Finance

How To Use A Secured Card

Published: March 1, 2024

Learn how to use a secured card to build credit and improve your financial standing. Discover the benefits and best practices for managing your finances effectively.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

**

Introduction

**

If you're looking to establish or rebuild your credit, a secured card can be a valuable tool to achieve your financial goals. This type of credit card is designed to help individuals with limited or damaged credit history access a line of credit by providing a security deposit. Understanding how to use a secured card effectively can pave the way for improving your credit score and gaining financial independence.

A secured card operates similarly to a traditional credit card, but with one key difference: the cardholder must provide a cash deposit as collateral, which typically determines the credit limit. This security deposit reduces the risk for the card issuer, making it an accessible option for individuals with a limited credit history or a lower credit score.

By responsibly managing a secured card, individuals can demonstrate their creditworthiness and establish a positive credit history. This can open doors to better financial opportunities, such as qualifying for unsecured credit cards, loans, and favorable interest rates in the future.

In the following sections, we will delve into the mechanics of secured cards, from understanding how they work to the process of applying for one. We will also explore the best practices for using a secured card responsibly, leveraging it to build credit, and monitoring your card activity to ensure financial stability. By the end of this guide, you will have a comprehensive understanding of how to harness the potential of a secured card to improve your financial standing.

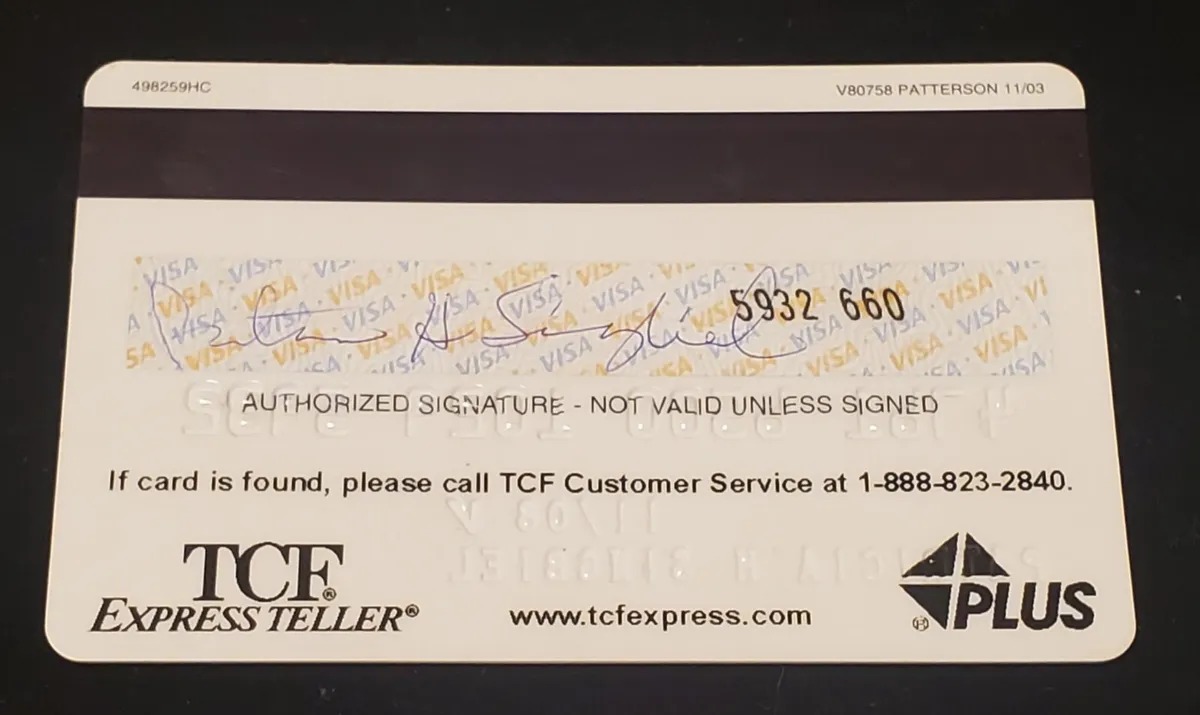

What is a Secured Card?

A secured card is a type of credit card that requires the cardholder to provide a cash deposit as collateral, which serves as security for the card issuer. This deposit typically determines the credit limit of the card. Unlike traditional unsecured credit cards, which are extended based on the cardholder’s creditworthiness and financial history, secured cards offer a way for individuals with limited or damaged credit to access a line of credit.

Secured cards are often recommended for individuals who are new to credit or are working to rebuild their credit. By providing a security deposit, the cardholder mitigates the risk for the issuer, making it a viable option for those who may not qualify for an unsecured credit card due to a lack of credit history or a low credit score.

While secured cards require a cash deposit, they function similarly to traditional credit cards. Cardholders can make purchases, pay bills, and build a credit history by using the card responsibly. Many secured card issuers report card activity to the major credit bureaus, which can help individuals establish a positive credit history when payments are made on time and balances are kept low.

It’s important to note that a secured card is not a prepaid card. With a prepaid card, the cardholder loads funds onto the card to use for purchases, and the spending is limited to the available balance. In contrast, a secured card is a true credit card, and the security deposit is held as collateral in the event that the cardholder defaults on payments.

Overall, a secured card provides an opportunity for individuals to demonstrate responsible credit management while building or rebuilding their credit history. By understanding the mechanics of secured cards and their role in the credit landscape, individuals can make informed decisions about utilizing this financial tool to improve their financial standing.

How Does a Secured Card Work?

A secured card operates on the same fundamental principles as a traditional credit card, with the added layer of security provided by a cash deposit. When a cardholder opens a secured card account, they are required to make a security deposit, which typically determines the credit limit of the card. This deposit serves as collateral and reduces the risk for the card issuer, allowing individuals with limited credit history or lower credit scores to access a line of credit.

Once the secured card account is opened and the security deposit is provided, the cardholder can use the card to make purchases, just like with a standard credit card. It’s important to note that the security deposit is not used to pay off monthly charges; it is held as collateral in case the cardholder defaults on payments. Cardholders are still responsible for making monthly payments on their secured card balance, and failure to do so can result in the forfeiture of the security deposit and damage to the cardholder’s credit.

Many secured card issuers report card activity to the major credit bureaus, which means that responsible use of a secured card can help individuals build or rebuild their credit history. Making timely payments and keeping card balances low can have a positive impact on the cardholder’s credit score over time.

It’s important to understand the terms and conditions of a secured card, including any fees associated with the account. Some secured cards may have annual fees, monthly maintenance fees, or other charges that should be considered when evaluating the overall cost of the card. Additionally, cardholders should be aware of the interest rates associated with their secured card, as carrying a balance from month to month can result in accruing interest charges.

By understanding how a secured card works and the responsibilities that come with it, individuals can make informed decisions about how to use this financial tool to improve their credit standing. The next section will delve into the process of applying for a secured card and the considerations involved in choosing the right card for your financial needs.

Applying for a Secured Card

When considering applying for a secured card, it’s important to research and compare the offerings of various card issuers to find the best fit for your financial needs. Here are the key steps involved in the application process:

Research and Comparison:

Begin by researching secured card options from different financial institutions, including banks and credit unions. Compare factors such as the minimum required security deposit, annual fees, interest rates, and any rewards or benefits offered. Look for a secured card that aligns with your financial goals and offers terms that are favorable for your circumstances.

Application Process:

Once you’ve selected a secured card that suits your needs, you can initiate the application process. This typically involves filling out an application form provided by the card issuer. You may be required to provide personal information, such as your full name, address, social security number, employment details, and income information. Be prepared to consent to a credit check, as the issuer will assess your creditworthiness as part of the application review.

Security Deposit:

After submitting your application, you will be required to make a security deposit to fund the secured card. The amount of the deposit often determines the credit limit of the card. This deposit is held as collateral and is refundable when the secured card account is closed, provided that the cardholder has fulfilled their payment obligations and the account is in good standing.

Account Activation:

Upon approval of your secured card application and receipt of the security deposit, the card issuer will activate your secured card account. You will receive the physical card, along with instructions on how to manage your account online or through mobile banking apps. It’s essential to review the terms and conditions provided by the issuer to understand the account features, fees, and payment due dates.

Responsible Use and Credit Building:

Once you have your secured card in hand, it’s crucial to use it responsibly to build or rebuild your credit history. Make regular purchases within your means and ensure that you pay off the balance on time each month. By demonstrating responsible credit management, you can improve your credit score over time and work towards qualifying for an unsecured credit card in the future.

By following these steps and utilizing a secured card wisely, individuals can embark on a journey to strengthen their credit profile and pave the way for improved financial opportunities. In the next section, we will explore the best practices for using a secured card responsibly to maximize its benefits.

Using a Secured Card Responsibly

Using a secured card responsibly is essential for building a positive credit history and maximizing the benefits of this financial tool. Here are key strategies for responsible secured card usage:

Timely Payments:

One of the most impactful ways to demonstrate responsible credit management is by making timely payments on your secured card balance. Paying at least the minimum amount due by the due date can help you avoid late fees and, more importantly, contribute to a positive payment history, which is a crucial factor in determining your credit score.

Low Credit Utilization:

Keeping your credit utilization low is important for maintaining a healthy credit profile. Aim to use only a small portion of your available credit each month, ideally below 30% of your credit limit. This shows that you can manage your credit responsibly and can positively impact your credit score.

Avoiding Cash Advances:

While some secured cards may offer cash advance options, it’s advisable to avoid using this feature whenever possible. Cash advances often come with high fees and interest rates, and utilizing them can lead to unnecessary debt and financial strain.

Regular Monitoring:

Stay vigilant about monitoring your secured card activity. Review your monthly statements to verify all transactions and ensure there are no unauthorized charges. Monitoring your account can also help you track your spending habits and stay within your budget.

Graduating to an Unsecured Card:

As you build a positive credit history with your secured card, you may become eligible to transition to an unsecured credit card. Some card issuers offer the opportunity to "graduate" to an unsecured card after demonstrating responsible card usage over a period of time. This can open doors to higher credit limits, better rewards, and improved financial flexibility.

Regular Account Reviews:

Periodically review the terms and conditions of your secured card account. As your credit improves, you may qualify for better terms, lower fees, or the opportunity to upgrade to an unsecured card with the same issuer. Staying informed about your options can help you make strategic decisions to further enhance your credit profile.

By implementing these responsible usage strategies, individuals can harness the full potential of a secured card to strengthen their credit standing and pave the way for a healthier financial future. In the next section, we will explore the process of building credit with a secured card and the long-term benefits it can yield.

Building Credit with a Secured Card

A secured card can be a powerful tool for building or rebuilding your credit history. By using the card responsibly and making timely payments, you can demonstrate your creditworthiness and establish a positive credit profile. Here’s how a secured card can help in building credit:

Positive Payment History:

Consistently making on-time payments on your secured card demonstrates responsible credit management and contributes to a positive payment history. Payment history is a significant factor in determining your credit score, and by paying your secured card balance in full and on time each month, you can bolster your creditworthiness.

Credit Utilization Ratio:

Your credit utilization ratio, which is the amount of credit you’re using compared to your total credit limit, plays a crucial role in your credit score. By keeping your credit utilization low and using only a small portion of your available credit, you can show that you are not overly reliant on credit, which can positively impact your credit score.

Establishing Credit History:

For individuals who are new to credit, a secured card provides an opportunity to begin establishing a credit history. By using the card responsibly and building a track record of on-time payments, you can lay a solid foundation for future credit endeavors, such as obtaining a car loan or a mortgage.

Credit Score Improvement:

Over time, responsible use of a secured card can lead to an improvement in your credit score. As you demonstrate creditworthy behavior, such as paying bills on time and managing credit responsibly, credit scoring models may reflect the positive changes in your credit profile, potentially leading to an increase in your credit score.

Qualifying for Unsecured Credit:

As your credit history strengthens with a secured card, you may become eligible to apply for an unsecured credit card. Some secured card issuers offer the opportunity to transition to an unsecured card after a period of responsible card usage. This can expand your credit options and open doors to higher credit limits and better rewards.

By leveraging a secured card to build credit, individuals can lay the groundwork for improved financial opportunities and a stronger credit standing. In the following section, we will delve into the importance of monitoring your secured card activity and maintaining financial stability as you build and manage your credit.

Monitoring Your Secured Card Activity

Regularly monitoring your secured card activity is essential for maintaining financial stability and safeguarding your credit profile. Here are key practices for effectively monitoring your secured card:

Reviewing Monthly Statements:

Take the time to carefully review your monthly secured card statements. Verify all transactions to ensure they are accurate and authorized. Monitoring your statements can help you detect any unauthorized charges or errors promptly.

Tracking Spending Habits:

By reviewing your secured card statements, you can gain insights into your spending patterns and identify areas where you may need to adjust your budget. Understanding your spending habits can help you make informed financial decisions and stay on track with your financial goals.

Monitoring Credit Utilization:

Keep an eye on your credit utilization, which is the amount of credit you’re using compared to your total credit limit. Maintaining a low credit utilization ratio can positively impact your credit score. Monitoring this metric can help you make adjustments to your spending to keep your credit utilization in check.

Alerts and Notifications:

Many secured card issuers offer account alerts and notifications that can be set up to provide real-time updates on account activity. These alerts can include payment due reminders, transaction alerts for large purchases, and notifications for when your statement is available. Leveraging these features can help you stay on top of your finances and avoid missing important deadlines.

Reporting Errors or Discrepancies:

If you identify any errors or discrepancies in your secured card activity, promptly report them to your card issuer. This can involve unauthorized charges, billing errors, or any other irregularities. Resolving these issues in a timely manner can help protect your financial interests and prevent potential damage to your credit standing.

Regular Credit Reports:

Obtain and review your credit reports from the major credit bureaus on a regular basis. Your credit reports provide a comprehensive overview of your credit accounts, payment history, and other factors that contribute to your credit score. Monitoring your credit reports can help you spot any inaccuracies or signs of potential identity theft.

By staying proactive in monitoring your secured card activity, you can maintain financial awareness and ensure that your credit profile remains healthy. In the concluding section, we will summarize the key insights into using a secured card effectively and its impact on building a solid credit foundation.

Conclusion

Understanding how to use a secured card effectively is a valuable skill for individuals looking to establish or improve their credit standing. A secured card offers a pathway to accessing credit, even for those with limited credit history or lower credit scores. By providing a security deposit as collateral, individuals can obtain a secured card and use it to demonstrate responsible credit management.

Throughout this guide, we’ve explored the mechanics of secured cards, from the application process to the responsible usage strategies that can lead to credit improvement. Secured cards serve as a stepping stone for individuals to build or rebuild their credit history, paving the way for future financial opportunities.

Key takeaways from this guide include the importance of making timely payments, maintaining low credit utilization, and monitoring secured card activity to ensure financial stability. By adhering to these best practices, individuals can leverage a secured card to bolster their creditworthiness and work towards qualifying for unsecured credit in the future.

Ultimately, the journey of using a secured card responsibly is a transformative one, leading to improved financial literacy, disciplined budgeting, and a stronger credit foundation. As individuals progress in their credit-building journey, they may find themselves eligible for better financial products, improved interest rates, and enhanced purchasing power.

By embracing the principles outlined in this guide and committing to sound financial habits, individuals can harness the potential of a secured card to shape a brighter financial future. With dedication and strategic credit management, the path to achieving a solid credit standing becomes attainable, setting the stage for long-term financial well-being and stability.

As you embark on your journey with a secured card, remember that responsible credit usage is a continuous process that yields enduring benefits. By staying informed, proactive, and diligent in your financial endeavors, you can navigate the credit landscape with confidence and achieve your long-term financial aspirations.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance