Home>Finance>Which Is Better: Debt Relief Or Debt Consolidation?

Finance

Which Is Better: Debt Relief Or Debt Consolidation?

Published: March 6, 2024

Find out which option is best for your financial situation. Learn the differences between debt relief and debt consolidation to make an informed decision. Get expert advice on managing your finances effectively.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

Introduction

Debt can be a significant source of stress and financial burden for many individuals and families. The weight of multiple debts, high interest rates, and the struggle to make minimum payments can feel overwhelming. In such situations, exploring debt relief and debt consolidation options becomes crucial. Understanding the differences between these two financial strategies is essential for making informed decisions about managing and ultimately eliminating debt.

Debt relief and debt consolidation are two common approaches to addressing debt-related challenges, each with its unique advantages and considerations. Debt relief typically involves negotiating with creditors to reduce the total amount owed or to establish more favorable repayment terms. On the other hand, debt consolidation focuses on combining multiple debts into a single, more manageable loan with a potentially lower interest rate.

As individuals navigate their financial journeys, it's essential to comprehend the intricacies of debt relief and debt consolidation to determine the most suitable path for their specific circumstances. This article delves into the nuances of these approaches, outlining their pros and cons and providing insights to help individuals make well-informed choices regarding their debt management strategies.

Understanding Debt Relief

Debt relief encompasses various strategies aimed at alleviating the burden of overwhelming debt. One common form of debt relief is debt settlement, which involves negotiating with creditors to accept a reduced amount as payment in full, typically in a lump sum. This approach can be beneficial for individuals facing financial hardship, as it allows them to satisfy their debts for less than the total amount owed.

Another form of debt relief is debt management, often facilitated through credit counseling agencies. These organizations work with individuals to create structured repayment plans and negotiate with creditors to lower interest rates and waive fees, making it easier for debtors to manage their obligations. Debt management plans consolidate multiple debts into a single, more manageable monthly payment, providing a structured pathway to becoming debt-free.

Bankruptcy, while considered a last resort, is another form of debt relief that provides legal protection to individuals who are unable to repay their debts. Chapter 7 and Chapter 13 bankruptcies offer different approaches to addressing debt, with Chapter 7 involving the liquidation of assets to discharge debts and Chapter 13 entailing a court-approved repayment plan over a specified period.

It is important to note that debt relief options may have varying impacts on individuals’ credit scores and financial well-being. Debt settlement, for instance, can result in a negative mark on credit reports, albeit temporary, while bankruptcy can have long-term implications. However, for those facing overwhelming debt and financial distress, debt relief options can provide a means to regain control of their finances and work towards a debt-free future.

Understanding Debt Consolidation

Debt consolidation involves combining multiple debts, such as credit card balances, personal loans, or medical bills, into a single, more manageable loan. This approach aims to streamline debt repayment by consolidating various obligations into a single monthly payment, potentially with a lower interest rate. By simplifying the repayment process, debt consolidation can help individuals stay organized and reduce the risk of missing payments.

One common method of debt consolidation is obtaining a consolidation loan, which can be secured or unsecured. A secured loan is backed by collateral, such as a home or other valuable asset, and typically offers lower interest rates. Unsecured consolidation loans, on the other hand, do not require collateral but may have higher interest rates due to the increased risk for lenders.

Another form of debt consolidation involves utilizing balance transfer credit cards, which allow individuals to transfer high-interest credit card balances to a single card with a lower introductory or promotional interest rate. This can provide temporary relief from high interest charges, allowing individuals to focus on paying down their principal balances more effectively.

Additionally, some individuals may opt for debt consolidation through a home equity loan or a home equity line of credit (HELOC), leveraging the equity in their homes to consolidate and pay off existing debts. While this approach can offer lower interest rates, it is essential to consider the potential risks, including the possibility of losing the home if repayment obligations are not met.

Debt consolidation can be an effective tool for simplifying repayment and potentially reducing overall interest costs. By consolidating multiple debts into a single loan or payment, individuals can gain better control over their finances and work towards becoming debt-free more efficiently.

Pros and Cons of Debt Relief

Debt relief offers several potential benefits for individuals struggling with overwhelming debt. One of the primary advantages is the opportunity to negotiate with creditors to reduce the total amount owed. This can result in significant savings for debtors, allowing them to satisfy their obligations for less than the original balances. Debt relief strategies, such as debt settlement and debt management plans, also provide structured pathways for individuals to regain control of their finances and work towards becoming debt-free.

Furthermore, debt relief can alleviate the stress and anxiety associated with unmanageable debt. By establishing more favorable repayment terms, such as lower interest rates or waived fees, debtors can experience reduced financial strain and a clearer path towards financial stability. Debt relief options also offer the potential for consolidating multiple debts into a single, more manageable payment, simplifying the repayment process and reducing the risk of missed payments.

However, it is essential to consider the potential drawbacks of debt relief. One notable disadvantage is the impact on individuals’ credit scores. Debt settlement, for example, can result in negative marks on credit reports, albeit temporary, which may affect individuals’ ability to obtain future credit or loans. Additionally, certain debt relief options, such as bankruptcy, can have long-term implications for individuals’ financial well-being, including limitations on future credit access and potential asset liquidation.

Moreover, debt relief may involve associated fees and costs, particularly when working with debt settlement companies or credit counseling agencies. It is crucial for individuals to carefully evaluate the terms and potential expenses of pursuing debt relief to ensure that the overall benefits outweigh the associated costs.

While debt relief can provide a lifeline for individuals facing overwhelming debt, it is essential to weigh the potential advantages and disadvantages carefully and consider the long-term implications on financial health and creditworthiness.

Pros and Cons of Debt Consolidation

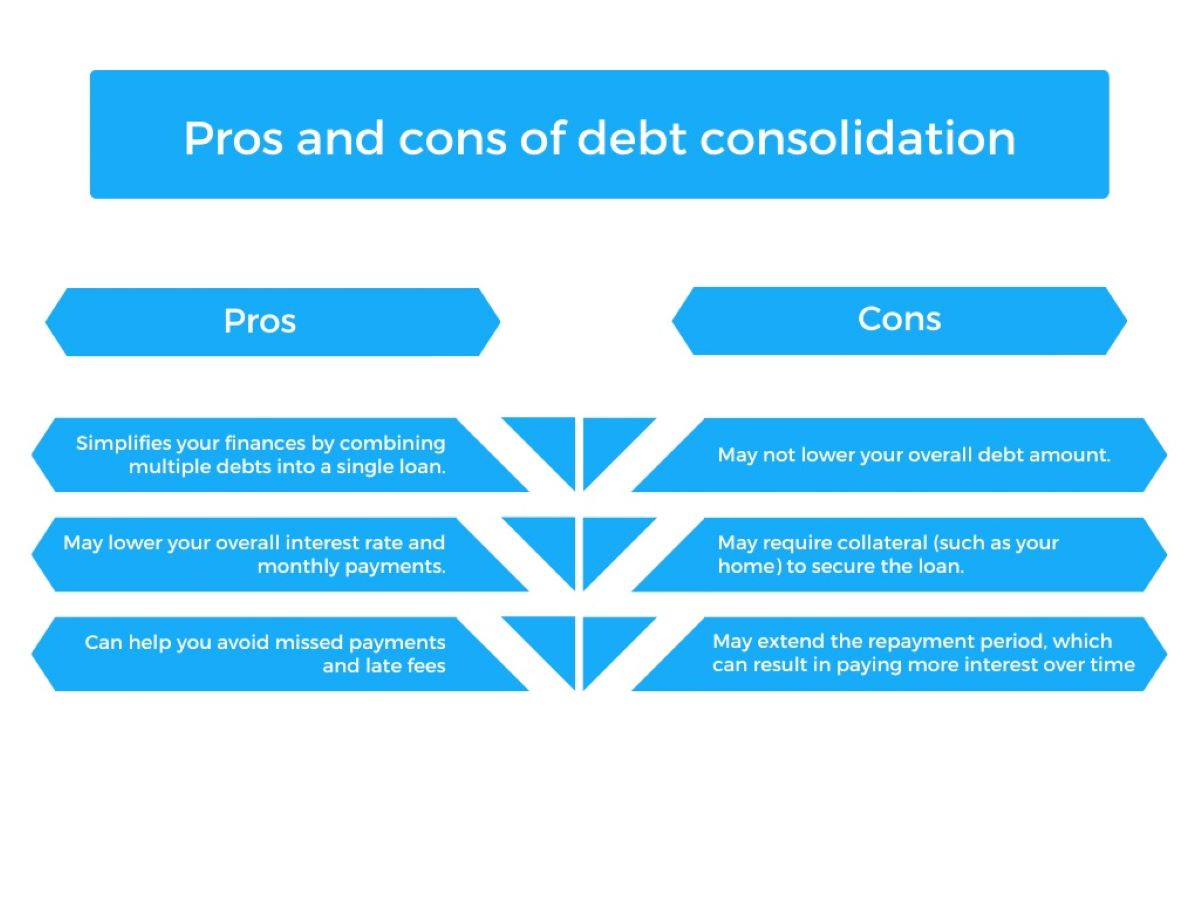

Debt consolidation offers several potential benefits for individuals seeking to streamline their debt repayment and improve their financial management. One of the primary advantages of debt consolidation is the opportunity to combine multiple debts into a single, more manageable loan or payment. This can simplify the repayment process, reduce the risk of missed payments, and provide individuals with a clearer overview of their financial obligations.

Furthermore, debt consolidation can potentially lead to lower overall interest costs. By consolidating high-interest debts into a single loan with a more favorable interest rate, individuals may save money on interest charges over the repayment period. This can result in more efficient debt repayment and potentially faster progress towards becoming debt-free.

Debt consolidation also offers the convenience of a structured repayment plan, providing individuals with a clear timeline for debt elimination. This can reduce the stress and uncertainty associated with managing multiple debts and empower individuals to take control of their financial futures.

However, it is important to consider the potential drawbacks of debt consolidation. One notable disadvantage is the risk of obtaining a consolidation loan with a higher interest rate, particularly for unsecured loans. Individuals must carefully assess the terms and conditions of consolidation loans to ensure that they are securing a more favorable arrangement than their existing debts.

Additionally, some forms of debt consolidation, such as balance transfer credit cards, may involve introductory or promotional interest rates that expire after a specified period. If individuals are unable to pay off their consolidated balances within this timeframe, they may face higher interest charges, potentially negating the initial benefits of consolidation.

Moreover, leveraging assets, such as home equity, for debt consolidation carries the risk of losing the collateral if repayment obligations are not met. It is essential for individuals to weigh the potential consequences of using secured loans or home equity options for debt consolidation and ensure that they are comfortable with the associated risks.

While debt consolidation can offer valuable benefits in simplifying repayment and potentially reducing overall interest costs, individuals must carefully evaluate the terms, risks, and potential long-term implications to determine if it aligns with their financial goals and circumstances.

Which Option is Better for You?

When considering whether debt relief or debt consolidation is the better option for addressing your financial challenges, it’s essential to evaluate your unique circumstances, financial goals, and preferences. Both approaches offer distinct benefits and considerations, and the most suitable option for you depends on various factors, including the nature of your debts, your credit standing, and your long-term financial objectives.

If you are facing overwhelming debt and struggling to meet your financial obligations, debt relief options, such as debt settlement or debt management plans, may offer a lifeline for regaining control of your finances. Debt relief can provide opportunities to negotiate with creditors, reduce the total amount owed, and establish more manageable repayment terms, offering a pathway to becoming debt-free. However, it’s crucial to weigh the potential impact on your credit score and consider any associated fees or costs when pursuing debt relief.

On the other hand, if you have multiple debts with varying interest rates and monthly payments, debt consolidation may be a more suitable option for simplifying your repayment process. By consolidating your debts into a single, more manageable loan or payment, you can streamline your financial obligations and potentially reduce overall interest costs. However, it’s important to carefully assess the terms of consolidation loans and consider the potential risks, particularly when leveraging collateral or assets for consolidation.

When determining the better option for your situation, consider your short-term and long-term financial goals. If your primary focus is on reducing the total amount owed and finding a structured pathway to eliminate debt, debt relief may align more closely with your objectives. Conversely, if you aim to simplify your repayment process, potentially lower your interest costs, and gain a clearer overview of your financial obligations, debt consolidation may be the more favorable choice.

Ultimately, the decision between debt relief and debt consolidation should be based on a comprehensive evaluation of your financial circumstances, preferences, and the potential impacts on your credit and long-term financial well-being. It may also be beneficial to seek guidance from financial advisors or credit counseling professionals to explore the most suitable option for your specific needs.

Conclusion

Managing and overcoming debt challenges requires careful consideration of available options and a thorough understanding of the potential impacts on one’s financial well-being. Debt relief and debt consolidation represent two distinct approaches to addressing debt-related burdens, each offering unique advantages and considerations.

Debt relief, encompassing strategies such as debt settlement, debt management plans, and bankruptcy, provides opportunities for individuals to negotiate with creditors, reduce the total amount owed, and establish more manageable repayment terms. While debt relief can offer a structured pathway to becoming debt-free, it is essential to weigh the potential impact on credit scores, associated fees, and long-term financial implications.

On the other hand, debt consolidation enables individuals to streamline their debt repayment by combining multiple obligations into a single, more manageable loan or payment. This approach can potentially lead to lower overall interest costs and provide a structured repayment plan, offering convenience and clarity in managing financial obligations. However, individuals must carefully assess the terms, risks, and potential consequences of debt consolidation, particularly when leveraging collateral or assets for consolidation.

When determining the most suitable option for addressing debt challenges, individuals should evaluate their unique circumstances, financial goals, and preferences. Whether prioritizing structured debt elimination through debt relief or seeking to simplify repayment and potentially reduce interest costs through debt consolidation, making an informed decision is essential for long-term financial well-being.

Ultimately, seeking guidance from financial advisors, credit counseling professionals, or reputable debt relief and consolidation services can provide valuable insights and support in navigating the complexities of debt management. By understanding the nuances of debt relief and debt consolidation, individuals can make informed choices that align with their financial objectives and pave the way towards a more secure and stable financial future.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance