Home>Finance>How To Find The Minimum Payment On A Credit Card At RBC

Finance

How To Find The Minimum Payment On A Credit Card At RBC

Published: February 26, 2024

Learn how to calculate the minimum payment on your RBC credit card with our helpful finance tips. Take control of your finances today!

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

- Understanding the Basics of Minimum Credit Card Payments at RBC

- The Role of Minimum Payments in Credit Card Management

- Understanding the Calculation and Retrieval Process

- Influential Variables in Minimum Payment Calculations

- Empowering Strategies for Responsible Credit Card Management

- Navigating Minimum Payments with Confidence

Introduction

Understanding the Basics of Minimum Credit Card Payments at RBC

Credit cards are convenient financial tools that offer flexibility and purchasing power. However, it's crucial to understand the responsibilities that come with using credit cards, including making timely payments. One of the most important aspects of managing a credit card is ensuring that the minimum payment is met each month. In this article, we will explore the concept of minimum payments on credit cards, specifically focusing on RBC credit cards, and provide insights into how to effectively manage these payments.

When it comes to credit cards, the minimum payment is the lowest amount a cardholder needs to pay by the due date to keep the account in good standing. Failing to meet this minimum requirement can result in late fees, increased interest charges, and potential damage to one's credit score. Therefore, understanding how minimum payments are calculated and the factors that influence them is essential for responsible credit card management.

In the context of RBC credit cards, it's important for cardholders to grasp the specific guidelines and procedures for determining the minimum payment. By gaining a comprehensive understanding of these details, individuals can make informed financial decisions and effectively manage their credit card obligations. This article will delve into the intricacies of minimum payments on RBC credit cards, offering practical tips and insights to empower cardholders to navigate this aspect of their financial journey with confidence.

Throughout this article, we will discuss how minimum payments are calculated, how to find the minimum payment on an RBC credit card, the factors that influence minimum payments, and valuable tips for managing these payments effectively. By the end of this comprehensive guide, readers will have a clear understanding of the crucial role that minimum payments play in responsible credit card usage and how to navigate this aspect of their financial obligations with ease.

Understanding Minimum Payments on Credit Cards

The Role of Minimum Payments in Credit Card Management

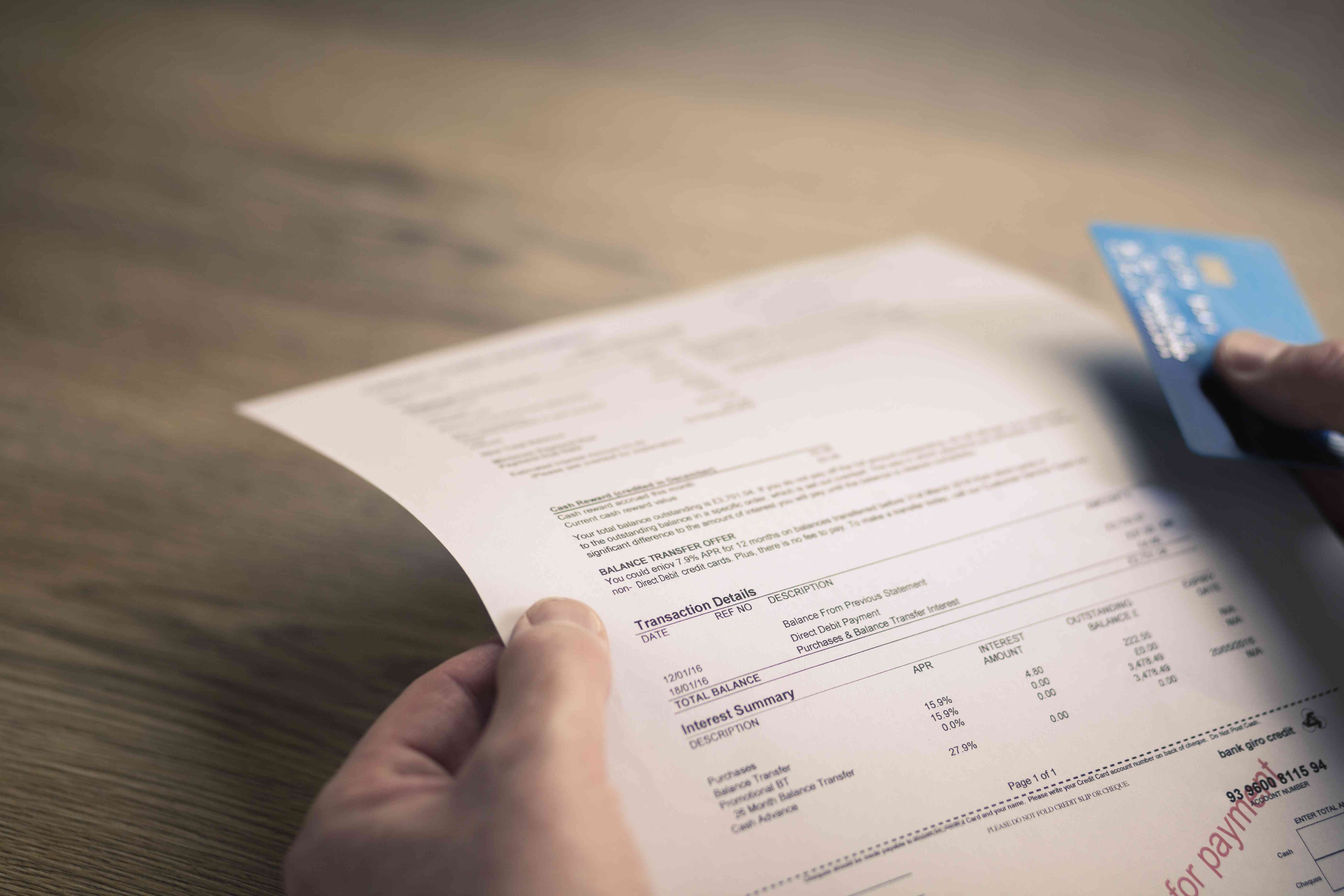

Minimum payments on credit cards serve as the baseline requirement for cardholders to fulfill their financial obligations to the credit card issuer. These payments are typically calculated as a percentage of the outstanding balance, subject to a minimum dollar amount. While making the minimum payment by the due date helps avoid late fees and negative credit reporting, it’s important to recognize that carrying a balance and consistently making minimum payments can lead to long-term interest accrual and potential debt escalation.

When cardholders only make minimum payments, they may find themselves trapped in a cycle of debt, as a significant portion of their payment goes towards interest rather than reducing the principal balance. This can prolong the time it takes to pay off the debt and result in higher overall interest costs. Understanding the implications of minimum payments is crucial for maintaining financial health and making informed decisions about credit card usage.

It’s essential for cardholders to recognize that while minimum payments provide short-term relief by allowing them to meet their immediate financial obligations, they are not a sustainable long-term strategy for managing credit card debt. Responsible credit card usage involves striving to pay more than the minimum whenever possible, thereby reducing the overall balance and minimizing interest charges.

By comprehending the significance of minimum payments and their impact on overall debt management, cardholders can make informed choices about their financial well-being. In the following sections, we will explore how to find the minimum payment on an RBC credit card, the factors that influence minimum payments, and practical tips for effectively managing these payments to maintain financial stability and minimize debt accumulation.

How to Find the Minimum Payment on an RBC Credit Card

Understanding the Calculation and Retrieval Process

As an RBC credit cardholder, it’s essential to have clarity on how the minimum payment is determined for your specific card. RBC provides multiple convenient methods for cardholders to access this information and stay informed about their minimum payment obligations. The following are the primary avenues through which RBC credit cardholders can find their minimum payment details:

- Online Banking: RBC’s online banking platform offers a comprehensive overview of credit card accounts, including the current balance, available credit, and minimum payment due. By logging into their online banking account, cardholders can easily access this information and plan their payments accordingly.

- Mobile App: RBC’s mobile app provides on-the-go access to credit card details, allowing cardholders to view their minimum payment requirements from their mobile devices. This convenient feature enables individuals to stay up to date with their financial obligations while managing their accounts seamlessly.

- Monthly Statements: RBC issues monthly credit card statements that outline the minimum payment due for the billing cycle. Cardholders can refer to these statements to identify the specific amount they are required to pay to meet the minimum payment threshold.

By leveraging these resources, RBC credit cardholders can easily retrieve the details of their minimum payment, empowering them to plan their finances effectively and ensure timely payments. Additionally, RBC’s customer service representatives are readily available to assist cardholders in understanding their minimum payment requirements and addressing any related inquiries.

Understanding the process of finding the minimum payment on an RBC credit card is pivotal for maintaining financial discipline and meeting payment deadlines. By staying informed about their minimum payment obligations, cardholders can navigate their credit card responsibilities with confidence and make informed decisions about managing their finances.

In the subsequent sections, we will delve into the factors that influence minimum payments and provide valuable tips for effectively managing these payments to optimize financial well-being and minimize the impact of credit card debt.

Factors that Affect Minimum Payments

Influential Variables in Minimum Payment Calculations

Several key factors play a role in determining the minimum payment on an RBC credit card. Understanding these variables is essential for cardholders seeking to manage their credit card obligations effectively. The following are the primary factors that influence the calculation of minimum payments:

- Outstanding Balance: The outstanding balance on the credit card directly impacts the minimum payment. Typically, minimum payments are calculated as a percentage of the total balance, ensuring that a higher outstanding amount results in a proportionally higher minimum payment requirement.

- Interest Rate: The annual interest rate, also known as the annual percentage rate (APR), significantly influences the minimum payment. Higher interest rates lead to increased interest charges, thereby affecting the minimum payment amount required to cover both the interest and a portion of the principal balance.

- Fixed Minimum Amount: Some credit cards have a predetermined fixed minimum payment amount, ensuring that cardholders are required to pay at least a specified sum each month, regardless of their outstanding balance or interest charges.

- Fee Assessments: Additional fees, such as late payment fees or over-limit fees, can impact the minimum payment due for a particular billing cycle. These fees are added to the minimum payment amount, increasing the total payment obligation for the cardholder.

By considering these influential factors, RBC credit cardholders can gain insight into the variables that contribute to their minimum payment requirements. This understanding empowers individuals to make informed financial decisions and proactively manage their credit card obligations to maintain financial stability and minimize unnecessary costs.

It’s important for cardholders to recognize that while these factors influence minimum payments, they also present opportunities for proactive debt management. By strategically addressing the outstanding balance, interest rates, and additional fees, individuals can work towards optimizing their minimum payments and ultimately reducing their overall credit card debt.

In the subsequent section, we will provide valuable tips for managing minimum payments on RBC credit cards, offering actionable insights to help cardholders navigate this aspect of their financial responsibilities with confidence and prudence.

Tips for Managing Minimum Payments on Credit Cards at RBC

Empowering Strategies for Responsible Credit Card Management

Effectively managing minimum payments on RBC credit cards is pivotal for maintaining financial health and minimizing the long-term impact of credit card debt. The following tips offer actionable guidance for cardholders seeking to navigate their minimum payment obligations with prudence and foresight:

- Pay More Than the Minimum: Whenever possible, strive to pay more than the minimum required amount. By allocating additional funds towards reducing the outstanding balance, cardholders can minimize interest charges and expedite the repayment process, ultimately reducing the overall cost of credit card debt.

- Monitor Interest Rates: Stay informed about the interest rates associated with the RBC credit card. Understanding the impact of interest charges on the minimum payment empowers cardholders to make informed decisions about managing their balances and prioritizing debt repayment.

- Create a Payment Schedule: Establish a consistent payment schedule to ensure that minimum payments are made on time. By proactively planning and organizing payment deadlines, cardholders can avoid late fees and maintain a positive credit standing.

- Utilize Online Banking Tools: Leverage RBC’s online banking platform to set up payment reminders and automatic transfers. These features streamline the payment process and facilitate proactive management of minimum payment obligations.

- Seek Financial Guidance: If facing challenges in meeting minimum payment requirements, consider reaching out to RBC’s customer service or financial advisors for assistance. Exploring available resources and support can provide valuable insights into managing credit card obligations effectively.

- Limit New Purchases: Exercise restraint in making new purchases on the credit card, especially if struggling to meet minimum payment obligations. Minimizing additional charges can alleviate financial strain and create opportunities to allocate funds towards reducing existing balances.

By integrating these strategies into their financial practices, RBC credit cardholders can proactively manage their minimum payments and work towards optimizing their overall financial well-being. Responsible credit card management involves a combination of informed decision-making, proactive planning, and disciplined financial habits, all of which contribute to long-term financial stability and debt management.

Ultimately, by implementing these tips and maintaining a proactive approach to credit card management, RBC cardholders can navigate their minimum payment obligations with confidence and work towards achieving their broader financial goals.

Conclusion

Navigating Minimum Payments with Confidence

In conclusion, understanding and effectively managing minimum payments on RBC credit cards are integral components of responsible financial management. By grasping the calculation methods, accessing minimum payment details, considering influential factors, and implementing proactive strategies, RBC credit cardholders can navigate their payment obligations with confidence and prudence.

It’s essential for cardholders to recognize that while minimum payments provide short-term relief, they should strive to pay more than the minimum whenever feasible to expedite debt repayment and minimize interest costs. Additionally, staying informed about interest rates, leveraging online banking tools, and establishing consistent payment schedules are instrumental in maintaining financial discipline and meeting payment deadlines.

By proactively managing minimum payments and embracing a proactive approach to credit card management, RBC cardholders can work towards optimizing their overall financial well-being and minimizing the impact of credit card debt. Seeking guidance from financial advisors and exploring available resources can provide valuable support for individuals facing challenges in meeting minimum payment requirements.

Ultimately, responsible credit card management involves a combination of informed decision-making, proactive planning, and disciplined financial habits. By integrating these principles into their financial practices, RBC credit cardholders can navigate their minimum payment obligations with confidence and work towards achieving their broader financial goals.

By applying the insights and strategies outlined in this guide, RBC credit cardholders can empower themselves to make informed decisions, manage their credit card obligations effectively, and progress towards long-term financial stability.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance