Home>Finance>What Happens When A Life Insurance Policy Becomes Incontestable?

Finance

What Happens When A Life Insurance Policy Becomes Incontestable?

Published: October 14, 2023

Learn the importance of incontestability in life insurance policies and how it affects your financial security. Discover what happens when a life insurance policy becomes incontestable.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

- Introduction

- Understanding Incontestability Period

- What Does it Mean for a Life Insurance Policy to Become Incontestable?

- When Does a Life Insurance Policy Become Incontestable?

- Benefits of Incontestability

- Limitations of Incontestability

- Common Misconceptions about Incontestability

- How Does the Incontestability Clause Affect Policyholders?

- Reasons Why Life Insurance Claims Get Contested

- The Process of Contesting a Life Insurance Claim

- Legal Actions and Remedies for Contesting Incontestable Policies

- Conclusion

Introduction

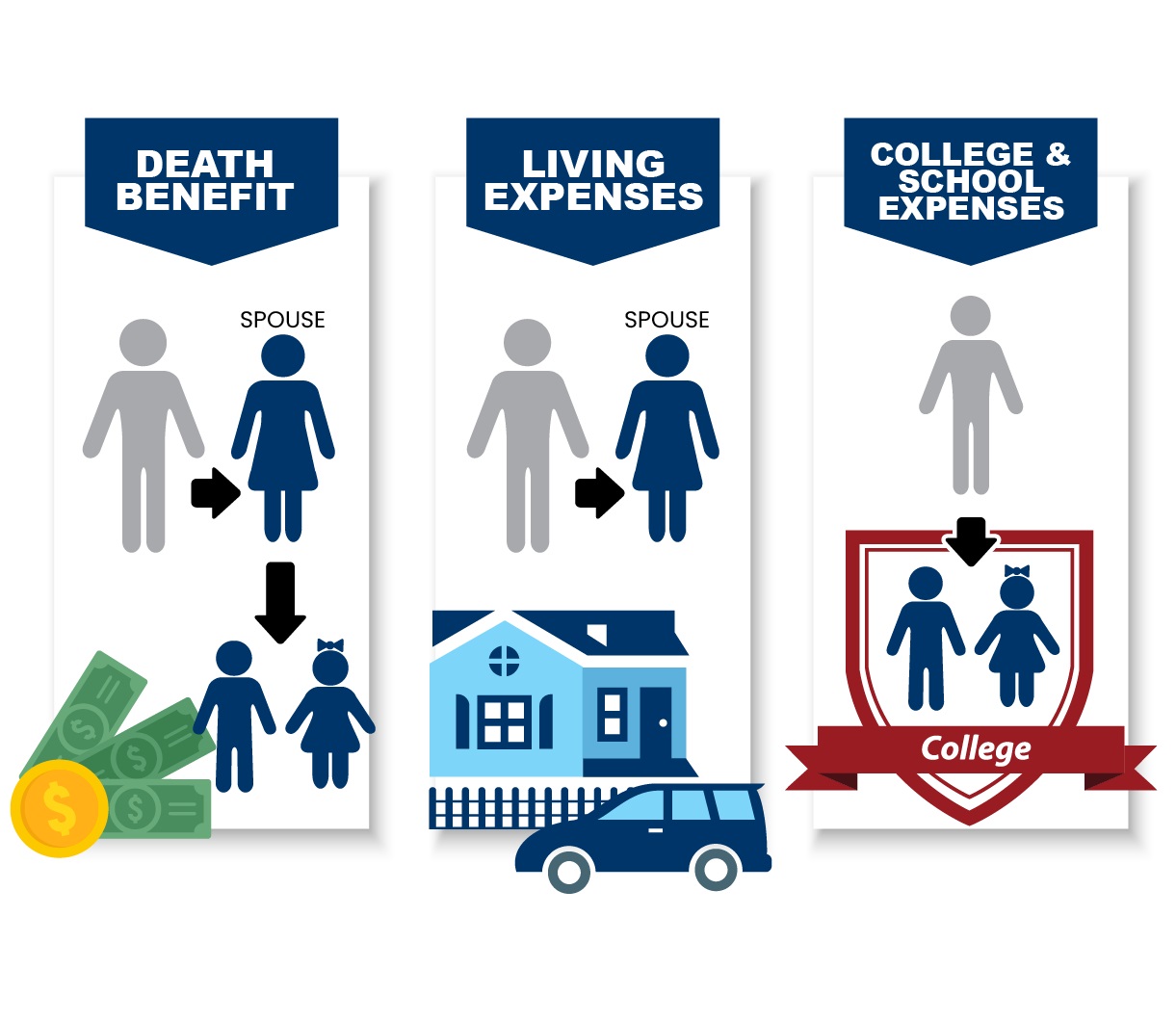

Life insurance is an essential financial tool that provides financial protection to individuals and their loved ones in the event of unfortunate circumstances. When purchasing a life insurance policy, it is important to understand the terms and conditions associated with the policy, including the concept of the incontestability period.

The incontestability period is a specific timeframe during which the insurance company has the right to contest or investigate the validity of the policy. It is a crucial aspect of a life insurance policy that affects both the policyholder and the beneficiary.

In this article, we will delve into the concept of the incontestability period, understand what it means for a life insurance policy to become incontestable, explore the benefits and limitations of incontestability, and discuss common misconceptions surrounding this clause.

We will also examine how the incontestability clause affects policyholders and the reasons why life insurance claims are contested. In addition, we will provide insights into the process of contesting a life insurance claim and the legal actions and remedies that can be pursued in such cases.

By gaining a comprehensive understanding of the incontestability period and its implications, individuals can make informed decisions when purchasing life insurance and have the necessary knowledge to navigate any potential issues that may arise throughout the policy duration.

Understanding Incontestability Period

The incontestability period is a specific period of time after a life insurance policy has been in effect, during which the insurance company cannot contest or dispute the validity of the policy, except in cases of fraud or material misrepresentation. It is designed to protect policyholders from having their claims denied arbitrarily after a certain amount of time has elapsed.

During the incontestability period, the insurance company can still investigate a claim and gather evidence. However, they are restricted from using any information that was not disclosed by the policyholder at the time of application to deny a claim or cancel the policy.

The incontestability period typically begins from the date the life insurance policy is issued, and its duration varies depending on the laws and regulations of the country or state. In most cases, the incontestability period lasts for two years, but it can be longer or shorter depending on the policy terms and local regulations.

It is important to note that the incontestability period applies to the entire life insurance policy, including both the death benefit and cash value components (if applicable). Therefore, during this period, the policyholder can rest assured that their policy is secure, and any claims made by their beneficiaries will be valid, provided that the premiums have been paid on time and there has been no fraud or misrepresentation.

Once the incontestability period expires, the life insurance policy becomes “incontestable,” meaning that the insurance company can no longer contest or challenge the validity of the policy, even if there were misrepresentations or omissions in the application. This provision provides a certain level of certainty and peace of mind for policyholders and their beneficiaries.

It is worth noting that the concept of incontestability applies to most types of life insurance policies, including term life, whole life, and universal life insurance. However, it is always important to review the specific terms and conditions of your policy to understand the exact provisions related to the incontestability period.

What Does it Mean for a Life Insurance Policy to Become Incontestable?

When a life insurance policy becomes incontestable, it means that the insurance company loses the right to contest or dispute the policy’s validity, except in cases of fraud or material misrepresentation. Once the incontestability period expires, typically after two years, the insurance company is legally bound to honor any claims made by the policyholder’s beneficiaries, regardless of any discrepancies or errors that were present in the application.

For policyholders, the transition of their life insurance policy to the incontestable phase provides a sense of security. It ensures that if they were upfront and honest at the time of application and have been paying their premiums on time, their beneficiaries will receive the death benefit without the risk of the insurance company denying the claim based on technicalities.

When a life insurance policy becomes incontestable, it also signifies the completion of the insurance company’s investigation period. During the incontestability period, the insurance company has the right to scrutinize the policy and gather any necessary evidence or information related to the policyholder’s insurability. However, once the incontestability period ends, the insurance company can no longer use any undisclosed information or discrepancies found during the investigation to deny a claim or cancel the policy.

For beneficiaries, the incontestability of a life insurance policy ensures that they will receive the intended financial protection from the policy. They can be confident in the policy’s validity and the payment of the death benefit, allowing them to cope with the financial implications of losing a loved one.

It is important to note that while a life insurance policy becomes incontestable after the expiration of the incontestability period, there are still certain conditions that can result in denial of a claim. These conditions include fraudulent actions, intentional misrepresentations, or the policy lapsing due to non-payment of premiums. Additionally, if the policy has exclusions or limitations specified in the terms and conditions, those would still apply even after the policy becomes incontestable.

In summary, when a life insurance policy becomes incontestable, it means that the insurance company can no longer challenge the policy’s validity or use undisclosed information to deny a claim. This provides policyholders and beneficiaries with peace of mind, ensuring that the policy will fulfill its intended purpose of providing financial protection to loved ones upon the policyholder’s passing.

When Does a Life Insurance Policy Become Incontestable?

A life insurance policy typically becomes incontestable after the expiration of the incontestability period, which is a predetermined timeframe established by the insurance company and governed by local laws and regulations. The duration of the incontestability period can vary, but it is commonly set at two years from the date the policy is issued.

During the initial period from the policy’s inception, which is commonly referred to as the contestability period, the insurance company has the right to investigate and contest the validity of the policy based on any misrepresentations or omissions made by the policyholder during the application process. This allows the insurance company to ensure that the policy was issued based on accurate and truthful information.

After the incontestability period elapses, the life insurance policy becomes incontestable, which means the insurance company can no longer contest or challenge the policy’s validity, except in cases of fraud or intentional misrepresentation.

It is essential to note that the incontestability period begins on the date the policy is issued and not on the date the policyholder passes away. Therefore, if the policyholder were to pass away before the expiration of the incontestability period, the insurance company might still conduct an investigation to determine whether there was any fraud or material misrepresentation that would warrant denying the claim.

However, it is crucial to understand that the incontestability provision does not provide blanket protection for policyholders who intentionally provide false information or engage in fraudulent activities. If the insurance company discovers instances of fraud or intentional misrepresentation at any point in time, they can still contest the policy’s validity and deny the claim, regardless of whether the incontestability period has elapsed.

It’s important to note that the specific duration of the incontestability period can vary between different countries and states, and it is essential to review the terms and conditions of the life insurance policy to understand the exact timeframe applicable to your specific policy.

Overall, once the incontestability period ends, policyholders can have peace of mind knowing that their life insurance policy has become incontestable, and the insurance company can no longer challenge the policy’s validity or use undisclosed information to deny a claim, except in cases of fraud or intentional misrepresentation.

Benefits of Incontestability

The incontestability provision in a life insurance policy offers several benefits to both policyholders and their beneficiaries. Understanding these benefits can provide peace of mind and assurance that the policy will fulfill its intended purpose. Let’s explore the key advantages of the incontestability clause:

- Protection against Arbitrary Denials: The incontestability period protects policyholders from having their claims denied arbitrarily by the insurance company. After this period expires, the insurance company cannot challenge the validity of the policy or use any undisclosed information to deny a claim, ensuring that the policyholder’s beneficiaries will receive the intended financial protection.

- Certainty and Peace of Mind: Knowing that the life insurance policy has become incontestable provides policyholders with a sense of security. They can rest assured that if they were honest and upfront during the application process and have diligently paid their premiums, their beneficiaries will receive the death benefit without the risk of the insurance company denying the claim.

- Stability and Consistency: The incontestability provision offers stability and consistency to policyholders and their beneficiaries. It provides a clear timeline within which the insurance company can investigate the policy and raise any concerns about misrepresentations or omissions. Once the incontestability period ends, the policy becomes secure, ensuring that the beneficiaries will receive the agreed-upon benefits upon the policyholder’s passing.

- Simplifies the Claims Process: With the incontestability provision, the claims process becomes simpler and smoother for beneficiaries. They can file a claim without worrying about the insurance company disputing the policy’s validity or searching for any undisclosed information that could lead to claim denial. This makes the process less stressful and allows beneficiaries to focus on their emotional well-being during a difficult time.

- Encourages Policyholders to Disclose Accurate Information: The incontestability period incentivizes policyholders to provide accurate and truthful information during the application process. Policyholders understand that the insurance company has a limited timeframe to investigate the policy’s validity, and after that period, they cannot deny a claim based on non-fraudulent discrepancies or omissions. This encourages policyholders to be transparent and forthcoming when disclosing their personal and health information.

Overall, the incontestability provision offers significant benefits to both policyholders and beneficiaries. It ensures that the life insurance policy remains protective and reliable, allowing policyholders to secure the financial future of their loved ones with confidence.

Limitations of Incontestability

While the incontestability provision in a life insurance policy offers numerous benefits, it is important to understand its limitations. Being aware of these limitations can help policyholders make informed decisions and manage expectations. Let’s explore the key limitations of the incontestability clause:

- Fraudulent Activities: The incontestability provision does not protect policyholders who engage in fraudulent activities when applying for or maintaining their life insurance policy. If the insurance company discovers deliberate misrepresentations or fraudulent actions, they can contest the policy’s validity, deny the claim, or even cancel the policy, even if the incontestability period has elapsed.

- Intentional Misrepresentations: Apart from outright fraud, intentional misrepresentations can also lead to the contestability of a life insurance policy, even after the incontestability period has ended. If the insurance company can prove that the policyholder knowingly provided false information or concealed material facts, they may still have grounds to dispute the policy’s validity.

- Non-Payment of Premiums: Failure to pay premiums can result in a lapsed policy, regardless of whether the incontestability period has expired. If the policyholder fails to make timely premium payments, the insurance company may cancel the policy, rendering it void and disregarding the incontestability clause.

- Policy Exclusions and Limitations: The incontestability provision does not override the specific exclusions or limitations mentioned in the policy. If a claim falls within the scope of these exclusions or limitations, the insurance company may deny the claim, irrespective of the incontestability period.

- Material Mistakes: In some cases, innocent mistakes or errors made by the policyholder at the time of application may not fall under the protection of the incontestability provision. If the mistake is deemed to be substantial and material to the insurance company’s decision to issue the policy, they may still contest the policy’s validity.

It is important for policyholders to be aware of these limitations and to answer all application questions truthfully and accurately. Providing transparent and accurate information to the best of their knowledge can help prevent any potential issues or disputes in the future.

It is also advisable to review the specific terms and conditions of the life insurance policy to understand the exclusions, limitations, and conditions under which the insurer can contest the policy’s validity.

While the incontestability provision provides significant protection and peace of mind to policyholders and beneficiaries, understanding its limitations helps manage expectations and ensures that the policy remains valid and enforceable throughout its duration.

Common Misconceptions about Incontestability

While the incontestability provision in a life insurance policy is designed to protect policyholders and their beneficiaries, there are several common misconceptions surrounding this clause. It’s important for individuals to have a clear understanding of the incontestability provision to avoid misunderstandings. Let’s debunk some of these misconceptions:

- The Incontestability Period is the Same for All Policies: One common misconception is that the incontestability period is the same for every life insurance policy. In reality, the duration of the incontestability period can vary depending on the policy terms and local regulations. It’s important to review the specific terms of your policy to determine the length of the incontestability period applicable to your policy.

- Incontestability Guarantees Payment of All Claims: While the incontestability provision provides significant protection, it does not guarantee the payment of all claims. Policyholders must still meet the policy’s requirements, such as paying premiums and ensuring that the cause of death is covered under the policy. Exclusions and limitations specified in the policy may still result in claim denial, even after the incontestability period has expired.

- Any Misrepresentation or Omission Voids the Policy: Another misconception is that any misrepresentation or omission automatically voids the entire policy. In reality, the insurance company needs to prove that the misrepresentation was material and influenced their decision to issue the policy. Mere errors or minor discrepancies may not be enough to contest the policy’s validity.

- Once the Incontestability Period Ends, Misrepresented Information No Longer Matters: While the incontestability provision limits the insurance company’s ability to contest the policy’s validity based on non-fraudulent misrepresentations, intentional misrepresentations can still result in claim denial even after the incontestability period has expired. Policyholders should always provide accurate and truthful information during the application process.

- The Incontestability Provision Protects Against All Forms of Non-Disclosure: It’s a common misconception that the incontestability provision protects against all forms of non-disclosure, including intentional concealment of relevant facts. The insurance company can still challenge the policy if they can establish intentional non-disclosure or fraudulent actions that materially impact the policy’s risk assessment.

Understanding these misconceptions is crucial for policyholders to have realistic expectations and make informed decisions regarding their life insurance policies. It’s recommended to thoroughly review the terms and conditions of the policy and seek clarification from the insurance company or a qualified professional to ensure a clear understanding of the incontestability provision and its implications.

By dispelling these misconceptions, individuals can approach their life insurance policies with a better understanding of their rights and responsibilities, enabling them to make informed decisions and avoid potential disputes or claim denials in the future.

How Does the Incontestability Clause Affect Policyholders?

The incontestability clause in a life insurance policy has a significant impact on policyholders. Understanding how this clause affects policyholders is crucial for making informed decisions and managing their life insurance coverage. Let’s explore the ways in which the incontestability clause affects policyholders:

- Security and Certainty: The incontestability clause provides policyholders with a sense of security and certainty. Once the incontestability period ends, policyholders can rest assured that their life insurance policy is secure, and the insurance company cannot contest the policy’s validity based on non-fraudulent misrepresentations made during the application process. This ensures that the policyholders’ beneficiaries will receive the intended financial protection upon the policyholder’s passing.

- Transparency and Accountability: The presence of the incontestability clause encourages policyholders to provide accurate and truthful information during the application process. Knowing that there is a limited timeframe within which the insurance company can investigate the policy’s validity, policyholders are more likely to disclose their personal and health information transparently. This fosters a higher level of accountability and promotes ethical practices within the life insurance industry.

- Claim Settlement: The incontestability provision facilitates a smoother and faster claims settlement process for policyholders’ beneficiaries. Once the incontestability period ends, the insurance company cannot raise issues about the policy’s validity based on non-fraudulent misrepresentations. This eliminates potential delays or complications in the claims settlement process and ensures that the beneficiaries can receive the death benefit without unnecessary hurdles or uncertainties.

- Policy Evaluation: The incontestability clause prompts policyholders to thoroughly review and evaluate their life insurance policies during the incontestability period. This period offers an opportunity for policyholders to ensure that the policy accurately reflects their needs and circumstances. Policyholders may review their coverage, beneficiaries, and any additional riders or endorsements to make necessary adjustments or updates to their policy.

- Protection against Arbitrary Denials: The incontestability clause protects policyholders from having their claims denied arbitrarily by the insurance company. Once the incontestability period ends, the insurance company cannot use undisclosed information or non-fraudulent misrepresentations to question the validity of the policy or deny a claim. This ensures that policyholders and their beneficiaries receive the intended financial protection as agreed upon in the policy.

It’s important for policyholders to understand the impact of the incontestability clause on their life insurance coverage. By being aware of their rights and the limitations of the clause, policyholders can confidently navigate their life insurance policies and ensure that they provide adequate financial protection for themselves and their loved ones.

Reasons Why Life Insurance Claims Get Contested

While the incontestability provision in a life insurance policy provides significant protection for policyholders, there are certain situations where life insurance claims may still get contested. It’s crucial to understand the reasons behind these contests to navigate potential challenges. Here are some common reasons why life insurance claims may be contested:

- Fraudulent Misrepresentations: Insurance companies may contest a life insurance claim if they discover that the policyholder intentionally provided false information or engaged in fraudulent activities during the application process. This includes misrepresenting health conditions, income, or other pertinent details. Fraudulent misrepresentations can void the policy and result in claim denial.

- Non-Disclosure of Material Facts: If a policyholder fails to disclose material facts that are crucial to the underwriting process or that would have impacted the insurance company’s decision to issue the policy, the claim may be contested. Material facts can include pre-existing medical conditions, risky occupations, or dangerous hobbies. Non-disclosure of material facts may be seen as a breach of the duty of utmost good faith, leading to contesting the claim.

- Lapsed Policy Due to Non-Payment of Premiums: If the policyholder fails to pay premiums within the grace period specified in the policy, the policy may lapse, leading to claim denial. It’s vital for policyholders to stay current with premium payments to maintain the policy’s validity and ensure that claims can be successfully made.

- Discrepancies in the Cause of Death: If the cause of death outlined in the death certificate does not align with the terms and conditions of the life insurance policy, the claim may be contested. The insurance company may request additional information or investigation to verify the cause of death and its correlation to the policy coverage.

- Policy Exclusions or Limitations: Some life insurance policies have specific exclusions or limitations that restrict coverage for certain situations or causes of death. If the claim falls within these exclusions or limitations, the insurance company may contest the claim based on the terms outlined in the policy.

- Policy Contestability Period: During the contestability period, which typically lasts for the first two years of the policy, the insurance company has the right to contest the policy based on any misrepresentations or omissions. If the insurance company finds discrepancies in the application during this period, they may contest the policy’s validity and deny the claim.

- Unintentional Errors or Mistakes: In some cases, genuine errors or mistakes may occur in the application process or policy documentation. While these errors are not intentional misrepresentations, they can still impact the claims settlement process and may need to be resolved before the claim can be approved.

It’s important for policyholders to provide accurate and truthful information during the application process and throughout the life of the policy. Understanding the reasons why life insurance claims may be contested can help policyholders take necessary precautions and ensure that their policies remain valid and enforceable.

The Process of Contesting a Life Insurance Claim

While the incontestability provision in a life insurance policy provides protection for policyholders, there may be instances where a claim becomes contested. The process of contesting a life insurance claim involves several steps and requires both the policyholder and the insurance company to navigate through the dispute. Here is a general overview of the process:

- Initiating the Claim: The first step is for the beneficiary or the policyholder’s representative to initiate the claim by notifying the insurance company of the policyholder’s passing. They usually need to provide the necessary documentation, such as the death certificate, policy details, and any other supporting documents requested by the insurer.

- Claim Investigation: The insurance company will initiate an investigation into the claim. This typically includes reviewing the policyholder’s application, medical records, and any other relevant documents. The purpose of the investigation is to assess whether the claim meets the policy’s terms and conditions and determine if any misrepresentations or omissions were made.

- Communication and Documentation: Throughout the investigation process, both the insurance company and the beneficiary or representative of the policyholder should maintain open communication. The insurance company may request additional information or documentation to support the claim, and it is essential to provide prompt and accurate responses.

- Resolution and Decision: Once the investigation is complete, the insurance company will make a decision regarding the claim. If they find that the claim is valid and meets the policy’s terms, they will proceed with the claim settlement. However, if there are concerns regarding misrepresentations, non-disclosure, or other factors, the insurance company may contest the claim and deny payment.

- Dispute Resolution: In the event of a contested claim, the beneficiary or representative can engage in dispute resolution processes to seek a resolution. This may involve negotiations or mediation with the insurance company, or, if necessary, seeking legal recourse through arbitration or filing a lawsuit.

- Legal Actions and Remedies: If all attempts at dispute resolution fail, the beneficiary may pursue legal actions against the insurance company. This involves working with an attorney who specializes in insurance law to present the case in court and seek a favorable outcome.

- Court Decision and Appeal: If the case reaches the court, a judgment will be made based on the evidence and arguments presented. If the beneficiary is dissatisfied with the court’s decision, they may have the option to appeal the decision and continue the legal process.

It’s important to note that the process of contesting a life insurance claim can be complex and time-consuming. Engaging professional assistance, such as hiring an attorney well-versed in insurance law, can provide valuable guidance and representation throughout the process.

Policyholders and beneficiaries should familiarize themselves with the terms and conditions of the life insurance policy to understand the requirements, exclusions, and limitations that may impact the claims process. Promptly notifying the insurance company of the policyholder’s passing and providing complete and accurate documentation can help facilitate a smoother claims process and potentially prevent disputes.

Ultimately, contesting a life insurance claim requires careful consideration and thorough understanding of the policy and legal options available. Seeking professional advice is crucial to navigate the complexities and ensure the best possible outcome.

Legal Actions and Remedies for Contesting Incontestable Policies

While life insurance policies are generally considered incontestable after the expiration of the incontestability period, there are situations where beneficiaries may need to contest the policy’s validity. Contesting an incontestable policy involves legal actions and remedies that can help beneficiaries seek a favorable outcome. Here are some important options to consider:

- Review the Policy Terms: It’s crucial to thoroughly review the terms and conditions of the life insurance policy to understand the provisions, exclusions, and limitations that may impact the claim. This will help determine whether there are any grounds for contesting the incontestable policy.

- Consult with an Attorney: Engaging the services of an attorney who specializes in insurance law is highly recommended when contesting an incontestable policy. They can assess the situation, review the policy and relevant documents, and provide guidance on the legal options available.

- Investigate Misrepresentations or Fraud: If there is evidence of intentional misrepresentations or fraudulent activities by the policyholder during the application process, beneficiaries can gather documentation and present it as a basis for contesting the policy’s validity. This may involve providing evidence of forged signatures, false information, or other fraudulent actions.

- Non-Disclosure of Material Facts: If the policyholder failed to disclose material facts that would have influenced the insurance company’s decision to issue the policy, beneficiaries can explore contesting the policy on the grounds of non-disclosure. This may involve demonstrating how the undisclosed information is material and relevant to the policy’s validity.

- Presentation of Evidence: Beneficiaries contesting an incontestable policy may need to present evidence, such as medical records, expert opinions, or witness testimonies, to support their case. This evidence should clearly establish a breach of the policy’s terms, fraud, or material non-disclosure.

- Alternative Dispute Resolution: In some cases, beneficiaries may be able to engage in alternative dispute resolution methods such as mediation or negotiation. This can allow both parties to find a mutually agreeable resolution without resorting to full-scale litigation.

- Initiation of Legal Proceedings: If all other attempts at resolving the dispute fail, beneficiaries may need to initiate legal proceedings in court. This involves filing a lawsuit against the insurance company, presenting their case, and arguing for a just outcome.

- Appeal of Court Decisions: Should the court ruling be unfavorable, beneficiaries may have the option to appeal the decision. This involves presenting their case to a higher court and seeking a reversal or modification of the initial court’s ruling.

When contesting an incontestable life insurance policy, it’s vital to have proper legal representation and to follow the established procedures within the legal system. Working alongside an experienced attorney throughout the process can significantly enhance the chances of success in contesting the policy.

It’s important to note that contesting an incontestable policy can be complex and time-consuming. Beneficiaries should act promptly, gather all relevant evidence, and consult with legal professionals to ensure the strongest possible case is presented.

Overall, while incontestability generally limits contesting life insurance policies, there are legal actions and remedies available to beneficiaries in certain circumstances. Seeking legal advice and understanding the options within the legal system are crucial steps to contest an incontestable policy and seek a just resolution.

Conclusion

The incontestability provision in a life insurance policy serves as a crucial safeguard for policyholders and their beneficiaries. It provides a level of certainty and protection by limiting the insurance company’s ability to contest the policy’s validity after the expiration of the incontestability period. Understanding the incontestability clause and its implications is essential for policyholders to make informed decisions and have peace of mind.

While the incontestability provision offers significant benefits, such as protection against arbitrary denials and simplified claims processes, it is important to be aware of its limitations. Non-disclosure of material facts, intentional misrepresentations, policy exclusions, and non-payment of premiums can still impact the policy’s validity, warranting contestation of the claim.

In cases where beneficiaries need to contest an incontestable policy, it becomes crucial to engage legal resources. Consulting with an attorney who specializes in insurance law will help assess the situation, explore legal options, and navigate the complexities of the claims dispute process.

Policyholders should always strive to provide accurate and truthful information during the application process and throughout the policy’s duration. Maintaining open communication with the insurance company and promptly fulfilling any documentation or information requests can help streamline the claims process and minimize potential disputes.

Ultimately, the incontestability provision aims to provide policyholders and their beneficiaries with a sense of security and stability. It ensures that if the policyholder acted in good faith and fulfilled their obligations, their loved ones will receive the intended financial protection when it matters most.

By understanding the incontestability provision, being transparent in one’s disclosures, and seeking legal guidance when necessary, policyholders can effectively protect their interests and secure the intended benefits of their life insurance policies.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance