Finance

How To Forecast Interest Rates

Published: November 1, 2023

Learn how to forecast interest rates in the finance industry with these expert tips and strategies. Stay ahead of market trends and make informed financial decisions.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

- Introduction

- Understanding Interest Rates

- Factors Affecting Interest Rates

- Economic Indicators for Interest Rate Forecasting

- Analyzing Historical Interest Rate Data

- Using Yield Curve to Forecast Interest Rates

- Forward Rate Agreements and Interest Rate Futures

- Macroeconomic Models for Interest Rate Forecasting

- Market-Based Approaches for Interest Rate Forecasting

- Conclusion

Introduction

Interest rates play a crucial role in the world of finance. They have a direct impact on borrowing costs, investment decisions, saving strategies, and overall economic growth. For individuals, businesses, and governments, accurately forecasting interest rates is of utmost importance in order to make informed financial decisions.

In this article, we will explore various methods and techniques that can be used to forecast interest rates. From understanding the factors affecting interest rates to analyzing historical data and using different models, we will delve into the intricacies of interest rate forecasting.

Forecasting interest rates is not a simple task. Interest rates can be influenced by a multitude of factors, including economic indicators, inflation rates, central bank policies, and global market trends. Therefore, it is essential to examine these variables closely and use a combination of quantitative analysis, economic insights, and market-based approaches to come up with accurate interest rate forecasts.

Successful interest rate forecasting can provide individuals and businesses with valuable insights. For example, if you are a homeowner looking to refinance your mortgage, knowing the future direction of interest rates can help you decide when to lock in a lower rate. Similarly, businesses can determine the best time to secure loans for expansion or allocate funds for investments based on their interest rate projections.

In the following sections, we will discuss the key factors affecting interest rates, various economic indicators used for forecasting, how historical data can inform our predictions, as well as other advanced techniques such as using the yield curve, forward rate agreements, macroeconomic models, and market-based approaches.

It is important to note that interest rate forecasting is not an exact science, and no method can guarantee a foolproof prediction. However, by carefully analyzing the available data and considering the economic climate, it is possible to generate reasonably accurate forecasts that can guide financial decisions.

Without further ado, let’s dive into the fascinating world of interest rate forecasting and explore the techniques that can help us navigate the complex terrain of the financial markets.

Understanding Interest Rates

Before delving into interest rate forecasting, it is crucial to have a clear understanding of what interest rates are and how they function. In simple terms, interest rates represent the cost of borrowing money or the return on investment. They are expressed as a percentage and typically calculated annually.

Interest rates are determined by the interaction of various economic factors, including supply and demand dynamics in the loanable funds market, inflation expectations, central bank policies, and overall economic conditions. When the demand for credit is high and the supply of available funds is limited, interest rates tend to rise. Conversely, when the demand for credit is low and there is an abundance of available funds, interest rates tend to decrease.

Interest rates play a critical role in financial markets and have a significant impact on consumers, businesses, and governments. For consumers, interest rates affect the cost of borrowing, including mortgages, car loans, and credit card debt. For businesses, interest rates influence the cost of capital and can impact investment decisions and access to financing.

In the realm of government finance, interest rates directly affect the cost of borrowing for governments, impacting public debt levels and influencing fiscal policies. Moreover, interest rates also play a role in monetary policy, as central banks use them as a tool to manage economic growth and maintain price stability.

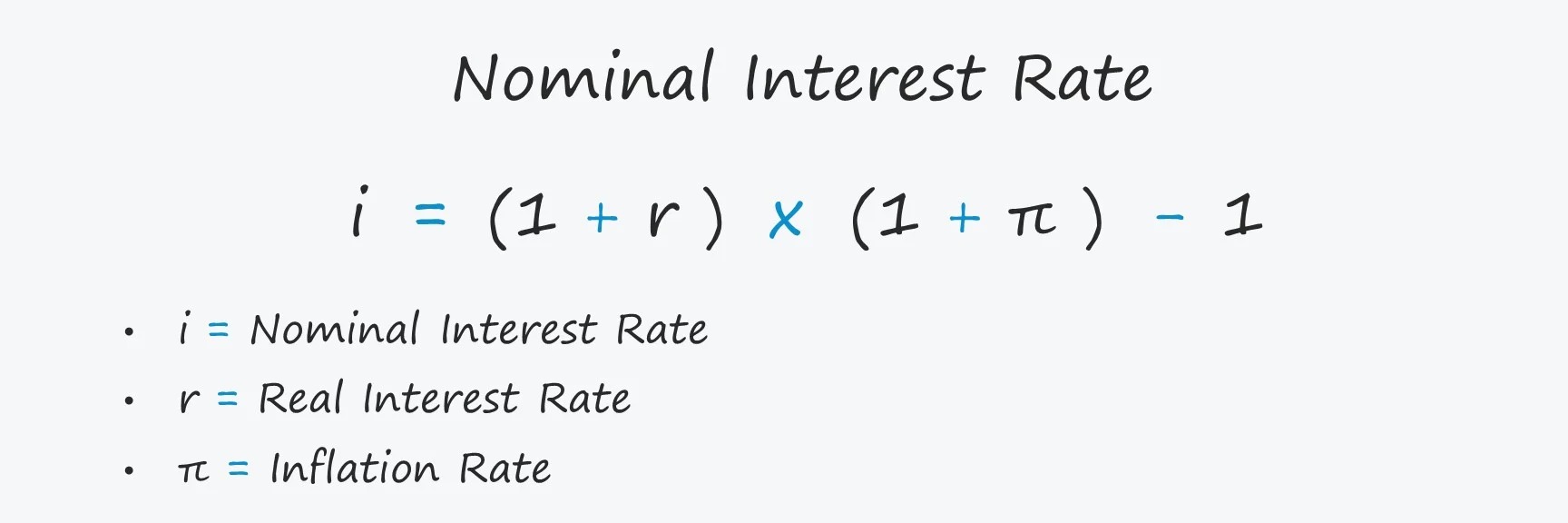

It is important to distinguish between nominal interest rates and real interest rates. Nominal interest rates are the actual rates charged or earned on financial instruments, while real interest rates take into account inflation. Real interest rates provide a more accurate measure of the purchasing power of money and can influence consumer spending and investment decisions.

Another crucial concept related to interest rates is the yield curve. The yield curve represents the relationship between interest rates and the time to maturity of debt securities, typically government bonds. The shape of the yield curve can provide insights into market expectations for future interest rates.

Understanding the key factors that impact interest rates and their implications on various financial instruments and economic sectors is essential for successful interest rate forecasting. By analyzing these factors, economists and financial professionals can develop models and methodologies to anticipate changes in interest rates, providing valuable insights for investors, businesses, and individuals alike.

Factors Affecting Interest Rates

Interest rates are influenced by a wide range of factors that can impact the supply and demand of credit in the financial markets. Understanding these factors is crucial for accurately forecasting interest rates. Here are some of the key factors that play a role in determining interest rates:

- Monetary Policy: Central banks have significant control over short-term interest rates through their monetary policy decisions. By adjusting interest rates, central banks can influence borrowing costs and stimulate or curtail economic activity. Changes in central bank interest rates can have a ripple effect on other market interest rates.

- Inflation Expectations: Inflation erodes the purchasing power of money over time. Lenders demand compensation for the expected loss in value of their money, which leads to higher interest rates. If inflation expectations are high, lenders will require higher interest rates to protect against potential future inflation.

- Economic Growth: The overall state of the economy, including GDP growth, employment levels, and business conditions, can impact interest rates. During periods of robust economic growth, demand for credit tends to be higher, leading to higher interest rates. Conversely, during economic downturns, interest rates tend to decrease to stimulate borrowing and spending.

- Government Fiscal Policy: Government policies, such as taxation, spending, and borrowing, can influence interest rates. Higher government borrowing can put upward pressure on interest rates as the government competes with other borrowers for available funds.

- Global Economic Conditions: Interest rates can be affected by global economic events and trends. Factors such as international trade, geopolitical developments, and global financial stability can impact global interest rates, which, in turn, can influence domestic interest rates.

- Central Bank Communication: The statements and communication from central banks about their future policy intentions can influence market expectations for interest rates. If a central bank signals a potential shift in monetary policy, it can affect interest rate expectations and lead to changes in market interest rates.

- Market Forces: Supply and demand dynamics in the financial markets can have a significant impact on interest rates. Factors such as investor sentiment, liquidity conditions, and risk appetite can drive interest rates higher or lower.

It is important to note that these factors interact with each other and can vary in their influence over time. Additionally, the relative importance of each factor can differ depending on the economic environment and specific circumstances.

By closely monitoring and analyzing these factors, economists and financial professionals can develop models and frameworks to forecast interest rate movements, providing valuable insights for investors, businesses, and individuals to make informed financial decisions.

Economic Indicators for Interest Rate Forecasting

When it comes to forecasting interest rates, economic indicators play a crucial role in providing insights into the current and future state of the economy. These indicators give an indication of the growth trajectory, inflation levels, and overall economic conditions, which can help in predicting changes in interest rates. Here are some key economic indicators that are commonly used for interest rate forecasting:

- Gross Domestic Product (GDP): GDP measures the total value of goods and services produced within a country. When GDP is growing rapidly, it suggests a strong economy and can lead to expectations of higher interest rates. On the other hand, a slowdown in GDP growth may indicate the possibility of lower interest rates.

- Inflation Rate: Inflation is the rate at which prices of goods and services rise over time. Central banks closely monitor inflation and adjust interest rates accordingly. Higher inflation can lead to expectations of higher interest rates as the central bank aims to control price stability. Conversely, low inflation or deflationary pressures may lead to expectations of lower interest rates.

- Employment Data: Employment data, such as non-farm payrolls, unemployment rates, and wage growth, provide insights into the labor market and overall economic health. A strong job market and rising wages may signal potential inflationary pressures and expectations of higher interest rates.

- Consumer Price Index (CPI): The CPI measures the change in prices of a basket of goods and services purchased by consumers. It is a widely used indicator to track inflationary trends. Higher CPI readings may suggest potential inflationary pressures and the possibility of higher interest rates.

- Producer Price Index (PPI): The PPI measures the change in prices at the producer level. It provides insights into inflationary pressures in the early stages of the supply chain. Changes in PPI can influence expectations for future consumer price inflation and interest rates.

- Consumer Confidence Index: Consumer confidence reflects the sentiment and outlook of consumers towards the economy. Higher consumer confidence may lead to increased consumer spending and economic growth, which can potentially result in expectations of higher interest rates.

- Business Investment: Data on business investment, such as capital expenditure and corporate profits, can provide insights into the overall business climate. Strong business investment indicates confidence in the economy and may lead to expectations of higher interest rates.

- Central Bank Communication: The statements and press conferences of central bank officials can provide hints about their future policy actions. Any signals of potential changes in interest rates by central banks can significantly influence market expectations and interest rate forecasts.

- Trade and Retail Data: Trade data, such as import/export figures, and retail sales data can offer insights into the strength of domestic and international demand. Strong trade and retail data may suggest a robust economy, which can lead to expectations of higher interest rates.

While these economic indicators provide valuable insights into the economy, it is important to note that they should be analyzed in conjunction with other factors and in the context of the specific economic environment. Additionally, the timing and magnitude of interest rate changes may also depend on the central bank’s policy stance, which can be influenced by a variety of factors.

By closely monitoring and analyzing these economic indicators, economists and market participants can form more accurate forecasts of future interest rate movements, enabling individuals, businesses, and investors to make informed financial decisions.

Analyzing Historical Interest Rate Data

One valuable tool for interest rate forecasting is the analysis of historical interest rate data. By examining past interest rate trends and patterns, analysts can gain insights into potential future movements. Here are some key considerations when analyzing historical interest rate data:

- Long-Term Trends: Examining long-term historical interest rate trends can provide a broader perspective on interest rate cycles. It allows analysts to identify patterns and cycles that may repeat in the future. For example, periods of economic expansion are often accompanied by higher interest rates, while periods of economic contraction may see lower interest rates.

- Volatility and Seasonality: Historical interest rate data can reveal periods of high volatility or seasonality in interest rate movements. Certain times of the year or economic cycles may exhibit consistent patterns of rate increases or decreases. Identifying such patterns can help forecasters understand the potential timing of future interest rate changes.

- Correlations with Economic Factors: Historical interest rate data can be analyzed in relation to various economic factors, such as GDP growth, inflation rates, or employment data, to identify correlations and potential cause-and-effect relationships. This analysis can provide insights into the factors that may drive interest rate movements and guide future forecasts.

- Policy Shifts: Historical interest rate data can shed light on the impact of policy shifts by central banks. By examining how interest rates have responded to previous monetary policy changes, analysts can gauge potential reactions in future rate changes. Understanding the relationship between central bank actions and interest rates is essential for accurate forecasting.

- Interest Rate Spreads: Analyzing historical data on interest rate spreads, such as the difference between short-term and long-term rates or between corporate and government bond yields, can provide insights into market expectations and potential shifts in interest rates. Widening or narrowing spreads can be indicative of changing economic conditions and can help in forecasting future rate movements.

- External Events: Historical interest rate data can also reveal the impact of major external events, such as financial crises or geopolitical events, on interest rate movements. Analyzing how interest rates have responded in the past can help forecasters anticipate potential reactions to similar events in the future.

- Statistical Analysis: In addition to qualitative analysis, statistical techniques can be applied to historical interest rate data to identify patterns, trends, and statistical relationships. Regression analysis, time series analysis, and other statistical models can help forecasters make more accurate predictions based on historical data.

While historical data analysis is informative, it is important to consider that the future may deviate from historical patterns due to changing economic, financial, or policy conditions. Therefore, it is essential to combine historical analysis with other forecasting methods to strengthen the accuracy of interest rate predictions.

By carefully analyzing historical interest rate data and combining it with other forecasting techniques, analysts can gain valuable insights into potential future interest rate movements, allowing individuals, businesses, and investors to make more informed financial decisions.

Using Yield Curve to Forecast Interest Rates

The yield curve is a graphical representation of the relationship between interest rates and the time to maturity of debt securities, typically government bonds. It is a powerful tool that can be used to forecast interest rates and provide insights into the market’s expectations for future economic conditions. Here’s how the yield curve can be used for interest rate forecasting:

Shape of the Yield Curve: The shape of the yield curve is an important indicator of market expectations for interest rates. There are three primary shapes of the yield curve:

- Normal Curve: A normal yield curve is upward-sloping, with longer-term bonds offering higher yields compared to shorter-term bonds. This shape typically indicates expectations of future economic growth and higher interest rates. However, it is essential to analyze other factors to validate these expectations.

- Flat Curve: A flat yield curve occurs when the yields on bonds with different maturities are relatively similar. This shape can indicate uncertainty or a balanced view on future economic conditions. It may suggest expectations of stable interest rates but lacks strong predictive power on its own.

- Inverted Curve: An inverted yield curve is downward-sloping, with longer-term bonds offering lower yields than shorter-term bonds. This shape is often seen as a warning sign of an impending economic downturn. It may suggest expectations of future interest rate cuts as investors seek the safety of longer-term bonds.

Steepness of the Yard Curve: Apart from the shape, the steepness of the yield curve can also provide insights into future interest rate movements. A steep yield curve indicates a large difference between short-term and long-term yields, which may suggest expectations of future interest rate increases. Conversely, a flat or narrow yield curve suggests minimal differences between short-term and long-term yields and may indicate expectations of stable or lower interest rates.

Yield Spread Analysis: Analyzing the difference, or spread, between yields on different points along the yield curve can provide further insights. Certain spreads, such as the difference between the 2-year and 10-year yields, are closely watched by market participants. Changes in these spreads can indicate shifts in market expectations for interest rates. For example, a narrowing spread may signal a potential economic slowdown and expectations of lower interest rates.

Forward Rate Estimation: Using the yield curve, it is also possible to estimate forward rates, which are implied future interest rates. By calculating the difference between yields on bonds with different maturities, forward rates can be derived. These forward rates provide an indication of market expectations for future interest rates at specific points in time.

While the yield curve can provide valuable insights into interest rate expectations, it is important to note that it is not infallible and should be used in conjunction with other forecasting techniques. Factors such as central bank policies, economic data, and market sentiment should also be considered to validate or challenge the signals provided by the yield curve.

By closely monitoring and analyzing the shape, steepness, and spreads of the yield curve, analysts can gain valuable insights into the market’s expectations for future interest rates. This information can guide individuals, businesses, and investors in making informed decisions about borrowing, lending, and investment strategies.

Forward Rate Agreements and Interest Rate Futures

Forward rate agreements (FRAs) and interest rate futures are financial instruments that allow market participants to hedge against or speculate on future interest rate movements. These instruments are widely used by investors, financial institutions, and corporations to manage interest rate risks and make informed financial decisions. Here’s how FRAs and interest rate futures can be utilized for interest rate forecasting:

Forward Rate Agreements (FRAs): FRAs are contracts between two parties to exchange fixed interest rate payments based on a specified notional amount and a predetermined future period. These agreements provide a means to “lock in” a future interest rate, allowing parties to hedge against potential interest rate fluctuations. By entering into an FRA, participants can make predictions about future interest rates and protect themselves from unexpected rate movements.

For interest rate forecasting, analysts can utilize the pricing and trading of FRAs to gather market expectations for future interest rates. The rates at which FRAs are traded reflect market participants’ predictions about future interest rates. By analyzing FRA prices and trading volumes, analysts can gather insights into market sentiment and expectations, which can be used for interest rate forecasting.

Interest Rate Futures: Interest rate futures are standardized contracts traded on futures exchanges. These contracts represent an agreement to buy or sell a financial instrument (typically a bond or a note) at a predetermined future date and at a specified price. Interest rate futures allow market participants to speculate on or hedge against future interest rate movements.

Interest rate futures can serve as a valuable tool for interest rate forecasting. By observing the prices and trading volumes of interest rate futures contracts, analysts can gain insights into market expectations for future interest rates. Increased activity and higher prices for contracts with longer maturities may indicate expectations of higher interest rates, while decreased activity and lower prices may suggest expectations of lower rates.

In addition to providing insights into interest rate expectations, interest rate futures also offer opportunities for market participants to actively manage their interest rate exposure and implement hedging strategies. By taking positions in interest rate futures contracts, participants can protect against adverse interest rate movements and manage their interest rate risk effectively.

It is important to note that while FRAs and interest rate futures provide valuable information for interest rate forecasting, these instruments are influenced by a range of factors beyond market expectations, such as liquidity, supply and demand dynamics, and regulatory changes. Therefore, it is essential to consider these factors in conjunction with other forecasting techniques to make more accurate predictions regarding future interest rate movements.

By monitoring and analyzing FRAs and interest rate futures, analysts can gain insights into market expectations and sentiment regarding future interest rate movements. These insights can guide individuals, businesses, and investors in managing their interest rate risk and making informed financial decisions.

Macroeconomic Models for Interest Rate Forecasting

Macroeconomic models are used by economists and analysts to forecast interest rates based on various economic indicators and relationships. These models provide a systematic framework for understanding the dynamics of the economy and making projections about future interest rate movements. Here are some commonly used macroeconomic models for interest rate forecasting:

Monetary Policy Models: These models focus on the relationship between monetary policy actions and interest rates. They analyze factors such as central bank decisions, policy rates, and the central bank’s reaction function to forecast future interest rate changes. By examining how central banks respond to changes in economic indicators, inflation rates, and other factors, these models provide insights into future interest rate adjustments.

Macroeconometric Models: Macroeconometric models utilize statistical techniques to estimate relationships between various economic variables, such as GDP, inflation, employment, and interest rates. These models incorporate historical data to identify patterns and quantify the relationships among different variables. They can be used to simulate different scenarios and project future interest rate movements based on changes in other economic indicators.

Vector Autoregression (VAR) Models: VAR models analyze the interdependencies among different economic variables to make predictions about future interest rates. These models look at the historical relationships between variables and use them to estimate future outcomes. By incorporating multiple economic indicators, VAR models capture the complex interactions in the economy and provide insights into the factors that drive interest rate movements.

Dynamic Stochastic General Equilibrium (DSGE) Models: DSGE models are comprehensive macroeconomic models that incorporate various economic sectors and their interrelations. These models take into account factors such as fiscal policy, monetary policy, inflation dynamics, and technological shocks. They provide a detailed understanding of the economy and allow for forecasting future interest rates based on changes in the underlying structural components of the economy.

Time Series Models: Time series models, such as autoregressive integrated moving average (ARIMA) models and exponential smoothing models, analyze the historical behavior of interest rates to project future trends. These models focus on identifying patterns, trends, and seasonality in the time series data of interest rates. By extrapolating historical patterns, these models can provide short-term and medium-term interest rate forecasts.

While these macroeconomic models provide valuable insights into interest rate forecasting, it is important to consider their limitations. Models rely on assumptions and simplifications of the complex economic reality, and unforeseen events or changes in the economic landscape can challenge the accuracy of their predictions. Therefore, it is crucial to regularly update and calibrate the models with the latest data and incorporate qualitative analysis and judgment to enhance their forecasting ability.

By utilizing macroeconomic models, analysts can gain a deeper understanding of the economic relationships and forecast future interest rate movements. These models provide a systematic and structured approach to interest rate forecasting, supporting individuals, businesses, and policymakers in making informed financial decisions.

Market-Based Approaches for Interest Rate Forecasting

Market-based approaches for interest rate forecasting utilize the information embedded in financial markets to make predictions about future interest rate movements. These approaches rely on the analysis of market prices and investor behavior to extrapolate market expectations for interest rates. Here are some commonly used market-based approaches for interest rate forecasting:

Forward Rate Agreements (FRAs) and Interest Rate Futures: FRAs and interest rate futures contracts provide a direct market-based indication of future interest rate expectations. By examining the pricing and trading activity of these contracts, analysts can gauge market sentiment about future interest rates. Increased buying activity or rising prices for contracts with longer maturities may suggest expectations of higher interest rates, while decreased activity or falling prices may indicate expectations of lower rates.

Bond Yields: Bond yields, particularly those on government bonds or benchmark bonds, are closely monitored by market participants for interest rate forecasting. When bond yields rise, it implies a decrease in bond prices, indicating expectations of higher interest rates in the future. Conversely, declining bond yields suggest expectations of lower rates. Analyzing the yield curve and changes in yields at various maturities can provide insights into market expectations for interest rates.

Option-Implied Volatility: Option markets also offer information about market expectations for future interest rates. By analyzing the implied volatility of interest rate options, analysts can infer the expected magnitude of future interest rate movements. Higher implied volatility suggests increased market uncertainty and potential larger rate fluctuations, while lower implied volatility may indicate expectations of more stable rates.

Interest Rate Swaps: Interest rate swaps involve the exchange of fixed and floating interest rate payments, allowing market participants to manage interest rate risk. The pricing and trading activity of interest rate swap contracts can provide insights into market expectations for future interest rates. Increased demand for fixed-rate swaps may indicate expectations of rising rates, while increased demand for floating-rate swaps may suggest expectations of falling rates.

Market Sentiment and Surveys: Monitoring market sentiment and surveys can also provide valuable information for interest rate forecasting. Surveys of financial market participants or business leaders can capture their expectations for future interest rates. Additionally, sentiment indicators, such as consumer confidence or investor sentiment indices, can provide insights into market expectations and sentiment towards interest rates.

Market-based approaches are powerful as they reflect the collective wisdom and expectations of market participants. However, these approaches have limitations as well. Market sentiment can be influenced by various factors, including short-term market dynamics and investor sentiment biases. Therefore, it is important to interpret market-based signals in conjunction with other forecasting methods and analyze them within the context of the broader economic environment.

By employing market-based approaches, analysts can gain insights into market expectations for future interest rates and incorporate these expectations into their interest rate forecasts. These approaches enhance the ability to make informed financial decisions and effectively manage interest rate risk.

Conclusion

Forecasting interest rates is a critical aspect of financial decision-making and risk management. By accurately predicting interest rate movements, individuals, businesses, and investors can make informed choices regarding borrowing, lending, investment, and financial planning. In this article, we explored various methods and approaches for interest rate forecasting.

We began by understanding the basics of interest rates and the factors that affect them. We then discussed the role of economic indicators in interest rate forecasting, such as GDP, inflation rate, employment data, and consumer confidence. Analyzing historical interest rate data, including long-term trends, volatility, and correlations with economic factors, can provide valuable insights for future interest rate predictions. Furthermore, using the yield curve, forward rate agreements, and interest rate futures can reveal market expectations for future interest rate movements.

We also explored the significance of macroeconomic models in interest rate forecasting. These models incorporate economic relationships, policy actions, and historical data to project future interest rates. Market-based approaches, including analyzing FRAs, interest rate futures, bond yields, and option-implied volatility, provide insights into market sentiment and expectations.

It is important to note that interest rate forecasting is subject to uncertainties and limitations. Economic conditions, policy changes, and unforeseen events can impact interest rates in unexpected ways. Therefore, it is crucial to combine various forecasting methods, validate predictions against economic conditions, and exercise judgment in making financial decisions.

In conclusion, interest rate forecasting plays a vital role in navigating the complex landscape of finance. By utilizing a combination of economic analysis, historical data, macroeconomic models, and market-based approaches, analysts and decision-makers can gain valuable insights into future interest rate movements. These insights enable them to formulate effective strategies, manage interest rate risks, and optimize financial outcomes.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance