Finance

When To File For Tax Return 2015

Published: October 29, 2023

Discover the key deadlines and important dates for filing your 2015 tax return. Stay on top of your finances with expert advice and assistance.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

- Introduction

- Understanding the Tax Filing Deadline

- Determining Your Filing Status

- Gathering Required Documents

- Calculating and Reporting Income

- Deductions and Credits

- Choosing Between Standard Deduction and Itemizing

- Filing Options

- Extensions and Late-Filing Penalties

- Tips for a Smooth Tax Filing Process

- Conclusion

Introduction

Tax season can be a stressful time for many individuals and businesses. It’s a time when financial matters come to the forefront, and everyone must ensure they are in compliance with the tax laws of their respective countries. In this article, we will delve into the topic of filing taxes and provide you with a comprehensive guide on when and how to file your tax return for the year 2015.

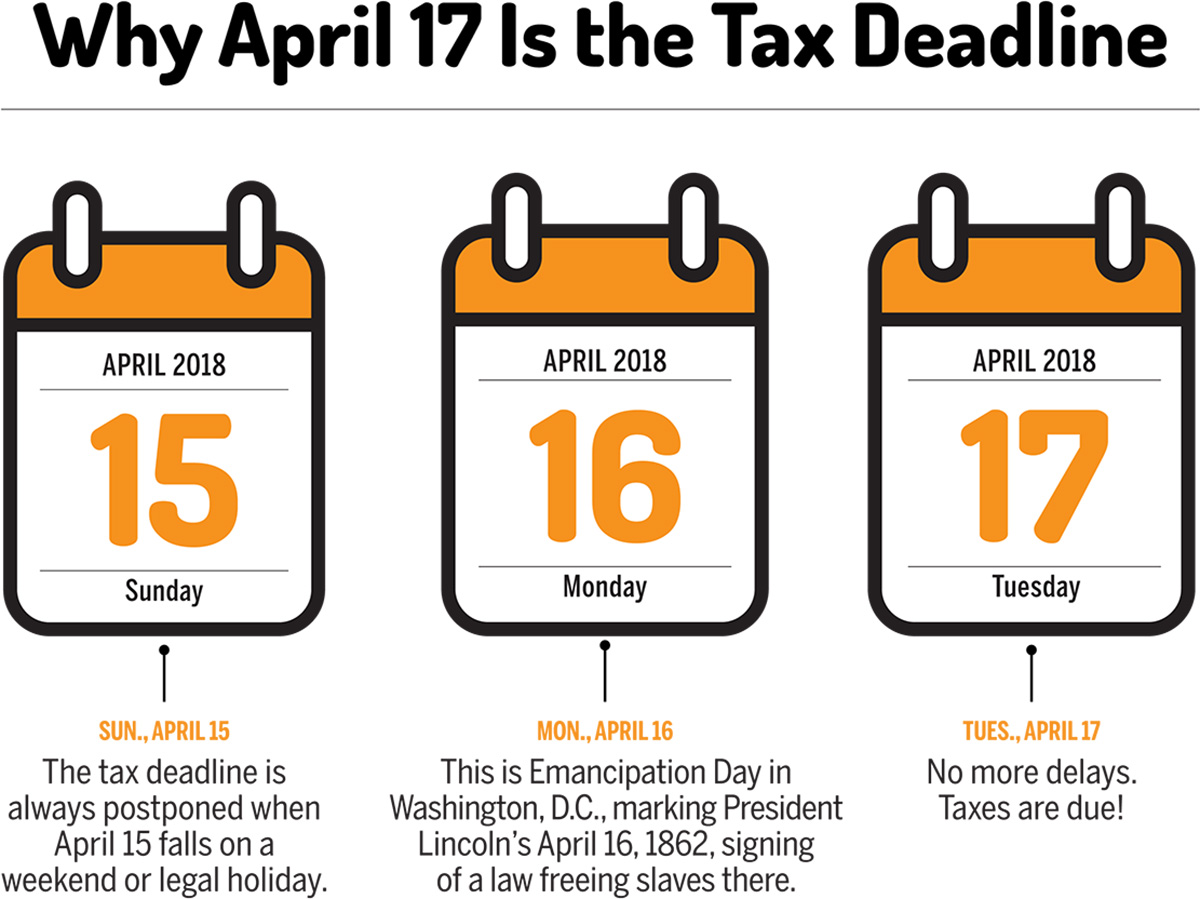

Filing your taxes accurately and on time is crucial to avoid penalties and keep your financial affairs in order. The tax filing deadline for the year 2015 was April 15th, 2016, for most individuals and businesses in the United States. However, it’s essential to note that deadlines may vary depending on your specific tax situation and jurisdiction. It’s always a good idea to consult with a tax professional or refer to the official tax authorities in your country to confirm the precise deadline.

Before diving into the details of filing your tax return for 2015, it’s essential to understand the different factors involved in the process. These factors include determining your filing status, gathering the required documents, calculating and reporting your income, identifying deductions and credits, and ultimately choosing the appropriate filing options.

Whether you are a first-time filer or have been filing taxes for years, understanding the intricacies of the tax filing process and staying updated on the latest tax laws and regulations is essential. In this guide, we will provide you with the necessary information and tips to navigate through the process smoothly.

It’s important to note that this article is intended to provide general guidance and information and should not be considered as professional tax advice. Every individual and business has unique tax circumstances, and it’s recommended to consult with a qualified tax professional to address your specific situation.

Understanding the Tax Filing Deadline

The tax filing deadline is the last day by which individuals and businesses must file their tax returns for a specific tax year. Meeting this deadline is crucial to avoid late filing penalties and interest charges. The tax filing deadline for the year 2015 was April 15th, 2016, for most individuals and businesses in the United States.

It’s important to note that the tax filing deadline may vary depending on your specific tax situation and jurisdiction. Some individuals may qualify for an extension, allowing them to file their taxes later than the initial deadline. Additionally, businesses and certain entities may have different filing deadlines depending on their organizational structure and tax classification.

To determine the exact deadline for your tax filing, it’s recommended to consult with a tax professional or refer to the official tax authorities in your country. They will provide you with accurate information regarding the deadline and any potential extensions or special circumstances that may apply to your tax situation.

It’s crucial to understand the consequences of missing the tax filing deadline. In most cases, if you fail to file your tax return by the deadline, you may incur late filing penalties and interest charges on any tax amount owed. These penalties can vary depending on your jurisdiction and the length of time you delay filing your taxes.

However, if you are due a tax refund, there is generally no penalty for filing your return after the deadline. It’s always recommended to file as soon as possible to receive your refund in a timely manner.

It’s important to note that even if you can’t pay the full tax amount by the deadline, you should still file your tax return to avoid additional penalties. You may be eligible for payment plans or other options to satisfy your tax liability.

In summary, understanding the tax filing deadline is vital to ensure compliance with tax laws and avoid penalties. Be sure to check the specific deadline for your tax situation and file your return on time. If you are unable to meet the deadline, explore options for extensions or consult with a tax professional for guidance.

Determining Your Filing Status

When filing your tax return, one of the first steps is to determine your filing status. Your filing status is used to determine your tax obligations, eligibility for certain deductions and credits, and the tax brackets that apply to you. There are five primary filing statuses: Single, Married Filing Jointly, Married Filing Separately, Head of Household, and Qualifying Widow(er) with Dependent Child.

The Single filing status is typically for individuals who are unmarried, divorced, or legally separated. If you were not married on the last day of the tax year and do not qualify for any other filing status, you will likely file as Single. This status may also apply if you were widowed before the tax year and did not remarry.

Married individuals have two filing options: Married Filing Jointly or Married Filing Separately. Married Filing Jointly is usually the most advantageous option for couples as it allows for potentially lower tax rates and more favorable deductions and credits. Married Filing Separately is chosen when spouses want to keep their finances separate or when specific circumstances require it, but it may result in higher tax rates and limitations on certain deductions and credits.

Head of Household is a filing status available to individuals who are unmarried but have dependents that they financially support. To qualify as Head of Household, you must be unmarried, provide more than half of the financial support for a qualifying dependent, and meet other criteria set by the IRS. This status often offers a more favorable tax rate compared to Single filing status.

Qualifying Widow(er) with Dependent Child is a special filing status available for two years after the year of a spouse’s death if you have a dependent child. It provides some of the benefits of the Married Filing Jointly status and may offer lower tax rates.

Determining your filing status accurately is crucial as it impacts your tax liability and the eligibility for certain deductions and credits. If you are unsure about which filing status applies to you, the IRS provides tools and resources to help you make the correct determination.

It’s important to note that your filing status for the year is determined by your marital status and other factors as of the last day of the tax year. If your situation changes during the year, make sure to select the appropriate filing status for the entire tax year.

Consulting with a tax professional or using tax software can also help ensure you choose the correct filing status and maximize your tax benefits. They will guide you through the process and help you accurately determine your filing status based on your specific circumstances.

Gathering Required Documents

Before you can start preparing your tax return, it’s important to gather all the necessary documents and records. Having these documents on hand will help you accurately report your income, deductions, and credits and ensure that you’re in compliance with tax regulations. Here are some of the key documents you’ll need:

1. W-2 Forms: These forms are provided by your employer and report your annual wages, taxes withheld, and other income-related information. You’ll receive a separate W-2 form from each employer you worked for during the tax year.

2. 1099 Forms: If you received income from sources other than traditional employment, such as freelance work or self-employment, you may receive various 1099 forms. These forms report income you received throughout the year and are used to report different types of income, such as 1099-MISC for miscellaneous income or 1099-INT for interest income.

3. Investment Statements: If you have investments, you’ll need to gather statements from your brokerage or financial institution. These statements provide details about your investment income, including dividends, capital gains, and interest earned.

4. Mortgage Statements: If you own a home, gather your mortgage statements, which will outline any mortgage interest you paid during the year. This information is important for claiming the mortgage interest deduction.

5. Student Loan Statements: If you have student loans, collect your loan statements, which will indicate the amount of interest you paid. This information is necessary for claiming the student loan interest deduction.

6. Receipts for Deductions: If you plan to itemize deductions, be sure to gather receipts and documentation for eligible expenses. This includes receipts for medical expenses, charitable donations, education expenses, and business expenses, among others.

7. Records of Estimated Tax Payments: If you made estimated tax payments throughout the year, keep records of these payments. This will be important for accurately reporting your tax payments and calculating any remaining tax liability.

8. Prior Year Tax Return: Having a copy of your prior year’s tax return can be helpful for reference and to ensure you don’t overlook any carryover items, such as capital losses or unused deductions.

These are just a few examples of the documents you may need when preparing your tax return. It’s important to review the specific requirements of your tax jurisdiction or consult with a tax professional to ensure you have all the necessary documents and records for your situation.

By gathering all the required documents before you start preparing your tax return, you’ll have a smoother and more accurate filing process. It’s also a good idea to keep these documents organized and easily accessible for future reference.

Calculating and Reporting Income

When it comes to filing your tax return, accurately calculating and reporting your income is crucial. Your income is the foundation of your tax liability, and it determines the amount of tax you owe or the refund you may receive. Here are key steps to follow when calculating and reporting your income:

1. Understanding Different Types of Income: Start by identifying the various sources of income you received during the tax year. This may include wages from employment, self-employment income, rental income, investment income, and any other sources of income.

2. Summarizing W-2s and 1099s: Gather your W-2 forms and 1099 forms to determine your total income from employment and other sources. Add up the amounts reported on these forms and ensure that they match your records.

3. Reporting Self-Employment Income: If you’re self-employed or run a business, you’ll need to calculate your business income by subtracting your business expenses from your business revenue. Keep detailed records of your income and expenses associated with your self-employment.

4. Including Other Sources of Income: Report any other types of income you received during the tax year, such as rental income, investment income, or alimony received. Be sure to accurately report all sources of income to ensure compliance with tax regulations.

5. Reporting Deductible Expenses: Some expenses may be deductible, reducing your taxable income. Determine if you qualify for any deductions, such as business expenses, education expenses, or medical expenses. Properly track and document these expenses to support your deduction claims.

6. Calculating Adjustments to Income: Certain deductions, known as adjustments to income, can be claimed even if you don’t itemize deductions. Examples include contributions to traditional IRAs, student loan interest, or self-employment taxes. Calculate and report these adjustments accurately.

7. Considering Tax Credits: Tax credits can directly reduce your tax liability, so it’s crucial to identify any tax credits you may qualify for, such as the Child Tax Credit, Earned Income Tax Credit, or education credits. Make sure to meet the eligibility requirements and properly claim these credits.

8. Utilizing Tax Software or Professional Help: Tax software can assist in calculating and reporting your income accurately. It can guide you through the process and help you identify potential deductions and credits. Alternatively, enlisting the help of a tax professional can ensure precise calculations and minimize errors.

9. Double-Check for Accuracy: Before submitting your tax return, carefully review all income calculations and ensure that everything is accurate and complete. Mistakes or omissions in reporting income can lead to penalties or unnecessary audit risks.

Remember, accurately calculating and reporting your income is crucial to ensure compliance with tax laws and maximize any available deductions and credits. Take the time to carefully review your income sources, seek professional help if needed, and double-check all calculations for accuracy.

Deductions and Credits

When filing your tax return, it’s important to take advantage of deductions and credits that can reduce your taxable income and potentially lower your overall tax liability. Deductions are expenses that can be subtracted from your income to determine your taxable income, while credits directly reduce the amount of tax you owe. Here are some key points to consider when it comes to deductions and credits:

1. Standard Deduction vs. Itemizing: When filing your tax return, you have the option to take the standard deduction or to itemize your deductions. The standard deduction is a fixed amount that reduces your taxable income based on your filing status. Itemizing deductions involves listing and calculating individual eligible expenses, such as mortgage interest, medical expenses, and charitable contributions. Choose the option that allows you to maximize your deductions.

2. Common Deductions: Some common deductions include mortgage interest, state and local taxes, medical expenses, education expenses, and certain business expenses. Keep track of all eligible expenses and gather the necessary documentation to support your deductions.

3. Above-the-Line Deductions: Some deductions, known as above-the-line deductions, can be claimed regardless of whether you itemize your deductions. These include deductions for student loan interest, self-employment taxes, and contributions to retirement accounts.

4. Qualified Business Deductions: If you’re a small business owner or self-employed, you may be eligible for various deductions related to your business. These include deductions for home office expenses, business-related travel and entertainment, and health insurance premiums for self-employed individuals.

5. Tax Credits: Tax credits directly reduce your tax liability, making them highly valuable. Some common tax credits include the Child Tax Credit, Earned Income Tax Credit, American Opportunity Credit for education expenses, and residential energy credits. Research and determine if you qualify for any applicable tax credits.

6. Education Tax Benefits: If you or your dependents are pursuing higher education, there are tax benefits available. The Lifetime Learning Credit, American Opportunity Credit, and the tuition and fees deduction can help offset the costs of education. Research and determine which benefits you may be eligible for.

7. Child and Dependent Care Credit: If you paid for child care expenses to enable you to work or seek employment, you may qualify for the Child and Dependent Care Credit. Keep records of your child care expenses and consult the IRS guidelines to determine your eligibility for the credit.

8. Medical Expense Deductions: Medical expenses that exceed a certain percentage of your adjusted gross income (AGI) may be deductible. Keep track of your medical expenses, including payments for doctor visits, prescriptions, and health insurance premiums.

9. Maximizing Deductions and Credits: To maximize your deductions and credits, keep detailed records of your expenses, maintain proper documentation, and stay informed about changes in tax laws. Utilize tax software or consult with a tax professional to ensure you capitalize on all available deductions and credits.

By understanding and utilizing deductions and credits, you can potentially lower your tax liability and save money. Deductions reduce your taxable income, while credits directly reduce the tax you owe. Take advantage of these opportunities by researching eligible expenses, keeping accurate records, and consulting with tax professionals to ensure you don’t miss out on any potential savings.

Choosing Between Standard Deduction and Itemizing

When filing your tax return, you have the option to take the standard deduction or to itemize your deductions. The choice between these two methods can significantly impact your tax liability. Here’s what you need to consider when deciding between the standard deduction and itemizing:

1. Standard Deduction: The standard deduction is a fixed amount that reduces your taxable income based on your filing status. It is a simplified method to claim deductions without having to calculate and list individual expenses. The standard deduction amount varies each year and is determined by the IRS.

2. Itemized Deductions: Itemizing deductions involves listing and calculating specific expenses that are eligible for deduction, such as mortgage interest, state and local taxes, medical expenses, and charitable contributions. If your itemized deductions exceed the standard deduction amount, it can be advantageous to itemize.

3. Determine Eligible Itemized Deductions: Before deciding whether to itemize, gather all relevant documentation and calculate your potential itemized deductions. This requires maintaining records of eligible expenses, such as receipts, invoices, and statements. Common itemized deductions include mortgage interest, property taxes, medical expenses above a certain threshold, and charitable contributions.

4. Evaluate Personal Financial Situation: Consider your personal financial situation when deciding between the standard deduction and itemizing. Factors such as homeownership, self-employment, high medical expenses, or substantial charitable contributions may make itemizing more beneficial. Conversely, if your eligible deductions do not exceed the standard deduction threshold, it may be more advantageous to take the standard deduction.

5. Consider Time and Effort: Itemizing deductions can be time-consuming and require attention to detail. It involves gathering and organizing documentation, performing calculations, and adhering to IRS guidelines. If your potential itemized deductions are not significantly higher than the standard deduction, it may not be worth the additional time and effort to itemize.

6. Tax Software and Professional Advice: Utilize tax software or consult with a tax professional to evaluate your options and determine which method is best for you. Tax software can automate the comparison between the standard deduction and itemizing, making it easier to make an informed decision. A tax professional can provide personalized advice based on your specific financial situation.

7. State and Local Considerations: It’s important to note that state and local tax laws may have different standard deduction amounts or allow different itemized deductions. Be aware of any specific rules or limitations in your jurisdiction when making your decision.

Remember, the goal is to choose the method that results in the lowest tax liability while remaining in compliance with tax laws. Analyze your financial situation, evaluate your eligible deductions, and consider the time and effort involved in itemizing to determine which approach is most beneficial for you.

Filing Options

When it comes to filing your tax return, you have several options to choose from. Understanding the different filing options available can help you determine the best approach for your specific situation. Here are the primary filing options to consider:

1. Paper Filing: The traditional method of filing your tax return is by mail using paper forms. This involves completing the necessary forms, attaching any required documentation, and mailing them to the appropriate tax authority. While it can be time-consuming and may take longer to process, paper filing allows you to have a physical copy of your return for your records. Ensure that you follow the correct mailing instructions and use certified mail or a tracking service when sending your return.

2. E-Filing: Electronic filing, or e-filing, has become increasingly popular due to its convenience and speed. With e-filing, you can submit your tax return electronically through IRS-approved software or a tax professional. E-filing offers various benefits, including faster processing, built-in error checks, and the ability to receive your refund via direct deposit. Additionally, e-filing reduces the risk of errors and helps ensure accurate calculation of your tax liability.

3. Free File: If you meet certain income requirements, you can take advantage of the Free File program offered by the IRS. Free File allows eligible individuals to use participating software providers to prepare and file their tax return for free. This option is ideal for individuals with simpler tax situations who want to save on the cost of tax preparation.

4. Professional Tax Preparation: If your tax situation is complex or if you prefer professional expertise, hiring a tax professional to prepare and file your return is an option worth considering. Tax professionals, such as certified public accountants (CPAs) or enrolled agents (EAs), have the knowledge and experience to navigate intricate tax scenarios, maximize deductions, and ensure compliance with tax laws. Be prepared to pay for their services, but the potential benefits may outweigh the cost.

5. Online Tax Software: Online tax software platforms, such as TurboTax, H&R Block, or TaxAct, offer a user-friendly and cost-effective way to prepare and e-file your tax return. These platforms provide step-by-step guidance, ask relevant questions, and help you accurately report your income, deductions, and credits. Many online tax software options offer both free and paid versions with varying levels of support and features.

When choosing a filing option, consider factors such as complexity of your tax situation, budget, preference for digital or physical records, and time constraints. It’s important to note that some options may be more suitable for simple tax returns, while others are better suited for more complex tax scenarios.

Regardless of the filing option you choose, ensure that you accurately report your income, deductions, and credits and meet all applicable deadlines. Review your return before submitting to minimize errors, and keep a copy of your filed return for your records.

Remember, the goal of choosing a filing option is to accurately report your tax information, minimize errors, and optimize any potential refunds or deductions. Select the option that best meets your needs and provides the level of assistance and convenience you desire during the tax filing process.

Extensions and Late-Filing Penalties

Life can sometimes get in the way, and meeting the tax filing deadline may not always be possible. If you’re unable to file your tax return by the original due date, you may need to request an extension. Understanding how extensions work and being aware of the potential late-filing penalties is essential. Here’s what you need to know:

1. Requesting an Extension: If you need more time to file your tax return, you can file for an extension using IRS Form 4868 (for U.S. taxpayers) or its equivalent in your tax jurisdiction. Filing for an extension gives you an additional six months to submit your tax return. It’s important to note that an extension applies only to the filing deadline and not the payment of any tax owed.

2. Extension Deadline: The extension deadline is usually October 15th for individual taxpayers in the United States. Ensure that your tax return is filed and any tax owed is paid by this extended due date to avoid penalties. Keep in mind that each tax jurisdiction may have different rules and deadlines, so be sure to check for specific information related to your situation.

3. Late-Filing Penalties: Failing to file your tax return or request an extension by the original due date can result in late-filing penalties. The penalty is typically calculated as a percentage of the unpaid tax owed and accrues each month or part of a month that the return is late. The penalty can be substantial, often starting around 5% of the unpaid tax and increasing each month the return remains unfiled.

4. Late-Payment Penalties: If you owe taxes and fail to pay by the original due date, you may also incur late-payment penalties. These penalties are separate from the late-filing penalties and are calculated as a percentage of the unpaid tax amount. It’s important to note that even if you file for an extension, any tax owed should be paid by the original deadline to avoid late-payment penalties and interest charges.

5. Reasonable Cause Exception: In some circumstances, individuals may be able to avoid or reduce late-filing penalties by demonstrating reasonable cause for the delay. Examples of reasonable cause include situations where the taxpayer experienced a natural disaster, serious illness, or other unforeseen circumstances beyond their control. However, providing proof and documentation to support the reasonable cause can be challenging, so it’s best to consult with a tax professional for guidance.

6. Automatic Extensions for U.S. Taxpayers: In certain situations, taxpayers in the United States may qualify for an automatic extension without filing Form 4868. This applies to individuals living outside the country or serving in the military in a combat zone. The automatic extension typically provides an additional two months to file and pay taxes.

If you find yourself unable to file your tax return by the deadline, it’s important to take appropriate action. Filing for an extension can provide additional time, but be sure to file and pay any tax owed by the extended due date to avoid or minimize late-filing penalties. Consulting with a tax professional can help you navigate the process and ensure compliance with tax regulations.

Remember, it’s crucial to stay informed about the specific rules and deadlines related to extensions and late-filing penalties in your tax jurisdiction. Be proactive in managing your tax obligations to avoid unnecessary penalties and keep your financial affairs in order.

Tips for a Smooth Tax Filing Process

Filing your taxes can seem daunting, but with some preparation and organization, you can make the process go smoothly. Here are some tips to help you navigate the tax filing process:

1. Start Early: Procrastination can lead to unnecessary stress and errors. Start gathering your tax documents and organizing your financial records well in advance of the filing deadline. This will give you sufficient time to review everything, seek professional help if needed, and accurately complete your tax return.

2. Keep Track of Important Deadlines: Mark important tax deadlines on your calendar, including the due date for filing your tax return and any estimated tax payment deadlines. Staying mindful of these dates will ensure that you don’t miss any crucial filings and avoid potential penalties.

3. Stay Organized: Maintain a system to organize your tax documents and records throughout the year. Create folders or use digital storage to store receipts, W-2 forms, 1099 forms, and other relevant documentation. Proper organization will help you avoid missing deductions or credits and make the tax filing process more efficient.

4. Take Advantage of Technology: Utilize tax software or online platforms to streamline the tax preparation process. These tools can guide you through each step, help you calculate your taxes accurately, and identify any missing information. They may also offer features like automatic importation of W-2 and 1099 data, making the process faster and more convenient.

5. Consider Professional Help: If you have a complex tax situation, owning a business, investing in the stock market, or facing other unique circumstances, don’t hesitate to seek professional advice. A tax professional can provide guidance, ensure compliance with tax regulations, and help you maximize deductions and credits.

6. Double-Check for Accuracy: Before submitting your tax return, carefully review all the information entered, calculations, and supporting documents for accuracy. Errors can lead to delays in processing or trigger audits. Take the time to verify that everything is correct to avoid potential problems.

7. Maximize Deductions and Credits: Educate yourself about eligible deductions and tax credits that you may qualify for. Examples include education credits, healthcare expenses, retirement contributions, and energy-efficient home improvements. Take advantage of these opportunities to reduce your taxable income and potentially increase your refund.

8. Keep Copies of Your Tax Return: After filing your tax return, make sure to keep a copy for your records. This will serve as a reference if needed in the future and can help facilitate any necessary amendments or provide proof of compliance.

9. Stay Informed: Keep up-to-date with changes in tax laws and regulations that may affect your filing. Subscribing to tax newsletters, following trusted sources, or consulting a tax professional can help you stay informed and adapt to any adjustments or new requirements.

10. File Electronically and Use Direct Deposit: Consider filing your tax return electronically and opting for direct deposit for any refund due. E-filing is faster, more secure, and reduces the chances of errors. Direct deposit ensures that you receive your refund in the quickest and most convenient way possible.

By following these tips, you can streamline the tax filing process, minimize errors, and potentially maximize your tax benefits. With careful planning, organization, and attention to detail, you can navigate the process with confidence and ensure compliance with tax laws.

Conclusion

Filing your tax return may seem overwhelming, but with a solid understanding of the process and some strategic planning, you can successfully navigate through it. Start by understanding the tax filing deadline and determining your filing status. Gather all the necessary documents and accurately calculate your income, deductions, and credits. Choose between the standard deduction and itemizing based on your specific circumstances. Explore different filing options, such as paper filing, e-filing, or professional tax preparation, to find the most suitable approach for you.

Remember to consider extensions if needed and be aware of potential late-filing penalties. Stay organized, utilize technology, and seek professional advice when necessary. Maximize deductions and credits to optimize your tax benefits, and double-check your tax return for accuracy before submitting it.

Ultimately, staying informed about tax law changes, maintaining good recordkeeping practices, and taking advantage of available resources will contribute to a smoother tax filing process.

By following the tips and guidelines outlined in this article, you can approach tax season with confidence and ensure compliance with tax regulations. Remember, each person’s tax situation is unique, so it’s always wise to consult with a tax professional to address your specific needs and circumstances.

While filing your taxes may not be the most exciting task, it is a necessary part of your financial responsibilities. By giving it the attention it deserves, you can ensure that your tax filing is accurate, timely, and stress-free. So, gather your documents, set aside the necessary time, and get ready to conquer tax season like a pro!

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance