Finance

What Is Provision For Income Tax

Published: November 2, 2023

Learn about provision for income tax and its implications in finance. Understand how it affects businesses and individuals, and plan your finances accordingly.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

- Introduction

- Definition of Provision for Income Tax

- Purpose and Importance of Provision for Income Tax

- Calculation and Recording of Provision for Income Tax

- Factors Affecting Provision for Income Tax

- Examples of Provision for Income Tax Calculation

- Financial Reporting of Provision for Income Tax

- Conclusion

Introduction

Welcome to our comprehensive guide on provision for income tax. In the realm of finance and accounting, provision for income tax plays a crucial role. It is an essential aspect of financial planning for businesses and individuals alike. Whether you are a business owner or an individual taxpayer, understanding the concept and importance of provision for income tax is essential to effectively manage your finances.

Provision for income tax refers to the estimation of the amount of income tax that will be payable by a business or an individual for a specific accounting period. It is a liability that is recorded in the financial statements and serves as a provision against the future tax liabilities.

The purpose of this provision is to ensure that businesses and individuals set aside an adequate amount of funds throughout the year to fulfill their tax obligations. By estimating the tax liability in advance, it allows for effective financial planning and avoids any last-minute financial burdens.

In this article, we will delve into the definition, calculation, and recording of provision for income tax. We will also explore its purpose, importance, and the factors that can affect its calculation. Additionally, we will provide examples of provision for income tax calculations and discuss how it is reported in financial statements.

Whether you are a business owner or an individual taxpayer, understanding provision for income tax is vital for effective financial management and compliance with tax regulations. So, let’s dive in and explore the world of provision for income tax in detail.

Definition of Provision for Income Tax

Provision for income tax is an accounting concept that refers to the estimated amount of income tax that a business or an individual is expected to pay for a specific accounting period. It is a liability that is recorded in the financial statements to account for the future tax obligations.

When preparing financial statements, it is important to estimate and accrue for the income tax liability that will arise from the profits or income earned during the accounting period. The provision for income tax is calculated based on the applicable tax rates and tax laws.

The provision for income tax is classified as a current liability, as it represents the tax liability that will be payable within one year from the reporting date. It is a legal obligation that businesses and individuals have to fulfill, and accurate estimation of this provision is essential for financial planning and reporting.

It is important to note that the provision for income tax is an estimated amount and may differ from the actual tax liability that will be calculated by the tax authorities. However, by making a reasonable estimate based on the available information and known tax laws, businesses and individuals can ensure that they set aside sufficient funds to cover their tax obligations.

Overall, the provision for income tax is a crucial component of financial reporting and planning, as it reflects the expected tax liability of a business or an individual. By accurately estimating and recording this provision, organizations can provide a true and fair view of their financial position and fulfill their tax obligations in a timely manner.

Purpose and Importance of Provision for Income Tax

The provision for income tax serves several important purposes and plays a pivotal role in financial planning and reporting for both businesses and individuals. Let’s explore the purpose and importance of provision for income tax:

1. Financial Planning: One of the primary purposes of provision for income tax is to facilitate effective financial planning. By estimating and setting aside an amount for future tax obligations, businesses and individuals can ensure that they have sufficient funds to meet their tax liabilities. This allows for better budgeting and allocation of resources.

2. Accurate Financial Statements: Provision for income tax is a crucial component of financial statements. Including this provision ensures that the financial statements present a true and fair view of the financial position and profitability of a business. It is essential for compliance with accounting standards and regulations.

3. Compliance with Tax Regulations: By estimating and recording the provision for income tax, businesses and individuals demonstrate their compliance with tax regulations. It showcases their commitment to fulfilling their tax obligations and helps avoid any penalties or legal issues that may arise from non-compliance.

4. Avoiding Last-Minute Financial Burdens: Estimating and setting aside funds for income tax throughout the accounting period helps businesses and individuals avoid last-minute financial burdens. By spreading the tax liability over time, they can better manage their cash flow and ensure that they have the necessary funds available to meet their tax obligations.

5. Improved Decision-Making: Provision for income tax provides a more accurate picture of a business or individual’s financial position. This information is valuable in making informed financial decisions, such as budgeting, investment planning, and evaluating profitability. It allows for a clearer understanding of the available funds and resources.

6. Transparency and Stakeholder Confidence: Including provision for income tax in financial statements enhances transparency and instills confidence in stakeholders, such as investors, lenders, and tax authorities. It reflects the organization’s commitment to accurate financial reporting and compliance with tax laws.

Overall, provision for income tax is an essential tool for financial planning, accurate financial reporting, compliance with tax regulations, and informed decision-making. It helps businesses and individuals manage their tax obligations effectively and ensures that they are well-prepared to meet their tax liabilities in a timely manner.

Calculation and Recording of Provision for Income Tax

The calculation and recording of the provision for income tax involves several steps and considerations. Let’s explore the process in detail:

1. Determine Taxable Income: The first step in calculating the provision for income tax is determining the taxable income for the accounting period. This involves assessing the financial statements, including income statement and balance sheet, to identify the taxable profits or income.

2. Apply Applicable Tax Rate: Once the taxable income is determined, the next step is to apply the applicable tax rate. The tax rate will be based on the tax laws and regulations of the jurisdiction in which the business or individual operates. It is important to consider any tax incentives, exemptions, or deductions that may be applicable.

3. Consider Tax Planning Strategies: Businesses and individuals may engage in tax planning strategies to minimize their tax liability within the boundaries of the law. This may involve utilizing tax credits, deductions, or structuring transactions in a tax-efficient manner. These strategies should be taken into account when calculating the provision for income tax.

4. Account for Prior Year Adjustments: In some cases, there may be adjustments related to prior years that impact the current provision for income tax. These adjustments should be considered and incorporated into the calculation to ensure accurate and complete provision for income tax.

5. Record the Provision: Once the calculation is complete, the provision for income tax is recorded as a liability on the balance sheet. It is classified as a current liability as it represents the tax liability that will be payable within one year from the reporting date. The provision amount should be disclosed in the financial statements.

6. Review and Update: The provision for income tax should be reviewed and updated regularly to reflect any changes in tax laws, tax rates, or financial circumstances. This ensures that the provision remains accurate and up-to-date.

7. Reconciliation with Actual Tax Liability: At the end of the accounting period, the provision for income tax should be reconciled with the actual tax liability calculated by the tax authorities. Any differences between the provision and the actual liability should be adjusted accordingly in the financial statements.

It is important to note that the calculation and recording of provision for income tax should be done in accordance with accounting standards and tax regulations. Consulting with tax professionals and accounting experts can provide valuable guidance and ensure compliance with applicable rules.

By accurately calculating and recording the provision for income tax, businesses and individuals can effectively manage their tax liabilities and provide transparent financial information in their financial statements.

Factors Affecting Provision for Income Tax

The provision for income tax is influenced by various factors that can impact the calculation and amount of tax liability. These factors should be taken into consideration to ensure an accurate and adequate provision. Let’s explore some of the key factors that can affect the provision for income tax:

1. Taxable Income: The level of taxable income earned by a business or individual is a crucial factor that affects the provision for income tax. Higher levels of taxable income will result in a higher tax liability and, therefore, a higher provision.

2. Changes in Tax Laws: Changes in tax laws and regulations can have a direct impact on the provision for income tax. Alterations in tax rates, deductions, exemptions, or other tax provisions may result in changes to the calculation and amount of the provision.

3. Tax Planning Strategies: Tax planning strategies employed by businesses and individuals can impact the provision for income tax. Utilizing tax credits, deductions, or structuring transactions in a tax-efficient manner can help reduce the tax liability and, consequently, the provision for income tax.

4. Timing of Income and Expenses: The timing of recognizing income and expenses can impact the provision for income tax. Different accounting methods and principles, such as cash basis or accrual basis, may result in different amounts of taxable income and, thus, affect the provision.

5. Tax Incentives and Exemptions: Tax incentives, exemptions, and allowances provided by tax authorities can influence the provision for income tax. Taking advantage of these benefits can lower the tax liability and reduce the provision amount.

6. Changes in Business Circumstances: Changes in the business environment, such as expansion, contraction, or restructuring, can impact the provision for income tax. These changes can alter the profitability of the business and, consequently, affect the amount of taxable income and the provision required.

7. International Tax Considerations: For multinational businesses or individuals with international income sources, international tax considerations can significantly impact the provision for income tax. Double taxation agreements, transfer pricing regulations, and foreign tax credits are some of the factors that should be considered.

8. Assessments and Tax Audits: Assessment notices or tax audits by the authorities can lead to adjustments in the provision for income tax. Any discrepancies or adjustments identified during the assessment process will impact the final tax liability and may require revisions to the provision.

It is important for businesses and individuals to stay informed about these factors and regularly review and update their provision for income tax accordingly. Seeking professional advice from tax experts and accountants can help navigate the complexities of tax regulations and ensure accurate provision calculations.

By considering these factors, businesses and individuals can make informed decisions, manage their tax liabilities effectively, and maintain compliance with tax laws and regulations.

Examples of Provision for Income Tax Calculation

Let’s take a look at some examples to illustrate how the provision for income tax is calculated:

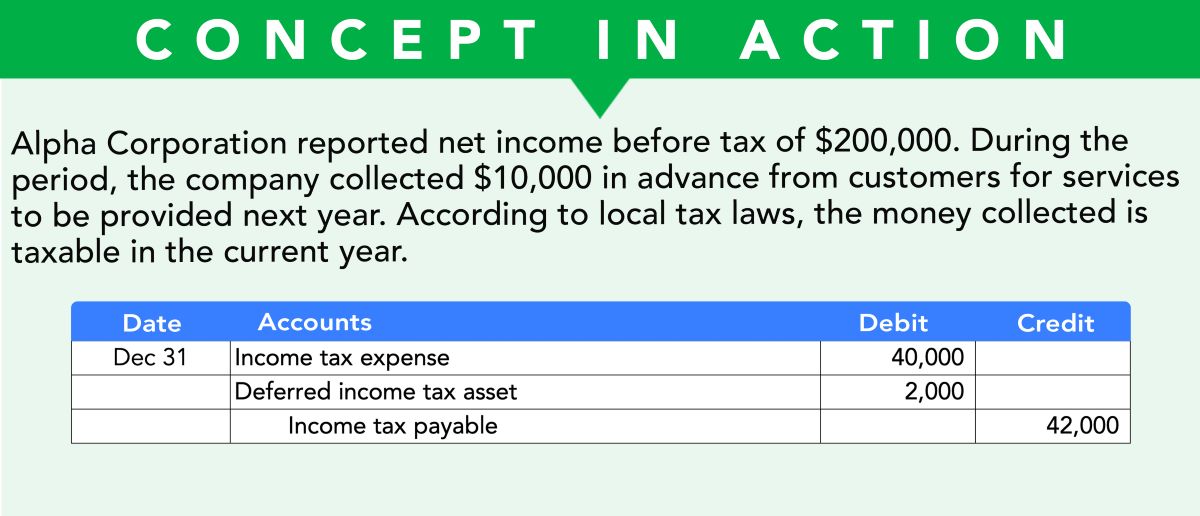

Example 1: ABC Company has taxable income of $500,000 for the year. The applicable tax rate is 25%. To calculate the provision for income tax, we multiply the taxable income by the tax rate:

- Taxable Income: $500,000

- Tax Rate: 25%

- Provision for Income Tax: $500,000 x 25% = $125,000

Therefore, the provision for income tax for ABC Company would be $125,000.

Example 2: XYZ Corporation operates in a jurisdiction with a progressive tax system. The first $100,000 of taxable income is taxed at a rate of 20%, and the remaining income is taxed at a rate of 30%. If the corporation has taxable income of $200,000, the provision for income tax can be calculated as follows:

- Taxable Income: $200,000

- Income up to $100,000: $100,000 x 20% = $20,000

- Income above $100,000: ($200,000 – $100,000) x 30% = $30,000

- Provision for Income Tax: $20,000 + $30,000 = $50,000

Therefore, the provision for income tax for XYZ Corporation would be $50,000.

Example 3: John is a self-employed individual with business income of $80,000. He is eligible for various business deductions, including $5,000 for business expenses. The applicable tax rate is 15%. To calculate John’s provision for income tax, we follow these steps:

- Business Income: $80,000

- Business Deductions: $5,000

- Taxable Income: $80,000 – $5,000 = $75,000

- Tax Rate: 15%

- Provision for Income Tax: $75,000 x 15% = $11,250

Therefore, John’s provision for income tax would be $11,250.

These examples demonstrate the basic calculations involved in determining the provision for income tax. It is important to note that the actual provision amount may vary depending on specific circumstances, applicable tax laws, and any tax planning strategies employed. Engaging with tax professionals and accountants can provide further guidance and ensure accurate provision calculations.

Financial Reporting of Provision for Income Tax

The provision for income tax is an important component of financial reporting and is reflected in the financial statements of businesses and individuals. Let’s explore how the provision for income tax is reported:

1. Balance Sheet: The provision for income tax is recorded as a liability on the balance sheet under the current liabilities section. It represents the amount of tax liability that is expected to be paid within one year from the reporting date. It is important to disclose the provision amount separately to provide transparency in financial reporting.

2. Income Statement: The provision for income tax is not a direct expense but is generally disclosed in the income statement as an item under the tax expense or tax provision section. It represents the estimated tax liability for the accounting period and helps in calculating the net income or loss after tax.

3. Footnotes: In the footnotes to the financial statements, additional disclosure may be provided regarding the provision for income tax. This may include explanations of significant tax positions, changes in tax laws or rates, and any tax planning strategies employed.

4. Disclosures: Apart from the balance sheet and income statement, other disclosures may be required by accounting standards or regulatory authorities. These disclosures may include details about tax incentives, tax credits, deferred tax assets, deferred tax liabilities, and any uncertain tax positions.

5. Tax Return Reconciliation: In some cases, businesses may be required to provide a reconciliation between the provision for income tax recorded in the financial statements and the tax liability calculated on the tax return. This helps in understanding the differences and adjustments made between the financial reporting and tax calculations.

It is important to follow the relevant accounting standards, tax regulations, and disclosure requirements when reporting the provision for income tax. The financial statements should provide a true and fair view of the financial position and profitability, and the provision for income tax is a significant element in achieving this objective.

Furthermore, it is advisable for businesses and individuals to engage with tax professionals and accountants to ensure compliance with reporting requirements and navigate the complexities of tax laws and regulations. They can provide guidance and expertise in accurately reporting the provision for income tax in accordance with the applicable standards and regulations.

By providing transparent and accurate financial reporting of the provision for income tax, businesses and individuals can maintain stakeholder confidence, comply with regulatory requirements, and effectively manage their tax liabilities.

Conclusion

The provision for income tax is a crucial aspect of financial planning and reporting for businesses and individuals. It represents the estimated amount of income tax liability that will be payable for a specific accounting period. By accurately calculating and recording the provision for income tax, organizations and individuals can effectively manage their tax obligations, make informed financial decisions, and maintain compliance with tax regulations.

In this comprehensive guide, we have explored the definition, purpose, and importance of provision for income tax. We have discussed the calculation and recording of provision, considering factors such as taxable income, tax laws, tax planning strategies, and changes in business circumstances. Additionally, we have examined examples of provision for income tax calculations and how it is reported in financial statements.

It is crucial for businesses and individuals to stay updated with tax laws, seek professional advice, and regularly review and update their provision for income tax to ensure accuracy and compliance. By doing so, they can effectively plan their finances, avoid last-minute financial burdens, and provide transparent financial reporting.

Remember, provision for income tax is not only about fulfilling legal obligations but also about effective financial management and accurate financial reporting. By understanding and appropriately managing the provision for income tax, businesses and individuals can achieve financial stability, make informed decisions, and build stakeholder confidence.

We hope this guide has provided valuable insights into provision for income tax and its significance in financial planning and reporting. Consulting with tax professionals and accountants will further enhance your understanding and ensure compliance with relevant regulations. With a solid grasp of provision for income tax, you are now better equipped to navigate the complexities of tax obligations and optimize your financial success.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance