Finance

What Is Deferred Income Tax

Modified: December 29, 2023

Learn what deferred income tax is in the field of finance and how it can impact your financial statements and tax returns.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

Introduction

Understanding the intricacies of finance is essential for individuals, businesses, and even governments. One critical aspect of financial management is the concept of deferred income tax. As we navigate through the complex world of finance, it is crucial to comprehend what deferred income tax entails and the implications it has on the financial statements.

Deferred income tax refers to the concept of postponing or deferring the payment of income taxes to future periods. This deferral occurs when there is a difference between the tax liability calculated based on the tax laws and regulations, and the amount recognized for financial reporting purposes. This difference arises due to variations in the timing of recognizing revenue, expenses, and assets/liabilities between accounting and tax rules.

Accounting for deferred income tax involves recognizing the future tax consequences of temporary differences between financial and taxable income. These temporary differences can occur due to various reasons, such as accelerated depreciation methods, inventory valuation differences, or the recognition of income in different periods for tax and accounting purposes.

Organizations are required to account for deferred income tax in order to provide accurate and transparent financial statements. Deferred tax assets and liabilities are recorded on the balance sheet and can have a significant impact on the company’s overall financial position and performance.

Understanding the reasons behind deferred income tax is crucial. One of the primary reasons for its existence is the difference between tax laws and accounting standards. Tax laws are designed to generate revenue for the government and may have different rules and rates compared to accounting principles. Furthermore, revenue recognition rules and timing differences between recognizing expenses and deductions for tax purposes also contribute to the creation of deferred income tax liabilities or assets.

The impact of deferred income tax on financial statements can be significant. Deferred tax liabilities represent future tax obligations, while deferred tax assets represent potential tax benefits. These balances can affect the organization’s net income, tax expense, and ultimately, its overall profitability. It is essential for financial analysts, investors, and other stakeholders to understand these impactsto make informed decisions.

Let’s dive deeper into the nuances of deferred income tax through examples and explore the importance of understanding it for financial management in our upcoming sections.

Definition of Deferred Income Tax

Deferred income tax refers to the accounting practice of recognizing the future tax consequences of temporary differences between the financial and taxable income. It arises when there is a timing difference in recognizing revenue, expenses, and assets/liabilities for tax and accounting purposes. The concept of deferred income tax is crucial for organizations to accurately reflect their financial position and performance.

When there is a temporary difference between the financial and taxable income, it results in deferred tax assets or deferred tax liabilities. These temporary differences can arise due to various factors, such as the use of different depreciation methods, recognition of revenue differently based on accounting standards and tax regulations, or the treatment of certain expenses.

A deferred tax liability is recognized when the taxable income is higher than the financial income, resulting in a future tax payment. This can happen, for example, when revenue is recognized for accounting purposes before it is taxable according to the tax regulations. The organization needs to account for the future tax obligation associated with this revenue.

On the other hand, a deferred tax asset is recognized when the financial income is higher than the taxable income, resulting in a potential tax benefit in the future. This can occur when an expense is recognized for accounting purposes, but it becomes deductible for tax purposes in a later period.

The recognition and measurement of deferred income tax are in accordance with accounting standards, such as Generally Accepted Accounting Principles (GAAP) or International Financial Reporting Standards (IFRS). Organizations need to calculate the deferred income tax by applying the applicable tax rates to the temporary differences and adjust it annually based on changes in tax laws or rates.

It is important to note that deferred income tax is a non-cash item, meaning it does not involve an actual cash outflow or inflow at the time it is recognized on the financial statements. However, it impacts the organization’s tax liability and ultimately influences its cash flow in the future when the deferred tax assets are realized or deferred tax liabilities are settled.

Overall, deferred income tax helps align the recognition of taxes with the corresponding revenue and expenses, providing a more accurate representation of the organization’s financial position and performance.

Accounting for Deferred Income Tax

Accounting for deferred income tax involves recognizing and measuring the future tax consequences of temporary differences between financial and taxable income. This process ensures that the organization’s financial statements accurately reflect its tax obligations and potential tax benefits.

When preparing financial statements, organizations are required to calculate their deferred income tax by applying the applicable tax rates to the temporary differences. These temporary differences can arise from various factors, including different depreciation methods, recognition of revenue or expenses at different times for tax and accounting purposes, or the treatment of certain items differently under tax regulations.

Deferred tax liabilities and deferred tax assets are recorded on the balance sheet as non-current assets or liabilities. Deferred tax liabilities represent the future tax obligations resulting from temporary differences that will lead to taxable income in the future. Deferred tax assets, on the other hand, are potential tax benefits that can be realized when there are temporary differences that will lead to deductible expenses or tax credits in the future.

The measurement of deferred income tax is based on the enacted tax rates or rates that are substantively enacted at the balance sheet date. If there are changes in tax rates or tax laws after the reporting date but before the financial statements are issued, the deferred income tax must be adjusted accordingly.

It is important to recognize that deferred income tax is a non-cash item, meaning there is no actual cash inflow or outflow when it is recorded. However, it impacts the organization’s future tax liabilities and benefits, which in turn affect its cash flow when the deferred tax assets are realized or deferred tax liabilities are settled.

Disclosures related to deferred income tax are usually provided in the notes to the financial statements. This includes the significant temporary differences, the applicable tax rates, the opening and closing balances of the deferred tax assets and liabilities, and the changes in these balances during the reporting period.

Overall, accounting for deferred income tax ensures that the organization meets its financial reporting obligations by accurately reflecting its future tax obligations and potential tax benefits. It provides transparency and helps stakeholders understand the organization’s tax position and its impact on financial performance.

Reasons for Deferred Income Tax

Deferred income tax arises due to several reasons, primarily stemming from the differences between tax laws and accounting principles. These differences create temporary timing discrepancies in recognizing revenue, expenses, and assets/liabilities for tax and financial reporting purposes. Understanding the reasons behind deferred income tax is crucial for organizations to accurately reflect their financial position and tax obligations.

One of the main reasons for deferred income tax is the disparity between tax laws and accounting standards. Tax laws are established to generate revenue for governments and may have different rules and rates compared to accounting principles. These differences can be related to the treatment of items such as depreciation, inventory valuation, or revenue recognition, leading to variations in taxable income compared to financial income.

Additionally, variations in the timing of recognizing revenue and expenses for tax and accounting purposes also contribute to the creation of deferred income tax. Tax regulations may require revenue or expenses to be recognized in different periods than accounting standards, resulting in temporary differences and the need to account for future tax consequences.

Companies may also engage in transactions that have tax implications but are not immediately taxable or deductible. For example, the recognition of revenue from a long-term contract or the realization of capital gains from investments may be deferred for tax purposes until a later period, creating temporary differences and the need for deferred income tax accounting.

Temporary differences can also arise due to changes in tax rates or tax laws. When there is a change in tax rates before the financial statements are issued, it may affect the calculation of deferred income tax. Organizations need to adjust their deferred income tax balances to reflect the new tax rates or laws.

Furthermore, international operations and cross-border transactions can lead to deferred income tax due to differences in tax laws and regulations across countries. Companies with global operations must navigate the complexities of international tax systems, which may result in temporary differences and the need for deferred income tax accounting.

Overall, the reasons for deferred income tax are rooted in the differences between tax laws and accounting principles, timing discrepancies in recognizing revenue and expenses, changes in tax rates or laws, and the complexities of international tax systems. Recognizing and accounting for deferred income tax is essential for organizations to provide accurate financial statements that reflect their tax obligations and potential benefits.

Impact of Deferred Income Tax on Financial Statements

Deferred income tax has a significant impact on an organization’s financial statements, affecting key components such as net income, tax expense, and the overall financial position. Understanding this impact is crucial for financial analysis and decision-making by stakeholders.

One of the primary impacts of deferred income tax is on the organization’s net income. Deferred tax liabilities, representing future tax obligations, are recorded as expenses on the income statement. This reduces the net income, reflecting the fact that the organization will have to pay taxes on the temporary differences in future periods. On the other hand, deferred tax assets, representing potential tax benefits, are recognized as income, increasing the net income. The net impact of these deferred tax items on net income depends on the specific circumstances and the balance between deferred tax assets and liabilities.

The impact of deferred income tax on tax expense is also significant. Tax expense is influenced by the changes in the balances of deferred tax assets and liabilities. When there is an increase in deferred tax liabilities or a decrease in deferred tax assets, the tax expense will be higher, as it represents the future tax obligations. Conversely, when there is a decrease in deferred tax liabilities or an increase in deferred tax assets, the tax expense will be lower, reflecting potential tax benefits in the future. Changes in tax laws or rates can also impact tax expense and the balances of deferred tax assets and liabilities.

Deferred income tax also affects the organization’s financial position. Deferred tax liabilities are recorded as non-current liabilities on the balance sheet, representing the future tax obligations. These liabilities reduce the organization’s equity and can impact its overall financial stability. On the other hand, deferred tax assets are recognized as non-current assets, reflecting the potential future tax benefits. These assets contribute to the organization’s overall financial strength and can be utilized to offset future tax liabilities or reduce tax payments.

Additionally, the changes in deferred tax balances can impact cash flow. While deferred income tax is a non-cash item, it influences the organization’s future tax payments or tax savings. When the deferred tax assets are realized or deferred tax liabilities are settled, the cash flow will be impacted accordingly. Understanding the timing and magnitude of these cash flows is important for financial planning and management.

Overall, the impact of deferred income tax on financial statements encompasses net income, tax expense, financial position, and cash flow. Its recognition and measurement provide insights into the organization’s tax obligations and potential benefits. Proper analysis and interpretation of these impacts are essential for stakeholders to assess the financial health of the organization and make informed decisions.

Examples of Deferred Income Tax

To further illustrate the concept of deferred income tax, let’s explore some common examples that demonstrate how temporary differences can arise and impact an organization’s financial statements.

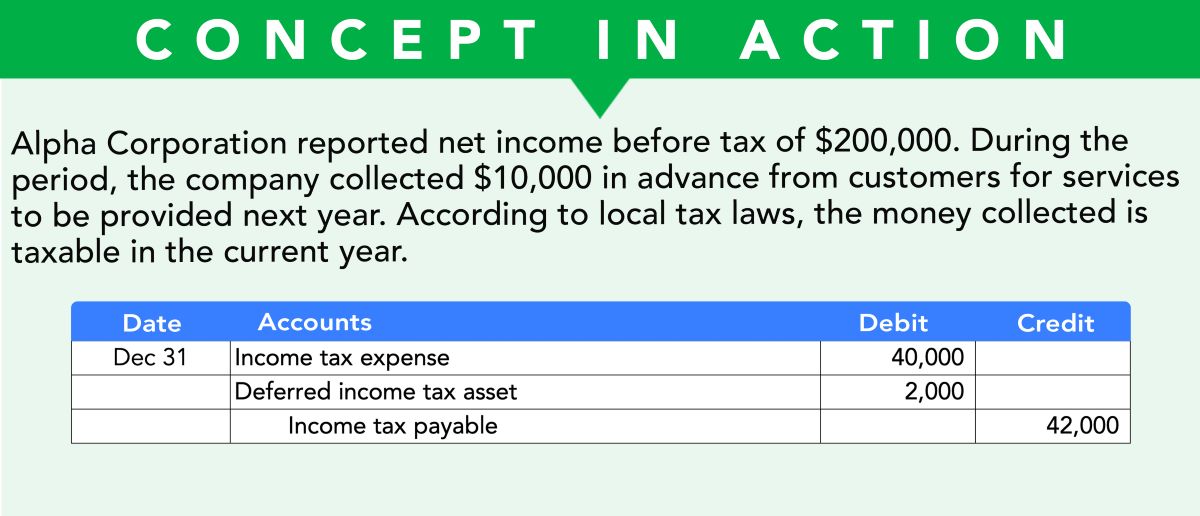

1. Depreciation: Suppose a company uses the straight-line method for financial reporting purposes but follows an accelerated depreciation method for tax purposes. This results in a temporary difference between the depreciation expense recognized on the financial statements and the depreciation expense allowed for tax deduction. The company would need to account for a deferred income tax liability to reflect the future tax that will be payable when the higher depreciation expense is deducted for tax purposes.

2. Revenue Recognition: Consider a situation where a company recognizes revenue upfront for accounting purposes but defers it for tax purposes. This can happen when a company sells goods or services under long-term contracts. The revenue recognized on the financial statements will be higher as compared to the taxable income reported to tax authorities. As a result, the company would record a deferred income tax liability since the tax on the deferred revenue will be paid in the future.

3. Tax Deductible Expenses: Let’s say a company incurs expenses that are deductible for tax purposes in the future, such as research and development costs. The organization can recognize a deferred income tax asset to reflect the future tax benefit it will receive when those expenses are deductible. The asset represents the potential reduction in future tax payments.

4. Business Combinations: In the case of mergers or acquisitions, the acquiring company may inherit assets and liabilities with different tax bases than their carrying values recorded for accounting purposes. This difference creates temporary differences that lead to the recognition of deferred income tax assets or liabilities. The acquirer needs to account for these differences in its financial statements.

5. Net Operating Losses: If a company incurs a net operating loss in one period, it can carry forward that loss to offset future taxable income. This creates a deferred income tax asset, representing the expected future tax benefit. The organization can use this asset to reduce future tax payments when it generates taxable income in subsequent periods.

These examples demonstrate how temporary differences can occur due to different depreciation methods, revenue recognition practices, tax-deductible expenses, business combinations, and net operating losses. Recognizing and accounting for these temporary differences through deferred income tax assets and liabilities allows organizations to accurately reflect their future tax obligations and potential tax benefits.

Importance of Understanding Deferred Income Tax

Understanding deferred income tax is crucial for various stakeholders, including management, investors, creditors, and financial analysts. Here are several reasons why understanding deferred income tax is important:

1. Accurate Financial Reporting: Deferred income tax ensures that financial statements provide a transparent and accurate reflection of an organization’s financial position and performance. By accounting for the future tax consequences of temporary differences, deferred income tax helps align the recognition of taxes with the corresponding revenue and expenses. This accuracy is essential for making informed decisions based on reliable financial information.

2. Tax Planning and Management: Understanding deferred income tax allows organizations to effectively plan and manage their tax obligations. By analyzing the balance between deferred tax assets and liabilities, organizations can evaluate their position and proactively make tax-efficient decisions. It provides insights into potential tax benefits that can be utilized and future tax liabilities that need to be accounted for.

3. Investment Decision-making: Investors and creditors consider the impact of deferred income tax in their decision-making process. By understanding the organization’s future tax obligations and potential tax benefits, stakeholders can assess the financial health and stability of the organization. This knowledge allows them to evaluate the organization’s ability to generate profits and manage its tax burden effectively.

4. Financial Statement Analysis: Financial analysts analyze and interpret an organization’s financial statements to assess its performance and viability. Understanding deferred income tax enables analysts to accurately analyze the organization’s profitability, cash flow, and tax efficiency. It provides valuable insights into the true financial position of the company and helps in making meaningful comparisons with industry peers.

5. Compliance with Accounting Standards: Deferred income tax accounting is a requirement under financial reporting standards, such as Generally Accepted Accounting Principles (GAAP) or International Financial Reporting Standards (IFRS). Organizations must comply with these standards to ensure the credibility and reliability of their financial statements. Understanding deferred income tax enables organizations to meet these compliance obligations.

6. Communication with Stakeholders: Through transparent reporting and disclosures, understanding deferred income tax allows organizations to effectively communicate their tax positions to stakeholders. This includes explaining the impact of deferred income tax on net income, tax expense, and financial position. Clear communication helps build trust and confidence among stakeholders.

7. Tax Compliance: Organizations must comply with tax laws and regulations in the jurisdictions they operate in. Proper understanding of deferred income tax ensures that organizations meet their tax compliance obligations and accurately report their tax liabilities. This reduces the risk of non-compliance penalties and ensures ethical conduct in tax matters.

In summary, understanding deferred income tax is crucial for accurate financial reporting, effective tax planning, informed investment decision-making, compliance with accounting standards, financial analysis, communication with stakeholders, and tax compliance. It enables organizations to provide transparent and reliable financial information, make tax-efficient decisions, and ensure compliance with regulatory requirements.

Conclusion

Deferred income tax is a fundamental concept in finance that has a significant impact on financial statements and tax obligations. It arises from the differences between tax laws and accounting principles, as well as timing discrepancies in recognizing revenue, expenses, and assets/liabilities. Understanding deferred income tax is essential for organizations and stakeholders alike.

Accounting for deferred income tax ensures accurate financial reporting by aligning the recognition of taxes with the corresponding revenue and expenses. It allows organizations to reflect their future tax obligations and potential tax benefits, providing transparency and reliability to financial statements.

The impact of deferred income tax on financial statements extends to key components such as net income, tax expense, and financial position. It affects the organization’s profitability, tax burden, and cash flow. Stakeholders, including investors and creditors, consider this impact when making investment decisions and assessing the financial health of the organization.

Understanding deferred income tax enables organizations to plan and manage their tax obligations effectively. It provides insights into potential tax benefits that can be utilized and future tax liabilities that need to be accounted for. Proper analysis and interpretation of deferred income tax are important for financial planning, compliance with accounting standards, and communication with stakeholders.

In conclusion, deferred income tax plays a crucial role in financial management, providing clarity and accuracy to financial statements, enabling tax planning and decision-making, and ensuring compliance with regulatory requirements. By recognizing and accounting for deferred income tax, organizations can navigate the complexities of taxation, optimize tax advantages, and present a true and transparent picture of their financial position and tax obligations.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance