Home>Finance>What Is A Bank Endorsement? Definition, How It Works, And Types

Finance

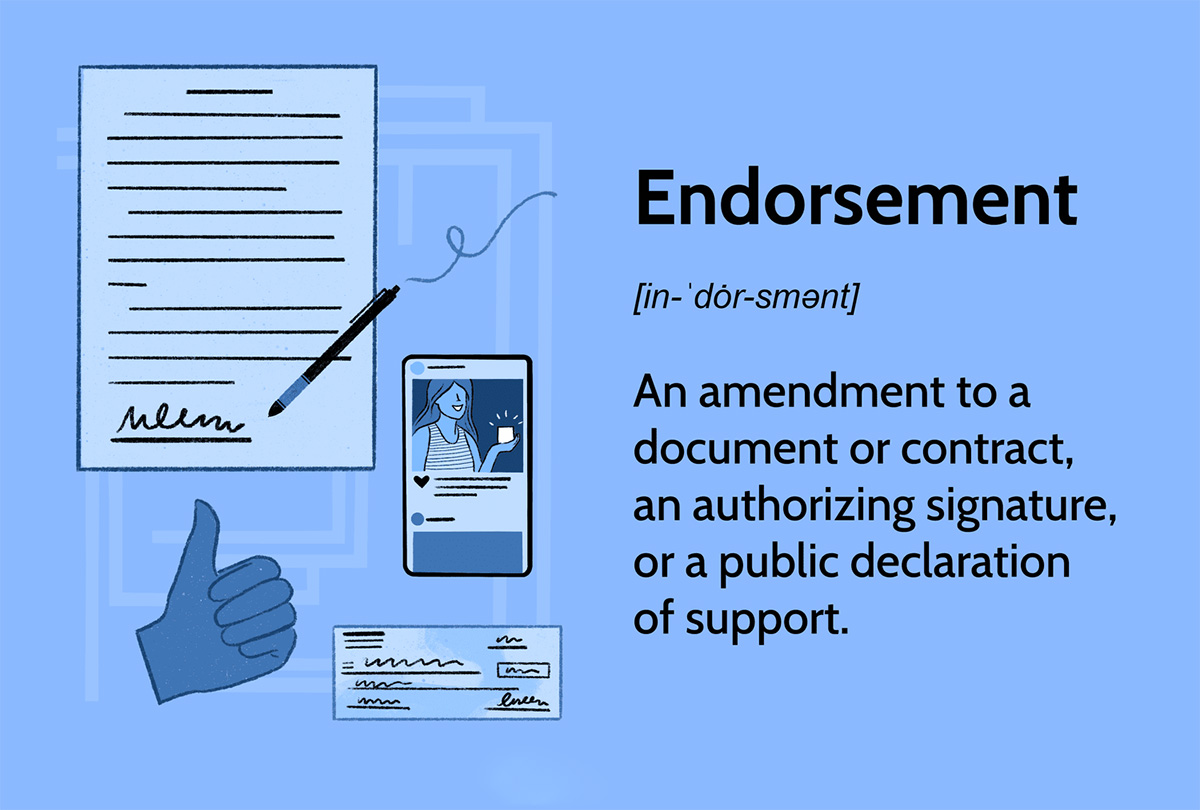

What Is A Bank Endorsement? Definition, How It Works, And Types

Published: October 13, 2023

Learn what a bank endorsement is, its definition, how it works, and the different types available. Discover the importance of endorsements in finance.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Understanding Bank Endorsements: A Guide to How It Works and the Different Types

Welcome to our Finance category where we dive deep into various aspects of banking, investing, and financial management. Today, we’re exploring an essential concept in the banking world: bank endorsements. Whether you’re a seasoned investor or new to the financial landscape, understanding bank endorsements is crucial for managing your finances effectively. In this article, we will define bank endorsements, explore how they work, and discuss the different types of endorsements you may encounter.

Key Takeaways:

- Bank endorsements provide legal authorization for a payee to negotiate or transfer a financial instrument, such as a check or promissory note, to a third party.

- Endorsements ensure the security and validity of financial transactions, protecting both the payer and the payee.

Definition of Bank Endorsements

When someone endorses a financial instrument, they are essentially providing their legal consent or authorization for that instrument to be negotiated or transferred to another party. In the context of banking, an endorsement typically involves a payee signing the back of a check or promissory note, thus indicating their acceptance of the payment and their intention to transfer or deposit it.

Endorsements serve several important purposes:

- Verification: By endorsing a check, the payee verifies that they are the intended recipient of the funds.

- Authorization: Endorsements grant the payee the authority to transfer or deposit the funds.

- Transfer of Ownership: An endorsed financial instrument becomes the property of the endorsee, allowing them to negotiate it further.

Bank endorsements are subject to legal regulations and vary depending on the jurisdiction and financial institution. It is crucial to understand the different types of endorsements to ensure compliance and avoid any potential legal issues.

How Bank Endorsements Work

Let’s say you receive a check as payment for a service you provided. To access the funds and either deposit them into your bank account or transfer them to another party, you must endorse the check. This endorsement can be done in several ways:

- Blank Endorsement: In a blank endorsement, you simply sign the back of the check, making it payable to the bearer or anyone possessing it. Blank endorsements should be done with caution as they essentially transform the check into a bearer instrument, which can be risky if lost or stolen.

- Special Endorsement: If you want to transfer the check to a specific person or entity, you can use a special endorsement. In this case, you sign the back of the check and include a written instruction such as “Pay to the order of [Name].”

- Restrictive Endorsement: A restrictive endorsement limits the further negotiation of the check. For example, if you want to deposit the check into your personal account, you can write “For deposit only” along with your signature.

Remember, different financial institutions may have their own specific requirements for endorsements, so be sure to familiarize yourself with their guidelines to ensure a smooth transaction.

Types of Bank Endorsements

In addition to the common types of endorsements mentioned above, there are a few other variations you may come across:

- Qualified Endorsement: A qualified endorsement includes some condition or limitation, which may affect the validity of the endorsement. For example, stating “Without Recourse” indicates that the endorser is not liable for any potential problems or issues with the instrument.

- Conditional Endorsement: A conditional endorsement includes a specific condition that must be met before the endorsee can negotiate the instrument. Until the condition is fulfilled, the instrument remains non-negotiable.

Understanding these different types of endorsements is crucial for safeguarding your financial interests and complying with banking regulations. Always consult with a financial advisor or banking professional if you have any uncertainties or specific questions regarding bank endorsements.

Bank endorsements play a vital role in ensuring the secure and efficient transfer of funds through negotiable instruments. By familiarizing yourself with the various types and understanding the process involved, you can confidently navigate the world of banking and safeguard your financial transactions.

Remember, bank endorsements are just one aspect of the vast financial landscape, and there is always more to explore. Stay tuned for our future articles where we continue to shed light on essential topics related to finance and banking.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance