Finance

What Is A 550 Credit Score

Modified: March 1, 2024

Learn what a 550 credit score means and how it can affect your financial situation. Discover strategies to improve your credit score and achieve better financial health.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

Introduction

When it comes to managing your personal finances, your credit score plays a crucial role. It is a three-digit number that reflects your creditworthiness and provides lenders with an assessment of your ability to repay loans and debts. A higher credit score indicates a lower risk for lenders, making it easier for you to secure favorable interest rates and loan terms.

However, not everyone has a perfect credit score. If you find yourself with a credit score of 550, you may be wondering what this means for your financial future. In this article, we’ll explore the specifics of a 550 credit score, including what it represents, factors that impact it, and steps you can take to improve it.

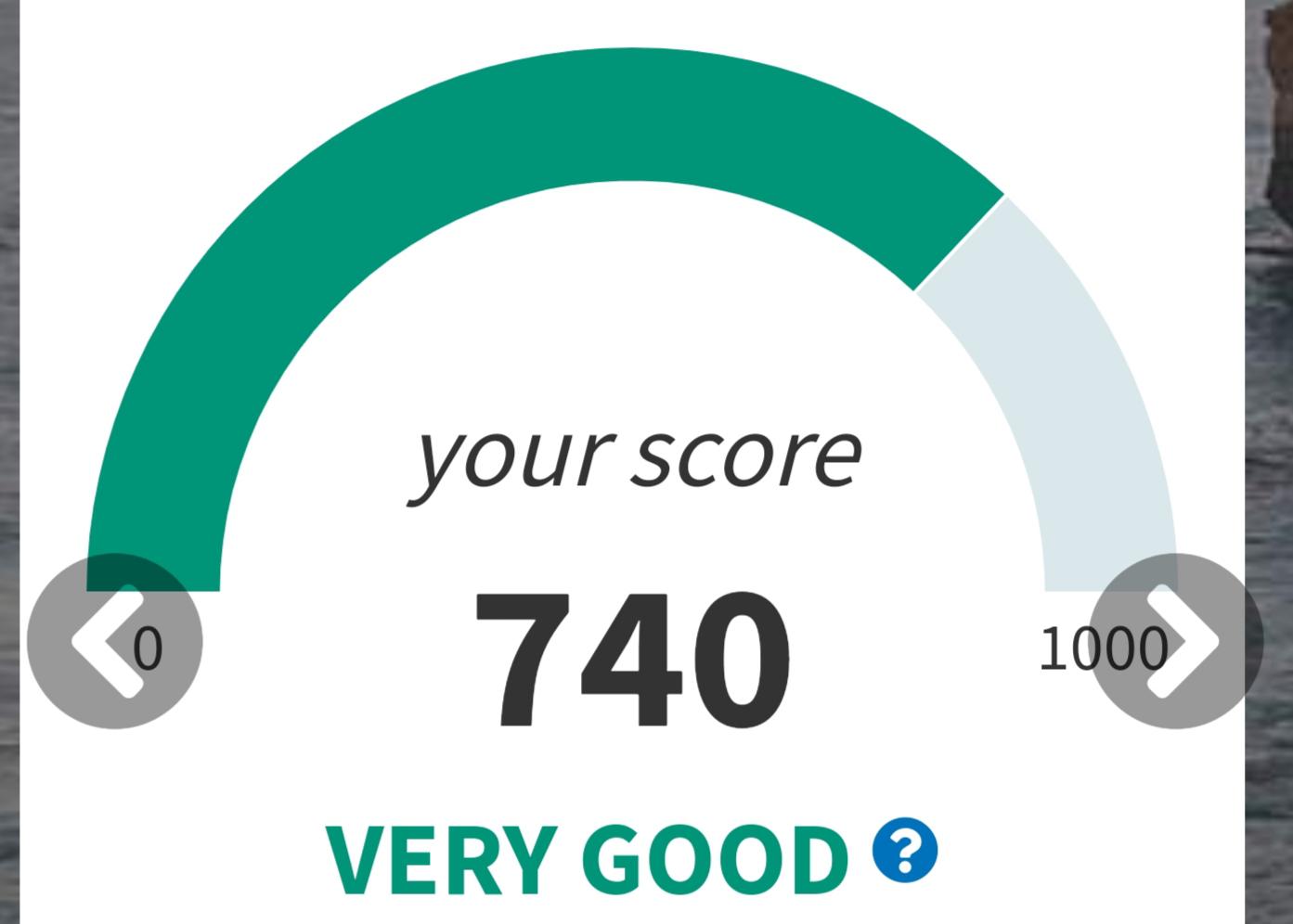

Understanding your credit score is the first step in taking control of your financial well-being. A credit score can range from 300 to 850, with higher scores indicating a healthier credit profile. Typically, lenders categorize credit scores in ranges, with each range reflecting different levels of creditworthiness.

With this in mind, let’s delve into the details of a 550 credit score and its implications.

Understanding Credit Scores

Before diving into the specifics of a 550 credit score, it’s important to have a basic understanding of how credit scores are calculated and what they entail. Credit scoring models, such as the widely used FICO® Score, take into account various factors to determine an individual’s creditworthiness.

The main components that contribute to a credit score include:

- Payment history: This is the most significant factor affecting your credit score, accounting for approximately 35%. It reflects how consistently you make your payments on time and if you have any delinquencies or defaults.

- Amounts owed: This considers the total amount of debt you have, including credit card balances, loans, and mortgages. It accounts for approximately 30% of your credit score.

- Length of credit history: The length of time you’ve been using credit is also important, as it demonstrates your ability to manage credit responsibly. This factor makes up about 15% of your credit score.

- New credit: Opening several new credit accounts within a short period can negatively impact your credit score. Lenders may perceive this as a sign of financial instability. New credit accounts for about 10% of your credit score.

- Credit mix: Having a diverse mix of credit accounts can positively impact your credit score. This includes credit cards, loans, and mortgages. Credit mix contributes to approximately 10% of your credit score.

Understanding these components will help you grasp how your financial behavior affects your credit score. It’s important to note that credit scores are dynamic and can change over time based on your financial decisions and actions.

What is a 550 Credit Score?

A credit score of 550 is considered a relatively low credit score. It falls within the poor or fair range, indicating potential credit challenges and higher borrowing costs. Lenders may view individuals with a 550 credit score as higher risk borrowers, which can make it more difficult to qualify for loans, credit cards, or favorable interest rates.

With a 550 credit score, you may face limitations and restrictions when it comes to accessing credit. Lenders may be hesitant to extend credit to you, and if they do, it may come with higher interest rates or more stringent terms. It’s also worth noting that utility providers, landlords, insurers, and even employers may check your credit score to determine your financial responsibility and reliability.

Having a 550 credit score suggests that you may have some negative marks on your credit history. This could include missed or late payments, high credit utilization, accounts in collections, or even bankruptcy. It’s crucial to thoroughly review your credit report to identify any errors or areas for improvement.

While a 550 credit score may limit your options in terms of credit, it is not a permanent condition. With dedication and effort, you can work towards improving your credit score over time.

Factors Affecting a 550 Credit Score

A credit score of 550 is influenced by several factors that contribute to its current state. Here are some key factors that can affect your credit score:

- Payment history: Late or missed payments can have a significant negative impact on your credit score. Payment history is one of the most influential factors determining your creditworthiness.

- Credit utilization: The amount of credit you’re currently using compared to your total available credit is known as credit utilization. Higher credit utilization ratios can lower your score. Ideally, you should aim to keep your credit utilization below 30%.

- Derogatory marks: Negative items such as bankruptcies, foreclosures, or collections can severely impact your credit score. These derogatory marks indicate a higher level of risk to lenders.

- Length of credit history: The length of time you have had credit accounts plays a role in determining your credit score. A longer credit history can demonstrate your ability to manage credit responsibly and may have a positive impact on your score.

- New credit applications: Applying for multiple new credit accounts within a short period can raise concerns for lenders. It can be seen as an indicator of financial distress or potential overextension.

These factors, among others, contribute to your credit score and can have a significant impact on its overall rating. It’s essential to understand how each factor affects your creditworthiness and take steps to improve areas that are negatively impacting your score.

Impact of a 550 Credit Score

A credit score of 550 can have various impacts on your financial life. Here are some key areas where the impact of a 550 credit score may be felt:

- Difficulty obtaining credit: With a low credit score, you may face challenges when applying for new lines of credit, such as loans or credit cards. Lenders may view you as a higher risk borrower and may be hesitant to extend credit to you.

- Higher interest rates: If you are approved for credit with a 550 credit score, you may encounter significantly higher interest rates compared to someone with a higher credit score. This can result in higher monthly payments and increased overall borrowing costs.

- Limited borrowing options: Your options for securing loans or credit cards may be limited with a 550 credit score. You may have to explore alternative lending options or consider secured credit cards to build or rebuild your credit.

- Difficulty securing housing: Landlords and property management companies often review credit scores when considering rental applications. With a score of 550, you may face challenges renting a desirable property or be required to provide a higher security deposit.

- Inability to qualify for certain services: Utility providers, insurance companies, and even employers may check credit scores to determine financial responsibility. A low credit score may lead to higher insurance premiums or result in being denied services or job opportunities.

It’s important to recognize the impact of a 550 credit score and take proactive steps to improve your creditworthiness. By doing so, you can expand your borrowing options, secure more favorable interest rates, and improve your overall financial stability.

Improving a 550 Credit Score

If you have a 550 credit score, don’t despair. There are several steps you can take to improve your creditworthiness and work towards a better credit score. Here are some strategies to consider:

- Pay your bills on time: Consistently making on-time payments is one of the most effective ways to improve your credit score. Set up payment reminders or automate payments to ensure you never miss a due date.

- Reduce your credit utilization: Aim to keep your credit utilization below 30% by paying down existing balances and avoiding maxing out your credit cards. Lower utilization demonstrates responsible credit management.

- Address derogatory marks: If you have derogatory marks, such as collections or bankruptcies, work towards resolving them. Consider negotiating with creditors or seeking professional help to establish payment plans or settle debts.

- Build a positive credit history: Open a secured credit card or become an authorized user on someone else’s credit card to start building a positive credit history. Make small purchases and pay them off in full each month.

- Monitor your credit report: Regularly review your credit report for any errors or discrepancies. Dispute any inaccuracies and follow up to ensure they are rectified, as they may be negatively impacting your score.

- Be patient and consistent: Improving a credit score takes time, so be patient and consistent with your efforts. Focus on positive financial habits and responsible credit management to see gradual improvements over time.

Remember, improving your credit score is a journey that requires discipline and commitment. By implementing these strategies and maintaining good financial habits, you can steadily raise your credit score and position yourself for better borrowing opportunities and financial stability.

Conclusion

Your credit score is a vital aspect of your financial health, and a 550 credit score may present some challenges. However, it’s important to remember that a credit score is not permanent, and there are steps you can take to improve it over time.

A 550 credit score indicates potential credit difficulties and may result in higher borrowing costs, limited options for credit, and difficulties in securing housing or certain services. However, by focusing on improving your financial habits and implementing strategies such as making timely payments, reducing credit utilization, and addressing derogatory marks, you can gradually rebuild your creditworthiness.

Patience and consistency are key when it comes to improving a credit score. While it may take time, the effort you put into managing your credit responsibly will eventually yield positive results.

Remember to monitor your credit report regularly for any errors or discrepancies, and take the necessary steps to correct them. Building a positive credit history and maintaining healthy financial habits will not only boost your credit score but also set you on the path to achieving long-term financial success.

So, if you find yourself with a 550 credit score, don’t lose hope. With determination and a focus on improving your creditworthiness, you can work towards a brighter financial future.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance