Home>Finance>How To Add Savings Accounts In Retirement Planning

Finance

How To Add Savings Accounts In Retirement Planning

Published: January 21, 2024

Learn how to incorporate savings accounts into your retirement planning for optimal finances and security. Finance your future wisely with these expert tips.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

- Introduction

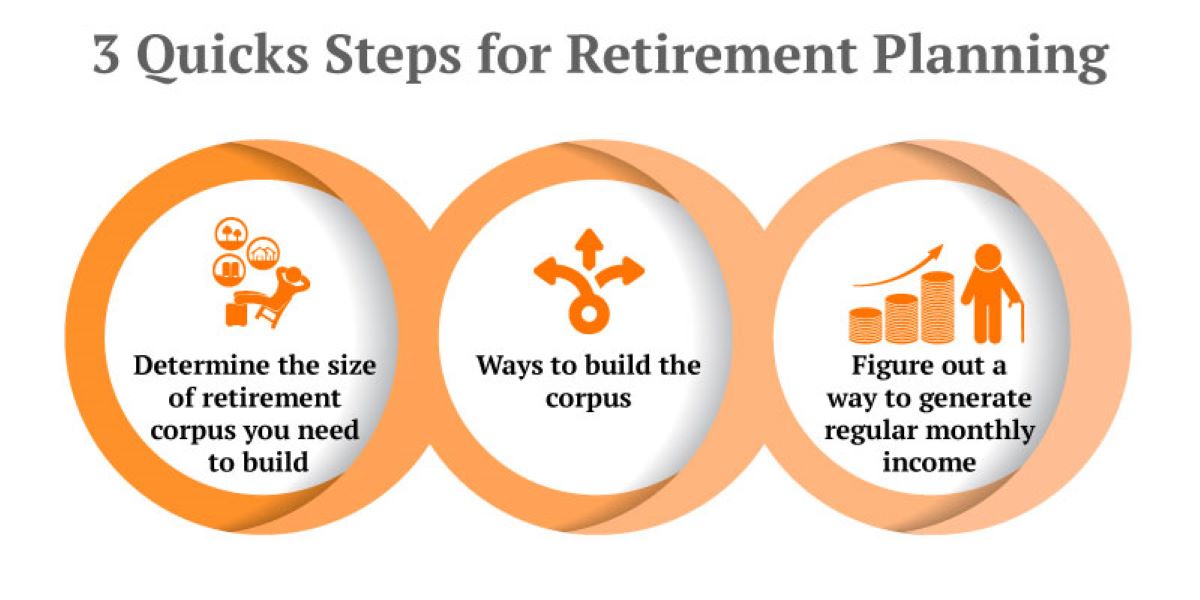

- Importance of Adding Savings Accounts in Retirement Planning

- Types of Savings Accounts for Retirement

- Factors to Consider when Choosing Savings Accounts for Retirement

- Steps to Add Savings Accounts in Retirement Planning

- Benefits of Adding Savings Accounts in Retirement Planning

- Risks and Challenges in Adding Savings Accounts in Retirement Planning

- Strategies to Maximize Savings Accounts in Retirement Planning

- Conclusion

Introduction

Retirement planning is a crucial aspect of personal finance that enables individuals to secure their financial well-being during their golden years. While traditional retirement vehicles like pension plans and 401(k)s are commonly used, incorporating savings accounts into retirement planning can provide additional benefits and flexibility.

Adding savings accounts to retirement planning offers individuals the opportunity to diversify their investment portfolio and access funds easily when needed. With the right approach, savings accounts can complement other retirement accounts and help retirees achieve their financial goals.

In this article, we will explore the importance of adding savings accounts to retirement planning, discuss the various types of savings accounts that can be utilized, and provide practical steps to integrate savings accounts into a comprehensive retirement strategy. Additionally, we will address the benefits of incorporating savings accounts, as well as the potential risks and challenges that may arise.

Furthermore, we will examine strategies to maximize the potential of savings accounts in retirement planning, ensuring individuals can make the most of their savings and optimize their financial security for the future.

By understanding the significance of savings accounts in retirement planning and utilizing them effectively, individuals can enhance their financial stability and enjoy a comfortable retirement.

Importance of Adding Savings Accounts in Retirement Planning

When it comes to retirement planning, many individuals focus primarily on retirement accounts like pension plans and 401(k)s. While these accounts are essential components of a comprehensive retirement strategy, it’s equally important to incorporate savings accounts into the plan. Here are several reasons why:

- Flexibility and Accessibility: Savings accounts provide a level of flexibility and accessibility that other retirement accounts may not offer. In the event of unexpected expenses or emergencies, having money readily available in a savings account can provide peace of mind and help avoid early withdrawals from retirement accounts, which may incur taxes and penalties.

- Opportunity for Diversification: By adding savings accounts to your retirement planning, you can diversify your investment portfolio. While retirement accounts are typically invested in stocks, bonds, or mutual funds, savings accounts provide an opportunity to keep funds in cash. This diversification helps spread risk and ensures that you have a mix of investments that can help protect your savings.

- Stable and Secure Returns: Unlike other investment options that come with some level of risk, savings accounts offer stable and secure returns. Although the interest rates might be relatively low compared to other investment vehicles, savings accounts provide a valuable element of stability to your retirement income.

- Short-term Financial Goals: Savings accounts can be particularly useful for short-term financial goals, even within retirement. Whether you’re planning a dream vacation, purchasing a new car, or covering unexpected medical expenses, having a dedicated savings account can help you achieve these goals without compromising your long-term retirement funds.

By incorporating savings accounts into your retirement planning, you can enjoy the benefits of flexibility, diversification, stability, and the ability to meet short-term financial goals. Furthermore, having accessible funds readily available can provide a safety net during unforeseen circumstances, ensuring that your retirement savings remain intact.

Types of Savings Accounts for Retirement

When it comes to adding savings accounts to your retirement planning, there are several options to consider. Each type of savings account carries unique features and benefits that can align with your financial goals and risk tolerance. Here are some common types of savings accounts for retirement:

- Traditional Savings Accounts: Traditional savings accounts, offered by banks and credit unions, provide a safe and secure place to store your cash while earning interest. These accounts typically have low minimum balance requirements, easy access to funds, and FDIC or NCUA insurance protection.

- Certificates of Deposit (CDs): CDs are time-bound savings accounts that require you to deposit a fixed sum of money for a specific period. They offer higher interest rates than traditional savings accounts, and the longer the CD term, the higher the interest rate. However, accessing funds before the CD maturity date may result in penalties.

- Money Market Accounts (MMAs): MMAs are a hybrid of checking and savings accounts that typically offer higher interest rates than traditional savings accounts. They often require a higher minimum balance but provide check-writing privileges and limited transaction capabilities.

- High-Yield Savings Accounts: High-yield savings accounts are similar to traditional savings accounts but offer higher interest rates. These accounts are typically offered by online banks and financial institutions and can be a good option to maximize the growth of your retirement savings.

- Health Savings Accounts (HSAs): While primarily used to cover medical expenses, HSAs can also be a valuable retirement savings tool. Contributions to HSAs are tax-deductible, earnings grow tax-free, and withdrawals for qualified medical expenses are tax-free.

The choice of which savings account to use for retirement planning depends on factors such as your financial goals, time horizon, risk tolerance, and liquidity needs. It’s advisable to compare interest rates, fees, and account features before deciding which type of savings account is most suitable for your specific circumstances.

Remember, diversity in your savings account portfolio is key. Consider a combination of different types of savings accounts to take advantage of their individual benefits and create a well-rounded retirement savings strategy.

Factors to Consider when Choosing Savings Accounts for Retirement

Choosing the right savings accounts for your retirement planning requires careful consideration of various factors. Here are some key aspects to keep in mind when making your decision:

- Interest Rates: One of the most important factors to consider is the interest rate offered by the savings account. Look for accounts that offer competitive rates to help maximize your returns over time.

- Fees and Charges: Be aware of any fees and charges associated with the savings account. These may include monthly maintenance fees or transaction fees. Opt for accounts with minimal fees or fee waivers based on specific criteria.

- Minimum Balance Requirements: Some savings accounts require you to maintain a minimum balance to avoid fees or earn interest. Consider your financial situation and ensure that you can comfortably meet the minimum balance requirement without incurring additional costs.

- Accessibility: Evaluate how easily you can access your funds when needed. Consider the account’s withdrawal limitations and any penalties that may be imposed for early withdrawals.

- Account Security: Look for savings accounts that offer deposit insurance, such as FDIC or NCUA protection, to ensure the safety of your funds.

- Tax Considerations: Understand the tax implications of the savings account you choose. Some accounts may provide tax advantages, such as tax-free earnings or tax-deductible contributions, which can enhance your retirement savings.

- Financial Institution Reputation: Research the reputation and stability of the financial institution offering the savings account. Consider factors such as customer reviews, ratings, and the institution’s financial strength.

- Account Features: Assess additional features offered by the savings account, such as online banking, mobile apps, customer support, and any perks or rewards programs.

It’s important to carefully evaluate and compare these factors to select the savings accounts that align with your retirement goals. Consider consulting with a financial advisor to get personalized insights and recommendations based on your unique financial situation.

By thoroughly considering these factors, you can make informed decisions and choose savings accounts that offer the right combination of features, benefits, and accessibility to support your retirement planning needs.

Steps to Add Savings Accounts in Retirement Planning

Integrating savings accounts into your retirement planning involves a systematic approach to ensure that you make the most of these financial tools. Here are the steps to follow:

- Evaluate Your Financial Goals: Begin by assessing your retirement goals and determining how savings accounts can help you achieve them. Consider factors such as the desired retirement age, estimated expenses, and lifestyle expectations.

- Analyze Your Current Savings: Take stock of your existing retirement savings, including pension plans, 401(k)s, or other retirement accounts. Evaluate how savings accounts can complement these investments and provide additional financial security.

- Research Savings Account Options: Explore different types of savings accounts available for retirement planning. Consider their interest rates, fees, minimum balance requirements, and any tax advantages they may offer.

- Assess Your Risk Tolerance: Determine your risk tolerance when it comes to retirement savings. Some individuals may prefer more conservative options, while others may be comfortable with higher-risk investments.

- Create a Budget: Develop a budget that outlines your income, expenses, and savings goals. Allocate funds to your savings accounts regularly to ensure consistent contributions.

- Set Up Automatic Transfers: Automate the process of depositing funds into your savings accounts. Set up automatic transfers from your checking account or paycheck to ensure a consistent savings habit.

- Monitor and Adjust: Regularly review your savings progress and make adjustments as needed. Consider increasing contributions to savings accounts during times of financial stability or when you receive a raise or bonus.

- Reassess as Retirement Nears: As retirement approaches, reevaluate your savings accounts and their role in your overall retirement plan. Make any necessary adjustments to ensure your savings align with your retirement income needs.

Remember, adding savings accounts to your retirement planning is an ongoing process. It requires regular monitoring and reassessment to ensure that your savings strategy remains aligned with your financial goals and objectives.

By following these steps and incorporating savings accounts into your retirement planning, you can enhance your financial security, diversify your investments, and have greater flexibility and accessibility to funds when needed.

Benefits of Adding Savings Accounts in Retirement Planning

Adding savings accounts to your retirement planning can bring numerous benefits that contribute to your overall financial security and well-being. Here are some key advantages of incorporating savings accounts into your retirement strategy:

- Flexibility and Access to Funds: Savings accounts provide a readily accessible pool of funds for emergencies or unexpected expenses during retirement. Having cash easily available can help you avoid early withdrawals from retirement accounts, which may come with penalties and tax implications.

- Stability and Security: Savings accounts offer stability and security, providing peace of mind during retirement. Unlike investment accounts that fluctuate with the market, savings accounts provide a guaranteed return on your investment, ensuring a stable income stream.

- Diversification of Investments: By adding savings accounts to your retirement portfolio, you can diversify your investment holdings. This diversification helps manage risk and reduces the potential impact of market downturns, providing a buffer against volatility in other investment accounts.

- Short-term Financial Goals: Savings accounts are ideal for achieving short-term financial goals within retirement, such as funding a vacation or covering unexpected medical expenses. By separating these funds from long-term investments, you can ensure that your retirement accounts remain untouched.

- Financial Safety Net: Having savings accounts as part of your retirement planning acts as a safety net. It provides a cushion in case of unexpected events, such as a job loss, healthcare expenses, or major home repairs, allowing you to navigate these situations without depleting your retirement savings.

- Tax Benefits: Depending on the type of savings account used, you may enjoy certain tax advantages. For example, contributions to Health Savings Accounts (HSAs) are tax-deductible, earnings grow tax-free, and withdrawals for qualified medical expenses are tax-free. Consider aligning your savings accounts with your tax strategies to optimize your retirement savings.

- Greater Control over Retirement Finances: Incorporating savings accounts into your retirement plan gives you more control and flexibility over your finances. It allows you to have accessible funds for various needs and gives you the autonomy to make financial decisions that align with your specific retirement goals.

By leveraging the benefits of savings accounts in retirement planning, you can enhance your financial stability, ensure funds are readily available, diversify your investment portfolio, and achieve your short-term financial goals without compromising your long-term retirement funds.

Risks and Challenges in Adding Savings Accounts in Retirement Planning

While savings accounts can offer numerous benefits in retirement planning, it is important to be aware of the potential risks and challenges associated with them. Here are key considerations to keep in mind:

- Low Interest Rates: One of the main drawbacks of savings accounts is that they typically offer lower interest rates compared to other investment options. This means that the growth of your funds may be slower compared to higher-risk investments like stocks or bonds.

- Inflation Risk: Over time, inflation erodes the purchasing power of your savings. If the interest earned on your savings account does not keep pace with inflation, your savings may effectively lose value in real terms. It’s important to carefully consider the impact of inflation and seek strategies to mitigate this risk.

- Opportunity Cost: By allocating a significant portion of your retirement savings to savings accounts, you may miss out on potential returns from other investment options. While savings accounts provide stability, it’s essential to find the right balance between safety and growth potential based on your financial goals and risk tolerance.

- Withdrawal Limitations: Some savings accounts come with withdrawal limitations, which may restrict access to your funds. This can be particularly challenging if you encounter unexpected expenses or need immediate access to cash. Be aware of any penalties or restrictions related to withdrawing funds from your savings accounts.

- Interest Rate Changes: Savings account interest rates are subject to change based on market conditions. This means that the interest you earn on your savings can fluctuate over time, impacting the growth of your funds. Stay informed about potential changes in interest rates and adjust your savings strategy accordingly.

- Fees and Charges: Some savings accounts may come with fees or charges, such as monthly maintenance fees or transaction fees. These costs can eat into your earnings and reduce the overall benefits of the account. It is important to review the fee structure of different savings accounts and choose those with minimal fees or fee waivers.

- Tax Considerations: While savings accounts offer certain tax advantages, it’s essential to understand the tax implications specific to each type of account. For example, interest earned on traditional savings accounts is subject to income tax. Consult with a tax professional to ensure you are maximizing your savings while minimizing any tax liabilities.

It is important to carefully weigh these risks and challenges against the benefits of savings accounts in your retirement planning. Consider diversifying your retirement portfolio with a combination of savings accounts and other investment vehicles to mitigate risks and maximize potential returns.

Strategies to Maximize Savings Accounts in Retirement Planning

While savings accounts may offer lower returns compared to other investment options, there are strategies you can employ to maximize the benefits of these accounts in your retirement planning. Here are some key strategies to consider:

- Shop Around for Competitive Interest Rates: When choosing savings accounts, compare interest rates offered by different financial institutions. Look for accounts that provide competitive rates to maximize the growth of your savings over time.

- Consider High-Yield or Online Savings Accounts: High-yield savings accounts and online banks often offer higher interest rates compared to traditional brick-and-mortar institutions. Explore these options to potentially earn more on your savings.

- Take Advantage of Employer-Matched Savings Programs: If your employer offers a retirement savings match program, contribute enough to receive the full match. This extra contribution effectively boosts your savings and helps you make the most of your retirement benefits.

- Automate Contributions: Set up automatic transfers to your savings accounts to ensure consistent contributions. Automating deposits from your paycheck or checking account can help you maintain a disciplined savings habit and prevent you from inadvertently spending money that should be allocated to retirement savings.

- Determine the Right Allocation: Consider the appropriate allocation of your retirement savings between different accounts. Balance the accessibility and stability of savings accounts with higher-risk, higher-return investments to achieve the potential for growth without sacrificing security.

- Regularly Increase Contributions: As your financial situation improves, aim to increase the amount you contribute to your savings accounts. Regularly review and adjust your budget to allocate more towards savings, ensuring that you’re consistently boosting your retirement savings.

- Minimize Fees and Charges: Be mindful of any fees or charges associated with your savings accounts. Choose accounts with minimal fees or seek fee waiver options to maximize the overall returns on your savings.

- Rebalance and Adjust: Periodically review and rebalance your savings accounts to ensure they align with your retirement goals. Make adjustments as needed, considering factors such as time horizon, risk tolerance, and any changes in financial circumstances.

- Continuously Educate Yourself: Stay informed about personal finance and retirement planning strategies. Attend seminars, read books, or consult with financial advisors to gain insights and make well-informed decisions about your savings accounts and overall retirement strategy.

By implementing these strategies, you can make the most of your savings accounts in retirement planning. Remember, the key is to strike a balance between stability and growth, leveraging savings accounts alongside other investment options to achieve your long-term financial goals.

Conclusion

Integrating savings accounts into your retirement planning can provide a range of benefits, including flexibility, stability, and diversification of investments. By adding savings accounts to your retirement portfolio, you can ensure easy access to funds, achieve short-term financial goals, and create a financial safety net for unexpected expenses.

When choosing savings accounts for retirement, it is essential to consider factors such as interest rates, fees, minimum balance requirements, and accessibility. Evaluate the risks and challenges associated with savings accounts, such as lower interest rates and potential inflation risks, and employ strategies to mitigate these risks.

Maximizing the potential of savings accounts in retirement planning involves shopping around for competitive rates, automating contributions, regularly increasing contributions, and finding the right balance between savings accounts and other investment options. Stay informed, reassess your savings strategy periodically, and adjust when necessary to ensure that your retirement savings align with your financial goals.

Ultimately, incorporating savings accounts into your retirement planning allows for greater security, financial control, and peace of mind. By utilizing these accounts effectively, you can enhance your financial well-being and enjoy a comfortable retirement.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance