Home>Finance>Which Is Better: Debt Relief Or Debt Consolidation

Finance

Which Is Better: Debt Relief Or Debt Consolidation

Published: December 21, 2023

Discover the best financial solution for your debt with this comparison of debt relief and debt consolidation. Find out which option is more suitable for your financial needs.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

Introduction

Dealing with overwhelming debt can be a stressful and challenging experience. It can feel like a never-ending cycle of late payments, high interest rates, and constant creditor calls. However, there are options available to help you regain control of your finances. Two popular solutions are debt relief and debt consolidation.

In this article, we will explore the differences between debt relief and debt consolidation, the pros and cons of each approach, and the factors to consider when deciding which option is best for you. By understanding these options, you can make an informed decision about how to tackle your debt and work towards a brighter financial future.

Debt relief refers to a strategy that aims to reduce your overall debt amount through negotiations with your creditors. It typically involves working with a debt relief agency or a professional who specializes in negotiating with creditors on your behalf. The goal of debt relief is to reach a settlement with your creditors, allowing you to pay off your debt for less than what you owe.

On the other hand, debt consolidation involves combining multiple debts into a single, unified loan. This loan usually comes with a lower interest rate and a structured repayment plan. Instead of dealing with multiple creditors and due dates, you make a single monthly payment towards the consolidation loan. Debt consolidation aims to simplify your debt management and potentially save you money on interest payments.

Both debt relief and debt consolidation have their advantages and considerations. The choice between the two depends on your specific financial situation, the amount of debt you have, and your long-term goals. Let’s take a closer look at the pros and cons of each approach to help you make an informed decision.

Understanding Debt Relief

Debt relief is a strategy that aims to alleviate the burden of debt by working with creditors to negotiate a reduction in the total amount owed. This approach is typically utilized when individuals or businesses find themselves unable to make regular payments and are at risk of defaulting on their loans.

There are several methods of debt relief, including debt settlement, debt management programs, and bankruptcy. Debt settlement involves negotiating with creditors to lower the outstanding balance in exchange for a lump sum payment or a structured repayment plan. Debt management programs, on the other hand, involve working with a credit counseling agency to establish a manageable payment plan and potentially reduce interest rates. Bankruptcy is a legal process that can provide relief by liquidating assets or restructuring debts.

When considering debt relief, it is essential to understand its consequences and potential impact on your credit score. Debt settlement, for example, may have a negative effect on your credit score, as it involves not paying the full amount owed. It can also result in tax implications, as forgiven debt may be considered taxable income by the IRS.

Working with a reputable debt relief agency or professional can help navigate the complexities of the process and ensure the best possible outcome. They will communicate and negotiate with creditors on your behalf, aiming to reduce your overall debt and provide you with a clear roadmap to financial recovery.

It is important to note that debt relief is not a one-size-fits-all solution. Each individual’s financial circumstances and level of debt will determine the most suitable approach. If you are considering debt relief, it is advisable to consult with a financial professional who can assess your situation and guide you toward the most appropriate course of action.

Pros and Cons of Debt Relief

Debt relief can provide a lifeline to individuals and businesses struggling with overwhelming debt. However, like any financial strategy, it comes with its own set of advantages and considerations. Let’s explore the pros and cons of debt relief to help you make an informed decision:

Pros of Debt Relief:

- Reduced Debt Amount: One of the primary benefits of debt relief is the potential to reduce the total amount owed. Through negotiations with creditors, debt relief professionals can help you reach a settlement that is less than what you owe.

- Manageable Payments: Debt relief can provide you with a structured repayment plan that fits your financial situation. This allows you to make more manageable monthly payments, easing the burden of high debt obligations.

- Professional Assistance: Working with a debt relief agency or professional provides you with expert guidance and support throughout the process. They have the knowledge and experience to negotiate with creditors on your behalf and ensure that your best interests are represented.

- Debt Resolution Timeline: Debt relief strategies often have specific timelines for resolution. This means that you can have a clear understanding of when you can expect to become debt-free, providing you with a sense of control and a light at the end of the tunnel.

Cons of Debt Relief:

- Negative Impact on Credit: Debt relief strategies, especially debt settlement, can have a negative impact on your credit score. This is because they involve not paying the full amount owed, which is viewed unfavorably by creditors and credit agencies. It may take time to rebuild your credit after going through a debt relief process.

- Potential Tax Consequences: Depending on the type of debt relief you pursue, there may be tax implications. For example, forgiven debt through debt settlement may be considered taxable income by the IRS, resulting in additional financial obligations.

- Debt Relief Fees: Debt relief services are not typically free. There are fees associated with working with a debt relief agency or professional, which can increase the overall cost of the debt relief process. It is crucial to carefully review and understand the fees involved before committing to a debt relief program.

- Potential for Lawsuits: In some cases, creditors may choose to pursue legal action instead of negotiating for debt relief. This can result in lawsuits, wage garnishments, and other legal complications, causing additional stress and financial hardship.

When considering debt relief, it is important to carefully weigh the advantages and disadvantages. You may also want to explore alternatives, such as debt consolidation, to see if there are other strategies that better align with your financial goals and circumstances.

How Debt Consolidation Works

Debt consolidation is a financial strategy that combines multiple debts into one consolidated loan. The aim is to simplify the debt repayment process by merging various debts, such as credit card balances, personal loans, and medical bills, into a single loan with a fixed interest rate and a structured repayment plan.

The process of debt consolidation typically involves the following steps:

Evaluating Your Debt:

The first step in debt consolidation is to assess your current debts. This includes gathering information on the outstanding balances, interest rates, and repayment terms of each debt. By understanding the specifics of your debt, you can determine the total amount you need to consolidate.

Exploring Consolidation Options:

Once you have a clear picture of your debts, it’s time to explore your consolidation options. This can involve researching and comparing various lenders and financial institutions that specialize in debt consolidation loans. Consider factors such as interest rates, repayment terms, fees, and customer reviews to find the best fit for your needs.

Applying for a Consolidation Loan:

After selecting a lender, you will need to apply for a consolidation loan. This involves submitting an application, providing necessary documentation, and undergoing a credit check. The lender will evaluate your application and determine whether you meet their criteria for approval.

Consolidating Your Debts:

If your loan application is approved, the lender will provide you with the funds to pay off your existing debts. You will then use these funds to settle your outstanding balances with your previous creditors. This process effectively consolidates your debts into a single loan.

Repaying the Consolidation Loan:

With your debts consolidated, you will start making regular monthly payments towards the consolidation loan. These payments will be determined by the terms and conditions agreed upon with the lender. It is crucial to make timely payments to avoid any penalties or adverse effects on your credit score.

Debt consolidation can offer several benefits, including:

- Simplified Debt Management: By merging multiple debts into one, debt consolidation simplifies your financial responsibilities. Instead of dealing with various due dates and payment amounts, you only need to manage a single monthly payment.

- Potential Cost Savings: Debt consolidation can potentially save you money on interest payments. If your consolidation loan comes with a lower interest rate compared to your previous debts, you can reduce the overall amount paid over the loan term.

- Improved Credit Score: Consistently making payments on time towards your consolidation loan can positively impact your credit score. This is because it shows responsible financial behavior and a commitment to paying off your debts.

However, it is important to consider potential downsides, such as the possibility of extending the repayment period and incurring additional fees. It is recommended to carefully evaluate your financial situation and seek advice from a financial professional before deciding if debt consolidation is the right option for you.

Pros and Cons of Debt Consolidation

Debt consolidation can be an effective financial strategy to help individuals manage their debts and work towards becoming debt-free. However, like any approach, it is important to consider both the advantages and disadvantages. Let’s explore the pros and cons of debt consolidation:

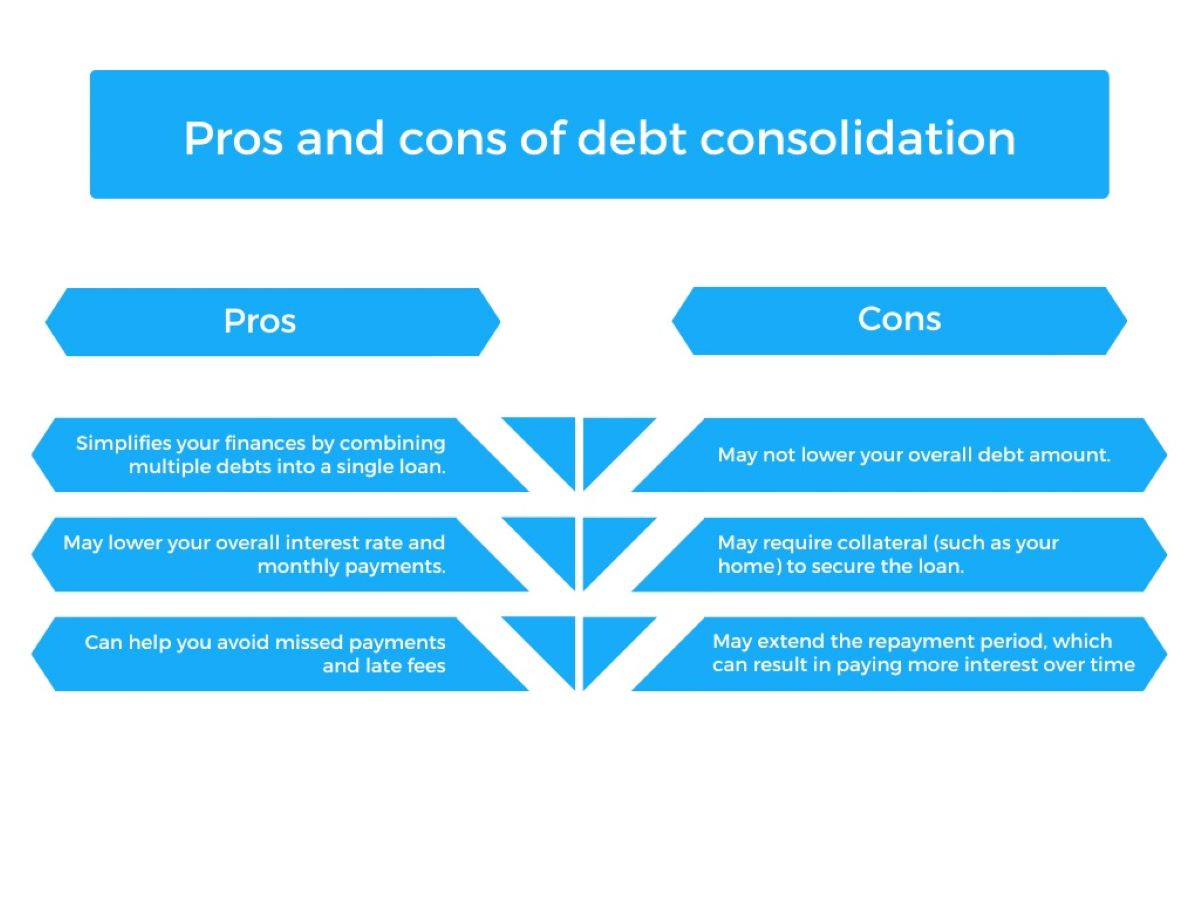

Pros of Debt Consolidation:

- Simplified Debt Management: One of the primary benefits of debt consolidation is the simplification of your financial obligations. By combining multiple debts into a single loan, you only need to make one monthly payment, making it easier to keep track of your finances.

- Lower Interest Rates: Debt consolidation loans often come with lower interest rates compared to credit cards, personal loans, or other forms of unsecured debt. This can result in significant savings over time and help you pay off your debt more efficiently.

- Potential for Improved Credit Score: If you make regular, timely payments on your consolidation loan, it can contribute to improving your credit score. Consistently meeting payment obligations demonstrates responsible financial behavior and can positively impact your creditworthiness.

- Faster Debt Repayment: Debt consolidation can offer a clear repayment plan with a structured timeline. This can help you stay focused and motivated to pay off your debts faster, ultimately helping you achieve financial freedom sooner.

Cons of Debt Consolidation:

- Extended Repayment Period: While debt consolidation can provide a more manageable payment plan, it may also result in a longer repayment period. By spreading your debt over a longer period, you may end up paying more in interest over the long term.

- Potential for Additional Fees: Some debt consolidation loans come with origination fees or other charges. It is essential to carefully review the terms and conditions of the loan to understand any associated fees and how they may impact the overall cost of consolidating your debt.

- Risk of Accumulating More Debt: Debt consolidation clears your existing debts, but it does not address the underlying financial behaviors that led to accumulating those debts in the first place. Without addressing these behaviors, there is a risk of falling back into old habits and accumulating new debts.

- Collateral Requirement: Depending on the type of debt consolidation loan you choose, you may be required to offer collateral, such as your home or a valuable asset. This poses the risk of losing the collateral if you default on the loan.

It is important to carefully evaluate your financial situation and consider all the pros and cons before pursuing debt consolidation. Analyze factors such as the interest rates, fees, repayment terms, and your ability to make consistent payments. Seeking advice from a financial professional can provide valuable guidance in determining if debt consolidation is the right choice for you.

Factors to Consider When Choosing Between Debt Relief and Debt Consolidation

When faced with overwhelming debt, it is essential to carefully assess your financial situation and consider the factors that will influence your decision between debt relief and debt consolidation. Here are some key considerations to keep in mind:

1. Total Amount of Debt:

The amount of debt you owe plays a significant role in determining which approach is more suitable for you. Debt relief, such as debt settlement, may be a viable option if you have a substantial amount of debt that you are unable to repay in full. Debt consolidation, on the other hand, is better suited for individuals with multiple debts that can be consolidated into a single loan.

2. Monthly Payment Affordability:

Consider your monthly budget and assess what you can realistically afford to pay towards your debts. Debt relief may be a better choice if you are struggling to make minimum payments and need a significant reduction in your overall debt burden. Debt consolidation, on the other hand, helps by providing a more organized repayment plan with a manageable monthly payment.

3. Credit Score and Financial Goals:

Evaluating the impact on your credit score is important when choosing between debt relief and debt consolidation. Debt settlement, a common form of debt relief, can have a negative impact on your credit score. If maintaining a good credit score is a priority for you, debt consolidation may be a better option, as consistent, timely payments can actually help improve your credit score over time.

4. Type of Debt:

Consider the types of debts you have. Debt relief is often more suitable for unsecured debts, such as credit card debts and medical bills. If you have secured debts, such as a mortgage or car loan, debt consolidation may be a more appropriate choice. Secured debts typically require collateral, which means you may risk losing your assets if you pursue debt relief options.

5. Long-Term Financial Impact:

Take into account the long-term financial impact of your chosen approach. Debt relief may offer immediate relief by reducing your overall debt burden, but it can have long-term consequences, such as potential tax implications and a negative impact on your credit score. Debt consolidation provides a structured repayment plan, potentially saving you money on interest payments and helping you build a positive credit history for the future.

6. Professional Guidance:

It is advisable to seek guidance from a financial professional who can assess your specific situation and provide personalized advice. They can help you understand the advantages and disadvantages of each approach and determine which one aligns better with your overall financial goals.

Ultimately, the decision between debt relief and debt consolidation will depend on your unique circumstances. Consider these factors, weigh your options carefully, and select the approach that provides the most effective and sustainable solution for managing your debt.

Conclusion

When confronted with overwhelming debt, making the right decision between debt relief and debt consolidation is crucial for regaining control of your financial situation. Both approaches have their merits and considerations, and understanding these can help you choose the strategy that aligns with your specific needs and goals.

Debt relief, which aims to reduce your overall debt amount through negotiations with creditors, can provide immediate relief for those struggling with unmanageable debt burdens. However, it may come with potential drawbacks such as adverse effects on your credit score and tax implications.

On the other hand, debt consolidation offers a way to simplify debt management by combining multiple debts into a single loan. It can provide a structured repayment plan, potentially lower interest rates, and an opportunity to improve your credit score over time. However, it may result in an extended repayment period and additional fees.

Factors such as the total amount of debt, monthly payment affordability, credit score, type of debt, long-term financial impact, and professional guidance should be considered when making your decision. Assessing these factors will help you determine which approach better aligns with your financial circumstances and long-term goals.

It is important to remember that there is no one-size-fits-all solution when it comes to managing debt. What works for one person may not work for another. Therefore, it is recommended to seek guidance from a financial professional who can evaluate your specific situation and provide personalized advice.

By carefully assessing your options, considering the advantages and disadvantages, and seeking professional guidance, you can make an informed decision that sets you on the path to financial stability and freedom from debt.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance