Finance

Why Is My Credit Score Not Showing Up

Published: October 22, 2023

Discover why your credit score is not showing up and get expert tips on how to improve it. Explore finance solutions and take control of your financial future.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

- Introduction

- Understanding Credit Scores

- Reasons why your credit score may not be showing up

- Lack of credit history

- Errors or discrepancies in your credit report

- Inactive or closed accounts

- Delayed reporting by lenders

- Identity theft or fraud

- Credit bureaus not having your information

- How to resolve the issue

- Check your credit report for errors

- Contact the credit bureaus

- Establish or build credit history

- Monitor your credit activity regularly

- Conclusion

Introduction

Credit scores play a crucial role in our financial lives, impacting our ability to secure loans, credit cards, and favorable interest rates. They are a reflection of our financial responsibility and how we handle credit. So, when you go to check your credit score and find that it is not showing up, it can be concerning and frustrating.

While it is understandable to feel anxious about this situation, it’s important to remember that there can be various reasons why your credit score may not be showing up. In this article, we will explore some of the common factors that can lead to this problem and provide suggestions on how to resolve it.

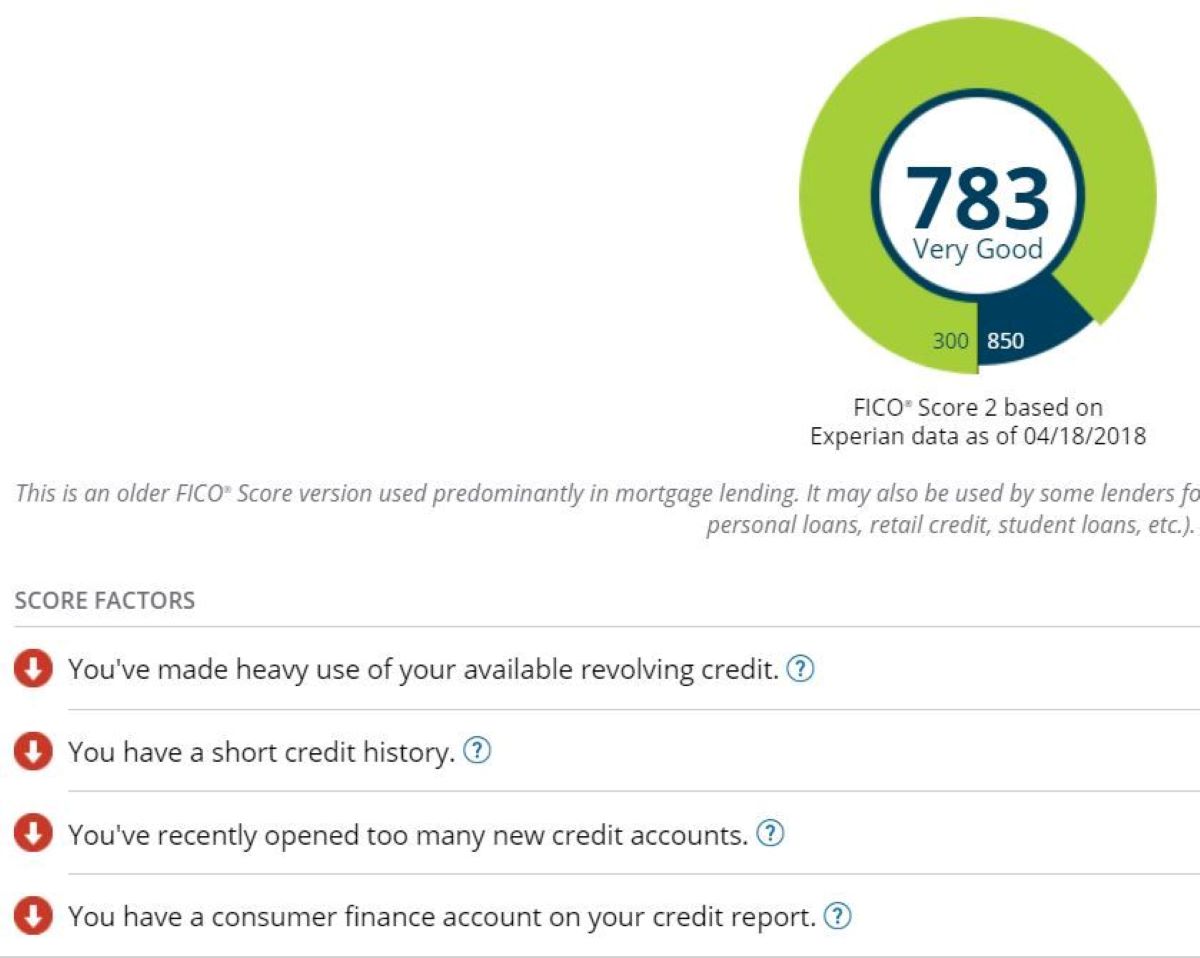

Before we delve into the reasons behind your missing credit score, it is crucial to have a basic understanding of what credit scores are. Credit scores are numerical representations of an individual’s creditworthiness, calculated based on information from their credit reports. They provide lenders with an assessment of the likelihood that a borrower will repay their debts on time.

Credit scores range from 300 to 850, with higher scores indicating a lower credit risk. The most commonly used credit scoring model is the FICO score, developed by the Fair Isaac Corporation. Other credit scoring models include VantageScore and Experian’s PLUS Score.

Understanding Credit Scores

Before we dive into why your credit score may not be showing up, let’s take a moment to understand how credit scores work and what factors influence them.

Credit scores are calculated based on information in your credit report, which includes details about your credit history and repayment patterns. The data in your credit report is collected and maintained by credit bureaus, such as Experian, Equifax, and TransUnion. These bureaus use various algorithms and formulas to calculate your credit score.

The factors that impact your credit score include:

- Payment History: Your track record of making on-time payments, late payments, or defaults on your credit accounts.

- Credit Utilization: The amount of your available credit that you are currently using. It is recommended to keep your credit utilization ratio below 30% of your total credit limit.

- Length of Credit History: The length of time you have been using credit. Generally, a longer credit history is viewed more positively by lenders.

- Types of Credit: The mix of credit accounts you have, such as credit cards, loans, and mortgages. Having a diverse range of credit types can positively impact your score.

- New Credit Inquiries: When you apply for new credit, a hard inquiry is made on your credit report. Too many recent inquiries can negatively impact your score.

It’s important to note that your credit score can vary slightly between credit bureaus, as they may use different scoring models or have access to different information. However, the overall trends and factors affecting your score should remain relatively consistent.

Having a good credit score is essential when applying for loans, mortgages, or credit cards. It can also affect other areas of your financial life, such as insurance premiums, rental applications, and even employment opportunities in some industries.

Now that we have a basic understanding of credit scores, let’s explore some of the reasons why your credit score may not be showing up.

Reasons why your credit score may not be showing up

There are several factors that could contribute to your credit score not showing up. It’s important to consider these possibilities and take appropriate steps to address the issue. Here are some common reasons why your credit score may not be appearing:

- Lack of credit history: If you are new to credit or have limited credit history, it’s possible that you don’t yet have a credit score. Credit scores are typically generated based on your payment history and credit accounts. Without any credit activity, there may be insufficient data to calculate a score.

- Errors or discrepancies in your credit report: Mistakes can occur on your credit report that might prevent your credit score from showing up. These errors could be anything from incorrect personal information to inaccurate account information or delinquent payments that you have actually made. It’s crucial to review your credit report regularly to identify and dispute any errors with the credit bureaus.

- Inactive or closed accounts: If you haven’t used a credit account in a while or if you closed an account, it may no longer be reported to the credit bureaus. Since credit scores are calculated based on the information in your credit report, the absence of these accounts can result in your credit score not appearing.

- Delayed reporting by lenders: Sometimes, lenders may not report your credit activity to the credit bureaus in a timely manner. This delay can lead to your credit score not being updated or even not showing up. It’s advisable to keep track of your credit activity and follow up with lenders if you notice any discrepancies or delays in reporting.

- Identity theft or fraud: If you have been a victim of identity theft or fraud, it’s possible that someone has used your personal information to open accounts or engage in fraudulent activities. In such cases, your credit score may not be showing up due to the ongoing investigations or disputes related to the fraudulent activity. It’s crucial to report any instances of identity theft or fraud immediately and work with the credit bureaus to resolve the issue.

- Credit bureaus not having your information: In some instances, your credit information may not have been reported to the credit bureaus. This could happen if a particular lender or creditor does not report your activity, or if there is a delay or technical issue in the reporting process. It’s advisable to contact the credit bureaus and provide them with the necessary information to ensure that your credit activity is being accurately reported.

These are some of the common reasons why your credit score may not be showing up. Understanding these factors can help you determine the appropriate steps to resolve the issue and ensure that your credit score is accurately reflected.

Lack of credit history

If you are just starting to build your credit or have limited credit history, it’s possible that your credit score is not showing up because there is not enough information to generate a score. Credit scores are calculated based on your credit activity and payment history, so without any credit accounts or transactions, there is simply not enough data for the credit bureaus to evaluate.

Having a limited credit history can be common for young adults or individuals who have never had a credit card or loan before. Without a credit score, it can be challenging to obtain credit cards, loans, or other forms of credit. Lenders rely on credit scores to assess your creditworthiness, which determines your ability to repay borrowed money.

To start building your credit history, you can take the following steps:

- Apply for a secured credit card: Secured credit cards are a great option for individuals with limited or no credit history. These cards require a cash deposit as collateral, which sets your credit limit. By using a secured credit card responsibly and making on-time payments, you can establish a positive credit history.

- Become an authorized user: If you have family members or close friends with well-established credit accounts, you may ask them to add you as an authorized user on their credit card. This allows you to piggyback off their credit history and build a positive credit profile.

- Consider a credit-builder loan: Credit-builder loans are designed to help individuals build credit. With these loans, you make small monthly payments into a savings account, and once you’ve completed the term, you receive the money plus interest. The lender reports your payment history to the credit bureaus, helping you build a positive credit history.

- Apply for a student or starter credit card: Some credit card companies offer cards specifically designed for students or individuals with limited credit history. These cards typically have lower credit limits and may have fewer rewards or perks, but they can help you establish credit when used responsibly.

- Pay your bills on time: While it may not directly build your credit history, consistently paying your bills on time demonstrates responsible financial behavior, which is crucial when lenders assess your creditworthiness in the future.

Building a credit history takes time and requires responsible financial habits. By taking these steps and being diligent in managing your credit, you can start establishing a positive credit history and eventually have a credit score that will be reflected when you check your credit.

Errors or discrepancies in your credit report

Errors or discrepancies in your credit report can prevent your credit score from showing up or may result in an inaccurate score. Mistakes can happen due to various reasons, including clerical errors, outdated information, or identity theft. It’s crucial to review your credit report regularly to identify and correct any errors that may be impacting your credit score.

Here are some steps you can take to address errors or discrepancies in your credit report:

- Obtain a free copy of your credit report: Under federal law, you are entitled to a free copy of your credit report from each of the major credit bureaus (Equifax, Experian, and TransUnion) once a year. You can request your reports online or by mail.

- Review your credit report thoroughly: Carefully examine your credit report for any errors, such as incorrect personal information, accounts that don’t belong to you, or late payments that you have actually made on time. Take note of any discrepancies or inaccuracies that may be affecting your credit score.

- Dispute any errors with the credit bureaus: If you find errors or discrepancies in your credit report, you have the right to dispute them. Contact the credit bureau(s) reporting the error and provide them with all the necessary documentation to support your claim. The credit bureau will investigate your dispute and make the necessary corrections if the information is found to be inaccurate.

- Follow up on the dispute process: Keep track of your dispute and follow up with the credit bureau(s) to ensure that the necessary changes are made. It’s advisable to maintain copies of all communication and documentation related to the dispute for future reference.

- Monitor your credit report regularly: After resolving any errors, continue to monitor your credit report regularly to ensure that the corrections have been made and that no new errors or discrepancies are appearing. You can consider using credit monitoring services or subscribing to credit monitoring apps to stay updated on any changes in your credit history.

By addressing errors or discrepancies in your credit report, you can ensure that your credit score is accurately reflected. It’s crucial to stay proactive in monitoring your credit report and taking steps to correct any inaccuracies to protect your creditworthiness.

Inactive or closed accounts

If you have inactive or closed accounts that are not being reported to the credit bureaus, it can lead to your credit score not showing up or not being updated. Credit scores are calculated based on the information in your credit report, so if those accounts are not being reported, it can impact your credit score visibility.

There are a few reasons why this might happen:

- Inactivity: If you haven’t used a credit account for a long period of time, the lender may stop reporting that account to the credit bureaus. Inactive accounts may not provide recent data on your credit activity and repayment history, which means they are not factored into your credit score.

- Closure: When you close a credit account voluntarily, it may no longer be reported to the credit bureaus. Closed accounts are generally excluded from credit score calculations, as they are no longer active and don’t reflect current credit behavior.

- Debt settlement or bankruptcy: If you had accounts that were settled for a lesser amount or included in a bankruptcy filing, they might be marked as “settled” or “included in bankruptcy” on your credit report. These accounts may not contribute positively to your credit score.

While inactive or closed accounts might not have a direct impact on your credit score, they can still be relevant to lenders when they review your credit history. Lenders may consider factors such as the age of your credit accounts and your overall credit utilization ratio, which includes both active and inactive accounts.

If you have concerns about inactive or closed accounts affecting your credit score visibility, there are a few steps you can take:

- Verify if the accounts are still active: Contact the lenders associated with the inactive or closed accounts to confirm whether they are still open and if they are being reported to the credit bureaus.

- Re-establish credit activity: To ensure that your credit score is being calculated accurately, you may need to re-establish credit activity. You can do this by using your existing credit accounts responsibly, applying for new credit, or utilizing credit building techniques such as a secured credit card or a credit-builder loan.

- Monitor your credit report: Regularly reviewing your credit report allows you to identify any errors or discrepancies related to inactive or closed accounts. If you notice any incorrect information, you can dispute it with the credit bureaus to ensure the accurate reporting of your credit history.

Remember, while inactive or closed accounts may not be directly impacting your credit score visibility, they can still have relevance in the eyes of potential lenders. Staying vigilant about your credit accounts and taking steps to maintain a healthy credit history is crucial for your financial well-being.

Delayed reporting by lenders

One possible reason why your credit score may not be showing up is due to delayed reporting by lenders. When you make payments or engage in credit activity, it is important for that information to be reported to the credit bureaus in a timely manner. If there are delays in reporting, it can result in your credit score not being updated or not showing up at all.

There are a few factors that can contribute to delayed reporting:

- Lender processes: Some lenders may have internal processes that cause delays in reporting your credit activity. These processes can include data validation, reconciliation, or other administrative procedures that need to be completed before the information is sent to the credit bureaus.

- Institution size: Larger financial institutions might have more complex reporting systems, which can lead to delays in updating your credit information. It may take some time for your payments or credit activity to be processed and reported to the credit bureaus.

- Reporting cycles: Lenders typically have specific reporting cycles to the credit bureaus. If your credit activity occurs shortly before or after a reporting cycle, there may be a delay in updating your credit score. It’s important to keep in mind that credit bureaus do not receive real-time updates from lenders.

- Technical issues: Occasionally, technical issues or glitches in the reporting systems can cause delays in updating your credit information. These issues can range from software malfunctions to connectivity problems that prevent the timely transmission of data to the credit bureaus.

If you believe there is a delay in the reporting of your credit activity, here are a few steps you can take:

- Contact the lender: Reach out to the lender or creditor associated with the account for which you suspect delayed reporting. Inquire about their reporting process and timelines to understand if there are any potential delays on their end.

- Keep track of your payments: Maintain a record of your payments and credit activity to ensure accuracy. If you notice a significant delay in your credit activity being reported, you may want to provide evidence, such as payment receipts or transaction history, to the lender and credit bureaus.

- Follow up with the credit bureaus: If you suspect that the delayed reporting is adversely impacting your credit score visibility, reach out to the credit bureaus to discuss the situation. Provide them with any relevant documentation or information to support your claim and request that they update your credit information accordingly.

While delayed reporting by lenders can be frustrating, it is important to be proactive in monitoring your credit activity and following up with both the lenders and credit bureaus to ensure the accurate reporting of your credit information. By staying vigilant, you can work towards resolving any delays and ensuring that your credit score reflects your creditworthiness accurately.

Identity theft or fraud

Identity theft and fraud can have a significant impact on your credit score, and it can also be a reason why your credit score may not be showing up. If you suspect that you have been a victim of identity theft or fraud, it’s crucial to take immediate action to protect your credit and resolve any issues that may arise.

Here are the steps you can take if you suspect identity theft or fraud:

- Review your credit report: Obtain copies of your credit reports from all three major credit bureaus (Equifax, Experian, and TransUnion) and carefully review them for any unfamiliar accounts, inquiries, or discrepancies. These could be signs of fraudulent activity.

- Place a fraud alert: Contact one of the credit bureaus and request to place a fraud alert on your credit file. This will notify lenders that you may be a victim of identity theft, and they should take extra precautions to verify your identity before granting credit in your name.

- File a police report: In cases of identity theft, filing a police report is crucial. Visit your local police department and provide them with all the relevant information about the identity theft. This report can serve as evidence of the crime and will be useful when disputing fraudulent accounts or charges.

- Contact creditors and dispute fraudulent accounts: Reach out to the creditors associated with any fraudulent accounts and inform them of the identity theft. Provide them with the details of the fraudulent activity and any supporting documentation, such as the police report. Request that the fraudulent accounts be closed and removed from your credit report.

- Work with the credit bureaus: Notify all three credit bureaus about the fraudulent accounts and provide them with the necessary documentation. They will initiate an investigation to verify the fraudulent activity and remove the incorrect information from your credit report. Regularly follow up with them to ensure that the necessary corrections have been made.

- Monitor your credit activity: After resolving the identity theft or fraud, it’s crucial to monitor your credit activity regularly. Consider using credit monitoring services or identity theft protection services to receive alerts about any suspicious activity. This will allow you to detect any potential signs of identity theft early on and take prompt action to prevent further damage.

Identity theft and fraud can have far-reaching consequences, including damage to your credit score. By taking immediate action and working with the appropriate authorities and credit bureaus, you can mitigate the impact of identity theft and restore your creditworthiness.

Credit bureaus not having your information

If your credit score is not showing up, it could be because the credit bureaus do not have your information on file. This can happen for several reasons, including data entry errors, technical glitches, or delays in the reporting process. While it can be frustrating, there are steps you can take to ensure that your credit information is accurately reflected.

Here’s what you can do if the credit bureaus do not have your information:

- Verify your personal details: Start by double-checking the personal information you provided to lenders or creditors. Ensure that your name, date of birth, address, and Social Security number are correct and consistent across all your credit accounts. Discrepancies or errors in this information can lead to missing or incorrect credit records.

- Contact the credit bureaus: Reach out to the credit bureaus directly to inform them about the missing credit information. Provide them with any supporting documentation or details, such as account statements or payment records, to help them verify and update your credit information. The credit bureaus may need to investigate the issue and work with the lenders to ensure accurate reporting.

- Follow up with your lenders: Contact your lenders or creditors to inquire about their reporting practices and confirm that they are sharing your credit information with the credit bureaus. If they have not been reporting your credit activity, provide them with your correct information and request that they start reporting to the credit bureaus.

- Keep records of your credit activity: Maintain detailed records of your credit activity, such as payment receipts, account statements, and loan agreements. These documents can serve as evidence to support your credit information and help resolve any discrepancies with the credit bureaus.

- Regularly check your credit reports: Monitor your credit reports from all three major credit bureaus to stay informed about any missing or incorrect information. By regularly reviewing your credit reports, you can identify any discrepancies or omissions and take the necessary steps to address them promptly.

- Consider credit monitoring services: Consider enrolling in credit monitoring services that provide real-time updates and alerts about any changes to your credit history. These services can help you stay informed about the status of your credit information and notify you of any potential issues.

By taking the initiative to contact the credit bureaus and your lenders, and by maintaining accurate records of your credit activity, you can help ensure that your credit information is properly reported and reflected in your credit score.

How to resolve the issue

If your credit score is not showing up or is inaccurate, it’s important to take steps to resolve the issue and ensure that your credit information is accurately reflected. Here are some steps you can take to address the problem:

- Check your credit report for errors: Obtain copies of your credit reports from all three major credit bureaus and carefully review them for any errors or discrepancies. Look for incorrect personal information, accounts you don’t recognize, or late payments that you have actually made on time. Dispute any errors or inaccuracies with the credit bureaus and provide supporting documentation to support your claim.

- Contact the credit bureaus: Reach out to the credit bureaus directly to discuss the issue. Provide them with any relevant information or documentation regarding the missing or inaccurate credit score. The credit bureaus will investigate your concerns and make the necessary corrections to your credit report if warranted.

- Establish or build credit history: If the issue is due to a lack of credit history, start building your credit by establishing new credit accounts or using credit-building techniques. This could include applying for a secured credit card, becoming an authorized user on someone else’s credit card, or taking out a credit-builder loan. Responsible use of credit and making timely payments will help establish a positive credit history.

- Monitor your credit activity regularly: Stay proactive by monitoring your credit activity on a regular basis. Keep track of your accounts, payments, and credit utilization. By being aware of your credit behavior, you can identify any issues or discrepancies quickly and take appropriate action.

- Consider credit counseling: If you’re struggling with managing your credit or have difficulty resolving the issue on your own, you may want to seek credit counseling. Credit counseling agencies can provide guidance on credit management, debt repayment strategies, and dispute resolution. They can help you navigate the process and work towards improving your credit situation.

Resolving issues with your credit score may take time and effort, but it’s crucial to take proactive steps to ensure the accuracy of your credit information. By addressing any errors or discrepancies, establishing a positive credit history, and monitoring your credit activity, you can work towards improving your credit score visibility and maintaining a strong financial foundation.

Check your credit report for errors

When your credit score is not showing up or is inaccurate, it is essential to start by checking your credit report for any errors. Your credit report contains the information that forms the basis of your credit score, so ensuring its accuracy is crucial for an accurate credit assessment. Here’s how you can proceed:

- Obtain copies of your credit reports: Request a copy of your credit report from each of the three major credit bureaus – Equifax, Experian, and TransUnion. Federal law entitles you to one free copy per year from each bureau, which you can obtain from AnnualCreditReport.com.

- Thoroughly review your credit reports: Carefully examine your credit reports to identify any errors, discrepancies, or inconsistencies. Look for incorrect personal information, such as your name, address, or Social Security number, as well as any inaccurate account information, late payments, or accounts that do not belong to you.

- Document any errors: Make note of any errors you identify on your credit reports. Keep a record of the specific details, including the account name, account number, and the nature of the error. It’s essential to have this information documented as you proceed to dispute the errors.

- Dispute erroneous information: If you find errors on your credit reports, it’s crucial to take action to have them corrected. You can file a dispute directly with the credit bureaus online, through their respective websites. Provide a clear explanation of each error and provide any supporting documentation you have to prove the inaccuracy. The credit bureaus will then investigate your dispute and make the appropriate corrections if the information is found to be inaccurate.

- Follow up on your disputes: Keep track of your disputes and maintain documentation of your communications. Follow up with the credit bureaus if necessary to ensure that the errors are being addressed. It may take some time for the investigations to be completed, so patience is key during this process.

- Review your updated credit reports: Once the investigation is complete, review your updated credit reports to ensure that the errors have been corrected. Verify that the inaccurate information has been removed, and check that your credit score has been updated accordingly.

Regularly checking your credit report for errors and taking steps to correct them is an important part of maintaining a healthy credit profile. By identifying and disputing any inaccuracies, you can help ensure that your credit reports are an accurate reflection of your credit history, which in turn can lead to a more accurate credit score.

Contact the credit bureaus

If your credit score is not showing up or is inaccurate, it is important to contact the credit bureaus directly to address the issue. The credit bureaus play a crucial role in maintaining and reporting your credit information, so reaching out to them can help resolve any discrepancies. Here’s how you can contact the credit bureaus:

- Identify the credit bureaus: There are three major credit bureaus – Equifax, Experian, and TransUnion. It’s important to identify which credit bureaus may be reporting the inaccurate information by checking your credit reports. Not all lenders report to all three bureaus, so the information may vary among them.

- Reach out to the credit bureaus: Contact the credit bureaus directly to inform them about the issues with your credit score or any inaccurate information on your credit reports. You can reach them through their websites, by phone, or by mail. Each credit bureau has dedicated channels for handling disputes and inquiries.

- Provide necessary information: When contacting the credit bureaus, be prepared to provide the necessary details to help them investigate and resolve the issue. This includes your personal information, such as your name, address, and Social Security number, as well as the specific details of the inaccurate information or missing credit score.

- File a dispute: If you have identified specific errors on your credit reports, you can file a dispute with the credit bureaus. This can typically be done online through their dispute resolution portals. Clearly explain the nature of the inaccuracies and provide any supporting documentation you have that proves the error.

- Follow up on your disputes: After filing a dispute, it is important to follow up with the credit bureaus to ensure that the investigation is progressing and that the necessary corrections are being made. Keep a record of all correspondence, including reference numbers or case IDs, as this will help you track the progress of your dispute.

- Monitor your credit reports: Regularly monitor your credit reports to ensure that any changes or corrections have been made. The credit bureaus are required to notify you of the results of their investigation. Review your updated credit reports to verify that the inaccurate information has been corrected and that your credit score is now accurately reflected.

By directly contacting the credit bureaus and providing them with the necessary information, you can take proactive steps to address any issues with your credit score or inaccurate information on your credit reports. Working with the credit bureaus is essential for resolving discrepancies and ensuring that your credit information is accurate and up to date.

Establish or build credit history

If your credit score is not showing up due to a lack of credit history, it’s important to take steps to establish or build your credit. Having a solid credit history is essential for lenders to assess your creditworthiness and calculate your credit score. Here are some strategies to help you establish or build your credit history:

- Apply for a secured credit card: A secured credit card requires a cash deposit as collateral, which becomes your credit limit. Using a secured credit card responsibly, such as making timely payments and keeping your balances low, can help you establish a positive credit history.

- Become an authorized user: If you have trusted family or friends with good credit, ask them to add you as an authorized user on one of their credit cards. Their positive credit history and responsible credit usage can help boost your credit profile as well.

- Get a co-signer or joint account: If you are unable to qualify for credit on your own, you may consider getting a co-signer or opening a joint account with someone who has established credit. By doing so, their credit history can support your creditworthiness.

- Apply for a starter credit card: Some credit card companies offer cards specifically designed for individuals with limited or no credit history. These starter credit cards may have lower credit limits or require a security deposit, but they can help you establish credit when used responsibly.

- Apply for a credit-building loan: Credit-building loans, also known as credit builder loans, help you establish credit while simultaneously saving money. These loans require you to make regular payments into a savings account, and once you’ve completed the term, you receive the money along with a positive credit history.

- Make on-time payments: Regardless of the type of credit you have, one of the most important factors in building credit is consistently making on-time payments. Pay your bills, loans, and credit card balances by the due dates to demonstrate good credit management.

It’s important to note that building or establishing credit takes time, patience, and responsible financial behavior. Avoid taking on too much debt, keep your credit utilization low, and avoid making multiple credit applications within a short period of time, as these can negatively impact your creditworthiness.

By taking proactive steps to build your credit history, you can gradually establish a positive credit profile. Over time, this will help your credit score to appear and improve, allowing you greater access to credit options and better interest rates in the future.

Monitor your credit activity regularly

Monitoring your credit activity regularly is essential for maintaining a healthy credit profile and ensuring the accuracy of your credit score. By staying informed of any changes or discrepancies, you can identify and address potential issues promptly. Here’s how you can effectively monitor your credit activity:

- Review your credit reports: Regularly obtain copies of your credit reports from the three major credit bureaus – Equifax, Experian, and TransUnion. Check your reports for any errors, inaccuracies, or signs of fraudulent activity. Reviewing your credit reports can help you identify potential issues that may be affecting your credit score.

- Take advantage of free credit monitoring services: Many financial institutions and credit card companies offer free credit monitoring services to their customers. These services provide alerts and notifications when there are changes to your credit reports or suspicious activity on your accounts. Enrolling in such services can help you stay on top of your credit activity more conveniently.

- Monitor your credit card and bank statements: Regularly review your credit card and bank statements for any unfamiliar or unauthorized transactions. If you notice any discrepancies, report them to your financial institution immediately. Monitoring your statements can help you detect potential fraudulent activity that could impact your credit.

- Set up fraud alerts and credit freezes: Consider placing fraud alerts or credit freezes on your credit files to provide an additional layer of protection. A fraud alert notifies lenders to take extra precautions when verifying your identity, while a credit freeze restricts access to your credit reports, making it difficult for identity thieves to open new accounts in your name.

- Monitor your credit utilization: Keep an eye on your credit utilization ratio, which is the amount of credit you are currently using compared to your total credit limit. Aim to keep your utilization below 30% to maintain a good credit score. Regular monitoring of your credit utilization can help you identify areas where you may need to adjust your spending habits or make additional payments to minimize your debt.

- Stay vigilant for signs of identity theft: Watch out for any unusual or suspicious activity that may indicate identity theft, such as unexpected credit inquiries, unfamiliar accounts, or sudden changes in your credit report. If you suspect identity theft, report it immediately to the proper authorities and take necessary steps to mitigate the damage.

By monitoring your credit activity regularly, you can quickly identify and address any errors, discrepancies, or potential fraud. Regular monitoring empowers you to take action, dispute inaccuracies, and protect your credit score. It also allows you to make more informed financial decisions and maintain control over your creditworthiness.

Conclusion

When your credit score is not showing up or is inaccurate, it can be concerning. However, there are several reasons why this might happen, and there are steps you can take to resolve the issue. Understanding the factors that may be impacting your credit score visibility is the first step towards finding a solution.

To address this issue, start by checking your credit report for errors, as inaccuracies can significantly impact your credit score. Contact the credit bureaus and provide them with any necessary documentation to dispute and correct any discrepancies. Additionally, if you have a lack of credit history, take proactive steps to establish or build it by using credit responsibly and making on-time payments.

Regularly monitoring your credit activity is essential to ensure the accuracy of your credit score. Review your credit reports, utilize credit monitoring services, and stay vigilant for any signs of identity theft or fraud. Taking these proactive measures will help you maintain a healthy credit profile and ensure that your credit score is accurately reflected.

In conclusion, while it can be frustrating when your credit score is not showing up, it is important to remain proactive and take the necessary steps to address the issue. By being diligent in monitoring your credit, disputing errors, and establishing a positive credit history, you can work towards improving your credit score visibility and ensuring your financial well-being.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance