Finance

When To File A Tax Return For 2017

Published: October 29, 2023

Learn when and how to file your tax return for the year 2017. Stay on top of your finances and ensure you meet all deadlines.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

Introduction

When it comes to tax season, knowing when to file your tax return is crucial. Filing your taxes on time not only ensures compliance with the law, but it also saves you from late filing penalties and potential auditing risks. If you’re unsure about the tax filing deadlines for the year 2017, this article will provide you with all the information you need.

Understanding the tax filing deadlines is important because it determines when you need to submit your tax return to the Internal Revenue Service (IRS). While the general deadline for filing individual tax returns is April 15th, there are certain circumstances when you may be eligible for an extension. By knowing the deadlines and requirements, you can avoid unnecessary stress and ensure that your tax return is filed accurately and on time.

What constitutes a timely filing for the 2017 tax year can vary depending on your specific situation. It’s important to note that filing requirements and deadlines may change from year to year, so it’s always best to stay up to date with the latest information provided by the IRS.

In this article, we will walk you through the key aspects of filing your tax return for the year 2017. We will cover the filing requirements, income thresholds, important forms and documents, common deductions and credits, special situations for filing, and provide tips for completing your tax return accurately and efficiently.

Whether you are an individual or a business entity, understanding the tax filing deadlines and requirements is essential for a hassle-free tax season. So let’s dive in and explore everything you need to know about filing a tax return for the year 2017.

Understanding Tax Filing Deadlines

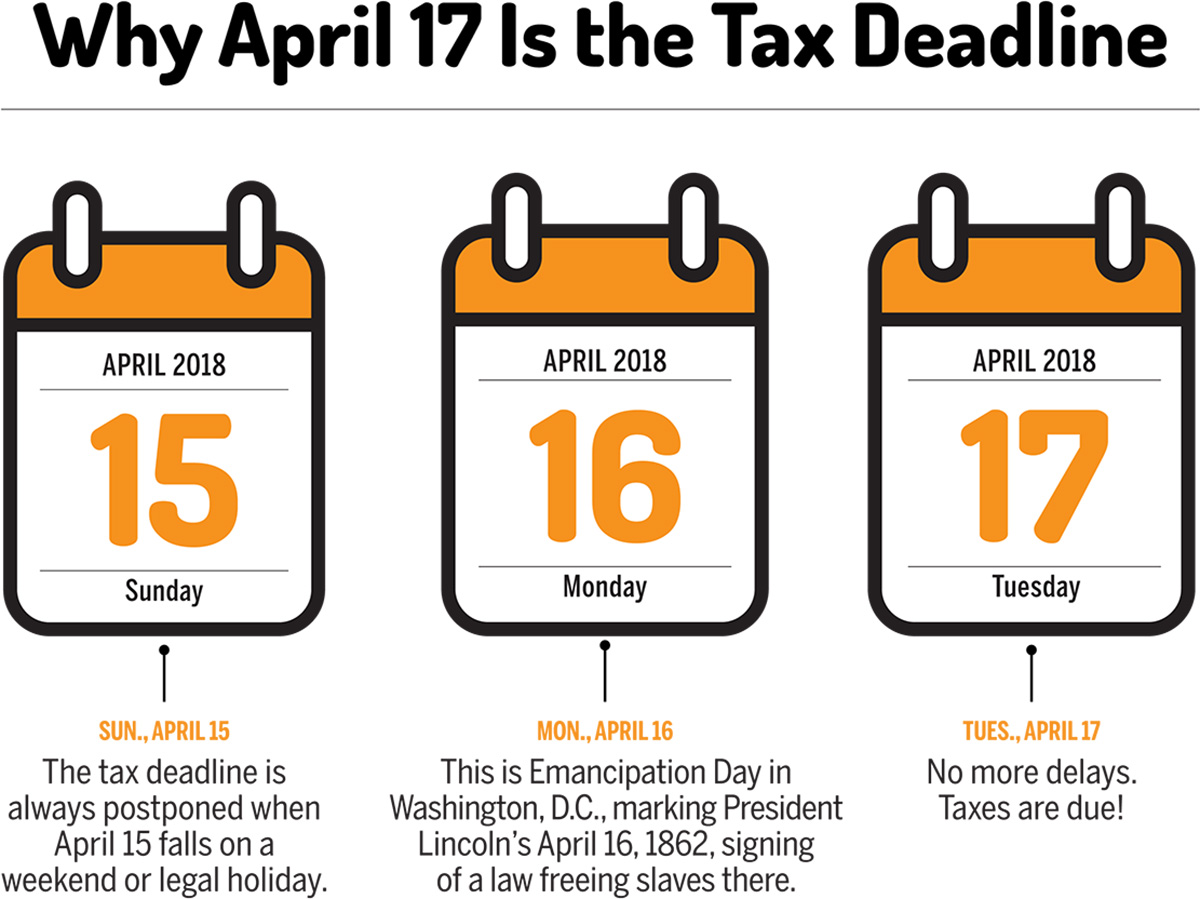

One of the most important factors to consider when filing your tax return is the deadline. The tax filing deadline for the year 2017 generally falls on April 15th. However, if this date falls on a weekend or a holiday, the deadline is usually extended to the next business day.

It’s important to note that there are certain circumstances where you may be eligible for an extension to file your tax return. The IRS provides an automatic six-month extension if you request it before the original deadline. This means that you would have until October 15th to submit your tax return. Keep in mind that while this extension allows you more time to file, it does not extend the deadline for paying any taxes owed. Any taxes owed must still be paid by the original filing deadline to avoid penalties and interest.

If you are living abroad or serving in the military, you may have additional time to file your tax return. The filing deadline for U.S. citizens and resident aliens living abroad is typically June 15th. However, it’s important to note that any taxes owed must still be paid by the original April 15th deadline.

Understanding the tax filing deadlines is crucial as failure to file your tax return on time can result in penalties and interest charges. The penalties for late filing can be significant, amounting to a percentage of the unpaid tax liability. It’s always best to file your tax return as early as possible, even if you are unable to pay the full amount owed. By doing so, you can avoid the late filing penalties and set up a payment plan with the IRS to manage any outstanding tax payments.

Being aware of the tax filing deadlines and any potential extensions is key to ensuring that your tax return is filed accurately and on time. The IRS provides resources on their website, including tax calculators and online filing options, to assist taxpayers in meeting the deadlines. By staying informed and prepared, you can navigate the tax filing process smoothly and avoid any unnecessary stress and penalties.

Filing Requirements for 2017

Understanding the filing requirements for the year 2017 is essential to determine whether you need to file a tax return. The filing requirements set by the IRS are based on factors such as your filing status, age, and income level.

For individuals, the basic filing requirements for the year 2017 are as follows:

- If you are single and under the age of 65, you must file a tax return if your gross income exceeds $10,400.

- If you are single and over the age of 65, the income threshold increases to $11,950.

- If you are married and filing jointly, and both spouses are under the age of 65, the income limit is $20,800.

- If one spouse is over the age of 65, the income threshold increases to $22,050.

- If both spouses are over the age of 65, the income limit is $23,300.

- If you are a head of household, the income threshold is $13,400 for those under 65, and $14,950 for those over 65.

It’s important to note that these income thresholds apply to gross income, which includes wages, tips, self-employment income, rental income, and other sources of income. It’s also worth mentioning that even if your income is below the filing requirement, it may be beneficial to file a tax return to claim any eligible deductions and credits.

Additionally, there are certain situations where you may be required to file a tax return regardless of your income level. For example, if you owe household employment taxes for a nanny or other household employee, you must file a tax return. Similarly, if you received advance payments of the premium tax credit, you are required to file a tax return to reconcile those payments.

If you are self-employed or have income from sources such as freelancing or rental properties, you may need to file a tax return even if your income falls below the filing requirements. The IRS requires self-employed individuals to file a tax return if their net earnings from self-employment income are $400 or more.

It’s important to carefully review the IRS guidelines and consult with a tax professional to determine whether you meet the filing requirements for the year 2017. Filing a tax return accurately and on time ensures compliance with the law and allows you to claim any eligible deductions and credits.

Determining Your Filing Status

When filing your tax return for the year 2017, it’s crucial to determine your correct filing status. Your filing status determines your tax rates, standard deduction, and eligibility for certain credits. There are five filing statuses recognized by the IRS.

- Single: You can file as single if you are unmarried, divorced, or legally separated from your spouse. Generally, you must be unmarried on the last day of the tax year to qualify for this filing status.

- Married Filing Jointly: If you’re married and want to file a joint tax return with your spouse, this filing status is applicable. You and your spouse will combine your incomes and deductions to calculate your taxes.

- Married Filing Separately: If you’re married but prefer to file separate tax returns, you can choose the Married Filing Separately status. Keep in mind that this status may result in a higher tax liability compared to filing jointly.

- Head of Household: To qualify as a head of household, you must be unmarried on the last day of the tax year, provide a home for a qualifying person (such as a dependent), and contribute to more than half of the household expenses.

- Qualifying Widow(er) with Dependent Child: If your spouse passed away within the last two years, and you have a dependent child, you may qualify for this filing status. It provides similar benefits as the Married Filing Jointly status.

Determining your correct filing status is important because it impacts your tax obligations, deductions, and potential credits. It’s essential to choose the filing status that provides the most favorable tax outcome for your situation.

If you are unsure about your filing status, the IRS provides an interactive tool called the “Interactive Tax Assistant” on their website. This tool can help you determine the most appropriate filing status based on your personal circumstances.

Keep in mind that if more than one filing status applies to you, it’s generally beneficial to choose the one that results in the lowest tax liability. However, it’s always wise to consult with a tax professional for personalized advice and guidance based on your specific situation.

By accurately determining your filing status, you can ensure that your tax return reflects your financial circumstances and that you take advantage of any tax breaks or deductions available to you. Understanding your filing status is a crucial step in the tax filing process and can help you maximize your tax savings.

Income Thresholds for Filing

When it comes to filing your tax return for the year 2017, the IRS has set income thresholds that determine whether you are required to file a tax return. These income thresholds vary depending on your filing status, age, and types of income you have.

For single individuals under the age of 65, the filing requirement is generally triggered when their gross income exceeds $10,400. If you are over the age of 65, the income threshold is slightly higher at $11,950. It’s important to note that gross income includes wages, salaries, tips, taxable interest, dividends, and other taxable income.

If you are married and filing jointly, the income threshold for both spouses under the age of 65 is $20,800. If one spouse is over the age of 65, the threshold increases to $22,050. If both spouses are over the age of 65, the threshold is $23,300.

If you are a head of household, the income requirement is $13,400 for those under 65 and $14,950 for those over 65. Head of household status typically applies to individuals who are unmarried but have dependents and contribute to more than half of the household expenses.

It’s important to note that these income thresholds apply to gross income, which is your total income before deducting any expenses or exemptions. The IRS may require you to file a tax return even if your income falls below these thresholds if you received advanced payments of the premium tax credit, owe household employment taxes, or have self-employment income of $400 or more.

It’s worth mentioning that even if you are not required to file a tax return based on these income thresholds, it may still be beneficial to file. Filing a tax return allows you to claim any eligible deductions, credits, or refunds that you may be entitled to, which can help reduce your overall tax liability or provide you with a refund.

It’s important to review the IRS guidelines and consult with a tax professional to determine whether you meet the income thresholds for filing a tax return for the year 2017. Filing your tax return accurately and on time ensures compliance with the law and allows you to take advantage of any potential tax benefits.

Important Forms and Documents

When it comes to filing your tax return for the year 2017, there are several important forms and documents that you will need to gather and submit to the IRS. These forms and documents provide the necessary information to calculate your tax liability accurately and claim any eligible deductions or credits.

Here are some of the key forms and documents you may need:

- Form W-2: This form is provided by your employer and reports your wages, salary, and any taxes withheld from your income. You will receive a separate Form W-2 for each job you held during the tax year.

- Form 1099: There are several variations of Form 1099, including 1099-DIV for dividends, 1099-INT for interest income, and 1099-MISC for miscellaneous income. These forms report income earned from sources other than employment, such as investments, freelance work, and rental income.

- Form 1040: This is the standard individual tax return form. It is used to report your income, deductions, credits, and calculate your tax liability or refund. Depending on your financial situation, you may need to file additional schedules and forms that are attached to Form 1040.

- Social Security Numbers: You will need the Social Security Numbers (SSN) or Individual Taxpayer Identification Numbers (ITIN) for yourself, your spouse (if applicable), and any dependents you are claiming on your tax return. This ensures accurate identification and eligibility for certain tax benefits.

- Receipts and Records: It’s important to keep a record of any expenses, deductions, or credits you plan to claim on your tax return. This includes receipts for charitable contributions, business expenses, medical expenses, and any other eligible deductions. These records provide proof in case of an audit.

- Prior Tax Returns: Having access to your prior year’s tax return can be helpful, especially if you are using tax software or seeking the assistance of a tax professional. It provides valuable information about your filing status, prior deductions, and any carryovers from previous years.

It’s important to note that these are just a few examples of the forms and documents you may need. The specific forms and documents required for your tax return will depend on your individual circumstances, such as your sources of income, eligibility for credits and deductions, and any special situations you may have.

Before you start preparing your tax return, gather all the necessary forms and documents to ensure a smooth and accurate filing process. Keep them organized and easily accessible, as you may need to refer to them throughout the preparation process.

If you are unsure about which forms and documents you need, the IRS website has comprehensive resources and instructions, or you can seek the guidance of a tax professional. Ensuring that you have all the necessary forms and documents in order will help you file your tax return accurately and timely.

Common Deductions and Credits

When filing your tax return for the year 2017, it’s important to be aware of the common deductions and credits that can help reduce your overall tax liability or increase your refund. Deductions and credits are valuable tax breaks that can lower the amount of income that is subject to tax and directly reduce the amount of tax owed.

Here are some of the common deductions and credits that you may be eligible for:

- Standard Deduction: The standard deduction is a set amount that reduces your taxable income. It varies depending on your filing status and is available to all taxpayers. For the tax year 2017, the standard deductions are as follows: $6,350 for single filers, $12,700 for married filing jointly, and $9,350 for head of household.

- Itemized Deductions: Instead of taking the standard deduction, you may choose to itemize your deductions if you have higher deductible expenses. Common itemized deductions include mortgage interest, state and local taxes, medical expenses, charitable contributions, and certain job-related expenses.

- Earned Income Tax Credit (EITC): The EITC is a credit designed to assist low-income individuals and families. It is based on your earned income and the number of qualifying children you have. The credit can significantly reduce your tax liability and may even result in a refund, depending on your income and family size.

- Child Tax Credit: This credit is available to taxpayers with dependent children who are under the age of 17. The credit can reduce your tax liability by up to $1,000 per qualifying child. It is subject to income limitations and is gradually phased out as your income exceeds certain thresholds.

- Education Tax Credits: There are two main education tax credits: the American Opportunity Credit and the Lifetime Learning Credit. These credits can help offset the costs of higher education expenses, such as tuition, fees, and textbooks. They have different eligibility requirements and income limitations.

- Child and Dependent Care Credit: This credit applies to the expenses you paid for the care of your dependent child or a disabled dependent adult. The credit can reduce your tax liability based on a percentage of the expenses, up to certain limits.

These are just a few examples of the common deductions and credits that can be available to taxpayers. It’s important to review the IRS guidelines, consult with a tax professional, or utilize tax software to determine which deductions and credits you qualify for based on your individual circumstances.

By taking advantage of these deductions and credits, you can reduce your tax burden and potentially increase your tax refund. Keep accurate records of your eligible expenses and consult with a tax professional to ensure that you are maximizing your tax savings within the confines of the tax laws.

Special Situations for Filing

When it comes to filing your tax return for the year 2017, there are special situations that may affect your filing requirements or qualify you for certain tax benefits. It’s important to be aware of these special situations to ensure that your tax return is filed accurately and that you are taking advantage of any available tax breaks.

Here are some of the common special situations to consider:

- Self-Employment: If you are self-employed and have income from freelance work, consulting, or running your own business, you will need to file a tax return even if your income falls below the normal filing thresholds. You may also need to pay self-employment taxes on your net earnings.

- Homeownership: If you own a home, you may be eligible for certain deductions and credits. For example, you may be able to deduct your mortgage interest and property taxes if you itemize your deductions. Additionally, if you purchased a home in 2017, you may be eligible for the First-Time Homebuyer Credit.

- Investments: If you have investment income from stocks, bonds, or mutual funds, you will likely receive Form 1099-DIV or Form 1099-INT, which reports the dividends or interest you have earned. It’s important to report this income on your tax return and determine if any tax is owed on these earnings.

- Healthcare Coverage: The Affordable Care Act (ACA) requires most individuals to have qualifying healthcare coverage. If you did not have coverage for the entire year, you may be subject to a penalty unless you qualify for an exemption. You will need to report your coverage on your tax return using Form 1095-A, 1095-B, or 1095-C.

- Residency Abroad: If you lived or worked abroad for part or all of the year, you may have different filing requirements and additional forms to complete. The IRS provides specific guidelines for U.S. citizens or resident aliens living abroad, including special considerations for foreign income and foreign tax credits.

- Disaster Recovery: If you experienced a natural disaster during the tax year that resulted in significant property damage or loss, you may be eligible for certain tax relief. The IRS may provide special provisions and extensions for individuals affected by federally declared disasters.

It’s important to be aware of these special situations and consult with a tax professional or review the IRS guidelines to ensure that you are meeting your tax obligations and taking advantage of any available tax benefits.

Keep in mind that each special situation may have specific requirements, forms, and deadlines associated with it. By understanding your unique circumstances and staying informed, you can navigate these special situations effectively and ensure that your tax return accurately reflects your financial situation.

Tips for Completing Your Tax Return

Filing your tax return for the year 2017 can seem like a complex task, but with careful preparation and attention to detail, it can be a smooth and hassle-free process. Here are some tips to keep in mind while completing your tax return:

- Gather all necessary documents: Before you start, gather all the required forms, documents, and records. This includes W-2s, 1099s, receipts for deductions, and any other relevant paperwork.

- Organize your information: Keep your documents organized and refer to them as you fill out your tax return. Create separate folders for income, deductions, and credits to streamline the process.

- Choose the right filing status: Determine the most appropriate filing status for your situation. Consider the tax implications and eligibility for certain deductions and credits based on your chosen status.

- Review your personal information: Double-check that your personal information, such as your name, Social Security Number, and mailing address, is entered correctly on your tax return to avoid delays or errors.

- Review your math and calculations: Make sure to double-check your calculations and math when completing your tax return to avoid mistakes. Use a calculator or tax software to ensure accuracy.

- Take advantage of tax software: Consider using tax software to simplify the process and ensure accurate calculations. Tax software can help you navigate complex tax situations, deductions, and credits.

- Consider itemizing deductions: Evaluate whether it is more advantageous for you to itemize deductions rather than taking the standard deduction. Compare the amounts to determine the option that reduces your tax liability the most.

- Review tax credits: Familiarize yourself with the available tax credits and determine if you qualify for any. Ensure that you have met all the requirements and gathered the necessary documentation to claim these credits.

- Check for errors and omissions: Carefully review your completed tax return for any errors or omissions. Missing or inaccurate information can lead to processing delays or even an audit. Take the time to review and verify all the information before submission.

- File electronically and choose direct deposit: Choosing to e-file your tax return and opting for direct deposit for any refund can expedite the process and reduce the chance of errors or lost documents.

Remember, it’s always a good idea to consult with a tax professional if you have complex tax situations, are unsure about certain deductions or credits, or need assistance in completing your tax return. They can provide personalized guidance based on your specific circumstances.

By following these tips and taking a proactive approach to your tax return, you can ensure that it is completed accurately and on time, reducing the likelihood of errors, penalties, or audits.

Avoiding Late Filing Penalties

When it comes to filing your tax return for the year 2017, it’s crucial to avoid late filing penalties by submitting your tax return on time. Late filing can result in significant penalties and interest charges imposed by the IRS. Here are some tips to help you avoid these penalties:

- Know the deadlines: Familiarize yourself with the tax filing deadlines for the year 2017. The general deadline for individual tax returns is April 15th, but it may be extended to the next business day if this date falls on a weekend or holiday.

- File an extension if necessary: If you are unable to file your tax return by the deadline, consider filing for an extension. The IRS provides an automatic six-month extension if requested before the original deadline. Keep in mind that an extension only extends the filing deadline, not the deadline for paying any taxes owed.

- Estimate your taxes due: If you anticipate owing taxes, estimate the amount and make a payment by the original filing deadline. This helps minimize penalties and interest charges for late payment while giving you additional time to complete your tax return accurately.

- E-file your tax return: Consider e-filing your tax return rather than mailing a paper return. E-filing is faster, more secure, and allows for quicker confirmation of receipt by the IRS. It also reduces the chances of errors or missing documents.

- Seek professional guidance: If you’re unsure about filing your tax return on time or have complex tax situations, consider seeking the assistance of a tax professional. They can guide you through the process and help ensure that your tax return is filed accurately and timely.

- Keep accurate records: Maintain detailed records of any tax-related documents, such as receipts, W-2s, and 1099s. This will help you complete your tax return accurately and provide documentation in case of an audit.

- Review before submitting: Before submitting your tax return, review it carefully to ensure all necessary information is included, and there are no errors or omissions. Check your math, verify your personal information, and make sure you have properly signed and dated the return.

It’s important to note that late filing penalties can add up quickly. The penalty for filing late is usually 5% of the unpaid tax amount for each month that the return is late, up to a maximum of 25%. If you file more than 60 days after the due date (including extensions), the minimum penalty is either $205 or 100% of the unpaid tax, whichever is less.

Avoiding late filing penalties is crucial to maintaining good tax compliance and avoiding unnecessary financial burdens. By staying organized, planning ahead, and seeking professional assistance when needed, you can ensure that your tax return is filed accurately and on time, minimizing the risk of penalties.

Conclusion

Filing your tax return for the year 2017 can seem like a daunting task, but with the right knowledge and preparation, it can be a manageable and even rewarding process. Understanding the tax filing deadlines, requirements, and special situations is key to ensuring compliance with the law and maximizing your tax benefits.

Throughout this article, we have covered important aspects of filing your tax return for the year 2017. From knowing when to file and understanding the income thresholds for filing, to determining your filing status and identifying common deductions and credits, each step plays a crucial role in submitting an accurate and timely tax return.

Remember, gathering all necessary forms and documents, organizing your information, and double-checking your calculations and math are essential for a smooth filing process. Utilizing tax software and consulting with a tax professional can also provide additional guidance and support.

Avoiding late filing penalties is of utmost importance. Familiarize yourself with the filing deadlines, consider filing for an extension if needed, and ensure that you accurately estimate and pay any taxes owed on time.

By following these guidelines and taking a proactive approach to your tax return, you can navigate the process with confidence and avoid unnecessary stress. Remember to review all the details, check for errors, and keep accurate records for future reference.

As always, it’s advisable to consult with a tax professional who can provide personalized advice based on your specific circumstances. They can help you identify additional deductions and credits, answer your questions, and ensure that your tax return is filed correctly.

By fulfilling your tax obligations and taking advantage of available tax benefits, you can successfully complete your tax return for the year 2017 and move forward with peace of mind. Take the time to educate yourself, stay organized, and approach the process with diligence, and you will be on your way to a successful tax filing experience.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance