Home>Finance>How Often Does Home Depot Increase Credit Limits

Finance

How Often Does Home Depot Increase Credit Limits

Modified: March 6, 2024

Learn about how Home Depot frequently increases credit limits and manage your finances effectively. Find out more about credit limits and staying on top of your financial game.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

Introduction

Welcome to Home Improvement Finance 101! As a homeowner, you’ve probably spent countless weekends browsing the aisles of Home Depot, searching for the perfect tools and materials to transform your living space. But did you know that Home Depot offers credit cards with the potential for credit limit increases?

Managing your credit limit effectively is vital if you want to make the most of your Home Depot financing options. In this article, we will explore how often Home Depot increases credit limits, the factors that influence these increases, and provide tips on how you can increase your Home Depot credit limit.

Whether you’re planning a small DIY project or a major home renovation, having a higher credit limit can give you the flexibility to purchase the materials you need without straining your budget. Understanding the credit limit increase process at Home Depot can help you maximize your purchasing power and take advantage of special financing offers.

So, let’s dive into the details and discover how Home Depot manages credit limits for its valued customers.

Factors that Influence Home Depot’s Credit Limit Increases

Home Depot considers various factors when determining credit limit increases for its customers. While the specific criteria may vary, here are some common factors that may influence how Home Depot evaluates credit limit increase requests:

- Payment History: Your payment history is a crucial factor that Home Depot considers. If you have consistently made payments on time and maintained a good credit standing, it increases your chances of getting a credit limit increase.

- Credit Utilization Ratio: Home Depot also looks at your credit utilization ratio, which is the percentage of available credit you are currently utilizing. If you are using a high percentage of your existing credit, it might indicate financial strain. Keeping a low credit utilization ratio can improve your chances of receiving a credit limit increase.

- Income and Employment: Your income and employment stability play a role in determining your creditworthiness. Home Depot may consider your income level and job tenure to assess your ability to handle increased credit limits.

- Credit Score: While Home Depot may not explicitly disclose the credit score requirement for credit limit increases, having a higher credit score generally increases your chances of getting an increase. A good credit score demonstrates responsible financial management.

- Account Activity: Home Depot may evaluate your account activity, including the frequency of purchases, average purchase amount, and the overall relationship with the company. Consistent and active use of your Home Depot credit card can signal responsible credit management.

It’s important to note that these factors are not exhaustive and Home Depot may have additional considerations when assessing credit limit increase requests. Remember, the decision ultimately lies with Home Depot’s credit department, which determines whether you qualify for a credit limit increase.

Now that we understand the factors that influence credit limit increases, let’s explore how often Home Depot increases credit limits for its customers.

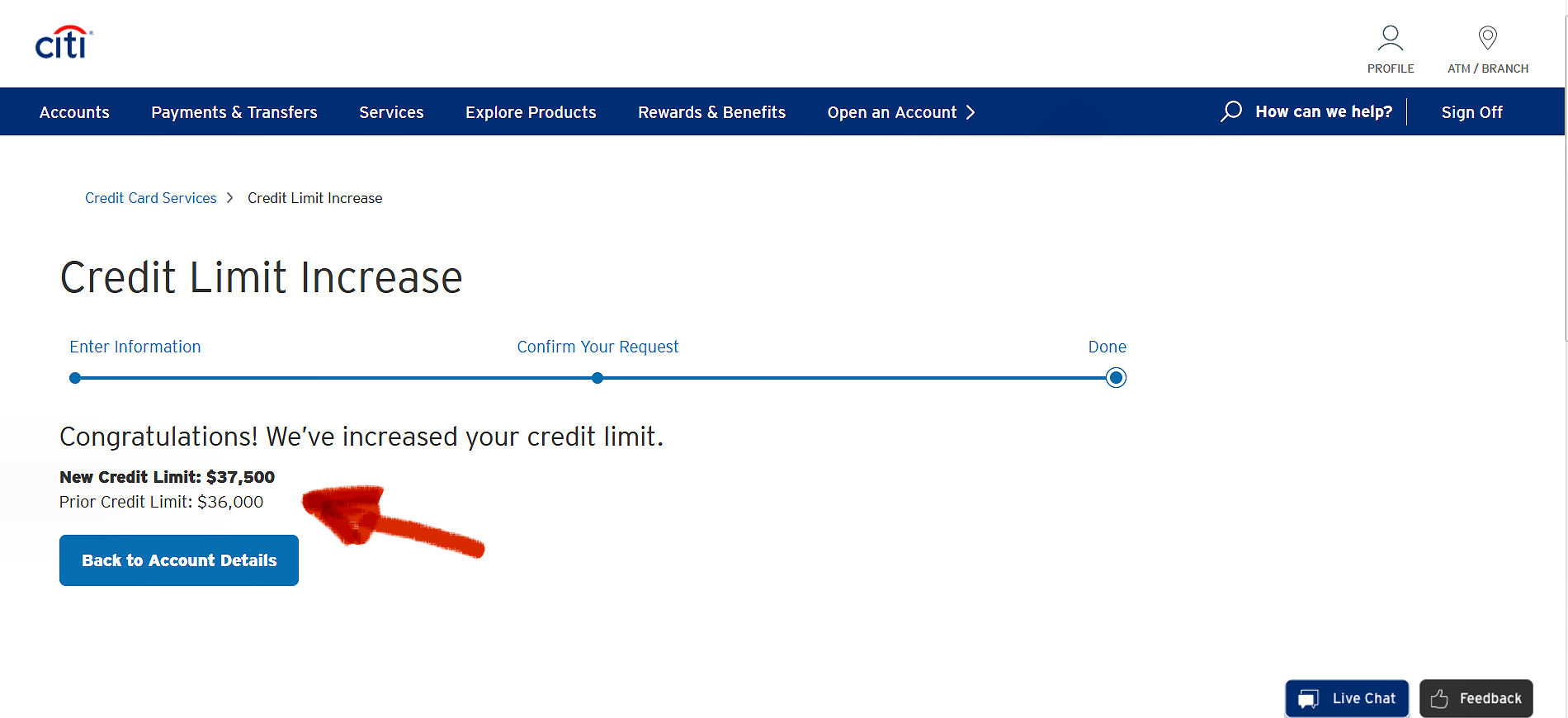

Home Depot’s Credit Limit Increase Frequency

Home Depot offers credit limit increases to eligible customers, but the exact frequency of these increases can vary. While Home Depot does not publicly specify a set schedule for credit limit increases, there are some general trends to consider.

Typically, Home Depot evaluates credit limit increase requests periodically. This evaluation process may occur every few months or annually, depending on factors such as your payment history, creditworthiness, and account activity. It’s worth noting that Home Depot may also proactively review and adjust credit limits for customers who demonstrate responsible credit management.

Moreover, Home Depot may automatically increase credit limits for eligible customers without the need for a specific request. These increases are often based on factors such as account usage, payment history, and creditworthiness. If you consistently make on-time payments and maintain a good credit standing, you may benefit from automatic credit limit increases.

While Home Depot may not guarantee specific timeframes for credit limit increases, there are steps you can take to increase your chances of securing a higher credit limit.

Let’s explore how you can proactively work towards increasing your Home Depot credit limit in the next section.

How to Increase Your Home Depot Credit Limit

If you’re looking to increase your Home Depot credit limit, here are a few strategies you can implement:

- Make Timely Payments: Consistently making on-time payments demonstrates financial responsibility and improves your creditworthiness. Ensure that you pay at least the minimum due amount on your Home Depot credit card every month.

- Pay More than the Minimum: While it’s important to make at least the minimum payment, try to pay more whenever possible. Paying more than the minimum can show that you’re capable of managing higher credit limits and may increase your chances of a credit limit increase.

- Reduce Credit Utilization: Keep your credit utilization ratio low by minimizing the percentage of your available credit that you are currently using. Aim to keep it below 30% to demonstrate responsible credit management.

- Regularly Use Your Home Depot Credit Card: Use your Home Depot credit card for regular purchases, as active account usage can show Home Depot that you are a valued customer. However, be sure to use it responsibly and within your budget.

- Improve Your Credit Score: Work on improving your credit score by paying all your bills on time, reducing outstanding debts, and managing your credit responsibly. A higher credit score can enhance your chances of receiving a credit limit increase.

- Contact Home Depot: If you believe you meet the criteria for a credit limit increase, consider reaching out to Home Depot’s customer service or visiting a local store. Inquire about the process for requesting a credit limit increase and provide any relevant information that may support your request.

Keep in mind that there is no guarantee of a credit limit increase, as Home Depot’s decision ultimately depends on their evaluation of your creditworthiness. However, by following these strategies, you can increase your chances of securing a higher credit limit and enjoying greater purchasing power at Home Depot.

Now that you’re equipped with tips on increasing your credit limit, let’s explore some recommendations for managing your Home Depot credit limit effectively.

Tips for Managing Your Home Depot Credit Limit

Managing your Home Depot credit limit effectively is essential for maintaining a healthy financial outlook. Here are some tips to help you make the most of your credit limit:

- Create a Budget: Establish a budget that includes your monthly income and expenses. Consider your Home Depot credit limit as part of your overall financial plan and allocate funds accordingly. This way, you can ensure that you stay within your credit limit and avoid overspending.

- Track Your Spending: Keep a record of your Home Depot purchases, either through a budgeting app or a simple spreadsheet. Monitoring your spending will help you stay aware of how much of your credit limit you have utilized and can prevent any surprises when it comes time to make payments.

- Avoid Maxing Out Your Credit Limit: While your credit limit may provide a sense of purchasing power, it’s important to use it responsibly. Avoid maxing out your credit limit as it can negatively impact your credit score and make it harder to manage your payments. Aim to keep your credit utilization ratio below 30%.

- Pay Your Balance in Full: Whenever possible, pay your Home Depot credit card balance in full each month to avoid accruing unnecessary interest charges. Not only does this help you stay on top of your finances, but it also demonstrates responsible credit management to Home Depot, increasing your chances of obtaining a credit limit increase in the future.

- Be Mindful of Special Financing Offers: Home Depot often offers special financing deals, such as zero percent interest for a set period. While these offers can be tempting, make sure you understand the terms and conditions before taking advantage of them. If you don’t pay off the balance within the promotional period, you may be subject to high interest charges.

- Regularly Review Your Credit Card Statements: Take the time to review your Home Depot credit card statements carefully. Check for any unauthorized transactions, errors, or discrepancies. Being proactive in monitoring your statements can help you catch any issues early and resolve them promptly.

By implementing these tips, you can effectively manage your Home Depot credit limit, avoid unnecessary debt, and maintain a positive financial standing.

Now let’s wrap up our discussion on Home Depot credit limit increases.

Conclusion

Managing your Home Depot credit limit wisely can provide you with the freedom and flexibility to complete your home improvement projects. While Home Depot does not disclose a specific schedule for credit limit increases, there are factors you can focus on to improve your chances.

Factors such as payment history, credit utilization ratio, income and employment stability, credit score, and account activity all play a role in Home Depot’s evaluation of credit limit increase requests. By maintaining a good payment history, keeping your credit utilization low, and demonstrating responsible credit management, you can increase the likelihood of receiving a credit limit increase.

Additionally, actively using your Home Depot credit card, paying more than the minimum amount due, and improving your credit score can also contribute to your eligibility for a credit limit increase.

Remember to manage your credit limit effectively by creating a budget, tracking your spending, and paying your balance in full whenever possible. Being mindful of special financing offers and regularly reviewing your credit card statements can also help you stay on top of your Home Depot credit card usage.

While there is no guarantee of a credit limit increase, by following these tips and maintaining good financial habits, you can position yourself for potential credit limit increases in the future.

Now that you have a better understanding of Home Depot’s credit limit increase process and how to manage your credit effectively, you can confidently make the most of your Home Depot credit card and embark on your home improvement endeavors.

Happy renovating and shopping at Home Depot!

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance