Finance

How To Use Annuities In Retirement Planning

Published: January 21, 2024

Learn how to incorporate annuities into your retirement planning and ensure a secure financial future. Discover valuable finance tips and guidance for retirement.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

- Introduction

- What are Annuities?

- Types of Annuities

- Benefits of Using Annuities in Retirement Planning

- Considerations Before Purchasing Annuities

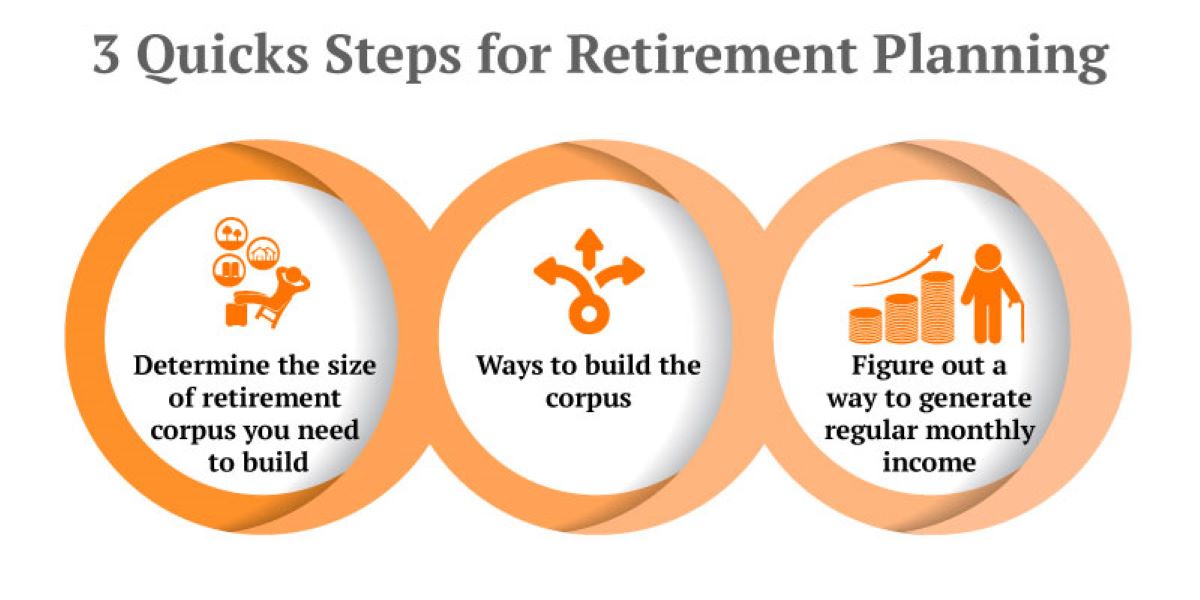

- How to Use Annuities in Retirement Planning

- Step 1: Determine Your Retirement Income Needs

- Step 2: Research Different Annuity Providers

- Step 3: Consult with a Financial Advisor

- Step 4: Choose the Right Type of Annuity

- Step 5: Determine the Annuity Payout Option

- Step 6: Set Up the Annuity Contract

- Step 7: Monitor and Review Your Annuity Performance

- Conclusion

Introduction

Planning for retirement can be a daunting task, and ensuring a steady stream of income during your golden years is crucial. While there are several investment options available, annuities have gained popularity as an effective tool for retirement planning. Annuities offer a unique way to receive regular payments after retirement, providing financial security and peace of mind.

In this article, we will explore what annuities are, the various types of annuities, and the benefits of using annuities in retirement planning. We will also discuss important considerations before purchasing annuities and provide a step-by-step guide on how to use annuities effectively in your retirement planning strategy.

Annuities are essentially insurance contracts that provide a regular income stream in exchange for a lump sum payment or a series of payments. They are commonly used to supplement other retirement savings and pension income. Annuities are typically offered by insurance companies and can be customized to meet individual retirement income needs.

As you delve into the world of annuities, it’s important to understand the different types available. The most common types include fixed annuities, variable annuities, indexed annuities, and immediate annuities. Each type has its own features and benefits, so it’s essential to choose the one that aligns with your financial goals and risk tolerance.

Using annuities in retirement planning can offer several advantages. First and foremost, annuities provide a reliable and predictable stream of income, which can help cover day-to-day expenses, medical costs, and other financial obligations in retirement. Annuities can also offer tax advantages, such as deferred taxes on earnings until withdrawals are made.

Furthermore, annuities provide protection against market volatility. Unlike other investment options like stocks or mutual funds, annuities offer a guaranteed return on investment, ensuring that your principal amount is protected. This can be particularly beneficial for individuals who prefer a more conservative approach to retirement planning.

However, before purchasing annuities, there are a few considerations to keep in mind. It’s important to evaluate the credibility and financial stability of the annuity provider. Additionally, understanding the terms and conditions of the annuity contract, including fees and surrender charges, is crucial. Finally, consulting with a financial advisor can help you make informed decisions and ensure that annuities align with your overall retirement strategy.

In the following sections, we will guide you through the process of using annuities effectively in your retirement planning. By following these steps, you can optimize the benefits of annuities and create a secure financial future for your retirement years.

What are Annuities?

Annuities are financial products offered by insurance companies that provide individuals with a guaranteed stream of income during retirement. They are essentially a contract between the individual, known as the annuitant, and the insurance company, where the annuitant makes a lump sum payment or a series of payments in exchange for regular income payments in the future.

There are several types of annuities, each with its own unique features and benefits. The most common types include:

- Fixed Annuities: With fixed annuities, the insurance company guarantees a fixed interest rate for a specific period of time. This provides the annuitant with a stable, predictable income stream. It is an attractive option for individuals who prefer a conservative approach to retirement planning and are looking for a guaranteed return on their investment.

- Variable Annuities: Variable annuities allow the annuitant to invest in a variety of investment options, such as stocks, bonds, and mutual funds. The income generated from variable annuities is not fixed and fluctuates depending on the performance of the underlying investments. This type of annuity offers the potential for higher returns but also carries higher risk.

- Indexed Annuities: Indexed annuities are linked to the performance of a specific financial index, such as the S&P 500. They provide a minimum guaranteed interest rate along with the opportunity to earn additional interest based on the performance of the index. Indexed annuities offer a balance between fixed and variable annuities, providing some potential for growth while protecting against market downturns.

- Immediate Annuities: Immediate annuities provide immediate income payments to the annuitant. They are typically purchased with a lump sum payment and can be a suitable option for individuals who need to start receiving income right away. The income generated from immediate annuities can be fixed or variable, depending on the annuitant’s preference.

Annuities can be tailored to suit individual needs, offering different payout options. Some common payout options include:

- Life Only: The annuitant receives income payments for the rest of their life, with no further payments made upon their death. This provides the highest monthly income but does not offer any continuation of payments for beneficiaries.

- Period Certain: Income payments are made for a specific period of time, typically 10, 15, or 20 years. If the annuitant passes away before the end of the specified period, the payments continue to the designated beneficiaries.

- Joint and Survivor: Income payments are made to the annuitant for their lifetime and continue to their spouse or designated beneficiary upon their death.

- Indexed Payout: Annuity payments increase over time, usually with a fixed interest rate or tied to the performance of a specific index.

Overall, annuities provide a reliable source of income in retirement and can offer protection against market volatility. They can play a crucial role in diversifying retirement income sources and providing financial stability during your golden years.

Types of Annuities

Annuities come in various forms, each designed to cater to different financial goals and risk tolerances. Understanding the different types of annuities can help you make an informed decision when planning for retirement. Here are the most common types of annuities:

- Fixed Annuities: Fixed annuities provide a guaranteed interest rate for a specific period of time. The rate remains fixed throughout the contract term, offering stability and predictability. This type of annuity is suitable for individuals who prefer a conservative approach to retirement planning and prioritize a steady source of income over potential high returns.

- Variable Annuities: Variable annuities allow you to invest in a range of investment options such as stocks, bonds, and mutual funds. The rate of return is not fixed and depends on the performance of the underlying investments. While variable annuities carry more risk, they also offer the potential for higher returns. This type of annuity is suited for individuals who are comfortable with market fluctuations and are seeking growth opportunities in their retirement portfolio.

- Indexed Annuities: Indexed annuities are linked to the performance of a specific financial index, such as the S&P 500. They offer a guaranteed minimum interest rate along with the potential for additional interest based on the performance of the chosen index. Indexed annuities provide a balance between the stability of fixed annuities and the potential for growth found in variable annuities.

- Immediate Annuities: Immediate annuities are designed to provide income right away. With an immediate annuity, you make a lump sum payment to the insurance company, and in return, you receive regular income payments immediately or within one year of purchase. This type of annuity is suitable for individuals who need immediate income during retirement.

- Deferred Annuities: Deferred annuities are designed to accumulate funds over a set period before making regular income payments. They can be either fixed or variable annuities. Deferred annuities are an effective tool for long-term retirement planning, allowing your investment to grow tax-deferred until you start receiving income.

Each type of annuity has its own advantages and considerations. It is important to carefully assess your financial goals, risk tolerance, and retirement income needs before choosing the type of annuity that best aligns with your requirements.

It’s worth noting that annuities can also be categorized based on their payout options. Some common payout options include:

- Life Only: The annuitant receives income payments for their lifetime, with no further payments made upon their death. This option provides the highest monthly income but does not offer any continuation of payments for beneficiaries.

- Period Certain: Annuity payments are made for a specific period of time, such as 10, 15, or 20 years. If the annuitant passes away before the end of the specified period, the remaining payments are made to the designated beneficiaries.

- Joint and Survivor: Income payments are made to the annuitant for their lifetime and continue to their spouse or designated beneficiary upon their death.

Choosing the right type of annuity involves careful consideration of your financial circumstances and retirement goals. It is advisable to consult with a financial advisor who can help evaluate your specific needs and guide you through the annuity selection process.

Benefits of Using Annuities in Retirement Planning

Annuities offer a range of benefits that make them a valuable tool for retirement planning. They provide individuals with a reliable source of income and can help ensure financial security during their golden years. Here are some key benefits of using annuities in retirement planning:

- Steady Stream of Income: Annuities provide a predictable and regular income stream, which can help cover essential expenses in retirement. This reliable cash flow can alleviate financial stress and provide peace of mind.

- Tax Advantages: Annuities offer tax advantages that can help maximize income during retirement. Earnings within an annuity grow tax-deferred until withdrawals are made. This can potentially lower your tax liability, especially if you are in a lower tax bracket during retirement.

- Protection Against Market Volatility: Unlike other investment options like stocks or mutual funds, annuities provide a guaranteed return on investment. This ensures that your principal amount is protected and shields you from the impact of market fluctuations. Having a portion of your retirement savings in annuities can provide stability and minimize the risk associated with market volatility.

- Income Tailored to Your Needs: Annuities can be customized to meet your specific income needs and goals. Depending on the type of annuity and payout option you choose, you can receive income for a set period of time or for the rest of your life, providing flexibility and long-term financial planning opportunities.

- Lifetime Income: Many annuities offer the option of receiving income for life, ensuring that you won’t outlive your savings. This protection against longevity risk is particularly valuable as life expectancies continue to increase.

- Ability to Leave a Legacy: Some annuities allow you to designate beneficiaries who will continue to receive income after your passing. This feature ensures that your loved ones are provided for and can create a lasting legacy.

- Options for Long-Term Care: Certain annuity contracts offer riders or features that can help cover long-term care expenses. These long-term care annuities provide additional protection and financial support should you require extended care later in life.

It is important to note that while annuities offer many benefits, they are not suitable for everyone. Consider your individual financial situation, risk tolerance, and retirement goals before deciding if annuities are right for you. Additionally, it is recommended to consult with a financial advisor who can provide personalized guidance based on your specific needs.

By leveraging the benefits of annuities in your retirement planning, you can create a solid foundation for your financial security and enjoy a comfortable retirement lifestyle.

Considerations Before Purchasing Annuities

While annuities can be a valuable tool for retirement planning, it is important to carefully consider certain factors before making the decision to purchase one. Understanding these considerations will help ensure that annuities align with your financial goals and meet your retirement income needs. Here are some key considerations to keep in mind:

- Financial Stability of the Annuity Provider: Before purchasing an annuity, it is essential to evaluate the financial stability and credibility of the insurance company offering the annuity. You want to choose a reputable and well-established company that has a strong track record of fulfilling its financial obligations.

- Annuity Fees and Charges: Annuities often come with various fees and charges, such as administrative fees, mortality and expense fees, and surrender charges. It is important to understand these costs and how they may impact your overall returns. Compare fees across different annuity providers to ensure you are getting a competitive deal.

- Surrender Period: Annuities typically have a surrender period, during which you may face penalties if you need to withdraw funds from the annuity before a certain period of time has elapsed. Understand the terms of the surrender period and carefully consider whether you may need access to your funds during that time.

- Guarantees and Benefits: Review the guarantees and benefits offered by the annuity, such as minimum interest rates, death benefits, and inflation protection. Assess whether these features align with your long-term financial goals and risk tolerance.

- Flexibility and Liquidity: Consider the level of flexibility and liquidity you need. Annuities are designed for long-term retirement income and may not offer the same level of liquidity as other investment options. Understand the limitations on withdrawals and assess whether you have other accessible sources of funds for unexpected expenses.

- Impact on Taxes: While annuities provide tax advantages, it is important to understand the tax implications of annuity withdrawals and income payments. Consult with a tax professional to assess the potential tax consequences and determine the most tax-efficient strategies for your retirement income.

- Consult with a Financial Advisor: Given the complexity of annuities and the significant financial commitment involved, it is highly recommended to consult with a qualified financial advisor. An advisor can help evaluate your individual circumstances, assess your retirement goals, and guide you through the annuity selection process.

Making an informed decision when purchasing an annuity is crucial to ensure that it aligns with your financial objectives and retirement needs. Taking the time to consider these factors and seeking professional guidance will help you make the right choice and maximize the benefits of annuities in your retirement planning.

How to Use Annuities in Retirement Planning

Using annuities effectively in your retirement planning can provide a reliable source of income and help secure your financial future. To make the most of annuities, consider following these steps:

- Determine Your Retirement Income Needs: Start by assessing your anticipated living expenses during retirement. Consider factors such as housing, healthcare, travel, and leisure activities. Understanding your income needs will help determine the appropriate amount to allocate to an annuity for generating consistent cash flow.

- Research Different Annuity Providers: Take the time to research and compare annuity providers. Look for reputable companies with a history of financial stability and excellent customer reviews. Consider factors such as the variety of annuity products offered, fees and charges, and customer service reputation.

- Consult with a Financial Advisor: Seek guidance from a qualified financial advisor who can help evaluate your financial goals and determine the role annuities should play in your retirement plan. An advisor can provide personalized recommendations based on your unique circumstances and help ensure that annuities align with your overall retirement strategy.

- Choose the Right Type of Annuity: Consider your risk tolerance and retirement income goals when selecting an annuity type. Fixed annuities provide stability and guaranteed income, while variable annuities offer potential growth but carry more risk. Discuss the pros and cons of each type with your financial advisor to make an informed decision.

- Determine the Annuity Payout Option: Decide on the annuity payout option that best suits your needs. You may opt for a lifetime income stream, periodic payments for a fixed term, or a joint and survivor option if you have a spouse or partner who will rely on the annuity income as well. Consider your longevity expectations and desire for potential inheritance when choosing the payout option.

- Set Up the Annuity Contract: Once you have selected the annuity provider, type, and payout option, it’s time to set up the annuity contract. Review the contract carefully, ensuring that all terms and conditions are clearly stated and align with your expectations. Seek clarification from the annuity provider or your financial advisor if you have any questions or concerns.

- Monitor and Review Your Annuity Performance: Regularly review the performance of your annuity to ensure it continues to align with your retirement goals. Stay informed about any changes in fees, interest rates, or market conditions that may affect your annuity. Maintain periodic communication with your financial advisor to assess whether adjustments are necessary to optimize your annuity for your evolving needs.

Remember that annuities are long-term commitments and should be considered as part of a broader retirement income strategy. They work best when combined with other sources of income, such as Social Security benefits and investment portfolios. Regularly reassess your retirement plan and make adjustments as needed to ensure a comfortable and secure financial future.

By following these steps and seeking professional guidance, you can effectively incorporate annuities into your retirement planning and enjoy the benefits of steady and reliable income throughout your golden years.

Step 1: Determine Your Retirement Income Needs

When using annuities in retirement planning, the first step is to determine your retirement income needs. This involves assessing your anticipated living expenses and understanding how much income you will require during your retirement years.

To get started, consider the following aspects:

- Lifestyle and Expenses: Evaluate your current lifestyle and estimate how it may change in retirement. Consider factors such as housing costs, healthcare expenses, transportation, groceries, and leisure activities. Create a comprehensive budget that includes both essential and discretionary expenses.

- Inflation: Take into account the impact of inflation on your future expenses. Prices tend to rise over time, so it’s important to factor in the potential increase in the cost of living during your retirement years. Consider using an inflation rate of around 2-3% to adjust your income needs accordingly.

- Healthcare Costs: Healthcare expenses can be significant during retirement. Estimate your healthcare needs based on your current health condition, family history, and potential future medical expenses. Consider the cost of health insurance, Medicare premiums, prescription drugs, and long-term care insurance, if applicable.

- Debt and Obligations: Take into account any outstanding debts or financial obligations you may have. Consider factors such as mortgage payments, credit card debts, and other loans. Determine if you will need a steady income stream to cover these obligations during your retirement years.

- Expected Retirement Age: Determine the age at which you plan to retire. This will help determine the number of years you will need to fund with your retirement savings. Keep in mind that the earlier you retire, the longer your retirement income will need to last.

- Expected Social Security Benefits: Take into account any expected Social Security benefits you will receive during retirement. Understand how these benefits contribute to your overall retirement income and consider how they align with your income needs.

By carefully evaluating these factors, you can develop a realistic estimate of your retirement income needs. This will serve as a foundation for determining the amount of income you will require from annuities and other income sources.

It’s important to be thorough and accurate when estimating your retirement income needs. Consider consulting with a financial advisor to ensure your calculations are comprehensive and aligned with your specific circumstances.

Keep in mind that your retirement income needs may change over time. Regularly reassess your expenses and adjust your plan accordingly as you approach retirement. By staying proactive and flexible, you can adapt your retirement income strategy to meet your evolving needs and enjoy a financially secure retirement.

Step 2: Research Different Annuity Providers

Once you have determined your retirement income needs, the next step is to research different annuity providers. This step is essential in finding a reputable and reliable company that offers annuity products that align with your retirement goals. Take the time to compare and evaluate various annuity providers to make an informed decision. Here are some key factors to consider during your research:

- Reputation and Financial Stability: Look for annuity providers with a solid reputation and a history of financial stability. Check their ratings from independent rating agencies such as Standard & Poor’s or Moody’s. Ensure they have a good track record of honoring their annuity contracts and paying claims promptly.

- Product Variety: Consider the range of annuity products offered by each provider. Look for providers that offer a variety of annuity types, such as fixed, variable, indexed, and immediate annuities. Having options allows you to choose the type of annuity that best suits your needs and preferences.

- Customer Service: Assess the quality of customer service provided by each annuity provider. Look for providers that have a reputation for excellent customer support and responsive communication. Consider reading customer reviews and testimonials to gauge the overall customer experience.

- Fees and Charges: Review the fees and charges associated with the annuity products offered by each provider. Compare costs such as administrative fees, mortality and expense fees, and surrender charges. Ensure that the fees are reasonable and competitive within the market.

- Financial Strength: Analyze the financial strength of the annuity providers by reviewing their financial reports and stability. Look for companies with strong financial ratings and solid capital reserves. A financially strong annuity provider is better positioned to fulfill its financial obligations and honor annuity payments.

- Additional Benefits and Features: Consider any additional benefits or features offered by the annuity providers. This could include options for long-term care coverage, enhanced death benefits, or inflation protection. Assess whether these features align with your specific retirement planning needs.

- Expert Opinions: Seek recommendations and expert opinions from trusted sources, such as financial advisors or retirement planning experts. They can offer valuable insights and guidance based on their experience and knowledge of the annuity market.

By conducting thorough research and considering these factors, you can narrow down your options and select annuity providers that meet your criteria. Remember to keep your retirement income needs and goals in mind as you assess each provider and their offerings.

Researching annuity providers is a crucial step in the annuity selection process. It ensures that you choose a reputable and trustworthy company that can provide the financial security and income stream you need for your retirement years.

Step 3: Consult with a Financial Advisor

When it comes to using annuities in retirement planning, seeking guidance from a qualified financial advisor is highly recommended. A financial advisor can provide personalized advice and help you navigate the complexities of annuities, ensuring that your retirement strategy aligns with your financial goals and needs. Here’s why consulting with a financial advisor is an important step:

- Expert Knowledge: A financial advisor has specialized knowledge and expertise in retirement planning and annuities. They can explain the intricacies of different annuity types, payout options, and contract terms. They stay up-to-date with changes and trends in the annuity market, allowing them to provide valuable insights and guidance related to your specific situation.

- Assessment of Your Financial Situation: A financial advisor will assess your overall financial situation, including your income, assets, debts, and investment portfolio. They will consider your retirement goals, risk tolerance, and income needs. Based on this comprehensive evaluation, they can determine whether annuities are suitable for you and to what extent they should be incorporated into your retirement plan.

- Customized Recommendations: A financial advisor can provide tailored recommendations based on your unique circumstances and retirement goals. They can help you determine the optimal amount to allocate to annuities, taking into account other sources of retirement income, such as Social Security benefits and investment portfolios. They can also help you select the most appropriate annuity type and payout option based on your risk tolerance and income needs.

- Annuity Selection Assistance: With their expertise, financial advisors can assist you in the annuity selection process. They can research and recommend reputable annuity providers for you to consider. They will assess the financial stability, product offerings, fees, and charges of different providers to ensure they align with your expectations.

- Risk Management: Financial advisors can help you assess and manage the risks associated with annuities and other investment options. They will explain the potential benefits and limitations of annuities, ensuring that you have a clear understanding of the risks involved. They can also discuss strategies for diversification and asset allocation to minimize risk and maximize your overall retirement income.

- Long-Term Relationship: Building a long-term relationship with a financial advisor can provide ongoing support and guidance throughout your retirement journey. As your financial needs and goals evolve, they can help you adjust your annuity strategy and make necessary changes to ensure your plan remains on track.

When choosing a financial advisor, look for individuals who are experienced, certified, and aligned with your values and goals. Seek recommendations from trusted sources, conduct interviews, and ask about their approach to retirement planning and their expertise in annuities.

Working with a financial advisor brings invaluable expertise, objectivity, and peace of mind to your retirement planning process. It ensures that you have a knowledgeable professional by your side, guiding you through the complexities of annuities and helping you make informed decisions for a secure financial future.

Step 4: Choose the Right Type of Annuity

After consulting with a financial advisor and understanding your retirement goals and income needs, the next step is to choose the right type of annuity. Different types of annuities offer varying features, benefits, and risks, so it’s important to select the one that aligns with your specific requirements. Consider the following factors when making your decision:

- Risk Tolerance: Assess your risk tolerance and determine whether you are comfortable with potential market fluctuations. Fixed annuities provide a guaranteed interest rate, making them suitable for individuals seeking stability and minimal risk. Variable annuities, on the other hand, allow for potential market growth but come with market risk.

- Income Goals: Consider your income goals and how you want to receive the annuity payments. Fixed annuities offer a predictable income stream, which may be appealing if you want a steady and reliable source of income. Variable annuities, on the other hand, provide the potential for growth, which may be beneficial if you desire higher income potential.

- Growth Potential: Evaluate your desire for potential growth. Fixed annuities provide a guaranteed interest rate, offering stability but limited growth potential. Variable annuities allow for investment in various asset classes, providing the possibility of higher returns but also exposing you to market risk.

- Tax Considerations: Understand the tax implications of different annuity types. Earnings within annuities grow tax-deferred until withdrawals are made. Fixed and variable annuities provide the potential for tax-deferred growth, while immediate annuities may have different tax implications depending on the source of the funds used to purchase the annuity.

- Flexibility: Consider the flexibility you require with your annuity. Fixed annuities have limited flexibility, as the interest rate is fixed for a specified period. Variable annuities offer more flexibility and potential for adjustments based on investment performance. Immediate annuities provide immediate income but lack the flexibility to change the payout structure later.

- Longevity Considerations: Factor in your life expectancy and longevity expectations. If you anticipate a longer lifespan, consideration might be given to annuities offering lifetime income options. This ensures that you receive income for as long as you live, providing protection against outliving your savings.

Based on these factors, work with your financial advisor to select the most suitable annuity type for your retirement plan. It’s important to choose an annuity that aligns with your risk tolerance, income goals, and desire for potential growth. Your financial advisor can provide personalized advice based on your specific circumstances and help you make an informed decision.

Remember that annuity contracts can vary among annuity providers, so review the contract details carefully. Understand the terms and conditions, including any fees, surrender charges, and specific features. Clear any doubts or queries you may have with your financial advisor or the annuity provider before making your final decision.

By selecting the right type of annuity, you can ensure that your retirement income needs are met and your financial goals are on track. Regularly reassess your annuity choice as your circumstances may change, and consult with your financial advisor to make any necessary adjustments to your annuity strategy.

Step 5: Determine the Annuity Payout Option

After selecting the type of annuity that suits your retirement needs, the next step is to determine the annuity payout option. The payout option determines how and when you will receive income from your annuity. Each option has its own advantages and considerations, so it’s important to choose the one that aligns with your financial goals and needs. Consider the following factors when determining the annuity payout option:

- Lifetime Income: The lifetime income option guarantees income for the rest of your life, irrespective of how long you live. This option offers the highest level of income security and is suitable if you are concerned about outliving your savings. However, it usually does not provide any payments to beneficiaries upon your passing.

- Period Certain: With a period certain annuity, you receive income for a specific period of time, such as 10, 15, or 20 years. If you pass away before the end of the specified period, your beneficiaries will continue to receive the remaining payments. This option offers the advantage of ensuring that someone will receive the full benefit of the annuity if you pass away before the term ends.

- Joint and Survivor: The joint and survivor option provides income for your lifetime and continues to your spouse or designated beneficiary upon your passing. This option ensures that your spouse or beneficiary is financially protected even after your death. Keep in mind that the initial income amount may be lower compared to other options due to the joint coverage.

- Indexed Payout: Some annuities offer indexed payout options where income payments increase over time, typically with a fixed interest rate or tied to the performance of a specific index. This option helps protect against inflation by providing income that keeps pace with rising costs over the long term.

When choosing the annuity payout option, consider your longevity expectations, marital status, and desire for potential inheritance. Evaluate your income needs and determine whether you prioritize maximizing income during your lifetime or providing financial support to beneficiaries.

Consult with your financial advisor to understand the implications of each payout option and how it aligns with your overall retirement strategy. They can provide personalized advice based on your specific circumstances, helping you make an informed decision.

Remember that the annuity payout option is typically irreversible once chosen, so consider your decision carefully. Review the terms and conditions of the annuity contract regarding payout options and discuss any concerns with your financial advisor or the annuity provider.

By selecting the most appropriate annuity payout option, you can ensure that your retirement income is structured to meet your needs and provide financial security, both for yourself and your loved ones.

Step 6: Set Up the Annuity Contract

Once you have determined the type of annuity and the payout option that aligns with your retirement goals, it is time to set up the annuity contract. This step involves finalizing the annuity agreement with the chosen annuity provider. Here’s what you need to do:

- Review the Contract: Carefully review the annuity contract and the associated terms and conditions. Understand the specific details of the annuity, such as the interest rate, fees, charges, and any riders or additional features that may be included. Ensure that the contract provisions align with your expectations and the discussions you had with your financial advisor.

- Complete Application and Documentation: Fill out the annuity application form provided by the annuity provider. Provide all necessary documentation and information accurately, including your personal details, beneficiary information, and designated payment preferences. Be prepared to provide identification documents and financial statements as required.

- Submit the Application: Submit the completed application form and supporting documents to the annuity provider. Follow their specified submission process, which may involve mailing the documents or submitting them electronically through their online portal. Keep a copy of all documents for your records.

- Make the Initial Payment: If required, make the initial payment for the annuity as specified in the contract. This payment may be a lump sum or a series of payments, depending on the terms of the annuity. Ensure that the payment method aligns with your financial capabilities and preferences.

- Beneficiary Designations: Review and confirm the beneficiary designations for the annuity. Consider naming primary and contingent beneficiaries to ensure that your assets are distributed according to your wishes in the event of your passing. Periodically review and update these designations as needed throughout your retirement journey.

- Read and Understand the Contract: It is crucial to thoroughly read and understand the annuity contract before signing it. If you have any questions or concerns, seek clarification from the annuity provider or consult with your financial advisor. Signing the contract signifies your agreement to the terms, so make sure you are comfortable with what has been laid out.

- Maintain a Copy for Your Records: Keep a copy of the fully executed annuity contract and other related documents for your records. These documents serve as a reference and should be readily accessible in case you need to review or reference them in the future.

Setting up the annuity contract is an important step that lays the foundation for your retirement income. Ensure that you carefully review and understand all aspects of the contract before proceeding. If you have any doubts or concerns, consult with your financial advisor to ensure that you are making an informed decision.

Remember to periodically review your annuity contract and stay informed about any updates or changes made by the annuity provider. Stay proactive in managing your annuity and continue to communicate with your financial advisor to assess whether any adjustments or changes are necessary based on your evolving retirement needs.

By following these steps and setting up the annuity contract properly, you are on your way to enjoying the benefits of a structured and secure retirement income stream.

Step 7: Monitor and Review Your Annuity Performance

Once you have set up your annuity contract, it’s important to regularly monitor and review its performance. Monitoring your annuity ensures that it continues to align with your retirement goals and provides the expected benefits. Here are some key considerations for monitoring and reviewing your annuity performance:

- Stay Informed: Stay informed about any updates or changes related to your annuity. This might include changes in interest rates, fees, or the annuity provider’s policies. Review the communications and statements provided by the annuity provider to keep track of your annuity’s performance.

- Evaluate Income Payments: Regularly assess the income payments you receive from your annuity. Ensure that the payments are accurate and consistent with the terms of your annuity contract. If any discrepancies or issues arise, contact the annuity provider promptly to address them.

- Review Fees and Charges: Understand the fees and charges associated with your annuity. Regularly review the fee structure and ensure that the charges are reasonable and align with industry standards. If you have concerns about the fees, discuss them with your financial advisor or contact the annuity provider for clarification.

- Assess Investment Performance: If you have a variable annuity, monitor the performance of the underlying investments. Evaluate how the investments are performing compared to your expectations and market conditions. If needed, consult with your financial advisor to make any necessary adjustments to your investment portfolio within the annuity.

- Consider Changes in Circumstances: Life circumstances may change over time, impacting your retirement goals and income needs. Regularly reassess your retirement plan and consider whether any adjustments or changes to your annuity strategy are necessary. Changes in factors such as health, income, or family situations may warrant modifications to your annuity contract.

- Annual Reviews with Your Financial Advisor: Schedule annual reviews with your financial advisor to discuss your overall retirement strategy, including the performance of your annuity. Your advisor can evaluate whether the annuity is meeting your expectations and make recommendations based on the latest market trends and your evolving needs.

- Consider Market Conditions: Monitor broader market conditions and economic trends that could impact your annuity and retirement plan. Stay informed about interest rate changes, inflation rates, and other factors that may influence your annuity’s performance. This awareness allows you to make informed decisions and adjust your annuity strategy accordingly.

Monitoring and reviewing your annuity performance ensures that it remains in line with your retirement goals and provides the financial security you expect. Regularly communicating with your financial advisor and staying proactive in managing your annuity will help optimize its benefits throughout your retirement journey.

Remember that while annuities offer a reliable income stream, they are just one component of a comprehensive retirement plan. Regularly evaluate your entire retirement portfolio, considering other sources of income and adjusting your annuity strategy as needed.

By staying actively involved in monitoring and reviewing your annuity performance, you can adapt your retirement plan to changing circumstances and make informed decisions to support your long-term financial well-being.

Conclusion

Incorporating annuities into your retirement planning can provide a reliable and secure source of income during your golden years. By following the steps outlined in this guide, you can effectively utilize annuities to help meet your retirement income needs while safeguarding your financial future.

In Step 1, you determined your retirement income needs by assessing your expenses and factoring in inflation, healthcare costs, and debt obligations. Armed with this understanding, you proceeded to Step 2, conducting research to identify reputable annuity providers offering the types of annuities that align with your goals.

Step 3 stressed the importance of consulting with a financial advisor who can provide expertise and personalized advice. This guidance ensures that annuities are integrated into your retirement plan appropriately and tailored to your specific circumstances.

Having gained insights from your financial advisor, Step 4 involved selecting the right type of annuity that matches your risk tolerance, income goals, and growth potential. Step 5 focused on determining the annuity payout option that best suits your longevity expectations, marital status, and desire for inheritance.

Once the annuity contract is set up in Step 6, it is vital to regularly monitor and review its performance and stay informed about any updates or changes. This proactive approach, outlined in Step 7, ensures that your annuity continues to align with your retirement goals and evolving financial needs.

In conclusion, annuities can play a significant role in retirement planning. They provide a dependable stream of income and offer protection against market volatility while providing tax benefits and flexibility. However, careful consideration of factors such as financial stability, fees, and payout options is crucial when choosing annuities.

By following the steps outlined in this guide and working with a financial advisor, you can effectively utilize annuities in your retirement planning and enjoy a financially secure and comfortable retirement. Remember to regularly reassess your annuity strategy and make adjustments as needed to ensure it aligns with your changing circumstances and goals.

Retirement planning is a complex process, and annuities are just one piece of the puzzle. It is always recommended to seek the guidance of financial professionals who can provide comprehensive advice tailored to your specific needs. With careful planning and informed decision-making, you can create a solid foundation for a financially stable and fulfilling retirement.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance