Home>Finance>How Do Finance Companies Life Insurance Companies And Pension Funds Channel Savings To Borrowers?

Finance

How Do Finance Companies Life Insurance Companies And Pension Funds Channel Savings To Borrowers?

Published: January 23, 2024

Learn how finance companies, life insurance companies, and pension funds efficiently channel savings to borrowers, driving economic growth and stability in the finance sector.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

Introduction

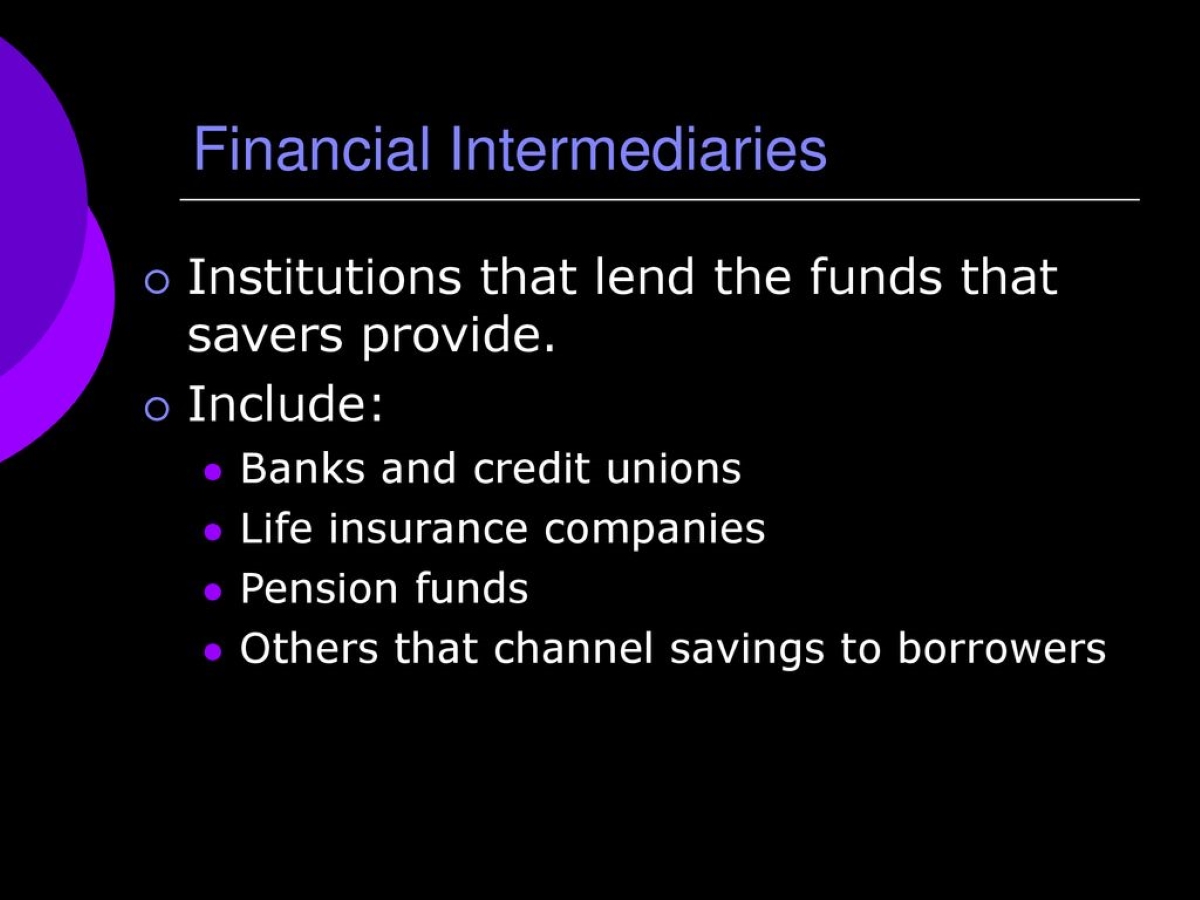

Finance companies, life insurance companies, and pension funds play crucial roles in channeling savings to borrowers, thereby facilitating the efficient allocation of capital in the economy. By connecting savers with borrowers, these financial institutions contribute to the overall economic growth and development. Understanding how these entities channel savings to borrowers is essential for comprehending the intricate workings of the financial system.

In this article, we will delve into the distinct roles of finance companies, life insurance companies, and pension funds in the process of channeling savings to borrowers. Through a comprehensive exploration of their functions and mechanisms, we aim to shed light on the vital contributions of these institutions to the financial landscape. By gaining insights into their operations, readers can develop a deeper appreciation for the interconnectedness of savings and borrowing within the broader framework of the economy.

Join us as we unravel the intricate web of financial intermediation and discover how these entities facilitate the flow of funds from savers to borrowers, fueling economic activities and fostering prosperity.

Role of Finance Companies in Channeling Savings to Borrowers

Finance companies serve as vital intermediaries that facilitate the flow of savings from individuals and institutions to borrowers in need of capital. These entities play a pivotal role in the financial ecosystem by offering a wide array of lending and financial services. One of the primary functions of finance companies is to gather funds from savers and subsequently deploy these funds to borrowers, thereby bridging the gap between surplus units and deficit units within the economy.

By engaging in activities such as consumer lending, commercial lending, and leasing, finance companies cater to the diverse financing needs of individuals, small businesses, and corporations. This broad spectrum of services enables finance companies to effectively channel savings into various sectors of the economy, thereby stimulating economic growth and development.

Moreover, finance companies often specialize in niche markets or specific types of financing, allowing them to cater to borrowers who may face challenges in obtaining funding through traditional banking channels. This targeted approach enables finance companies to reach underserved segments of the market, fostering financial inclusion and expanding access to credit for a broader range of borrowers.

Furthermore, finance companies leverage their expertise in risk assessment and underwriting to evaluate the creditworthiness of potential borrowers. This diligent assessment process enables them to extend credit to individuals and businesses while managing the associated risks prudently. Additionally, finance companies may package and securitize loans, thereby transforming illiquid assets into tradable securities that can be distributed to investors, further enhancing the efficiency of capital allocation.

Through their multifaceted operations and specialized offerings, finance companies play a vital role in channeling savings to borrowers, thereby contributing to the vibrancy and dynamism of the overall economy.

Role of Life Insurance Companies in Channeling Savings to Borrowers

Life insurance companies serve as key players in the financial landscape, not only providing protection and financial security to policyholders but also playing a significant role in channeling savings to borrowers. Through the sale of life insurance policies and the management of investment portfolios, these companies mobilize savings and direct them toward various borrowers, thereby contributing to the efficient allocation of capital within the economy.

One of the primary ways in which life insurance companies channel savings to borrowers is through their investment activities. Policyholder premiums and other funds collected by life insurers are often allocated to a diversified portfolio of assets, including bonds, equities, and other income-generating instruments. By investing these funds in the capital markets, life insurance companies effectively channel savings to governments, corporations, and other entities in need of capital for various projects and initiatives.

Furthermore, life insurance companies may also extend loans to individuals and businesses, utilizing the accumulated cash value within certain types of life insurance policies. This mechanism allows policyholders to access funds through policy loans, providing them with a source of borrowing while leveraging the accumulated savings within their insurance coverage. In this way, life insurance companies facilitate borrowing by offering a unique avenue for policyholders to access capital when needed.

Moreover, the long-term nature of life insurance liabilities enables these companies to make strategic, enduring investments that align with their long-duration obligations. By matching the maturities of their assets and liabilities, life insurers contribute to the stability and continuity of funding for borrowers, particularly those engaged in long-term projects and endeavors.

Additionally, life insurance companies play a role in the broader financial markets by participating in the purchase and sale of securities, thereby providing liquidity and contributing to the overall functioning of capital markets. This active involvement in the financial ecosystem further underscores their significance in channeling savings to borrowers and sustaining the flow of funds within the economy.

Through their investment activities, loan provisions, and participation in capital markets, life insurance companies play a pivotal role in channeling savings to borrowers, fostering economic growth and stability.

Role of Pension Funds in Channeling Savings to Borrowers

Pension funds are instrumental in channeling savings to borrowers, playing a critical role in the efficient allocation of capital within the financial system. These funds, established to provide retirement benefits to employees, accumulate substantial savings over time through contributions from both employers and employees. By leveraging these pooled savings, pension funds actively participate in financial markets and direct capital to borrowers, thereby contributing to the overall liquidity and vibrancy of the economy.

One of the primary mechanisms through which pension funds channel savings to borrowers is through their investment activities. Pension funds typically maintain diversified portfolios comprising a range of assets, including stocks, bonds, real estate, and alternative investments. By deploying these funds in various financial instruments, pension funds provide essential capital to governments, corporations, and other entities seeking financing for projects, expansion, and operational needs.

Furthermore, pension funds often invest in long-term infrastructure projects and capital-intensive ventures, aligning with their extended investment horizon and the long-term nature of their pension obligations. This strategic approach to investment not only supports the funding requirements of borrowers engaged in long-duration initiatives but also enhances the stability and sustainability of the projects receiving funding.

In addition to their investment activities, pension funds may also participate in the issuance and trading of corporate and government securities, contributing to the liquidity and efficiency of capital markets. By engaging in the purchase and sale of securities, pension funds facilitate the flow of funds to borrowers while maintaining a dynamic and responsive financial environment.

Moreover, pension funds play a vital role in supporting economic growth by providing a stable and enduring source of funding to borrowers. The long-term nature of pension fund investments aligns with the funding needs of entities engaged in extended projects, thereby fostering continuity and resilience in the financing of critical initiatives.

By effectively channeling savings to borrowers through their investment strategies and active participation in financial markets, pension funds bolster the overall capital allocation process, contributing to the vitality and sustainability of economic activities.

Conclusion

In conclusion, finance companies, life insurance companies, and pension funds play integral roles in channeling savings to borrowers, thereby facilitating the efficient allocation of capital within the economy. Through their diverse mechanisms and strategic involvement in financial markets, these entities contribute to the vitality and dynamism of the overall financial landscape.

Finance companies leverage their expertise in lending and risk management to gather savings from various sources and deploy these funds to borrowers, catering to the financing needs of individuals, small businesses, and corporations. Their specialized offerings and targeted approach enable them to reach underserved segments of the market, fostering financial inclusion and expanding access to credit.

Life insurance companies mobilize savings through policyholder premiums and investment activities, directing funds to borrowers through strategic investments and loan provisions. Their long-term orientation and participation in capital markets contribute to the stability and continuity of funding for borrowers engaged in diverse projects and endeavors.

Similarly, pension funds, with their substantial pooled savings and extended investment horizon, play a pivotal role in channeling funds to borrowers, particularly those involved in long-term initiatives and infrastructure projects. Their strategic investment approach and active participation in financial markets bolster the overall capital allocation process, supporting economic growth and sustainability.

By understanding the intricate functions and contributions of finance companies, life insurance companies, and pension funds in channeling savings to borrowers, individuals and institutions can gain valuable insights into the interconnectedness of savings and borrowing within the broader framework of the economy. This comprehension is essential for fostering a robust and resilient financial ecosystem that effectively supports the funding needs of borrowers while promoting economic growth and development.

Ultimately, the collaborative efforts of these financial intermediaries serve to bridge the gap between savers and borrowers, ensuring the efficient flow of funds and the sustained progression of economic activities, thereby contributing to the overall prosperity and stability of the economy.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance