Home>Finance>What Happens If You Cancel A Whole Life Insurance Plan?

Finance

What Happens If You Cancel A Whole Life Insurance Plan?

Published: October 15, 2023

Discover the financial implications of canceling a whole life insurance plan. Learn about potential penalties, surrender values, and alternatives to consider.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

- Introduction

- Understanding Whole Life Insurance Plans

- Reasons for Canceling a Whole Life Insurance Plan

- Consequences of Canceling a Whole Life Insurance Plan

- Cash Surrender Value and Policy Options

- Tax Implications of Canceling a Whole Life Insurance Plan

- Considerations Before Cancelling a Whole Life Insurance Plan

- Alternatives to Canceling a Whole Life Insurance Plan

- Conclusion

Introduction

Welcome to the world of whole life insurance plans! If you’re considering canceling your whole life insurance policy, it’s important to understand the potential consequences and explore your options. Canceling a whole life insurance plan is a significant decision that can have various financial implications.

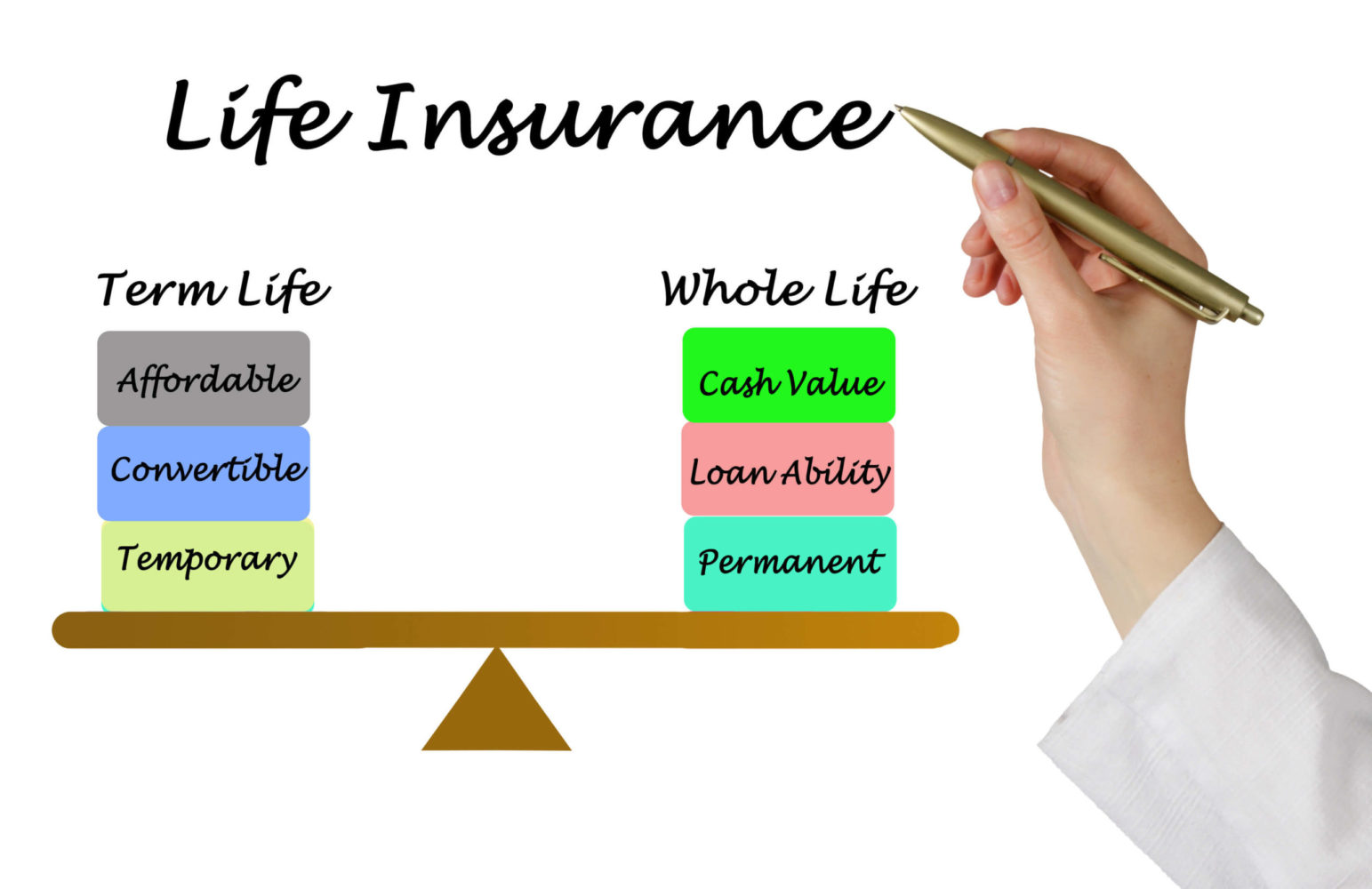

Whole life insurance is a type of permanent life insurance that provides coverage for the entire lifetime of the insured individual. Unlike term life insurance, which provides coverage for a specific period, whole life insurance offers lifelong protection. It combines a death benefit with a cash value component that accumulates over time. The cash value grows tax-deferred and can be accessed through policy loans or withdrawals.

However, life is full of unexpected twists and turns, and your financial circumstances may change. You might find yourself in a situation where canceling your whole life insurance plan is a consideration. It could be due to financial constraints, a shift in your insurance needs, or simply because you no longer wish to maintain the policy. Whatever the reason, it’s crucial to fully comprehend both the benefits and consequences of canceling your whole life insurance plan.

In this article, we’ll delve into the reasons why individuals decide to cancel their whole life insurance policies, the potential implications of doing so, and alternative options to consider. By understanding these aspects, you’ll have the knowledge to make an informed decision regarding your whole life insurance plan.

Understanding Whole Life Insurance Plans

Before we dive into the details of canceling a whole life insurance plan, let’s first establish a clear understanding of what a whole life insurance policy entails. Whole life insurance is a type of permanent life insurance that provides coverage for the entire lifetime of the insured individual.

Unlike term life insurance, which lasts for a specific term such as 10, 20, or 30 years, whole life insurance offers lifelong protection. The policy pays out a death benefit to the beneficiaries upon the insured’s passing, as long as the premiums are paid.

What sets whole life insurance apart from other types of life insurance is the cash value component. A portion of the premiums you pay is invested by the insurance company, and over time, this cash value grows tax-deferred. The cash value accumulates based on the policy’s dividend earnings, which can help offset the policy’s premiums or be accessed by the policy owner.

One of the primary benefits of whole life insurance is that the premiums remain level for the duration of the policy. This means that the amount you pay for the coverage remains the same, regardless of changes in your health or age.

Additionally, whole life insurance offers a guaranteed death benefit, ensuring that your loved ones will receive a predetermined sum upon your passing. This provides peace of mind and financial security for your family in the event of your death.

Another advantage of whole life insurance is the potential to earn dividends. Dividends are not guaranteed, but if the insurance company performs well, it may distribute a portion of its profits to policyholders. Policyholders can choose to reinvest the dividends, use them to reduce premiums, or receive a cash payment.

It’s important to note that whole life insurance tends to have higher premiums compared to term life insurance. This is because part of the premium goes towards the cash value accumulation and the guarantee of lifelong coverage.

Now that we have a basic understanding of what whole life insurance is, let’s explore the reasons why individuals may choose to cancel their whole life insurance plans.

Reasons for Canceling a Whole Life Insurance Plan

While whole life insurance offers lifelong coverage and the potential to accumulate cash value, there are several reasons why individuals may decide to cancel their policies.

1. Financial Constraints: One common reason for canceling a whole life insurance plan is financial difficulty. If you are facing a challenging financial situation, you may need to prioritize immediate expenses over the cost of maintaining your life insurance coverage. This can be particularly true if you are struggling to pay the premiums and need to free up funds for essential needs.

2. Changing Insurance Needs: Your insurance needs may change over time. For example, if your children have grown up and are financially independent, you may no longer require the same level of life insurance coverage. In such cases, canceling your whole life insurance plan may make sense to avoid unnecessary expenses.

3. Better Investment Opportunities: Some individuals may consider canceling their whole life insurance policies when they believe they can obtain better returns by investing the premium payments elsewhere. While whole life insurance offers the advantage of tax-deferred cash value growth, it may not always offer the same potential for high returns as other investment options.

4. Dissatisfaction with the Policy: If you are unsatisfied with the performance or features of your whole life insurance policy, you might consider canceling it. This could be due to issues such as high premiums, low cash value growth, or dissatisfaction with the customer service provided by the insurance company.

5. Estate Planning Changes: Changes in your estate planning goals or strategies may also prompt you to cancel your whole life insurance policy. For example, if you have established trusts or other mechanisms to provide for your beneficiaries, you may find that the policy is no longer necessary.

While these are some common reasons for canceling a whole life insurance plan, it’s essential to carefully evaluate your individual circumstances and consult with a financial advisor or insurance professional before making a decision. Canceling a whole life insurance policy can have significant financial implications, which we will explore in the next section.

Consequences of Canceling a Whole Life Insurance Plan

Canceling a whole life insurance plan can have several consequences, both immediate and long-term. It’s crucial to understand these implications before making a decision.

1. Loss of Coverage: The most apparent consequence of canceling a whole life insurance plan is the loss of life insurance coverage. Once the policy is canceled, your beneficiaries will no longer receive a death benefit upon your passing. This can leave your loved ones financially vulnerable in the event of your unexpected death.

2. Surrender Charges: Whole life insurance policies often have surrender charges, especially during the early years of the policy. Surrender charges are fees imposed by the insurance company to compensate for the expenses incurred when setting up the policy. These charges can significantly reduce the cash value you receive if you decide to surrender the policy.

3. Loss of Cash Value: By canceling your whole life insurance plan, you also forfeit the accumulated cash value. The cash value represents the amount of money that has grown over time through premium payments and investment returns. Depending on the length of time you’ve had the policy, the cash value can be a substantial asset that you lose access to when canceling the policy.

4. Tax Implications: Canceling a whole life insurance policy can have tax implications. Any cash value growth that you’ve accumulated and receive as a surrender payment may be subject to income tax. It’s essential to consult with a tax advisor to understand the potential tax consequences of canceling your policy.

5. Limited Future Coverage Options: If you cancel your whole life insurance plan and later realize that you still require coverage, obtaining new life insurance may be more challenging and expensive. Age and health changes can affect your insurability, making it more difficult to secure a new policy or leading to higher premiums.

It’s important to carefully weigh these consequences against your current financial situation and future needs before canceling a whole life insurance plan. Consider consulting with a financial advisor or insurance professional who can provide guidance tailored to your specific circumstances.

Next, let’s explore the concept of cash surrender value and the options available if you decide to proceed with canceling your whole life insurance plan.

Cash Surrender Value and Policy Options

When considering canceling a whole life insurance plan, it’s crucial to understand the concept of cash surrender value and explore the available options.

The cash surrender value is the amount of money you can receive if you choose to surrender your whole life insurance policy. It represents the accumulated cash value minus any surrender charges imposed by the insurance company. The cash surrender value is typically lower than the total cash value of the policy due to these charges.

Once you decide to surrender your policy, you have a couple of options in terms of receiving the cash surrender value:

1. Lump Sum Payment: You can choose to receive the cash surrender value as a lump sum payment. This provides you with immediate access to the accumulated cash value but also means that you lose the life insurance coverage and potential future growth of the policy.

2. Policy Loans: Instead of canceling the policy and receiving a lump sum payment, you may have the option to take out a policy loan against the cash value of the policy. Policy loans allow you to borrow a portion of the cash value while keeping the policy active. However, it’s important to note that policy loans accrue interest and must be repaid. Failure to repay the loan can result in a reduced death benefit.

3. Reduced Paid-Up Insurance: If you no longer wish to pay premiums but still want to retain some life insurance coverage, you may have the option to convert your whole life insurance policy into a reduced paid-up policy. This means that you stop making premium payments, and the cash value is used to provide a smaller death benefit for the remainder of your lifetime.

It’s crucial to carefully evaluate these options and their potential impact on your financial situation. Consider consulting with a financial advisor or insurance professional who can help you navigate the decision-making process and provide insight into the best course of action based on your specific needs and goals.

Next, let’s discuss the tax implications of canceling a whole life insurance plan.

Tax Implications of Canceling a Whole Life Insurance Plan

Canceling a whole life insurance plan can have tax implications that you need to be aware of. It’s important to understand these potential tax consequences before making a decision.

1. Income Tax on Surrender Value: If you decide to cancel your whole life insurance policy and receive the cash surrender value, any gain on the cash value may be subject to income tax. The gain is calculated by subtracting the total premium payments you made from the cash surrender value. This gain is considered taxable income in the year of surrender.

2. Tax-Free Dividends: Prior to canceling the policy, you may have received dividends from the insurance company. Dividends are typically treated as a return of premium and are not subject to income tax. However, if you surrender the policy and receive the cash value, any dividends included in the cash surrender value may be subject to income tax.

3. Estate Tax Considerations: Another aspect to consider is the potential impact of canceling a whole life insurance policy on your estate taxes. Life insurance death benefits are generally paid out tax-free to the beneficiaries. By canceling the policy, you may be reducing the size of your estate and the potential estate tax liability.

It’s important to consult with a tax advisor or financial professional who can provide personalized advice based on your specific situation. They can help you understand the potential tax implications of canceling your whole life insurance plan and guide you in making the most tax-efficient decision.

Before making any final decisions, let’s discuss some important considerations that you should keep in mind.

Considerations Before Cancelling a Whole Life Insurance Plan

Before making the decision to cancel a whole life insurance plan, it’s essential to carefully consider several factors and evaluate your unique circumstances. Here are some key considerations to keep in mind:

1. Insurance Needs: Assess your current and future insurance needs. Think about whether you still require life insurance coverage to protect your loved ones financially. Consider factors such as outstanding debts, dependent family members, and any financial obligations you may have.

2. Potential Future Needs: Anticipate any potential future needs for life insurance coverage. Even if your current needs have changed, think about whether you might require coverage later on. It could be for purposes such as estate planning, leaving a legacy, or providing for your family’s future needs.

3. Alternative Coverage Options: Investigate alternative coverage options before canceling your whole life insurance plan. These options may include term life insurance or other types of permanent life insurance policies that better align with your current needs and budget.

4. Financial Impact: Consider the financial impact of canceling the policy. Evaluate the surrender value, surrender charges, and potential tax implications. Think about how canceling the policy will affect your overall financial plan and long-term goals.

5. Consult with Professionals: Seek guidance from financial advisors, insurance professionals, and tax advisors who can provide expert advice tailored to your specific situation. They can help you understand the implications, explore alternative options, and make an informed decision.

6. Evaluate Other Uses of Cash Value: Assess if there are alternative uses for the cash value of your whole life insurance policy. The cash value could serve as a source of emergency funds or a potential investment opportunity that aligns better with your financial goals.

By carefully considering these factors, you can make an informed decision about whether canceling your whole life insurance plan is the right choice for you. Remember, the decision should be based on your individual circumstances and long-term financial objectives.

Now, let’s explore some alternative options to canceling a whole life insurance plan.

Alternatives to Canceling a Whole Life Insurance Plan

If you’re considering canceling your whole life insurance plan but would like to explore alternative options, there are several alternatives to consider. These alternatives can help you maintain some form of coverage or maximize the value of your policy. Here are a few options worth exploring:

1. Paid-Up Additions: Instead of canceling your whole life insurance policy, you may have the option to use the accumulated cash value to purchase paid-up additions. Paid-up additions are additional coverage units that can increase the death benefit of your policy without requiring additional premium payments. This can help you maintain some level of coverage while utilizing the cash value that has already accumulated.

2. Reduced Paid-Up Insurance: If you no longer wish to pay premiums but still want to retain some life insurance coverage, you may have the option to convert your whole life insurance policy into a reduced paid-up policy. This means that you stop making premium payments, and the cash value is used to provide a smaller death benefit for the remainder of your lifetime.

3. Policy Loans: Instead of canceling the policy and forfeiting the cash value, you may have the option to take out a policy loan against the cash value. This allows you to tap into the accumulated cash value while keeping the policy in force. Keep in mind that policy loans accrue interest and must be repaid, and failure to repay the loan can reduce the death benefit.

4. Policy Surrender for Reduced Cash Value: If you need immediate cash but still want to maintain some coverage, consider surrendering a portion of your policy. This option allows you to receive a reduced cash value while keeping a portion of your original coverage intact.

5. Policy Exchange: Depending on your specific circumstances and needs, you may consider exchanging your whole life insurance policy for a different type of policy, such as a term life insurance policy. This can help reduce premium costs while still providing the necessary coverage for a specified term.

It’s important to carefully evaluate these alternatives and compare them to the potential consequences of canceling your whole life insurance plan. Consider consulting with a financial advisor or insurance professional who can provide personalized advice and guide you in exploring the most suitable option for your specific situation.

Remember, each alternative has its own advantages and considerations, and the best option for you will depend on your individual needs, goals, and financial circumstances.

Continue to the concluding section to wrap up the article.

Conclusion

Canceling a whole life insurance plan is a significant decision that should not be taken lightly. Before making a final choice, it is crucial to thoroughly evaluate your individual circumstances, financial goals, and insurance needs. Understanding the potential consequences and exploring alternative options can help you make an informed decision.

While canceling a whole life insurance policy may alleviate financial burdens or align with your changing insurance needs, it’s important to consider the loss of coverage and potential surrender charges. Additionally, the tax implications and limited future coverage options should be carefully assessed.

Exploring alternatives such as paid-up additions, reduced paid-up insurance, policy loans, or policy exchanges may help you maintain coverage or maximize the value of your policy without canceling it entirely. Consulting with professionals, including financial advisors, insurance experts, and tax advisors, can provide valuable insights tailored to your specific situation.

Ultimately, the decision to cancel a whole life insurance plan should be based on a comprehensive assessment of your current and future needs, as well as the potential financial implications.

Remember, life insurance serves as a vital tool to protect your loved ones and provide financial security. While it is essential to make sound financial decisions, it is equally important to prioritize the well-being of your family and loved ones.

Take the time to carefully evaluate your options, seek professional advice, and consider the long-term implications before making a final decision regarding your whole life insurance plan.

By doing so, you will be equipped to make a decision that aligns with your financial goals, insurance needs, and overall peace of mind.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance