Finance

What Are Government Agency Bonds

Published: October 12, 2023

Learn about government agency bonds and how they fit into the world of finance. Understand the benefits and risks associated with these types of investments.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

Introduction

Government agency bonds are a type of investment instrument issued by government-sponsored entities (GSEs) or government-owned corporations. These bonds are considered to be relatively safer investments compared to other types of bonds due to the backing of the issuing government. Government agency bonds provide investors with a fixed income stream over a specific period of time, making them an attractive option for those seeking stable returns.

In the world of finance, government agency bonds play a crucial role in financing various public projects and initiatives. These bonds are often used to raise funds for infrastructure development, affordable housing programs, agricultural projects, and other government-backed endeavors. Unlike government bonds issued directly by the government, agency bonds carry the guarantee of specific agencies or corporations that are established and supervised by the government.

The key distinction between government agency bonds and traditional government bonds lies in the issuer. While government bonds are issued directly by the government, agency bonds are issued by government-sponsored entities or corporations. These entities are tasked with promoting specific sectors of the economy or providing support to particular industries.

Government agency bonds offer investors the opportunity to earn a steady stream of income through interest payments while minimizing the risk associated with volatile market conditions. These bonds are considered to have a lower level of credit risk due to the implied backing of the government. However, it is important to note that government agency bonds are not entirely risk-free, as they still carry a certain level of default risk that varies depending on the issuing agency.

In the following sections, we will delve deeper into the definition, types, features, and risks associated with government agency bonds. We will also explore the pros and cons of investing in these bonds and provide insights on how to invest in government agency bonds effectively. With a comprehensive understanding of government agency bonds, investors can make informed decisions and optimize their investment portfolios.

Definition of Government Agency Bonds

Government agency bonds are debt securities issued by government-sponsored entities (GSEs) or government-owned corporations. These entities are created and authorized by the government to fulfill specific purposes, such as supporting housing markets, financing agricultural projects, or facilitating infrastructure development. They act as intermediaries between investors and the government, raising funds through the issuance of bonds.

The primary function of government agency bonds is to provide a stable and consistent stream of income to investors. These bonds are typically issued for a fixed term, ranging from a few months to several years. During the bond’s tenure, investors receive periodic interest payments based on the coupon rate specified at the time of issuance.

The interest rates on government agency bonds are generally higher than those on government bonds, reflecting the relative credit risk associated with the issuing agency. However, these bonds are considered to be of higher quality and carry lower default risk compared to corporate bonds.

Government agency bonds are backed by the issuing agency’s ability to generate revenue and its implicit guarantee of support from the government. This backing provides investors with a certain level of assurance regarding the timely payment of principal and interest payments.

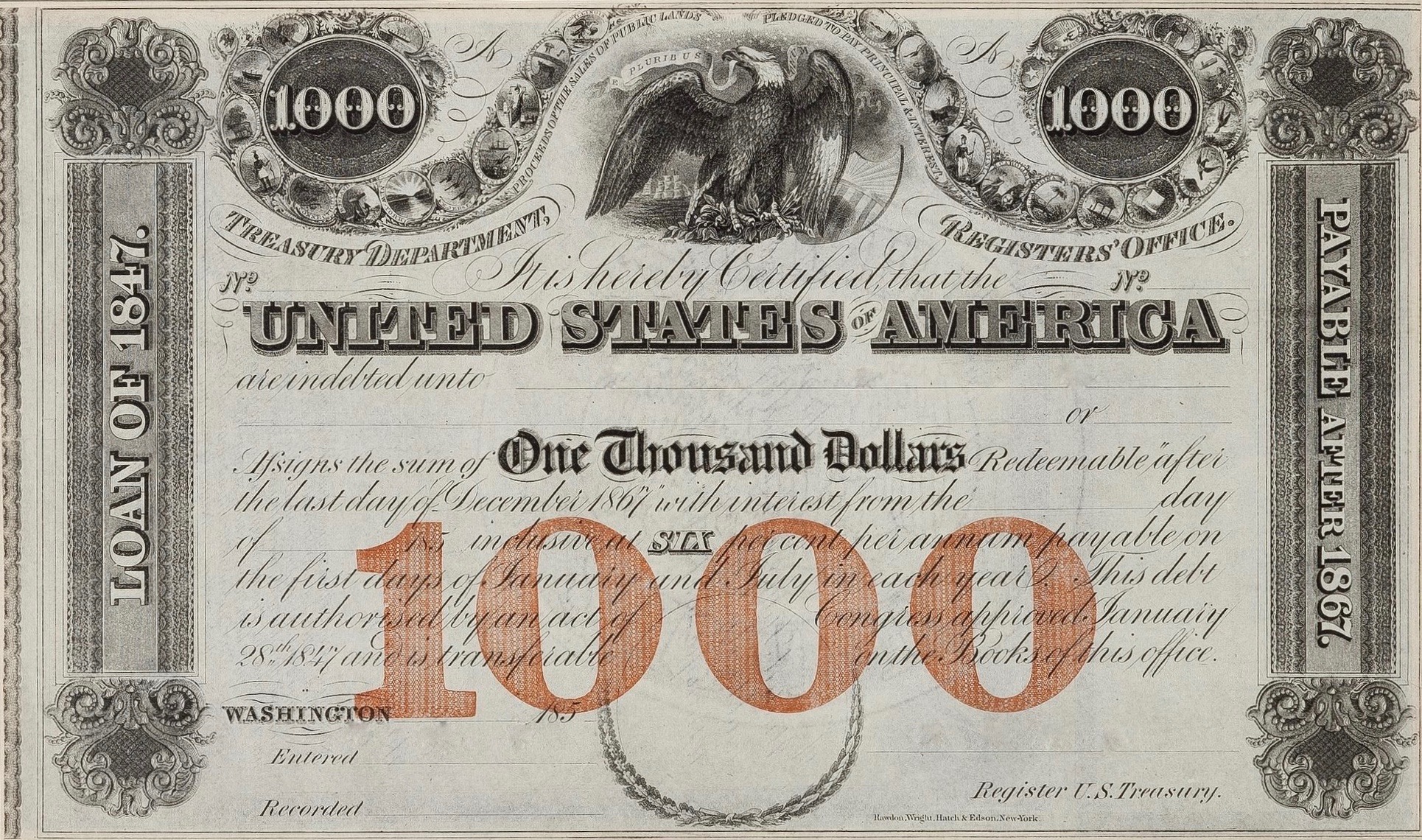

It is important to note that government agency bonds are distinct from Treasury securities issued by the U.S. Department of the Treasury. While both types of bonds are backed by the government, government agency bonds are the obligations of the issuing agency, rather than the U.S. government itself. Therefore, the creditworthiness of government agency bonds is subject to the financial standing and performance of the specific agency.

Examples of government agencies that issue bonds include the Federal National Mortgage Association (Fannie Mae), the Federal Home Loan Mortgage Corporation (Freddie Mac), and the Government National Mortgage Association (Ginnie Mae). These entities primarily focus on supporting the housing market and promoting homeownership by providing liquidity to the mortgage market.

In summary, government agency bonds are debt securities issued by government-sponsored entities or government-owned corporations. They provide investors with a reliable income stream and are backed by the issuing agency’s revenue-generating capacity and implicit support from the government.

Types of Government Agency Bonds

Government agency bonds encompass a variety of bond types issued by different government-sponsored entities or corporations. Each type serves a specific purpose and caters to different investors’ needs and preferences. Here are some common types of government agency bonds:

- Federal agency bonds: These bonds are issued by federal agencies, such as the Small Business Administration (SBA) or the Farm Credit System (FCS). Federal agency bonds are typically used to finance specific sectors of the economy, such as small businesses or agricultural projects. They offer competitive interest rates and can be an attractive option for investors interested in supporting these sectors.

- Government National Mortgage Association (Ginnie Mae) bonds: Ginnie Mae bonds are issued by the Government National Mortgage Association, a government agency focused on promoting affordable housing. These bonds are backed by mortgages insured or guaranteed by federal agencies, such as the Federal Housing Administration (FHA) or the Department of Veterans Affairs (VA). Ginnie Mae bonds provide investors with exposure to the mortgage market and can offer attractive yields.

- Federal Home Loan Bank (FHLB) bonds: FHLB bonds are issued by the Federal Home Loan Banks, a group of 11 regional banks established to support the lending activities of member institutions, such as commercial banks and credit unions. These bonds are backed by the collateral provided by member institutions, such as mortgage loans. FHLB bonds offer competitive interest rates and are considered relatively low risk due to the collateralized nature of the underlying assets.

- Federal Farm Credit System (FFCS) bonds: FFCS bonds are issued by the Farm Credit System, a network of borrower-owned lending institutions that provide credit and financial services to farmers, ranchers, and other agricultural entities. These bonds help finance agricultural projects and offer investors exposure to the agricultural sector. FFCS bonds typically come with attractive interest rates and are considered relatively safe investments.

- Federal National Mortgage Association (Fannie Mae) bonds: Fannie Mae bonds are issued by the Federal National Mortgage Association, a government-sponsored enterprise that facilitates liquidity in the mortgage market. Fannie Mae bonds are backed by a portfolio of mortgage loans and offer investors exposure to the housing market. These bonds are considered to be relatively safe investments with competitive yields.

- Federal Home Loan Mortgage Corporation (Freddie Mac) bonds: Freddie Mac bonds are issued by the Federal Home Loan Mortgage Corporation, another government-sponsored enterprise that supports the mortgage market. These bonds are backed by a portfolio of residential mortgage loans and provide investors with exposure to the housing market. Freddie Mac bonds are considered to be relatively safe investments with competitive yields.

These are just a few examples of government agency bonds. There are various other types issued by different agencies to support specific sectors or initiatives. It is important for investors to research and understand the specific characteristics and risks associated with each type of government agency bond before making investment decisions.

Features and Characteristics of Government Agency Bonds

Government agency bonds have distinct features and characteristics that set them apart from other types of bonds. Understanding these characteristics can help investors make informed decisions when considering investments in government agency bonds. Here are some key features and characteristics of government agency bonds:

- Backed by the issuing agency: Government agency bonds are backed by the issuing agency’s ability to generate revenue and its implicit support from the government. This backing provides investors with a level of assurance regarding the timely payment of principal and interest.

- Fixed income: Government agency bonds provide investors with a fixed income stream over a specific period of time. The interest payments, called coupon payments, are made at regular intervals, such as semi-annually or annually, based on the coupon rate specified at the time of issuance.

- Varying maturities: Government agency bonds are issued with various maturities, ranging from short-term bonds with maturities of a few months to long-term bonds with maturities of several years. Investors can choose bonds that align with their investment objectives and time horizons.

- Diverse risk profiles: Although government agency bonds are generally considered to have a lower level of credit risk compared to corporate bonds, the risk profile may vary among different agencies. It is essential for investors to assess the financial standing and creditworthiness of the specific agency before investing.

- Liquidity: Government agency bonds are typically traded in active secondary markets, providing investors with liquidity and the ability to buy or sell their bonds before maturity. This liquidity allows investors to adjust their portfolios to changing market conditions or avail themselves of investment opportunities.

- Tax implications: The interest income received from government agency bonds may be subject to federal, state, and local taxes. However, certain agency bonds, such as those issued by Ginnie Mae, are guaranteed by the U.S. government and are generally exempt from state and local taxes.

It is important to note that the specific terms and conditions of government agency bonds may vary depending on the issuing agency. Investors should carefully review the bond prospectus or offering statement to understand the exact features, such as call provisions, redemption options, and any special considerations.

Overall, government agency bonds offer investors a reliable source of fixed income and the potential for capital preservation. Their backing by government entities and diverse range of offerings make them appealing to a wide range of investors. However, it is crucial for investors to conduct thorough research, assess the risks involved, and diversify their portfolios to effectively navigate the world of government agency bonds.

Pros and Cons of Investing in Government Agency Bonds

Investing in government agency bonds offers a range of advantages and disadvantages that investors should consider before making investment decisions. Here are the pros and cons of investing in government agency bonds:

Pros:

- Relatively lower risk: Government agency bonds are considered to have lower credit risk compared to corporate bonds. The backing of the issuing agency and, in some cases, implicit support from the government provide investors with a level of assurance regarding the timely payment of principal and interest.

- Steady income stream: Government agency bonds offer a fixed income stream with regular interest payments. This can be appealing for investors seeking stable and predictable cash flows.

- Liquidity: Government agency bonds are generally traded in active secondary markets, providing investors with liquidity and the ability to buy or sell their bonds when needed. This flexibility allows investors to adjust their portfolios or take advantage of other investment opportunities.

- Tax advantages: Some government agency bonds, such as those issued by Ginnie Mae, may be exempt from state and local taxes, providing potential tax advantages for investors. This can enhance the after-tax returns on investments.

- Diversification: Government agency bonds offer investors the opportunity to diversify their investment portfolios. Including these bonds in a well-diversified portfolio can help mitigate risk and provide stability during market fluctuations.

Cons:

- Lower yields: Government agency bonds generally offer lower yields compared to riskier fixed-income investments, such as corporate bonds or high-yield bonds. However, the trade-off is the relative safety and stability provided by government agency bonds.

- Interest rate risk: Like other fixed-income securities, government agency bonds are susceptible to fluctuations in interest rates. When interest rates rise, bond prices tend to fall, potentially resulting in capital losses for investors selling their bonds before maturity.

- Prepayment risk: Some government agency bonds, such as mortgage-backed securities, may have prepayment risk. This means that if borrowers pay off their loans earlier than expected, investors may receive their principal back sooner than anticipated. This can impact the overall yield and duration of the bond.

- Issuer-specific risks: While government agency bonds enjoy the backing of the issuing agency, the creditworthiness of the specific agency may vary. Investors should carefully assess the financial stability and performance of the issuing agency before investing in its bonds.

It is important for investors to weigh these pros and cons based on their individual investment goals, risk tolerance, and overall portfolio strategy. Government agency bonds can be an excellent addition to an investment portfolio, providing stability, income, and the potential for capital preservation. However, investors should consider their own financial circumstances and consult with a financial advisor to determine the suitability of government agency bonds within their overall investment strategy.

Risks Associated with Government Agency Bonds

While government agency bonds are generally considered to be relatively low-risk investments, they still carry certain risks that investors should be aware of. Understanding these risks is crucial in making informed investment decisions. Here are some of the key risks associated with government agency bonds:

- Interest Rate Risk: Government agency bonds are sensitive to changes in interest rates. When interest rates rise, the value of existing bonds tends to decline, potentially resulting in capital losses for investors who sell their bonds before maturity. Conversely, when interest rates fall, bond prices tend to rise.

- Credit Risk: While government agency bonds are generally considered to have lower credit risk compared to corporate bonds, there is still a degree of credit risk involved. The creditworthiness of the issuing agency may vary, and there is always a possibility of default or delayed payments. Investors should assess the financial stability and performance of the specific agency before investing in its bonds.

- Prepayment Risk: Some government agency bonds, such as mortgage-backed securities, are subject to prepayment risk. This means that if borrowers pay off their loans earlier than expected, investors may receive their principal back sooner than anticipated. This can impact the overall yield and duration of the bond.

- Market and Liquidity Risk: The secondary market for government agency bonds may experience periods of illiquidity or volatility. An illiquid market can make it difficult for investors to buy or sell bonds at desired prices, potentially resulting in higher transaction costs or the inability to execute trades at all.

- Political and Regulatory Risk: Changes in government policies, regulations, or legislation can impact the performance and value of government agency bonds. Political and regulatory risks can arise if there are shifts in government priorities, changes in regulations governing the functions of government-sponsored entities, or alterations in the legal framework that governs these bonds.

- Inflation Risk: Inflation erodes the purchasing power of fixed income investments over time. While government agency bonds provide periodic interest payments, the real return (adjusted for inflation) may be reduced if inflation exceeds the coupon rate.

It’s important for investors to assess their risk tolerance and understand the potential risks associated with government agency bonds. Diversification, thorough research, and careful consideration of the specific agency’s financial health can help mitigate some of these risks. Additionally, consulting with a financial advisor can provide valuable guidance in managing risk and constructing a well-balanced investment portfolio.

How to Invest in Government Agency Bonds

Investing in government agency bonds can be a suitable option for investors looking for stable returns and lower risk. Here are some steps to consider when investing in government agency bonds:

- Educate Yourself: Start by gaining a thorough understanding of government agency bonds, their features, and the specific agencies that issue them. Research the different types of government agency bonds available and familiarize yourself with their risks and benefits.

- Assess your Investment Goals and Risk Tolerance: Determine your investment objectives and assess your risk tolerance. Consider how government agency bonds fit within your overall investment strategy and the role they will play in your portfolio. This will help you determine the appropriate allocation to government agency bonds.

- Research Agencies and Credit Ratings: Evaluate the creditworthiness and financial stability of the specific government agency whose bonds you are considering. Review credit ratings assigned by reputable rating agencies to understand the agency’s creditworthiness and default risk. Higher credit ratings generally indicate lower risk.

- Select the Type and Maturity: Decide which type of government agency bond suits your investment goals and time horizon. Consider factors such as the bond’s maturity, coupon rate, and yield. Shorter-term bonds may be suitable for investors who prefer more immediate returns, while longer-term bonds offer potentially higher yields.

- Open an Investment Account: To invest in government agency bonds, you will need to open an investment account with a brokerage firm or a financial institution that offers bond trading services. Ensure that the chosen platform provides access to government agency bonds and offers competitive pricing and a user-friendly interface.

- Place an Order: Once you have chosen the agency and type of government agency bond you wish to invest in, place an order through your investment account. Specify the quantity, desired price, and indicate whether you want to purchase the bonds in the primary market (at the time of issuance) or in the secondary market (after they have been issued).

- Monitor and Manage your Investments: Keep track of your government agency bond investments and monitor any changes in interest rates, market conditions, or the financial health of the issuing agency. Regularly review your investment portfolio and make necessary adjustments to ensure it remains aligned with your financial goals.

It is important to note that investing in government agency bonds involves risks, and past performance is not indicative of future results. Consider working with a financial advisor who can provide personalized advice and tailored recommendations based on your individual financial situation and goals.

Conclusion

Government agency bonds offer investors a unique opportunity to earn stable income while preserving capital. These bonds are backed by government-sponsored entities or government-owned corporations, providing a level of assurance regarding payment of principal and interest. While they carry certain risks, such as interest rate risk and credit risk, government agency bonds are generally considered lower risk compared to corporate bonds.

Investing in government agency bonds can be suitable for investors seeking steady income, diversification, and a relative level of safety. These bonds offer benefits such as fixed income, liquidity, and potential tax advantages. They can be purchased through brokerage firms or financial institutions that offer bond trading services.

However, it is essential for investors to conduct research, evaluate the creditworthiness of the issuing agency, and align their investment goals and risk tolerance before investing. This will help ensure that government agency bonds are a suitable fit for their portfolios.

Overall, government agency bonds can serve as a reliable component of a well-diversified investment portfolio. They can provide stability, consistent income, and the potential to preserve capital. By understanding the features, risks, and types of government agency bonds, investors can make informed decisions and optimize their investment strategies.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance