the specified time frame. This may involve careful budgeting and planning to ensure timely payments.

Understanding the pros and cons of “2/10, N/30” credit terms allows buyers and sellers to assess the benefits and risks involved. It’s essential to consider factors such as cash flow, financial capabilities, and relationships with suppliers when determining whether these credit terms are suitable for a particular business or transaction.

In the final section, we will explore important factors to consider when deciding on credit terms.

Factors to Consider

When deciding on credit terms such as “2/10, N/30,” it is important to take several factors into consideration. These factors can help both buyers and sellers make informed decisions that align with their financial goals and capabilities. Let’s explore some key factors to consider:

- Cash Flow: Evaluate your cash flow and determine if you have the resources to take advantage of the early payment discount. Consider whether the discount outweighs the strain on your cash flow and if it aligns with your budgeting and financial obligations.

- Supplier Relationships: Assess the importance of your relationship with the seller. If maintaining a strong partnership is crucial, utilizing the early payment discount can positively impact your relationship by establishing trust and reliability.

- Purchasing Volume: Consider the volume of purchases you make from the seller. If you have significant purchases, even a small discount percentage can add up to substantial savings over time.

- Payment Terms Negotiation: Remember that credit terms are often negotiable. If the offered terms do not align with your needs or if you believe you can secure more favorable terms, discuss them with the seller to find a mutually beneficial agreement.

- Industry Norms: Consider the credit terms commonly used in your industry. Understanding industry norms can provide guidance on what is typically expected and help you make educated decisions regarding credit terms.

By considering these factors, you can make strategic decisions regarding credit terms that align with your financial capacity, business goals, and relationships with suppliers. Remember that credit terms can have a significant impact on your cash flow, profitability, and overall financial management.

Now that we have explored the factors to consider, let’s conclude our discussion on “2/10, N/30” credit terms.

Conclusion

Understanding credit terms is essential for both buyers and sellers involved in financial transactions. “2/10, N/30” is a commonly used credit term that offers a 2% early payment discount if the buyer settles the invoice within 10 days. If the discount is not taken, the full invoice amount must be paid within 30 days.

By offering an early payment discount, sellers can encourage prompt payments from buyers, improving cash flow and reducing the risk of late payments. Buyers, on the other hand, can benefit from cost savings through the discount.

When considering “2/10, N/30” credit terms, it is important to weigh the pros and cons. The advantages include discount incentives, improved cash flow, and stronger supplier relationships. However, there are also considerations such as tight payment deadlines and the need for financial resources.

Several factors should be taken into account when deciding on credit terms, including cash flow, supplier relationships, purchasing volume, negotiation potential, and industry norms. By considering these factors, buyers and sellers can make informed decisions that align with their financial objectives.

In conclusion, “2/10, N/30” credit terms can provide an opportunity for buyers to save money and sellers to improve cash flow. However, careful evaluation of the terms and consideration of individual circumstances is crucial. By understanding the meaning and implications of credit terms, businesses can effectively manage their finances and build strong relationships with their suppliers.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance