Home>Finance>Which Is Better Personal Loan Or Debt Consolidation

Finance

Which Is Better Personal Loan Or Debt Consolidation

Modified: December 30, 2023

Discover the pros and cons of personal loans and debt consolidation, and find out which option is best for your financial situation. Get expert advice on managing your finances with Finance.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

Introduction

When faced with financial difficulties, many individuals consider taking out a personal loan or exploring debt consolidation as potential solutions. Both options offer unique benefits and considerations. Understanding the differences between a personal loan and debt consolidation can help you make an informed decision based on your specific financial situation.

A personal loan is a type of loan that allows you to borrow money for various purposes, such as funding a major purchase, covering unexpected expenses, or consolidating existing debts. On the other hand, debt consolidation involves combining multiple debts into a single loan, typically with a lower interest rate and more manageable repayment terms.

Choosing between a personal loan and debt consolidation requires a careful evaluation of your financial needs, goals, and circumstances. By considering factors such as interest rates, repayment terms, fees, and your credit score, you can determine which option is the better fit for your situation.

Throughout this article, we will delve into the specifics of personal loans and debt consolidation, outlining their key features, benefits, drawbacks, and factors to consider. By the end, you will have a comprehensive understanding of both options, allowing you to make an informed decision regarding your financial future.

Personal Loan

A personal loan is a type of unsecured loan that can be used for a variety of purposes. It provides individuals with access to funds that can be used to address immediate financial needs or fulfill long-term goals. Unlike a mortgage or auto loan, a personal loan does not require collateral, making it a popular choice for many borrowers.

Personal loans typically have fixed interest rates and repayment terms ranging from one to seven years, depending on the lender and the borrower’s creditworthiness. The loan amount can vary depending on factors such as income, credit score, and repayment capacity.

One of the main advantages of a personal loan is its versatility. Borrowers can use the funds for a wide range of purposes, including debt consolidation, home improvements, medical expenses, vacations, or even starting a small business. The flexibility and freedom associated with personal loans make them an attractive option for many individuals.

The application process for a personal loan is relatively straightforward. Borrowers are required to fill out an application, provide documentation such as proof of income and identification, and undergo a credit check. Once approved, the loan funds are disbursed, and borrowers can start using them according to their needs.

While personal loans offer numerous benefits, there are some drawbacks to consider. One factor to be aware of is the interest rate. Personal loans can come with higher interest rates compared to other types of secured loans. Additionally, borrowers with poor credit may face difficulty in getting approved or may be subjected to higher interest rates.

Despite these potential drawbacks, a personal loan can be an excellent option for those looking for quick access to funds without offering collateral. Whether you need to consolidate debts, make a large purchase, or cover unexpected expenses, a personal loan can provide the financial backing you need to achieve your goals.

Debt Consolidation

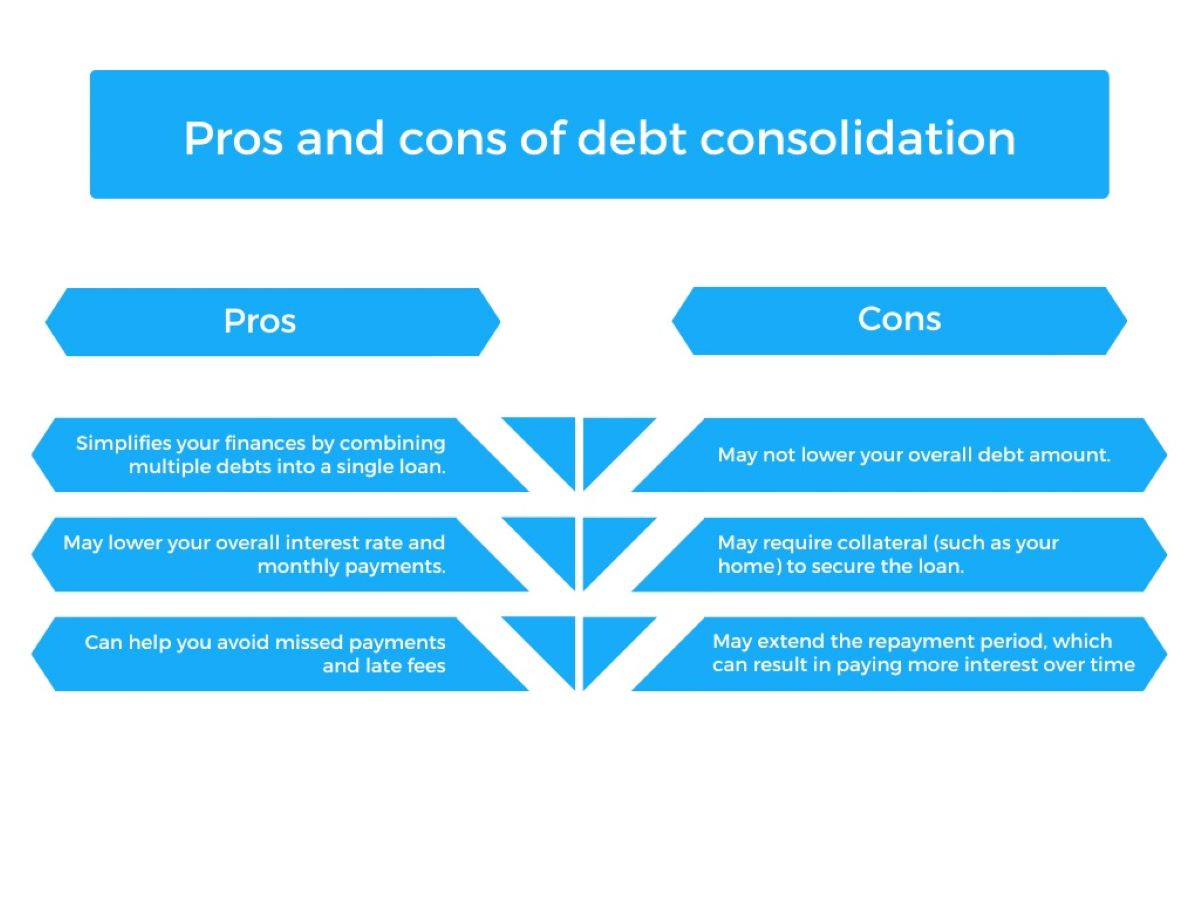

Debt consolidation involves combining multiple debts into a single loan, typically with a lower interest rate and more structured repayment terms. This approach is popular among individuals who are struggling to manage multiple debts and want to simplify their financial obligations.

By consolidating debts, borrowers can streamline their payments and potentially save money on interest charges. Instead of making multiple payments to different creditors each month, a debt consolidation loan allows borrowers to make a single monthly payment to their new lender. This can make budgeting and managing finances much easier.

In addition to the convenience of a single payment, debt consolidation loans often come with lower interest rates compared to credit cards or other high-interest loans. By taking advantage of a lower interest rate, borrowers can potentially save a significant amount of money over the life of the loan.

Another advantage of debt consolidation is that it can help improve your credit score. By consolidating debts and making regular, on-time payments, borrowers can demonstrate a responsible approach to managing their finances. This can have a positive impact on their credit history and score.

It’s important to note that debt consolidation may not be the right solution for everyone. Before opting for a debt consolidation loan, borrowers should carefully consider their financial situation and repayment capacity. It’s crucial to ensure that the new loan terms are affordable and that there won’t be any additional financial strain.

Some potential drawbacks of debt consolidation include the possibility of longer loan terms, which could mean paying more interest over time. Additionally, if borrowers do not address the underlying issues that led to their debt accumulation, they may find themselves in a similar situation in the future.

In summary, debt consolidation can be a valuable tool for individuals looking to simplify their finances and potentially save money on interest charges. However, it’s essential to carefully consider the terms, affordability, and potential long-term impact before pursuing a debt consolidation loan.

Factors to Consider

When deciding between a personal loan and debt consolidation, there are several important factors to consider. Taking the time to evaluate these factors can help you make an informed decision that aligns with your financial goals and circumstances.

1. Interest Rates: Compare the interest rates offered for personal loans and debt consolidation loans. Look for the option that provides the most favorable interest rate, as this will directly impact the overall cost of the loan.

2. Repayment Terms: Evaluate the repayment terms of both options. Consider whether you prefer a shorter repayment period with higher monthly payments or a longer term that allows for more affordable monthly installments.

3. Total Cost: Calculate the total cost of each option by taking into account the interest rates, fees, and any additional charges associated with the loan. This will give you a clear understanding of the overall financial implications of each option.

4. Credit Score: Assess your credit score and credit history. Personal loans may require a higher credit score for approval, whereas debt consolidation loans may be more lenient. Understanding your creditworthiness will help determine which option is more feasible for you.

5. Financial Goals: Consider your financial goals and priorities. If your primary objective is to simplify your debts and improve your financial management, debt consolidation may be the better choice. However, if you have specific needs or goals that require a lump sum of money, a personal loan may be more suitable.

6. Debt Situation: Evaluate the nature and amount of your existing debts. If you have multiple high-interest debts, debt consolidation can help save money on interest charges. On the other hand, if you have a single large expense, a personal loan may be more appropriate.

7. Loan Amount: Determine the loan amount you require. Some lenders may have borrowing limits, so ensure that the option you choose can provide the necessary funds to meet your needs.

By considering these factors, you can make a well-informed decision that takes into account your financial situation, goals, and preferences. It’s important to weigh the advantages and disadvantages of each option to find the one that best fits your needs.

Pros and Cons

Both personal loans and debt consolidation have their advantages and disadvantages. Understanding the pros and cons of each option can help you make an informed decision based on your specific financial needs and goals.

Pros of Personal Loans:

- Flexibility: Personal loans can be used for a variety of purposes, providing borrowers with the freedom to address different financial needs.

- Quick Access to Funds: Personal loans often have a straightforward application process and can provide funds relatively quickly, making them suitable for urgent financial situations.

- No Collateral Required: Personal loans are typically unsecured, meaning you don’t have to put any assets at risk as collateral.

- Improvement of Credit Score: Making regular, on-time payments towards a personal loan can help improve your credit score over time.

Cons of Personal Loans:

- Higher Interest Rates: Personal loans often come with higher interest rates compared to secured loans, which can increase the overall cost of borrowing.

- Approval Criteria: Lenders may have strict approval criteria, including credit score requirements, which could potentially limit your eligibility.

- Potential Debt Accumulation: If not used responsibly, taking out a personal loan could lead to increased debt and financial strain.

Pros of Debt Consolidation:

- Simplified Finances: Combining multiple debts into a single loan makes it easier to manage your finances, as you only have one monthly payment to worry about.

- Potential Savings on Interest: Debt consolidation loans often come with lower interest rates than credit cards or other high-interest loans, potentially saving you money in the long run.

- Improved Credit Score: Consistently making on-time payments towards a debt consolidation loan can positively impact your credit history and score.

Cons of Debt Consolidation:

- Extended Loan Terms: Debt consolidation loans may have longer repayment terms, resulting in more interest being paid over time.

- Need for Financial Discipline: Debt consolidation is not a solution for overspending or financial mismanagement. Without addressing the root causes of debt accumulation, borrowers may find themselves in a similar situation in the future.

- Possible Fees and Charges: Some debt consolidation loans may come with fees and charges, so it’s important to carefully review the terms and conditions before proceeding.

Considering these pros and cons will help you weigh the advantages and disadvantages of personal loans and debt consolidation, enabling you to make a well-informed decision based on your unique financial circumstances.

Conclusion

Choosing between a personal loan and debt consolidation requires careful consideration of your financial situation, goals, and priorities. Both options offer unique benefits and drawbacks that can impact your decision-making process.

A personal loan provides flexibility and quick access to funds for various purposes. It can be an excellent option for those needing immediate financial assistance or funding for specific endeavors. However, higher interest rates and strict approval criteria may be potential drawbacks to keep in mind.

Debt consolidation, on the other hand, simplifies your finances and potentially saves money on interest charges. It can be a valuable tool for individuals struggling to manage multiple debts. However, longer loan terms and the need for financial discipline must be considered.

To make a well-informed decision, evaluate factors such as interest rates, repayment terms, total cost, credit score, financial goals, debt situation, and loan amount. By considering these factors, you can align your choice with your specific needs and circumstances.

In the end, it’s crucial to remember that both personal loans and debt consolidation should be utilized responsibly. Understand the terms, weigh the pros and cons, and assess your ability to meet the repayment obligations before committing to any financial solution.

Whether you opt for a personal loan or debt consolidation, the key is to take control of your finances and take steps towards achieving your financial goals. Make your choice wisely, create a realistic budget,and maintain discipline in managing your debts. By doing so, you can pave the way towards a brighter and more stable financial future.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance