Finance

What Is Endorsement In Banking

Published: October 11, 2023

Learn about endorsement in banking and its significance in the world of finance. Gain insights into the various aspects and implications of endorsement to navigate the banking industry effectively.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

Introduction

When it comes to banking transactions, endorsements play a crucial role. They provide a level of security and validity to financial instruments such as checks or promissory notes. Understanding what endorsement is and how it works in the banking industry is essential for both individuals and businesses.

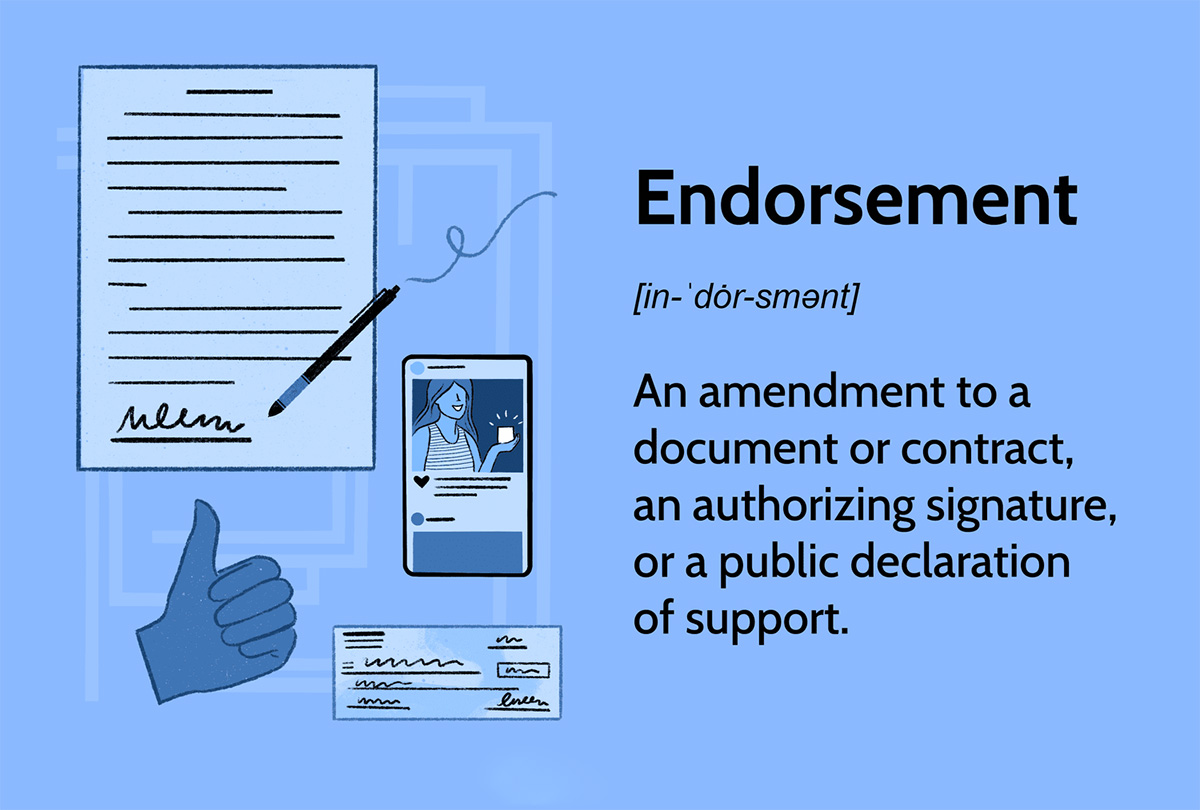

An endorsement, in the context of banking, refers to the act of signing the back of a financial instrument to transfer the ownership rights or to give the authority to another person or entity to negotiate or collect the funds. It serves as a legal authorization for the subsequent party to receive the payment stated on the instrument.

Endorsements come in different types, each serving a specific purpose and offering varying levels of flexibility. The three main types of endorsements are blank endorsement, special endorsement, and restrictive endorsement. Each of these has its own set of requirements and implications.

In the following sections, we will delve deeper into these types of endorsements and explore how they work in banking transactions. We will also discuss the importance of endorsements in ensuring the legitimacy of financial instruments and address some of the legal considerations and potential risks associated with endorsements in the banking industry.

Definition of Endorsement in Banking

In the banking industry, endorsement refers to the process of signing the back of a financial instrument, such as a check, promissory note, or draft, to transfer ownership rights or authorize another party to negotiate or collect funds on behalf of the original payee.

An endorsement serves as a legal and valid authorization for the subsequent party to receive the payment stated on the instrument. By endorsing the instrument, the original payee effectively transfers the rights to the funds to another individual or entity.

Endorsements are typically placed on the back of the financial instrument, although some instruments may have designated areas for endorsements on the front. In most cases, endorsements must be made in ink and include the signature of the endorser, along with any additional instructions or conditions.

It is important to note that endorsements in banking are not limited to just checks or promissory notes. Other financial instruments, such as money orders, traveler’s checks, or even electronic payments, may also require endorsements to ensure the proper transfer of funds.

The purpose of endorsements in banking is to establish a clear chain of ownership and provide a level of security and authenticity to financial transactions. They help prevent unauthorized individuals from accessing and withdrawing funds by requiring proper endorsements for negotiation or collection.

Without a valid endorsement, financial institutions are less likely to accept the instrument or process the transaction. This safeguards the interests of both the payer and the payee by ensuring that only authorized parties have access to the funds specified in the instrument.

Types of Endorsements

In banking, there are three main types of endorsements: blank endorsement, special endorsement, and restrictive endorsement. Each type serves a different purpose and has its own set of requirements and implications.

- Blank Endorsement: A blank endorsement is the simplest and most common type of endorsement. It involves signing the back of the financial instrument without specifying a particular payee. This type of endorsement effectively transforms the instrument into a bearer instrument, meaning that it can be negotiated by anyone who possesses it. Blank endorsements are commonly used for checks that are intended to be cashed or deposited by the bearer. However, it is important to exercise caution when using a blank endorsement as it carries a higher risk of loss or theft.

- Special Endorsement: A special endorsement, also known as an endorsement in full or an endorsement with recourse, is used when the payee wants to transfer the instrument to a specific person or entity. In addition to signing the back of the instrument, the payee must also include the name of the new payee. This type of endorsement restricts the negotiation of the instrument solely to the specified party, providing an added layer of security and control over the funds.

- Restrictive Endorsement: A restrictive endorsement is used when the payee wants to limit the use or negotiation of the instrument. This type of endorsement includes the payee’s signature along with specific instructions or conditions for the instrument’s use. Some common examples of restrictive endorsements include “For Deposit Only” or “Pay to XYZ Bank Only.” Restrictive endorsements help prevent unauthorized parties from cashing or negotiating the instrument and provide an added level of protection against potential fraud.

It is important to choose the appropriate type of endorsement based on the intended purpose and level of control desired. Understanding the implications and limitations of each type is crucial to ensure the proper transfer of funds and to mitigate potential risks associated with improper or unauthorized endorsement.

Blank Endorsement

A blank endorsement is the simplest and most straightforward type of endorsement in banking. It involves signing the back of a financial instrument, such as a check or promissory note, without specifying a particular payee. The endorsement typically consists of the payee’s signature alone, and no additional instructions or conditions are provided.

By using a blank endorsement, the payee effectively transforms the instrument into a bearer instrument. This means that whoever possesses the endorsed instrument can negotiate or collect the funds specified on it. In other words, a blank endorsement allows the instrument to be cashed or deposited by anyone who has physical possession of it.

Blank endorsements are commonly used for checks that are intended to be cashed or deposited by the bearer. For example, when a payee receives a check and does not want to restrict its negotiation to a specific person or entity, they can simply sign the back of the check and leave it blank.

While blank endorsements offer flexibility and ease of use, they also come with a higher risk of loss or theft. Since the instrument becomes payable to the bearer, anyone who comes into possession of the endorsed instrument can potentially access the funds. Therefore, it is crucial to handle checks with blank endorsements with caution and ensure their safe delivery to the intended recipient.

It is worth noting that some financial institutions may have additional safeguards or policies in place when it comes to accepting checks with blank endorsements. For example, they may require identification or verification of the bearer’s relationship to the payee.

If you choose to utilize a blank endorsement, it is essential to keep track of the endorsed instrument until it reaches its intended destination. Additionally, it is recommended to avoid using blank endorsements for high-value checks or sensitive transactions where additional security measures may be necessary.

Overall, a blank endorsement provides flexibility and convenience in the negotiation of financial instruments. However, it is important to be aware of the associated risks and to exercise caution when using this type of endorsement.

Special Endorsement

A special endorsement, also known as an endorsement in full or an endorsement with recourse, is a type of endorsement used in banking to transfer a financial instrument, such as a check or promissory note, to a specific person or entity.

Unlike a blank endorsement, a special endorsement requires the signature of the payee along with the name of the new payee. By including the new payee’s name, the payee designates the specific party to whom they are transferring the rights to the funds stated on the instrument.

Special endorsements provide an extra layer of security and control over the funds. They restrict the negotiation and collection of the instrument solely to the party specified in the endorsement. This means that only the named payee can negotiate the instrument and receive the funds.

For example, if John is the payee of a check and wants to transfer it to his business partner Sam, John would write “Pay to the order of Sam” on the back of the check, along with his signature. This would constitute a special endorsement, effectively transferring the ownership rights to Sam and authorizing him to negotiate the check and receive the funds.

Special endorsements are commonly used in situations where the payee wants to ensure that the instrument is only negotiable by the intended recipient. By specifying the new payee, the payee retains control over who can access the funds and mitigates the risk of unauthorized individuals attempting to cash or deposit the instrument.

Financial institutions generally require special endorsements for certain transactions, such as when depositing checks into business accounts or transferring funds to a third party. By endorsing the instrument with the name of the new payee, the payee provides a clear indication of their intention to transfer the ownership rights and directs the financial institution on how to process the transaction.

It is important to note that special endorsements can only be used once, as they designate a specific party as the new payee. If, for any reason, the intended recipient cannot or does not want to negotiate the instrument, they should not endorse it and should instead return it to the original payee for further action.

Overall, special endorsements offer an added level of control and security in banking transactions. By specifying the new payee, the payee ensures that only the designated party can negotiate the instrument and access the funds.

Restrictive Endorsement

A restrictive endorsement is a type of endorsement used in banking to place specific limitations or conditions on the negotiation or use of a financial instrument, such as a check or promissory note.

When using a restrictive endorsement, the payee signs the back of the instrument and includes specific instructions or conditions for its use. These instructions can vary depending on the desired level of restriction and the purpose of the transaction.

Common examples of restrictive endorsements include statements such as “For Deposit Only,” “Pay to XYZ Bank Only,” or “Account Payee Only.” These endorsements indicate that the instrument can only be deposited into a specific account or that it can only be collected by the named payee.

The purpose of a restrictive endorsement is to prevent unauthorized parties from cashing or negotiating the instrument. By restricting its use, the payee ensures that the funds are used for the intended purpose and reduce the risk of fraud or misuse.

For example, if Jane receives a check payment from a customer and wants to ensure that it is only used for deposit, she can endorse the back of the check with “For Deposit Only.” This restricts the instrument from being cashed and ensures that it is only deposited into her business account.

Financial institutions generally adhere to the instructions provided in a restrictive endorsement. They will only process the instrument according to the specified conditions and ensure that the funds are directed as intended by the payee.

It is important to note that restrictive endorsements may not always be legally enforceable in every jurisdiction. However, they serve as a strong indication of the payee’s intent and are generally respected by financial institutions as a best practice for preventing unauthorized access to funds.

When using a restrictive endorsement, it is crucial to ensure that the instructions are clear and specific. Ambiguous or vague instructions may lead to confusion or delays in processing the instrument, potentially causing inconvenience or complications.

Additionally, it is essential to remember that restrictive endorsements limit the negotiability of the instrument. Any subsequent parties who receive the instrument must adhere to the specified conditions or instructions, providing an additional layer of protection and control for the payee.

Overall, restrictive endorsements offer an effective way to safeguard the use and negotiation of financial instruments. By providing specific instructions or conditions, the payee can ensure that the funds are used for their intended purpose and reduce the risk of unauthorized access or misuse.

How Endorsements Work in Banking

In the banking industry, endorsements play a crucial role in facilitating the transfer of ownership and ensuring the validity of financial instruments such as checks, promissory notes, or drafts.

When a financial instrument is received by the payee, they must endorse the back of the instrument before it can be negotiated or collected. The endorsement typically involves the payee’s signature and, depending on the type of endorsement, may include additional instructions or the name of the new payee.

Once the financial instrument is properly endorsed, it can be presented to a financial institution for processing. The institution will then verify the endorsement, ensuring that it meets the requirements and conditions set forth by the payee and follows the accepted industry standards.

In the case of a blank endorsement, the instrument becomes a bearer instrument, allowing anyone who possesses it to negotiate or collect the funds. This type of endorsement provides maximum flexibility but also carries a higher risk of loss or theft.

On the other hand, special endorsements specify the new payee and restrict the negotiation solely to that designated party. This type of endorsement provides an added layer of security and control over the funds, ensuring they reach the intended recipient.

Restrictive endorsements place limitations or conditions on the use or negotiation of the instrument. These instructions guide the financial institution on how to process the transaction and prevent unauthorized parties from cashing or misusing the instrument.

Once the financial institution verifies the endorsement, it will process the instrument according to the specified conditions. This may involve depositing the funds into the designated recipient’s account, issuing the payment to the named payee, or following any additional instructions provided in the endorsement.

It is important to note that financial institutions have procedures and policies in place to ensure the legitimacy of endorsements. They will carefully scrutinize the endorsement to prevent fraud, unauthorized access, or improper negotiation of the instrument.

Furthermore, in the case of high-value transactions or situations with a higher risk of fraud, financial institutions may request additional documentation or identification to verify the authenticity of the endorsement and the parties involved.

Overall, endorsements in banking serve as a critical mechanism for transferring ownership, ensuring the validity of financial instruments, and protecting the interests of both the payer and the payee. They establish a clear chain of ownership and provide a level of security and confidence in financial transactions.

Importance of Endorsements in Banking

Endorsements play a significant role in the banking industry, serving important purposes that ensure the integrity, legitimacy, and security of financial transactions. Understanding the importance of endorsements is crucial for individuals and businesses alike. Here are some key reasons why endorsements are vital in banking:

- Transfer of Ownership: Endorsements provide a legal mechanism for the transfer of ownership rights in financial instruments. When a payee endorses a check or promissory note, they are effectively transferring the rights to the funds to another individual or entity. This ensures that only authorized parties have access to the funds specified in the instrument.

- Credentialing and Authorization: Endorsements serve as a form of authorization for the subsequent party to negotiate or collect the funds specified on the instrument. Financial institutions rely on valid endorsements to verify the authority of the individual or entity presenting the instrument. In this way, endorsements act as a type of credentialing system, ensuring that only authorized individuals can access the funds.

- Security and Fraud Prevention: Endorsements provide a level of security and prevent fraud in banking transactions. By requiring proper endorsements, financial institutions can verify the authenticity of the instrument and the authority of the party presenting it. This helps mitigate the risk of unauthorized individuals cashing or negotiating the instrument and provides a traceable record of the transaction.

- Clear Chain of Ownership: Endorsements establish a clear chain of ownership for financial instruments. Each endorsement on the instrument’s back serves as evidence of who has possessed and transferred the instrument. This documentation is crucial in tracing the history of the instrument and resolving any disputes that may arise.

- Compliance with Banking Regulations: Endorsements are essential for ensuring compliance with banking regulations and industry standards. Financial institutions are required to follow specific guidelines when accepting and processing endorsed instruments. By adhering to these regulations, institutions uphold the integrity and reliability of the financial system.

Overall, endorsements are of paramount importance in the banking industry. They facilitate the transfer of ownership, provide authorization for fund collection or negotiation, enhance security, establish a clear chain of ownership, and ensure compliance with banking regulations. By understanding and adhering to endorsement requirements, individuals and businesses can protect their financial interests and contribute to the smooth operation of the banking system.

Legal Considerations for Endorsements in Banking

In the realm of banking, endorsements carry legal implications that require careful attention and consideration. Understanding the legal aspects surrounding endorsements is crucial for both individuals and financial institutions. Here are some key legal considerations for endorsements in banking:

- Validity and Authorization: Endorsements must be valid and authorized to be legally recognized. A valid endorsement requires the signature of the payee or endorser. Financial institutions rely on these endorsements to verify the authenticity and authority of the individual or entity presenting the instrument. Without a valid endorsement, the financial institution may decline to honor the transaction.

- Endorsement Liability: Endorsing a financial instrument carries liability for the endorser. This means that the endorser can be held responsible for any breaches or fraudulent activities related to the instrument. It is important to exercise caution when endorsing instruments and to only do so when confident in the legitimacy and authenticity of the transaction.

- Forgery and Fraud: Endorsements are a key area where forgery and fraud can occur in banking. To mitigate these risks, financial institutions have mechanisms in place to detect and prevent fraudulent endorsements. These mechanisms may include signature verification, document examination, and risk assessment procedures. Individuals should also remain vigilant and report any suspicious activity related to their endorsed instruments.

- Proper Endorsement Procedures: It is essential to follow proper endorsement procedures to ensure the validity and legal recognition of the endorsement. Financial institutions may have specific requirements or guidelines for endorsements, such as endorsing in a certain location or using certain language. Failure to meet these requirements may result in the rejection of the instrument or complications in the transaction process.

- Business and Legal Documentation: In certain cases, businesses may need to provide additional legal documentation to support endorsements. This can include documents such as power of attorney, corporate resolutions, or contracts that authorize specific individuals to endorse on behalf of the entity. It is crucial to consult legal professionals to ensure compliance with relevant laws and regulations.

Failure to comply with legal considerations for endorsements can result in financial loss, disputes, legal consequences, or damage to reputation. Therefore, it is essential to understand the legal framework surrounding endorsements and to seek appropriate legal advice when necessary.

By adhering to the legal considerations for endorsements, individuals and financial institutions can uphold the integrity of banking transactions and protect themselves from potential risks and liabilities associated with improper or unauthorized endorsements.

Endorsement Fraud in Banking

Endorsement fraud is a type of fraudulent activity that can occur in the banking industry. It involves the unauthorized or fraudulent endorsement of financial instruments, such as checks, with the intention of illegally accessing or redirecting funds. Understanding the risks and common types of endorsement fraud is crucial for individuals and financial institutions to safeguard against such fraudulent activities.

One common type of endorsement fraud is forged endorsements. This occurs when an unauthorized individual forges the signature of the payee or endorser on a financial instrument. By doing so, the fraudster attempts to present the instrument as if it were properly endorsed and gain access to the funds.

Another type of endorsement fraud is the alteration of endorsements. This involves modifying or tampering with an existing endorsement to change the payee or redirect the funds to a different recipient. Fraudsters may attempt to alter endorsements to divert funds to their own accounts or the accounts of accomplices.

Endorsement fraud can also involve counterfeit endorsements, where fraudsters create fake endorsements to make it appear as if the instrument has been properly endorsed by the authorized party. These counterfeit endorsements can be highly deceptive and difficult to detect without proper scrutiny.

Financial institutions employ various safeguards and fraud detection measures to mitigate the risks associated with endorsement fraud. These include signature verification, document examination, and comparison with authorized endorsement samples. Institutions also leverage technology and advanced security features to detect counterfeit endorsements and fraudulent alterations.

Individuals and businesses can also take steps to protect themselves from endorsement fraud. This includes securely storing financial instruments, safeguarding personal information, and regularly monitoring bank statements and transactions for any unauthorized activity.

If one suspects endorsement fraud or believes they have been a victim of such fraud, it is crucial to report it immediately to their financial institution and follow the necessary steps to minimize financial loss and resolve the issue. Prompt reporting can help initiate investigations and recovery processes, aiding in the prevention of further fraudulent activity.

Endorsement fraud is a serious issue that can result in significant financial loss and legal consequences. Heightened awareness, adherence to proper endorsement procedures, and vigilance can help individuals and financial institutions combat and mitigate the risks associated with endorsement fraud.

Conclusion

Endorsements play a pivotal role in the banking industry, serving as a mechanism for transferring ownership, ensuring the validity of financial instruments, and safeguarding the integrity of transactions. Understanding the different types of endorsements – blank endorsements, special endorsements, and restrictive endorsements – is essential for individuals and businesses engaging in banking transactions.

Blank endorsements provide flexibility and convenience but carry a higher risk of loss or theft. Special endorsements offer an added layer of security by designating a specific party as the new payee, while restrictive endorsements place limitations on the use or negotiation of the instrument to prevent unauthorized access and fraud.

Endorsements are not only important for the smooth flow of financial transactions but also have legal considerations. Understanding the legal framework surrounding endorsements, ensuring proper endorsement procedures are followed, and taking necessary precautions can help individuals and financial institutions avoid fraudulent activities, such as forgery or alteration of endorsements.

Financial institutions have procedures and policies in place to verify the authenticity and authorization of endorsements, protecting the interests of both payers and payees. Compliance with banking regulations is crucial in upholding the integrity and reliability of the financial system.

Endorsement fraud poses a risk in the banking industry, and awareness of its various forms – forged endorsements, altered endorsements, and counterfeit endorsements – is vital. By implementing robust fraud detection measures and promptly reporting any suspected fraudulent activity, individuals and financial institutions can mitigate the risks associated with endorsement fraud.

In conclusion, endorsements are an integral part of banking, facilitating the transfer of ownership, establishing clear chains of ownership, and ensuring the legitimacy of financial instruments. By understanding the importance of endorsements, adhering to proper endorsement procedures, and remaining vigilant against endorsement fraud, individuals and businesses can navigate banking transactions with confidence and security.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance