Home>Finance>Where To Find Tax-Deferred Pension And Retirement Savings Plans On 1040

Finance

Where To Find Tax-Deferred Pension And Retirement Savings Plans On 1040

Published: January 16, 2024

Looking for tax-deferred pension and retirement savings plans on your 1040? Find all the finance solutions you need right here.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

- Introduction

- Understanding Tax-Deferred Pension and Retirement Savings Plans

- Traditional IRA (Individual Retirement Account)

- Roth IRA (Individual Retirement Account)

- SEP IRA (Simplified Employee Pension)

- SIMPLE IRA (Savings Incentive Match Plan for Employees)

- 401(k) Plan

- 403(b) Plan

- 457(b) Plan

- Thrift Savings Plan (TSP)

- Conclusion

Introduction

Planning for retirement is an essential aspect of financial stability. As people enter different stages of their lives, they often seek ways to save and invest for retirement. One popular approach is to take advantage of tax-deferred pension and retirement savings plans. These plans allow individuals to contribute money towards their retirement while enjoying potential tax benefits.

In this article, we will explore various tax-deferred pension and retirement savings plans that you can consider for your financial planning. By understanding these plans and how they work, you will be better equipped to make informed decisions about your retirement savings.

It’s important to note that tax laws and regulations may vary across different countries, so this article focuses primarily on tax-deferred plans available within the United States.

With that said, let’s dive into the world of tax-deferred pension and retirement savings plans and find out how they can help you secure a financially stable future.

Understanding Tax-Deferred Pension and Retirement Savings Plans

Tax-deferred pension and retirement savings plans are financial vehicles designed to help individuals save for retirement while receiving potential tax benefits. These plans allow individuals to contribute a portion of their income to their retirement savings before taxes are deducted, resulting in a lower taxable income.

One of the key benefits of tax-deferred plans is that the contributions made into these accounts grow tax-free until withdrawal. This means that the earnings on your investments within these plans are not subject to immediate taxation, allowing your savings to potentially grow faster over time.

Additionally, these plans often provide individuals with a range of investment options to choose from, enabling them to customize their portfolios based on their risk tolerance and financial goals.

When it comes time to retire and start accessing the funds in your tax-deferred plan, the withdrawals are typically taxed as ordinary income. However, it’s important to note that depending on the plan and certain eligibility requirements, some withdrawals may be subject to penalties if taken before a specific age or under certain circumstances.

Understanding the different types of tax-deferred pension and retirement savings plans available will help you identify which plan is most suitable for your needs. Let’s explore some of the most common options.

Traditional IRA (Individual Retirement Account)

A Traditional IRA is a popular tax-advantaged retirement account that allows individuals to contribute pre-tax dollars towards their retirement savings. Contributions to a Traditional IRA may be tax-deductible, meaning they can potentially lower your taxable income in the year they are made.

One of the main advantages of a Traditional IRA is the potential for tax-deferred growth. Any earnings on your investments within the account are not subject to taxes until you begin making withdrawals during retirement.

It’s important to note that there are contribution limits for Traditional IRAs, which can vary based on factors such as age and income. For 2021, the maximum contribution limit is set at $6,000 for individuals under the age of 50, with an additional catch-up contribution of $1,000 for individuals age 50 and older.

When you withdraw funds from a Traditional IRA in retirement, the withdrawals are considered taxable income. It’s essential to consider potential tax implications when planning your retirement income strategy.

Another aspect to consider is that individuals who are covered by an employer-sponsored retirement plan, such as a 401(k), may have limitations on their ability to deduct contributions to a Traditional IRA depending on their income. This is known as the “income limit” for deductible contributions.

With a Traditional IRA, you have control over your investment choices, allowing you to select from a wide range of investment options such as stocks, bonds, mutual funds, and more.

In summary, a Traditional IRA offers tax advantages through potential tax-deductible contributions and tax-deferred growth. It provides individuals with flexibility and control over their investments, making it a popular choice for retirement savings.

Roth IRA (Individual Retirement Account)

A Roth IRA is another type of tax-advantaged retirement account that offers distinct advantages compared to a Traditional IRA. Unlike a Traditional IRA, contributions to a Roth IRA are made with after-tax dollars, meaning they are not tax-deductible in the year they are made.

One of the primary benefits of a Roth IRA is that qualified withdrawals in retirement are tax-free. This means that the earnings on your investments within the account can grow tax-free, and when you withdraw funds during retirement, you won’t owe taxes on those withdrawals.

Contributions to a Roth IRA are subject to income limits. For 2021, the eligibility to contribute to a Roth IRA begins to phase out at certain income levels, and individuals with higher incomes may not be eligible to contribute. However, there are strategies such as a backdoor Roth IRA conversion that can potentially allow individuals to contribute to a Roth IRA regardless of income limitations.

Another advantage of a Roth IRA is that unlike a Traditional IRA, there are no required minimum distributions (RMDs) during your lifetime. This means that you can keep the funds in your Roth IRA for as long as you wish, allowing for potential continued tax-free growth.

Similar to a Traditional IRA, a Roth IRA gives you control over your investment choices. You can select from various investment options including stocks, bonds, mutual funds, and more, based on your risk tolerance and financial goals.

One point to consider is that while contributions to a Roth IRA are made with after-tax dollars, there is a unique provision called the “Roth IRA conversion” that allows individuals to convert funds from a Traditional IRA to a Roth IRA, potentially taking advantage of the tax-free growth and tax-free withdrawals in retirement.

In summary, a Roth IRA offers the benefit of tax-free withdrawals in retirement, no required minimum distributions, and potential flexibility for individuals who may not be eligible to contribute to a Traditional IRA due to income limitations. It provides a unique opportunity for tax-free growth and can be a valuable addition to your retirement savings strategy.

SEP IRA (Simplified Employee Pension)

A SEP IRA, short for Simplified Employee Pension IRA, is a retirement plan that allows self-employed individuals and small business owners to contribute to their retirement savings. SEP IRAs are relatively easy to set up and have higher contribution limits compared to traditional IRAs.

SEP IRAs are primarily designed for small businesses or self-employed individuals who do not have a separate retirement plan in place. These plans can also be extended to include eligible employees of the business.

One of the key benefits of a SEP IRA is its high contribution limit. As of 2021, business owners can contribute up to 25% of their net self-employment income or compensation, up to a maximum of $58,000. However, it’s important to note that contributions to SEP IRAs must be made by the employer and are not deducted from the employee’s wages.

Contributions made to a SEP IRA are tax-deductible for the employer. This means that the contributions reduce the employer’s taxable income, providing potential tax savings for the business.

Employees who participate in a SEP IRA have the advantage of having their contributions grow tax-deferred until retirement. Similar to a Traditional IRA, withdrawals from a SEP IRA during retirement are taxed as ordinary income.

SEP IRAs offer flexibility when it comes to investing. Individuals can choose from a variety of investment options such as stocks, bonds, mutual funds, and more, allowing them to tailor their investments to their risk tolerance and financial objectives.

While SEP IRAs offer many advantages, it’s important to remember that they are subject to certain rules. For example, contributions to SEP IRAs must be made by the tax-filing deadline, including extensions, of the business. Additionally, SEP IRAs must cover all eligible employees, and contributions must be proportional to each participant’s income.

In summary, a SEP IRA is a retirement savings plan that provides high contribution limits and tax advantages for self-employed individuals and small business owners. It offers an opportunity to save for retirement while potentially lowering taxable income and allowing for tax-deferred growth.

SIMPLE IRA (Savings Incentive Match Plan for Employees)

A SIMPLE IRA, which stands for Savings Incentive Match Plan for Employees, is a retirement savings plan that is designed for small businesses with 100 or fewer employees. It offers a straightforward and cost-effective way for both employers and employees to save for retirement.

One of the main advantages of a SIMPLE IRA is its simplicity in terms of administration and low costs compared to other retirement plans. Employers have fewer administrative responsibilities and generally lower administrative costs, making it an attractive option for small businesses.

Under a SIMPLE IRA, both employers and employees can make contributions to the plan. Employees can contribute a portion of their salary, up to a certain limit set by the IRS each year. In addition, employers are required to make either a matching contribution or a non-elective contribution on behalf of eligible employees.

Employees can choose to contribute a percentage of their salary or a fixed dollar amount to their SIMPLE IRA. The contributions are made on a pre-tax basis, meaning they are not subject to income taxes at the time of contribution, providing potential tax savings for participants.

Employers have the option to match employee contributions up to a certain percentage of their salary. The matching contribution can be either a dollar-for-dollar match up to a certain percentage or a reduced match, such as 50 cents for every dollar contributed by the employee. Alternatively, employers can choose to make a non-elective contribution to all eligible employees, regardless of whether the employees make their own contributions.

One important aspect of a SIMPLE IRA is that it has lower contribution limits compared to some other retirement plans. For 2021, employees can contribute up to $13,500 to their SIMPLE IRA, with a catch-up contribution of $3,000 for participants aged 50 and older.

Similar to other retirement plans, funds contributed to a SIMPLE IRA grow tax-deferred until withdrawal. Withdrawals made during retirement are generally taxed as ordinary income.

In summary, a SIMPLE IRA offers small businesses a cost-effective and straightforward retirement savings plan for their employees. It allows both employers and employees to make contributions, provides potential tax advantages, and offers an accessible way to save for retirement.

401(k) Plan

A 401(k) plan is a popular employer-sponsored retirement savings plan that allows employees to contribute a portion of their salary on a pre-tax basis. It is named after the section of the Internal Revenue Code that governs these plans.

One of the key advantages of a 401(k) plan is the high contribution limits it offers. For 2021, employees can contribute up to $19,500 to their 401(k) plan, with an additional catch-up contribution of $6,500 for participants aged 50 and older. Employers may also choose to match a portion of their employees’ contributions, providing an additional incentive to save.

Contributions made to a 401(k) plan are tax-deferred, meaning they are not subject to income tax until the funds are withdrawn. This allows for potential tax savings and the opportunity for tax-deferred growth on investments within the plan.

Many 401(k) plans offer a variety of investment options, including mutual funds, index funds, and target-date funds. Participants have the flexibility to choose their investment allocations based on their risk tolerance and financial goals.

One added benefit of a 401(k) plan is the ability to borrow against the account, known as a 401(k) loan. While generally not recommended, a 401(k) loan can provide individuals with access to funds for certain expenses, such as purchasing a home or covering education costs. It’s important to understand the terms and implications of a 401(k) loan before considering this option.

Another feature of a 401(k) plan is the option for a Roth 401(k) contribution. This allows participants to make after-tax contributions to their 401(k) plan, offering the potential for tax-free withdrawals in retirement. Some employers offer a combination of traditional pre-tax contributions and Roth contributions, providing individuals with flexibility based on their tax planning strategies.

While 401(k) plans offer many benefits, it’s important to be aware of any fees associated with the plan, such as management fees or administrative expenses. It’s also crucial to understand the vesting schedule, which dictates when the employer matching contributions are fully owned by the employee.

In summary, a 401(k) plan is a valuable employer-sponsored retirement savings plan that offers high contribution limits, tax advantages, and investment options. It provides individuals with an opportunity to save for retirement while potentially benefiting from employer matching contributions and tax-deferred growth.

403(b) Plan

A 403(b) plan is a retirement savings plan for employees of public schools, tax-exempt organizations, and certain ministers. It is similar to a 401(k) plan in many ways but has specific provisions that cater to the unique circumstances of employees in these sectors.

One of the main advantages of a 403(b) plan is the ability for employees to make pre-tax contributions, reducing their taxable income. These contributions are deducted from the employee’s paycheck before taxes are calculated, providing potential tax savings.

Like a 401(k) plan, the funds contributed to a 403(b) plan grow tax-deferred, meaning that investment earnings within the plan are not subject to taxes until withdrawn. This tax-deferred growth allows for potential accumulation of greater retirement savings over time.

One notable difference between a 403(b) plan and a 401(k) plan is the investment options available. 403(b) plans are often offered through annuity contracts or custodial accounts and typically offer a range of fixed and variable annuities or mutual funds as investment choices. These options cater to the risk tolerance and preferences of employees in the education and nonprofit sectors.

Another unique feature of a 403(b) plan is the opportunity for employees to make additional catch-up contributions if they meet certain requirements. This can be particularly beneficial for individuals approaching retirement age who wish to boost their savings in the years leading up to retirement.

Employees participating in a 403(b) plan may also be eligible for employer contributions. This can come in the form of a matching contribution or a non-elective contribution made by the employer. These contributions increase the overall retirement savings and serve as an additional incentive for employees to save for the future.

While 403(b) plans offer many advantages, it’s important to be aware of any fees associated with the plan, such as administrative fees or investment expenses. Participants should carefully review the investment options available and consider their objectives and risk tolerance when selecting funds.

In summary, a 403(b) plan is a retirement savings plan tailored for employees of public schools, tax-exempt organizations, and certain ministers. It offers tax advantages, a range of investment options, and the potential for employer contributions. By taking advantage of a 403(b) plan, employees in these sectors can effectively save for retirement and work towards achieving financial security.

457(b) Plan

A 457(b) plan is a retirement savings plan available to employees of state and local governments, as well as employees of certain tax-exempt organizations. It is designed to help these employees save for retirement while enjoying potential tax advantages.

One of the key advantages of a 457(b) plan is the ability for employees to make pre-tax contributions, reducing their taxable income. This allows participants to potentially lower their tax liability in the year the contributions are made, providing immediate tax savings.

Contributions to a 457(b) plan grow on a tax-deferred basis, meaning that investment earnings within the plan are not subject to taxes until withdrawn. This tax-deferred growth allows for potential accumulation of greater retirement savings over time.

One notable feature of a 457(b) plan is the absence of an early withdrawal penalty for participants who separate from service before reaching the age of 59 ½. This can be particularly beneficial for employees who retire early or transition to a different job, as they can access their funds without incurring a penalty.

Additionally, participants in a 457(b) plan may have the option to make additional catch-up contributions in the years leading up to retirement if certain criteria are met. This allows individuals nearing retirement to maximize their savings potential and make up for any previous years in which they did not contribute the maximum amount.

Employers may also have the option to make contributions to the 457(b) plan on behalf of eligible employees, providing an additional incentive to save for retirement. However, it’s important to note that contributions made by the employer may be subject to certain limitations and regulations.

When it comes to investment options, 457(b) plans generally offer a range of choices, such as mutual funds, annuities, and other investment vehicles. Participants have the flexibility to select the investment options that align with their risk tolerance and long-term objectives.

While 457(b) plans offer many advantages, it’s important to review the plan details and any associated fees, such as administrative expenses or investment fees, to ensure they align with your needs and goals.

In summary, a 457(b) plan is a retirement savings plan available to employees of state and local governments, as well as certain tax-exempt organizations. It offers tax advantages, the potential for employer contributions, and the flexibility to make additional catch-up contributions. By participating in a 457(b) plan, employees can save for retirement and work towards a financially secure future.

Thrift Savings Plan (TSP)

The Thrift Savings Plan (TSP) is a retirement savings plan available to federal employees, including members of the uniformed services. It is designed to provide federal employees with a cost-effective and convenient way to save for their retirement.

One of the key advantages of the TSP is its low costs. The TSP operates with exceptionally low administrative expenses and investment fees, allowing participants to maximize their savings potential. Moreover, the TSP offers a range of investment options, including various index funds that aim to match broad market performance.

The TSP offers both traditional and Roth contribution options. Traditional contributions are made with pre-tax dollars, reducing the participant’s taxable income in the year of contribution. Roth contributions, on the other hand, are made with after-tax dollars, meaning withdrawals during retirement can potentially be tax-free.

Another advantage of the TSP is the generous employer match known as the automatic agency contribution and the matching contributions for Federal Employees Retirement System (FERS) employees. This match can significantly boost an employee’s retirement savings and is a valuable benefit for federal employees.

Participants of the TSP have the flexibility to choose their contribution rate, select from a variety of investment funds, and adjust their allocations over time. The TSP offers investment options such as government securities, corporate bonds, domestic and international stock funds, and a lifecycle retirement fund that automatically adjusts the asset allocation according to the participant’s target retirement date.

One notable feature of the TSP is the loan option, which allows participants to borrow against their TSP account balance. This can be beneficial for individuals who need access to funds for certain expenses, such as home purchases or education costs. However, it’s important to understand the terms and implications of taking a TSP loan.

When it comes to the withdrawal phase, participants have several options. They can choose to take periodic payments, opt for a single lump-sum distribution, purchase an annuity, or roll over the funds into another eligible retirement account.

In summary, the Thrift Savings Plan (TSP) is a retirement savings plan available to federal employees. It offers low costs, a range of investment options, and the potential for employer matching contributions. By participating in the TSP, federal employees can effectively save for retirement and build a solid financial foundation for their future.

Conclusion

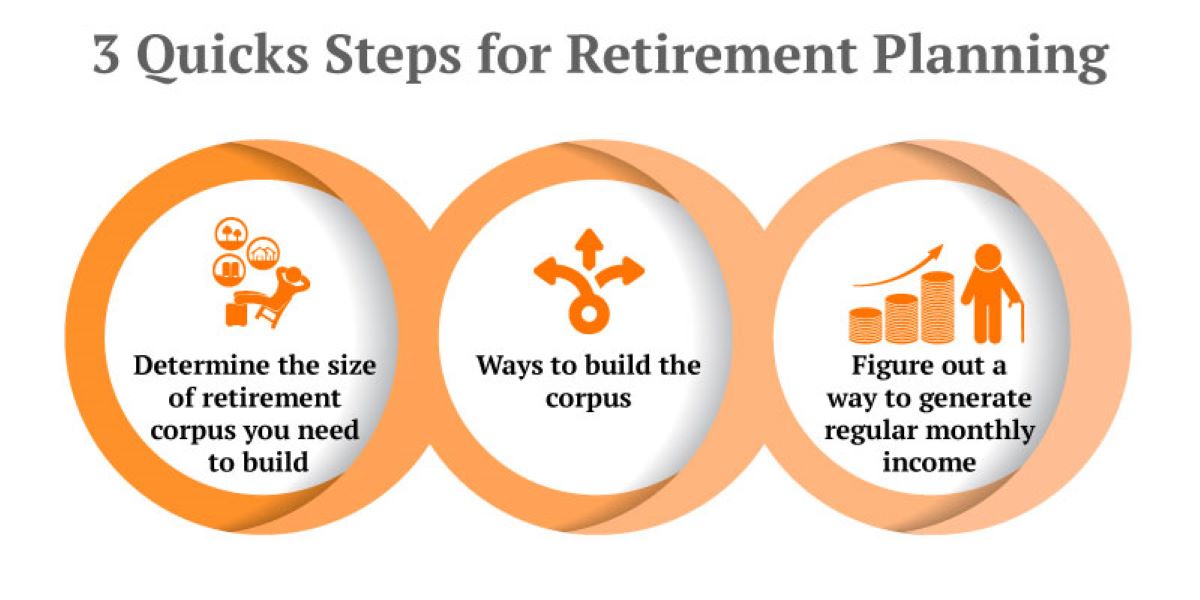

When it comes to planning for retirement, tax-deferred pension and retirement savings plans are powerful tools to help individuals prepare for a financially secure future. Whether you’re self-employed, a small business owner, or an employee of a public sector organization, there are various options available to suit your needs and goals.

In this article, we explored several common tax-deferred pension and retirement savings plans. The Traditional IRA offers potential tax deductions for contributions and tax-deferred growth, while the Roth IRA provides the advantage of tax-free withdrawals during retirement. The SEP IRA and SIMPLE IRA are ideal for self-employed individuals and small businesses, with higher contribution limits and employer contribution options. The 401(k) plan is a well-known employer-sponsored plan that offers high contribution limits and potential employer matching contributions. The 403(b) plan is tailored for employees of educational and nonprofit organizations, while the 457(b) plan caters to state and local government employees. Lastly, the Thrift Savings Plan (TSP) is designed for federal employees, offering low costs and diverse investment options.

Each plan has its own unique features, contribution limits, and tax advantages. When choosing a plan, it’s important to consider factors such as eligibility requirements, contribution limits, investment options, fees, and potential employer contributions. It’s also beneficial to consult with a financial advisor or tax professional to ensure you select the plan that aligns with your retirement goals.

Ultimately, the key is to start saving for retirement as early as possible. Every dollar contributed to these tax-deferred pension and retirement savings plans increases the likelihood of a comfortable retirement. By taking advantage of these plans, individuals can enjoy the potential tax benefits, tax-deferred growth, and employer contributions available to them.

Remember, retirement planning is a journey that requires ongoing assessment and adjustment. Regularly review your retirement goals, monitor your contributions, and reassess your investment strategies to ensure you are on track to meet your retirement objectives.

In conclusion, tax-deferred pension and retirement savings plans provide individuals with opportunities to save for retirement in a tax-efficient manner, maximize their savings potential, and achieve long-term financial security.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance