Finance

How To Lower My APR With Capital One

Published: March 3, 2024

Learn how to reduce your APR with Capital One and save money on your finances. Discover effective strategies to lower your interest rates and manage your finances wisely.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

Introduction

Welcome to the world of credit and finance, where understanding the intricacies of Annual Percentage Rates (APR) can make a substantial difference in your financial well-being. If you’re a Capital One credit card holder, you may be wondering how to lower your APR and potentially save money on interest charges. Fortunately, there are several strategies you can employ to achieve this goal, and in this article, we’ll explore them in detail.

Capital One is a prominent player in the financial industry, offering a wide range of credit cards tailored to different lifestyles and financial needs. Whether you’re aiming to reduce your existing APR, seeking a better deal on a new card, or simply looking to optimize your financial management, understanding how to lower your APR with Capital One can empower you to make informed decisions and take control of your financial future.

By delving into the factors that influence APR, exploring negotiation tactics, and considering alternative approaches such as balance transfers and credit score improvement, you can gain valuable insights into the mechanisms at play. This knowledge will not only help you reduce your APR but also equip you with a deeper understanding of the credit landscape and how to navigate it effectively.

So, whether you’re a seasoned credit card user or just starting your financial journey, join us as we unravel the strategies for lowering your APR with Capital One, empowering you to make informed decisions and take charge of your financial well-being.

Understanding APR

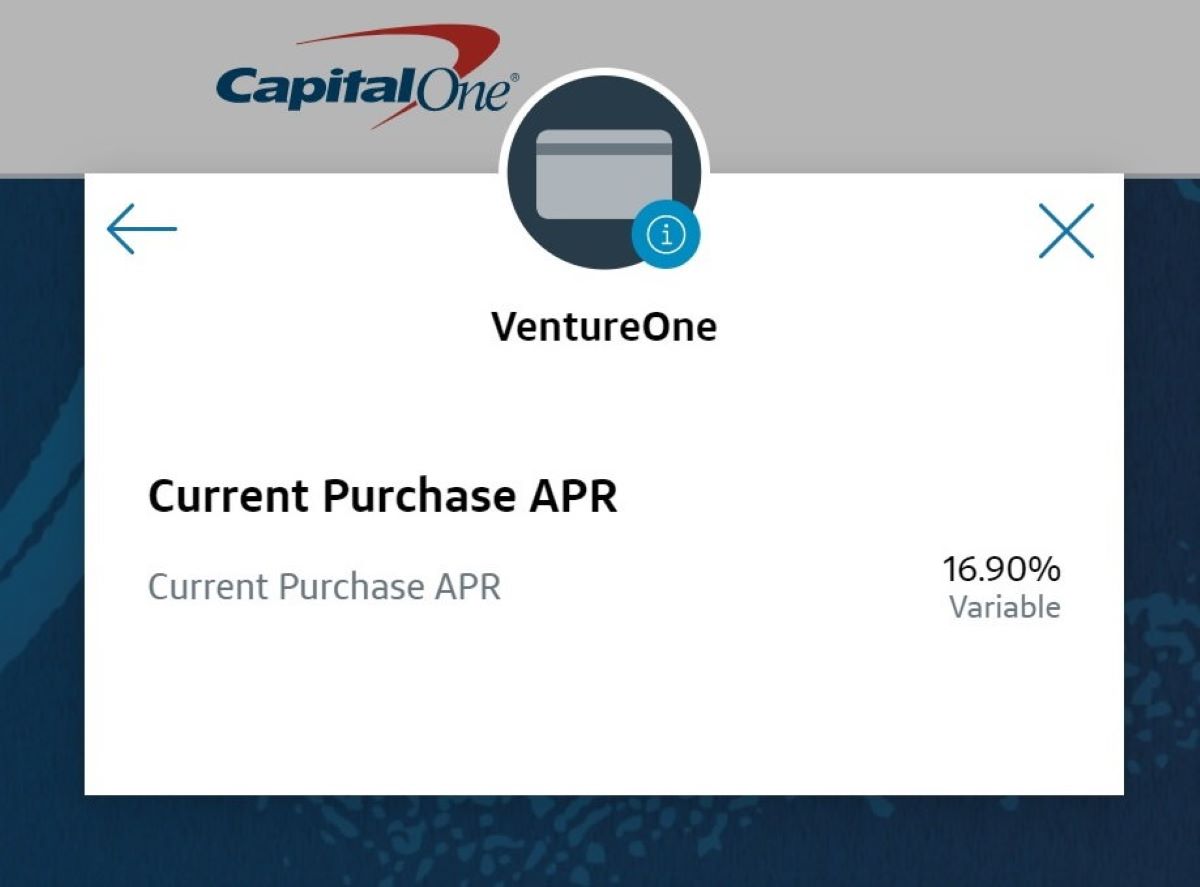

Before delving into the methods for lowering your APR with Capital One, it’s essential to grasp the concept of Annual Percentage Rate (APR) and its significance in the realm of credit cards. APR represents the cost of borrowing on a yearly basis, including interest and certain fees, expressed as a percentage. For credit card users, the APR directly influences the amount of interest accrued on outstanding balances, making it a crucial factor in managing credit card debt.

It’s important to note that APR can vary based on several factors, including the type of transaction (such as purchases, balance transfers, or cash advances) and the cardholder’s creditworthiness. Additionally, many credit card issuers, including Capital One, offer different APRs for different card products, with some featuring promotional rates for a specified period.

When examining your credit card statement, you’ll typically find several APRs listed, each corresponding to different types of transactions. For instance, you may have a separate APR for purchases, balance transfers, and cash advances. Understanding these distinctions is crucial, as it enables you to discern the specific rates applied to various activities and plan your repayment strategy accordingly.

Furthermore, it’s important to be aware of the potential impact of variable APRs, which can fluctuate based on changes in the prime rate or other economic factors. This variability can lead to adjustments in the interest charged on your outstanding balances, underscoring the need for vigilance in monitoring your credit card terms and conditions.

By gaining a comprehensive understanding of APR and its nuances, you can navigate the credit card landscape with greater confidence and insight. This knowledge forms the foundation for exploring strategies to lower your APR with Capital One, empowering you to make informed decisions and optimize your credit management.

Ways to Lower Your APR with Capital One

When it comes to reducing your Annual Percentage Rate (APR) with Capital One, several effective strategies can potentially lead to a lower interest burden and greater financial savings. By leveraging these approaches, you can take proactive steps to optimize your credit card terms and enhance your overall financial well-being.

- Understanding Promotional Offers: Capital One frequently introduces promotional offers and incentives for both existing and new cardholders. By staying informed about these promotions, you can capitalize on opportunities to secure a lower APR for a specified period or benefit from reduced fees. Keeping a close eye on promotional campaigns and special offers can provide avenues for minimizing your interest costs and maximizing your savings.

- Enhancing Your Creditworthiness: Improving your credit score and financial profile can significantly influence the APR you receive from Capital One. By demonstrating responsible credit behavior, such as making timely payments, maintaining low credit utilization, and managing your debts prudently, you can enhance your creditworthiness and potentially qualify for a lower APR. Capital One, like other issuers, often rewards responsible cardholders with improved terms, making it advantageous to focus on bolstering your credit standing.

- Exploring Card Upgrades: Capital One offers a diverse range of credit cards, each with distinct features and terms. By exploring the possibility of upgrading to a different Capital One card, you may gain access to more favorable APRs and enhanced benefits. Certain cards within the Capital One portfolio may be tailored to individuals with strong credit profiles, offering lower APRs and superior rewards. Engaging with Capital One to explore potential card upgrades can present opportunities to secure a more advantageous APR structure.

By strategically leveraging these methods, you can position yourself to potentially lower your APR with Capital One, thereby reducing your interest expenses and optimizing your credit card terms. Each approach offers a unique avenue for enhancing your financial standing and maximizing the value derived from your credit relationship with Capital One.

Negotiating with Capital One

Engaging in proactive negotiations with Capital One can be a powerful strategy for potentially securing a lower Annual Percentage Rate (APR) and improving your overall credit card terms. While credit card terms are typically set by the issuer based on various factors, including the cardholder’s creditworthiness and prevailing market conditions, there are instances where negotiating with Capital One can yield favorable outcomes.

When initiating negotiations with Capital One to lower your APR, it’s essential to approach the process with a clear understanding of your credit history, payment behavior, and the prevailing market conditions. Armed with this knowledge, you can present a compelling case for why a lower APR would be beneficial for both you and the issuer. Here are some effective strategies for negotiating with Capital One:

- Highlighting Your Loyalty and Payment History: Demonstrating a history of responsible credit card usage and loyalty to Capital One can serve as a compelling basis for negotiating a lower APR. By showcasing your consistent payment record, long-standing relationship with the issuer, and positive account behavior, you can present a strong case for why you deserve a more favorable APR.

- Researching Competing Offers: Prior to initiating negotiations, it’s beneficial to research and compare competing credit card offers, particularly those with lower APRs and favorable terms. By presenting Capital One with evidence of more attractive offers available in the market, you can underscore the rationale for seeking a lower APR to align with prevailing industry standards.

- Seeking Assistance from Customer Service: Capital One’s customer service representatives can be valuable allies in your negotiation efforts. Engaging with customer service to express your desire for a lower APR and articulate the reasons behind your request can potentially lead to a constructive dialogue and a reevaluation of your credit card terms.

By approaching negotiations with Capital One in a proactive and informed manner, you can potentially influence the terms of your credit card agreement and secure a more advantageous APR. While outcomes may vary based on individual circumstances and market conditions, the act of initiating negotiations demonstrates a proactive approach to managing your credit and seeking optimal terms for your financial well-being.

Transferring Your Balance

Transferring your credit card balance to a new or existing Capital One card with a lower Annual Percentage Rate (APR) can be a strategic and effective method for reducing your interest expenses and consolidating your credit card debt. Balance transfers enable you to move existing balances from high-APR cards to those offering more favorable terms, potentially saving you money and simplifying your repayment process.

When considering a balance transfer with Capital One, it’s important to assess the terms and conditions associated with the transfer, including any promotional APR periods, balance transfer fees, and the long-term APR after the promotional period expires. Here are key considerations and steps to take when contemplating a balance transfer:

- Evaluating Promotional Balance Transfer Offers: Capital One frequently extends promotional balance transfer offers to cardholders, providing opportunities to transfer balances at reduced or 0% APR for a specified period. By evaluating these offers and understanding the duration of the promotional period, associated fees, and post-promotion APR, you can assess the potential benefits of initiating a balance transfer.

- Assessing the Impact on Your Financial Goals: Before proceeding with a balance transfer, it’s essential to consider how it aligns with your financial objectives. Assess whether the transfer will contribute to debt consolidation, interest savings, or simplification of your repayment strategy. Understanding the impact on your financial goals can guide your decision-making process.

- Weighing the Costs and Benefits: While balance transfers can offer significant interest savings, it’s crucial to factor in any associated balance transfer fees and the long-term APR after the promotional period. By conducting a cost-benefit analysis, you can determine whether the potential interest savings outweigh the initial transfer costs.

By carefully evaluating these considerations and understanding the implications of a balance transfer, you can make an informed decision about leveraging this strategy to lower your APR with Capital One. Additionally, maintaining diligent repayment discipline and avoiding new charges on the transferred balance can further enhance the effectiveness of this approach, positioning you for improved financial management and reduced interest expenses.

Improving Your Credit Score

Enhancing your credit score can be a transformative strategy for potentially securing a lower Annual Percentage Rate (APR) with Capital One and other credit card issuers. A strong credit score not only reflects your creditworthiness but also influences the terms and APRs available to you. By focusing on credit score improvement, you can position yourself for more favorable APRs and enhanced financial opportunities.

Here are actionable steps to improve your credit score and potentially lower your APR with Capital One:

- Monitor Your Credit Report: Regularly reviewing your credit report enables you to identify inaccuracies, address discrepancies, and gain insights into factors impacting your credit score. By ensuring the accuracy of your credit report, you can maintain a solid foundation for credit score improvement.

- Manage Your Payment History: Timely payments are a cornerstone of a strong credit score. Consistently paying your bills on time demonstrates financial responsibility and positively impacts your creditworthiness, potentially leading to more favorable APRs from Capital One.

- Reduce Credit Utilization: Keeping your credit utilization ratio—the amount of credit used versus the total credit available—low can bolster your credit score. Aim to minimize outstanding balances and avoid maxing out your credit cards, as this can signal financial strain to lenders.

- Diversify Your Credit Mix: A well-rounded credit portfolio that includes a mix of credit cards, loans, and other credit accounts can contribute to a more robust credit score. By diversifying your credit mix responsibly, you can demonstrate your ability to manage different types of credit, potentially enhancing your creditworthiness in the eyes of Capital One.

- Limit New Credit Inquiries: Multiple credit inquiries within a short timeframe can have a negative impact on your credit score. Minimize new credit applications unless necessary, as excessive inquiries may signal financial instability to potential lenders, including Capital One.

By proactively addressing these factors and focusing on credit score improvement, you can potentially position yourself for a lower APR with Capital One, as well as gain access to more favorable credit terms and products. Additionally, maintaining a vigilant approach to credit management and consistently monitoring your credit score can pave the way for enhanced financial opportunities and long-term credit health.

Conclusion

As you navigate the realm of credit card management and seek to lower your Annual Percentage Rate (APR) with Capital One, it’s essential to approach the process with a strategic and informed mindset. Understanding the various avenues for potentially reducing your APR and optimizing your credit card terms can empower you to make impactful financial decisions and enhance your overall financial well-being.

From comprehending the nuances of APR and the factors that influence it to exploring strategies such as negotiating with Capital One, leveraging balance transfers, and focusing on credit score improvement, you have a range of tools at your disposal to potentially secure a lower APR and minimize your interest expenses. Each of these approaches offers distinct benefits and considerations, enabling you to tailor your strategy to align with your financial goals and circumstances.

By staying attuned to promotional offers, maintaining a positive credit history, and engaging in proactive negotiations, you can position yourself to potentially secure a more advantageous APR with Capital One. Furthermore, the strategic use of balance transfers and a concerted focus on credit score improvement can yield long-term benefits, strengthening your financial foundation and expanding your access to favorable credit terms.

As you embark on this journey to lower your APR with Capital One, remember that each step you take toward financial empowerment and credit management contributes to a more secure and prosperous financial future. By leveraging these strategies and maintaining a disciplined approach to credit card usage, you can not only reduce your APR but also enhance your overall financial resilience and well-being.

Ultimately, the pursuit of a lower APR with Capital One is a testament to your proactive approach to financial management and your commitment to optimizing your credit card terms. By harnessing these strategies and insights, you can navigate the credit landscape with confidence, secure in the knowledge that you are actively shaping a brighter financial future for yourself.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance