Finance

What Is A 650 Credit Score

Modified: March 6, 2024

Discover what a 650 credit score means for your financial future. Learn how to improve your credit and secure better finance opportunities.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

Introduction

Welcome to the world of credit scores! In today’s financial landscape, credit scores play a crucial role in determining our financial health and opportunities. Whether you’re applying for a loan, renting an apartment, or even getting a job, your credit score can have a significant impact on the outcome.

But what exactly is a credit score? Simply put, a credit score is a three-digit number that reflects your creditworthiness. It is a numerical representation of your credit history and serves as a measure of how responsible you are with credit. The higher your credit score, the more reliable and trustworthy you appear to lenders and creditors.

In this article, we will delve into the world of credit scores and focus specifically on a 650 credit score. We will explore what it means to have this score, the factors that affect it, and the implications it can have on your financial journey. So let’s dive in and unravel the mysteries of a 650 credit score!

Understanding Credit Scores

Before we delve into the specifics of a 650 credit score, let’s take a moment to understand the broader concept of credit scores. A credit score is a numerical representation of an individual’s creditworthiness and is used by lenders and creditors to assess the risk of extending credit to someone.

There are several credit scoring models in use today, but the most common one is the FICO score. FICO scores range from 300 to 850, with higher scores indicating better creditworthiness. The score is calculated using various factors, including your payment history, credit utilization, length of credit history, types of credit, and new credit applications.

Each credit bureau—Experian, Equifax, and TransUnion—generates its own credit report and FICO score based on the information contained in your credit history. It’s important to note that your credit score may vary slightly between these bureaus, as they may have different data or scoring models.

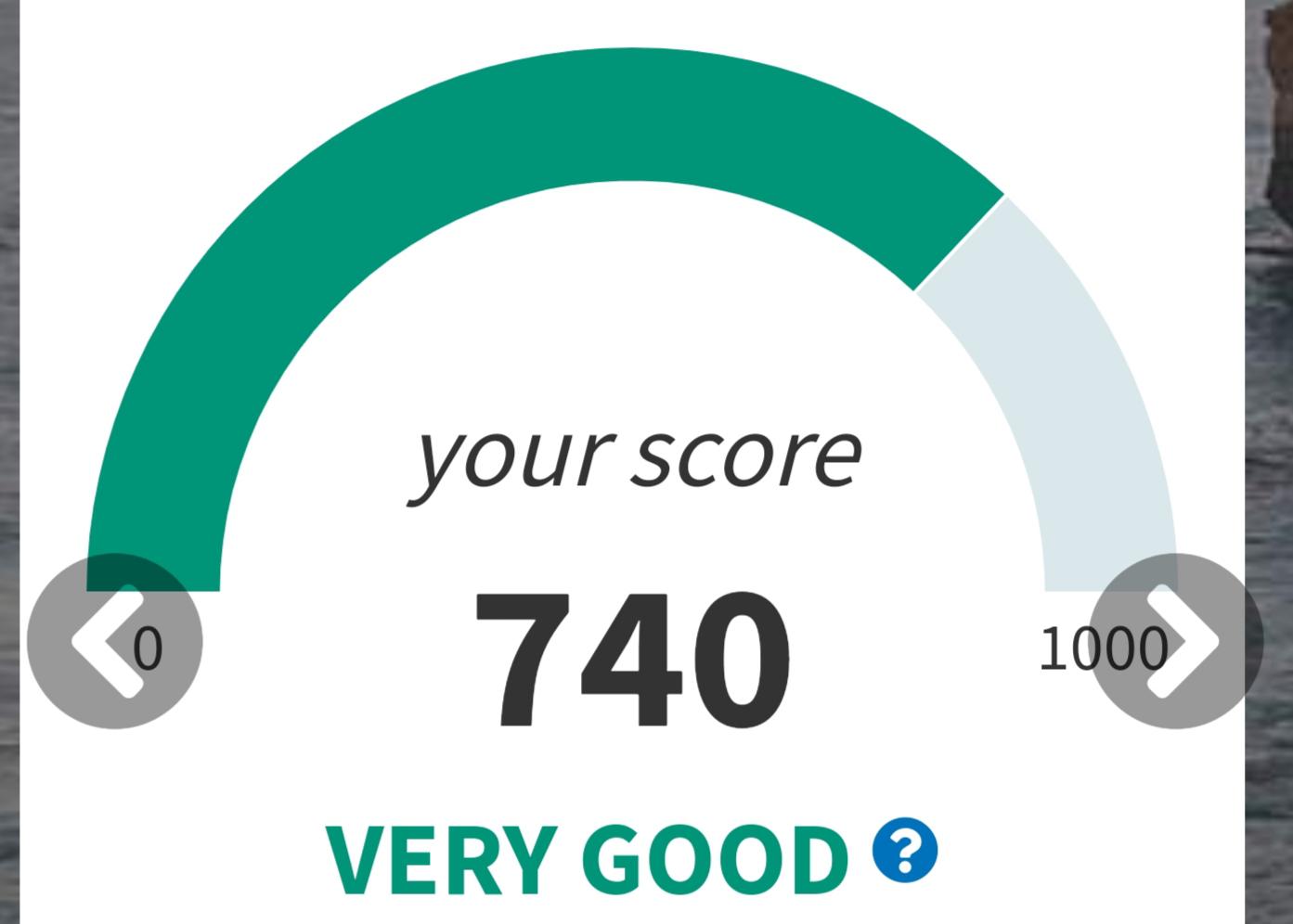

Understanding the range of credit scores is essential. Generally, a score above 700 is considered good, while a score below 600 may be viewed as poor credit. A score between 600 and 700 is considered fair, and this is where a 650 credit score falls – somewhere in the middle.

Now that we have a basic understanding of credit scores, let’s dive into what a 650 credit score means and how it can impact your financial journey.

What is a 650 Credit Score?

A 650 credit score is considered a fair credit score. It indicates that you have a moderate credit history and may have had some past credit challenges. While it may not be considered excellent, a 650 credit score is still within a range that allows you to access various financial opportunities.

With a 650 credit score, you may be able to qualify for loans and credit cards, although the interest rates and terms may not be as favorable as those offered to individuals with higher credit scores. Lenders may view you as a moderate risk and may have some reservations about extending credit to you.

It’s important to remember that a credit score is not a static number and can change over time. With responsible financial habits and management, you can work towards improving your credit score and gaining access to better opportunities in the future.

While a 650 credit score may not be ideal, it’s essential to understand that credit scores are just one piece of the financial puzzle. Lenders and creditors also consider other factors, such as income, employment history, and debt-to-income ratio, when evaluating creditworthiness.

Now that we understand what a 650 credit score represents let’s explore the factors that can affect this score.

Factors Affecting a 650 Credit Score

A 650 credit score is influenced by various factors that reflect your creditworthiness and financial behavior. Understanding these factors can help you identify areas where you can make improvements and work towards increasing your credit score over time.

1. Payment History: One of the most critical factors affecting your credit score is your payment history. Paying your bills on time and in full demonstrates responsible financial behavior and can have a positive impact on your credit score. On the other hand, late payments or defaulting on loans can significantly lower your score.

2. Credit Utilization: Credit utilization refers to the percentage of your available credit that you are currently using. It’s recommended to keep your credit utilization rate below 30%. Higher credit utilization can indicate a higher risk of default and can negatively impact your credit score.

3. Length of Credit History: The length of your credit history influences your credit score. A longer credit history signifies a more established financial track record, which can be beneficial for your score. If you’re just starting to build your credit, it may take time to see significant improvement in this area.

4. Types of Credit: The types of credit you have also play a role in determining your credit score. A healthy mix of revolving credit (credit cards) and installment loans (car loans, mortgages) can have a positive impact. However, having too many accounts or having a large amount of debt can negatively affect your score.

5. New Credit Applications: Every time you apply for new credit, it can result in a hard inquiry on your credit report. Multiple hard inquiries within a short period can signal potential financial distress and may lower your credit score. It’s important to be mindful of the number of credit applications you make.

6. Public Records and Collections: Public records such as bankruptcies, liens, or collections can have a severe negative impact on your credit score. It’s crucial to resolve any outstanding issues and maintain a clean credit history.

By understanding these factors, you can take proactive steps to improve your credit score over time. Let’s explore the pros and cons of having a 650 credit score next.

Pros and Cons of a 650 Credit Score

Having a 650 credit score comes with both advantages and disadvantages. Understanding the pros and cons can help you navigate your financial decisions and make informed choices.

Pros:

- Access to Credit: With a 650 credit score, you can still qualify for loans and credit cards, although the terms may not be as favorable as those offered to individuals with higher scores. This allows you to access credit and meet your financial needs.

- Opportunity for Improvement: A 650 credit score provides an opportunity for improvement. By practicing responsible financial habits and managing your credit wisely, you can work towards increasing your score over time and gain access to better financial opportunities.

- Building Credit History: A 650 credit score indicates that you have a moderate credit history, which means you have started building a credit profile. This can be advantageous, especially if you maintain positive financial behavior moving forward.

Cons:

- Higher Interest Rates: With a 650 credit score, you may be offered loans or credit cards with higher interest rates compared to those with excellent credit scores. This can result in paying more interest over the life of a loan, making borrowing more expensive.

- Limited Credit Options: Some lenders or credit issuers may have stricter requirements and may be less likely to extend credit to individuals with a 650 credit score. This can limit your options and make it more challenging to access certain financial products.

- Less Favorable Terms: Even if you do qualify for credit, the terms and conditions may not be as favorable as those offered to individuals with higher credit scores. This can include smaller credit limits, shorter repayment periods, or stricter borrowing terms.

It’s important to remember that a credit score is not the sole determinant of your financial health. While a 650 credit score may have its challenges, it’s possible to improve it over time and increase your opportunities for better financial outcomes.

Next, let’s explore some strategies you can use to improve your 650 credit score.

How to Improve a 650 Credit Score

If you have a 650 credit score and want to improve it, there are several strategies you can implement to help boost your score over time. Here are some steps you can take:

1. Pay Your Bills on Time: Consistently paying your bills by the due date is one of the most effective ways to improve your credit score. Set up reminders or automatic payments to ensure you never miss a payment.

2. Reduce Your Credit Utilization: Aim to keep your credit utilization below 30% of your available credit. Paying down your balances and avoiding maxing out your credit cards can have a positive impact on your score.

3. Dispute Any Inaccuracies: Regularly review your credit reports from all three credit bureaus and dispute any inaccuracies or errors. Mistakes in your credit report can drag down your score, so it’s important to keep your reports accurate and up to date.

4. Limit New Credit Applications: Each time you apply for new credit, it results in a hard inquiry on your credit report. Limit the number of new credit applications to minimize the potential negative impact on your score.

5. Diversify Your Credit Mix: Having a mix of different types of credit can demonstrate responsible credit management. Consider adding a different type of credit, such as an installment loan, to your credit profile if you only have credit cards.

6. Keep Old Accounts Open: Closing old accounts can shorten your credit history, which can negatively affect your score. If you have old accounts in good standing, consider keeping them open to maintain a longer credit history.

7. Practice Patience: Building or improving your credit score takes time. Be patient and consistent with your efforts, as positive changes to your credit score won’t happen overnight.

Implementing these strategies, along with responsible financial habits, can help improve your 650 credit score over time. Remember, the key is to maintain consistent positive behavior and be patient with the process.

Now, let’s wrap up the article.

Conclusion

A 650 credit score may fall in the fair credit range, but it doesn’t mean you’re locked into that category forever. With diligence and smart financial choices, you can improve your score and open doors to better financial opportunities.

Understanding the factors that affect your credit score is crucial. By managing your payment history, credit utilization, credit mix, and new credit applications, you can make significant strides in improving your score. It’s also important to address any inaccuracies in your credit reports and maintain a long-term perspective, as building credit takes time.

While a 650 credit score may come with some limitations, it also provides access to credit and a chance for improvement. Take advantage of the opportunities available to you, demonstrate responsible financial behavior, and build a strong credit foundation for your future.

Remember, a credit score is just one piece of the financial puzzle. It’s important to maintain overall financial health by budgeting, saving, and managing your debts effectively. By doing so, you’ll not only improve your credit score but also set yourself up for long-term financial success.

So, embrace the journey of improving your credit score and use it as a stepping stone towards achieving your financial goals. With determination and persistence, you can elevate your credit score and open doors to a brighter financial future.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance