Finance

Why My Credit Score Is Not Increasing

Modified: March 10, 2024

Learn why your credit score is not increasing and get expert advice on improving your financial situation. Discover effective strategies to boost your score and secure a better future in finance.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

- Introduction

- Understanding Credit Scores

- Factors Affecting Credit Scores

- Payment History

- Credit Utilization

- Length of Credit History

- Credit Mix

- Recent Credit Inquiries

- Monitoring Credit Score

- Reasons for Credit Score Not Increasing

- Late Payments

- High Credit Utilization

- Lack of Credit History

- Limited Credit Mix

- New Credit Inquiries

- Errors on Credit Report

- Improving Your Credit Score

- Paying Bills on Time

- Lowering Credit Utilization

- Building a Credit History

- Diversifying Credit Mix

- Being Cautious with New Inquiries

- Correcting Errors on Credit Report

- Conclusion

Introduction

Your credit score is an essential financial indicator that lenders use to evaluate your creditworthiness. A higher credit score generally translates to more favorable loan terms and lower interest rates. As such, it’s natural to aspire for your credit score to increase over time. However, if you find that your credit score is not increasing, it can be frustrating and confusing.

Before diving into possible reasons why your credit score is not increasing, it’s crucial to understand how credit scores work. Credit scores are calculated based on information contained in your credit report, such as your payment history, credit utilization, length of credit history, credit mix, and recent credit inquiries.

In this article, we will explore the various factors that can affect your credit score and why it may not be increasing as you would like. Additionally, we will discuss actionable steps you can take to improve your credit score and maintain a healthy credit profile.

It’s important to note that building and maintaining good credit takes time and diligence. It’s not an overnight process, and it requires a consistent track record of responsible financial behavior. Understanding the factors that contribute to your credit score can empower you to make informed decisions and take appropriate actions to improve it.

So, if you’ve been wondering why your credit score remains stagnant, even though you’ve been making an effort to improve it, keep reading. We will break down the possible reasons and provide practical tips to help you boost your credit score and achieve your financial goals.

Understanding Credit Scores

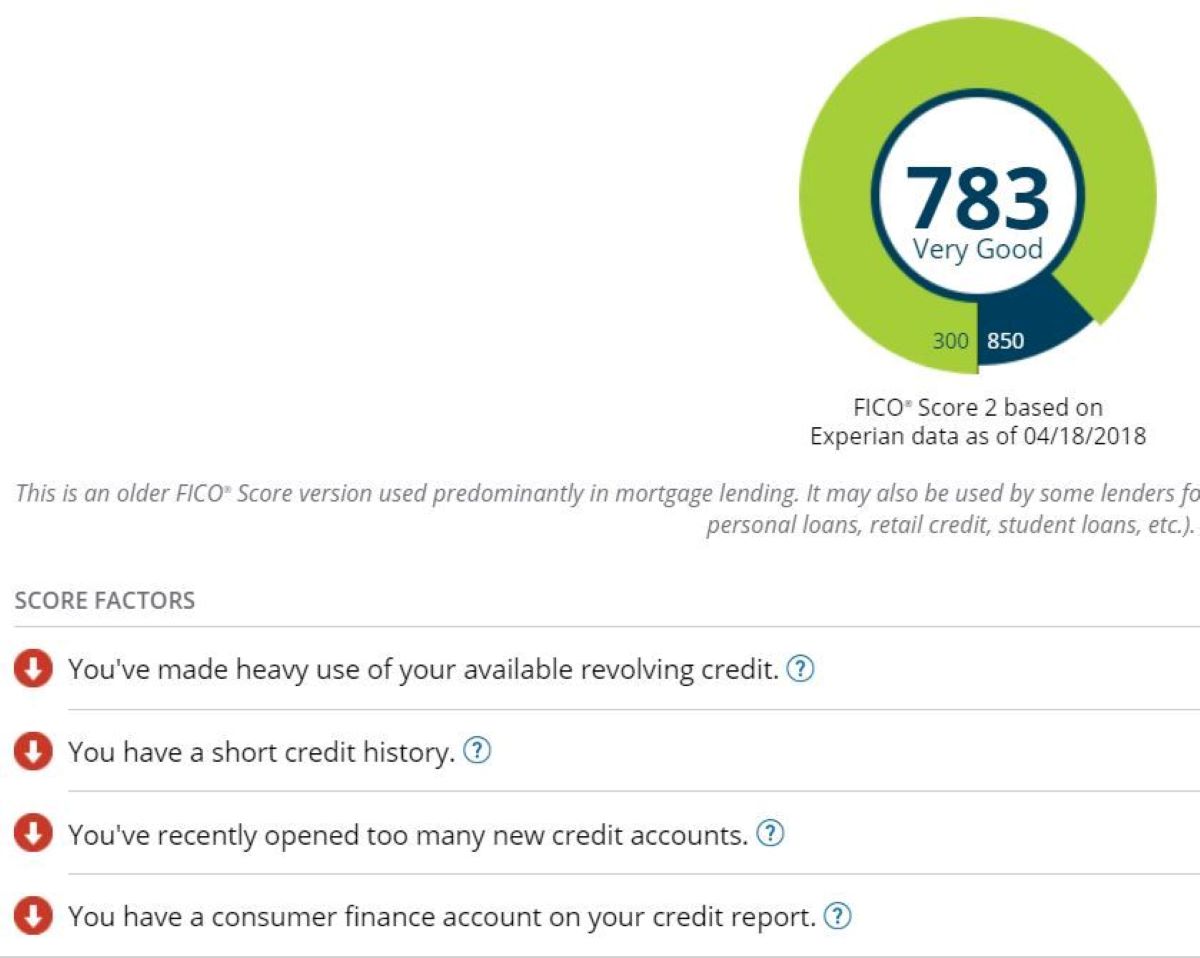

Before delving into the reasons why your credit score may not be increasing, it’s crucial to have a clear understanding of what a credit score is and how it is calculated. A credit score is a three-digit number that lenders use to assess your creditworthiness and the likelihood that you will repay borrowed money.

The most widely used credit scoring models, such as the FICO Score and VantageScore, consider several factors when calculating your credit score. These factors include:

- Payment History: This is one of the most significant factors in determining your credit score. Lenders want to see a history of on-time payments and a lack of late payments or defaults.

- Credit Utilization: This refers to the percentage of your available credit that you are currently using. A high credit utilization ratio can negatively impact your credit score.

- Length of Credit History: The length of time you have been using credit also plays a role in your credit score. Lenders prefer to see a longer credit history as it provides more information about your borrowing habits.

- Credit Mix: Having a diverse mix of credit accounts, such as credit cards, loans, and mortgages, can positively impact your credit score. It demonstrates your ability to manage different types of credit responsibly.

- Recent Credit Inquiries: When you apply for new credit, such as a loan or credit card, a hard inquiry is placed on your credit report. Multiple inquiries within a short period can negatively impact your credit score.

Now that you have a basic understanding of the factors that contribute to your credit score, it’s important to remember that each individual’s credit profile is unique. Therefore, the weight assigned to each factor may vary based on your specific circumstances.

Keep in mind that credit scores range from 300 to 850, with a higher score indicating better creditworthiness. It’s advisable to regularly monitor your credit score and review your credit report to ensure that the information is accurate and up to date. Understanding your credit score and the factors affecting it will help you take proactive steps towards improving it.

Factors Affecting Credit Scores

Several factors contribute to determining your credit score. Understanding these factors is crucial in identifying why your credit score may not be increasing as expected. Let’s take a closer look at each of these factors:

- Payment History: Your payment history is the most significant factor influencing your credit score. It reflects your track record of making timely payments on credit accounts such as loans, credit cards, and mortgages. Late payments, defaults, or accounts in collections can have a severe negative impact on your credit score.

- Credit Utilization: Credit utilization refers to the ratio of your credit card balances to your credit limits. High utilization, where you are using a large percentage of your available credit, can negatively impact your credit score. It is advisable to keep your credit utilization below 30% to maintain a healthy credit score.

- Length of Credit History: The length of your credit history plays a role in determining your creditworthiness. Lenders prefer a longer credit history as it provides more data to assess your credit management habits. If you have a limited credit history, it could be a factor contributing to your credit score not increasing.

- Credit Mix: Having a diverse mix of credit accounts, such as credit cards, installment loans, and mortgages, can positively impact your credit score. It shows that you can handle different types of credit responsibly. If you have only one type of credit account, it may be a reason why your credit score is not increasing significantly.

- Recent Credit Inquiries: When you apply for new credit, a hard inquiry is placed on your credit report. Multiple hard inquiries within a short period can lower your credit score. It is important to be cautious when applying for new credit and consider the potential impact on your credit score.

These factors are interconnected and collectively contribute to your credit profile and overall creditworthiness. Analyzing these factors can help in identifying potential areas for improvement to boost your credit score. It’s important to note that some factors carry more weight than others, and their impact on your credit score may vary based on individual circumstances.

Now that we have explored the key factors affecting credit scores, the next step is to dive deeper into each factor and understand how it can impact your credit score. By doing so, we can uncover why your credit score may not be increasing and take appropriate steps to address the underlying issues.

Payment History

Your payment history is the most crucial factor that affects your credit score. Lenders want to see a strong track record of making payments on time, as it reflects your ability to manage credit responsibly.

If you have late payments, defaults, or accounts in collections, it can seriously impact your credit score and make it difficult to increase it. Even a single late payment can have a negative effect on your credit score, especially if it is recent.

To improve your payment history and boost your credit score:

- Pay your bills on time: Make it a priority to pay all your bills, including credit cards, loans, and utilities, on or before the due date. Consider setting up automatic payments or reminders to ensure you never miss a payment.

- Catch up on past due payments: If you have any accounts with late payments, bring them current as soon as possible. Contact your creditors and work out a repayment plan, if necessary, to rectify any past delinquencies.

- Avoid collections and defaults: If you have any accounts that have been sent to collections or are in default, it’s important to address them promptly. Paying off or settling these accounts can help improve your credit score over time.

Keep in mind that negative information, such as late payments, can remain on your credit report for up to seven years. However, the impact on your credit score lessens over time as newer positive information is added to your credit history.

By maintaining a consistent track record of timely payments and addressing any past delinquencies, you can positively impact your payment history and increase your credit score over time.

Credit Utilization

Credit utilization refers to the percentage of your available credit that you are currently using. It is an important factor that impacts your credit score. Lenders prefer to see a low credit utilization as it indicates responsible credit management.

If your credit utilization is high, meaning you are using a significant portion of your available credit, it can negatively affect your credit score and hinder its increase. High credit utilization can signal financial stress and a higher risk of default to lenders.

To improve your credit utilization and boost your credit score:

- Keep your credit card balances low: Try to keep your credit card balances as low as possible relative to your total credit limit. Aim to keep your credit utilization below 30%, but lower is generally better. Paying off your credit card balances in full each month is recommended.

- Consider increasing your credit limit: If you have a good payment history and a low credit utilization ratio, you can contact your credit card issuer to request a credit limit increase. This can help lower your credit utilization ratio and potentially improve your credit score.

- Avoid closing unused credit accounts: Closing a credit account may decrease your available credit limit, thus increasing your credit utilization ratio. Instead, consider keeping the account open and occasionally making small purchases to keep it active.

It’s important to note that credit utilization is reported to credit bureaus on a monthly basis. So, even if you pay off your credit card balances in full each month, the balance at the time of reporting can impact your credit utilization ratio. To minimize the impact, you can make multiple payments throughout the month or request a mid-cycle balance update from your credit card issuer.

By actively managing your credit card balances and keeping your credit utilization ratio low, you can improve your credit utilization and increase your credit score over time.

Length of Credit History

The length of your credit history is an essential factor that lenders consider when evaluating your creditworthiness. It reflects your experience with credit and shows how well you have managed it over time. Having a longer credit history can positively impact your credit score.

If your credit history is relatively short, it may be a reason why your credit score is not increasing as expected. Lenders prefer to see a substantial track record of responsible credit management to assess your repayment behavior and financial stability.

To improve the length of your credit history and potentially boost your credit score:

- Maintain older credit accounts: Keeping your long-standing credit accounts open can help increase the average age of your credit history. Closing old accounts can shorten your credit history and potentially impact your credit score.

- Do not open too many new accounts: Opening several new credit accounts within a short period can lower the average age of your credit history. Avoid unnecessary new credit inquiries unless required, as they can temporarily impact your credit score.

- Be patient: Building a credit history takes time. It’s important to consistently demonstrate responsible credit behavior by making timely payments and managing your credit accounts wisely. Over time, your credit history will lengthen, contributing to an improved credit score.

It’s worth noting that the impact of credit history length on your credit score lessens as your credit history becomes more established. However, maintaining a longer credit history gives lenders more data to assess your creditworthiness and can positively impact future credit applications.

By being patient and maintaining a track record of responsible credit behavior, you can improve the length of your credit history and potentially increase your credit score over time.

Credit Mix

The credit mix refers to the different types of credit accounts you have, such as credit cards, loans, mortgages, and other forms of credit. It is another factor that affects your credit score. Having a diverse mix of credit accounts can have a positive impact on your credit score.

If your credit mix is limited, it may be a reason why your credit score is not increasing as expected. Lenders want to see that you can handle various types of credit responsibly, as it demonstrates your ability to manage different financial obligations.

To improve your credit mix and potentially boost your credit score:

- Consider different types of credit accounts: If you have only one type of credit account, such as only credit cards, it may be beneficial to diversify your credit mix. This can be achieved by responsibly managing different forms of credit, such as obtaining an installment loan or a line of credit.

- Use caution when taking on new credit: While it’s important to have a diverse credit mix, it’s equally important to be cautious when applying for new credit. Only take on new credit accounts if necessary and ensure that you can responsibly manage the new obligations.

- Do not open unnecessary accounts: Opening new credit accounts just to diversify your credit mix can have negative consequences. It can result in additional credit inquiries and potentially lower your credit score temporarily.

Remember, the credit mix is just one factor among many that determine your credit score. It is not necessary to have every type of credit account to have a good credit score. Responsible management of the credit accounts you do have is paramount.

By diversifying your credit mix over time and demonstrating responsible credit behavior, you can improve your credit mix and potentially increase your credit score.

Recent Credit Inquiries

Recent credit inquiries, also known as credit applications, occur when you apply for new credit, such as a loan, credit card, or line of credit. While each credit inquiry may have a minimal impact on your credit score, multiple inquiries within a short period can have a negative effect and may be a reason why your credit score is not increasing.

When lenders see numerous recent credit inquiries on your credit report, it can signal a potential financial risk. It may indicate that you are taking on a significant amount of new credit or facing financial difficulties.

To manage your recent credit inquiries and potentially boost your credit score:

- Limit new credit applications: Be selective when applying for new credit. Evaluate whether you truly need the new credit account and consider the potential impact on your credit score. Avoid multiple credit applications within a short period.

- Shop for credit within a focused timeframe: Understand that when you are shopping for the best loan or credit card rates, multiple inquiries by different lenders within a specific period are usually treated as a single inquiry. This allows you to compare offers without significantly impacting your credit score.

- Monitor your credit report: Regularly review your credit report to ensure that all inquiries listed are accurate. If you notice any unauthorized or incorrect inquiries, dispute them with the credit bureaus to have them removed from your report.

It’s important to note that certain types of inquiries, such as those made by yourself for personal information or by employers for background checks, do not impact your credit score since they are classified as soft inquiries.

By being mindful of your credit applications and strategically managing new credit inquiries, you can minimize their impact on your credit score and potentially increase it over time.

Monitoring Credit Score

Monitoring your credit score is an essential practice for understanding your creditworthiness and ensuring the accuracy of the information reported by credit bureaus. Regularly monitoring your credit score can help you identify any inconsistencies or potential issues that may be preventing your credit score from increasing.

Here are some steps to effectively monitor your credit score:

- Check your credit report regularly: Obtain a copy of your credit report from each of the three major credit bureaus (Experian, TransUnion, and Equifax) at least once a year. Review the report thoroughly for any errors, inaccuracies, or signs of fraudulent activity.

- Sign up for credit monitoring services: Consider enrolling in a credit monitoring service or utilizing free credit score tracking tools to keep a close eye on your credit score. These services notify you of any significant changes in your credit report, such as new accounts, inquiries, or negative information.

- Monitor for potential identity theft: Regularly monitor your credit report for any suspicious activity or unauthorized accounts. Identity theft can negatively impact your credit score and overall financial well-being, so it’s important to address any signs of fraudulent activity promptly.

- Understand factors impacting your credit score: When you monitor your credit score, pay attention to the various factors that contribute to its calculation. Assess how these factors may be affecting your score and identify areas for improvement.

- Use credit score simulators: Some credit monitoring services offer credit score simulators that allow you to see how certain actions, such as paying off a debt or opening a new credit card, may impact your credit score. Utilize these tools to gain insights into potential strategies for raising your credit score.

By staying vigilant and regularly monitoring your credit score, you can stay informed about your financial standing and take proactive steps to address any issues that may be hindering your credit score from increasing.

Keep in mind that improving your credit score takes time and consistent effort. By actively monitoring and managing your credit, you can navigate towards a stronger credit profile and achieve your financial goals.

Reasons for Credit Score Not Increasing

There can be several reasons why your credit score is not increasing as expected. It’s important to identify these factors to understand the specific areas that may be impacting your creditworthiness. Here are some common reasons why your credit score may not be increasing:

- Late Payments: One of the significant contributors to a stagnant credit score is the presence of late payments. Consistently missing or making late payments can have a detrimental effect on your credit score. It’s essential to make payments on time to establish a track record of responsible payment behavior.

- High Credit Utilization: If your credit card balances are consistently close to or above the credit limit, it can negatively impact your credit score. High credit utilization suggests a greater risk of default to lenders, making it difficult for your credit score to increase. Aim to keep your credit utilization below 30% to maintain a healthy credit score.

- Lack of Credit History: If you have a limited credit history or are relatively new to credit, it may be challenging to see significant increases in your credit score. Building and establishing a positive credit history takes time. It’s important to consistently demonstrate responsible credit behavior and avoid any negative marks on your credit report.

- Limited Credit Mix: Having a narrow range of credit accounts, such as only credit cards or only installment loans, can impact your credit score. Lenders prefer to see a diverse mix of credit accounts to assess your ability to handle different types of credit. Consider adding different types of credit accounts to improve your credit mix and potentially increase your credit score.

- New Credit Inquiries: Applying for too much new credit within a short period can raise concerns among lenders and lead to a lower credit score. Each hard inquiry can have a temporary negative impact on your credit score. Be mindful of the number of credit applications you submit and space them out strategically when necessary.

- Errors on Credit Report: Mistakes or errors on your credit report can have an adverse effect on your credit score. It’s crucial to regularly review your credit report to identify any inaccuracies or fraudulent activity. Dispute any errors with the credit bureaus to have them corrected and potentially improve your credit score.

It’s important to recognize that improving your credit score is a gradual process. It requires consistent and responsible credit behavior over time. By addressing these common reasons for a stagnant credit score, you can make targeted improvements and work towards increasing your credit score for better financial opportunities in the future.

Late Payments

One of the significant factors that can hinder the increase of your credit score is the presence of late payments. Paying bills late or missing payments altogether can have a detrimental effect on your creditworthiness and make it difficult to see improvements in your credit score.

Late payments are reflected in your credit report and can stay on your credit history for up to seven years, depending on the severity of the delinquency. They are considered negative marks and can lower your credit score, especially if they are recent or frequent.

To avoid late payments and improve your credit score:

- Create a budget and set reminders: Develop a monthly budget to ensure you allocate enough funds to cover your bills and credit obligations. Set up reminders or automatic payments to help you stay on top of due dates.

- Establish an emergency fund: Having an emergency fund can provide a financial cushion to handle unexpected expenses or hardships, reducing the likelihood of falling behind on payments.

- Communicate with creditors: If you are unable to make a payment on time, it’s essential to communicate with your creditors. Contact them as soon as possible to explain the situation and explore possible solutions, such as setting up a payment plan.

- Consider automatic payments: Automating your payments can ensure that your bills are consistently paid on time. However, it is crucial to monitor your accounts and make sure you have sufficient funds to cover the payments.

- Address any financial difficulties: If you are struggling to make payments due to financial hardships, such as job loss or medical expenses, seek assistance and explore options for debt restructuring or refinancing.

Remember, late payments can have a lasting impact on your credit score, but the effect diminishes over time as you establish a pattern of on-time payments. By consistently paying your bills on time and avoiding late payments, you can gradually improve your payment history and increase your credit score.

High Credit Utilization

Having a high credit utilization ratio can significantly impact your credit score and be a reason why your credit score is not increasing. Credit utilization refers to the percentage of your available credit that you are currently using.

Lenders consider high credit utilization as a sign of potential financial strain or over-reliance on credit. A high utilization ratio can negatively affect your credit score and hinder its growth, even if you make payments on time.

To improve your credit utilization and potentially increase your credit score:

- Pay down credit card balances: Focus on reducing the outstanding balances on your credit cards. Aim to keep your credit card balances well below their credit limits. Paying off credit card debt can have a positive impact on your credit utilization ratio.

- Monitor credit limits and utilization: Keep a close eye on your credit limits and ensure they are accurately reported. If your credit limits increase or you pay down balances, the utilization ratio can improve, potentially leading to an increase in your credit score.

- Consider spreading out credit card usage: If you have multiple credit cards, try distributing your spending across them instead of maxing out a single card. This can help keep individual card balances lower and improve your overall credit utilization.

- Avoid closing unused credit accounts: Closing a credit account may decrease your available credit, which can negatively impact your credit utilization ratio. Instead, consider keeping those accounts open, especially if they have a long and positive credit history.

- Request a credit limit increase: Contact your credit card issuers and inquire about a credit limit increase. A higher credit limit can lower your credit utilization ratio, assuming you maintain the same level of spending.

It’s important to note that maintaining a low credit utilization ratio is a continuous effort. Regularly monitoring your credit utilization and keeping it as low as possible can contribute to improving your credit score over time.

By actively managing your credit card balances and striving to keep your credit utilization ratio low, you can positively impact your credit score and improve your overall creditworthiness.

Lack of Credit History

If you have a limited credit history, it may be a reason why your credit score is not increasing as expected. Lenders rely on your credit history to assess your creditworthiness and determine the level of risk associated with lending to you.

Building a strong credit history takes time and demonstrates your ability to manage credit responsibly. Without a robust credit history, it can be challenging for lenders to gauge your creditworthiness, resulting in a stagnant credit score.

To overcome the lack of credit history and potentially increase your credit score:

- Open a starter credit account: Consider opening a secured credit card or a credit-builder loan to establish a positive credit history. These types of accounts are designed for individuals with limited or no credit history.

- Become an authorized user: Ask a family member or close friend with a strong credit history and responsible credit behavior to add you as an authorized user on one of their credit accounts. This can help you benefit from their positive credit history and build your own.

- Pay bills on time: Even if certain bills, such as rent or utilities, are not typically reported to credit bureaus, establishing a habit of timely payments can lay the foundation for a positive credit history. Some services allow you to report rental payments to credit bureaus, further enhancing your credit file.

- Monitor your credit: Regularly review your credit report to ensure that any accounts you have opened are being reported accurately and to identify any potential errors. Monitoring your credit allows you to stay informed about changes and progress in your credit history.

- Practice responsible credit habits: Be mindful of your spending habits and avoid taking on more credit than you can comfortably handle. Make timely payments, keep credit card balances low, and demonstrate responsible financial behavior to build a positive credit history.

Building a credit history is a gradual process. It takes time and consistent effort to establish a solid foundation. By taking proactive steps to build your credit, you can improve your creditworthiness and increase your credit score over time.

Limited Credit Mix

If you have a limited credit mix, it may be a reason why your credit score is not increasing as expected. Lenders consider your credit mix when assessing your creditworthiness as it indicates your ability to manage different types of credit.

Having a diverse mix of credit accounts, such as credit cards, loans, and mortgages, can have a positive impact on your credit score. It demonstrates that you can handle various types of credit obligations responsibly.

To address a limited credit mix and potentially increase your credit score:

- Consider different types of credit: Explore opportunities to diversify your credit mix. This can be achieved by applying for different types of credit accounts, such as an installment loan, a store credit card, or a secured credit card.

- Become an authorized user: Ask a family member or close friend with a diverse credit mix and a positive credit history to add you as an authorized user on one of their credit accounts. This can help enhance your own credit mix without taking on new debt.

- Manage credit accounts responsibly: Once you have diversified your credit mix, make sure to manage all your credit accounts responsibly. Make timely payments, keep balances low, and avoid opening unnecessary new credit accounts. Responsible credit management is key to improving your credit score.

- Be patient: Building a robust credit mix takes time. It’s important to be patient and allow sufficient time for your credit history to reflect the diversity of your credit accounts. Continue practicing good credit habits, and over time, your credit mix will strengthen.

Remember, having a limited credit mix does not automatically mean your credit score will be low. It is just one of many factors considered. However, diversifying your credit mix can provide more comprehensive information to lenders when assessing your creditworthiness.

By actively seeking opportunities to diversify your credit mix and responsibly managing your credit accounts, you can potentially increase your credit score and demonstrate your ability to handle various types of credit.

New Credit Inquiries

If you have recently applied for new credit, it may be a reason why your credit score is not increasing as expected. When you apply for new credit, a hard inquiry is recorded on your credit report, indicating that you are seeking additional credit. While a single inquiry has a minimal impact, multiple inquiries within a short period can negatively affect your credit score.

Lenders view multiple recent inquiries as a potential sign of financial distress or a sudden increase in debt. These inquiries can lower your credit score because they suggest a higher risk of default.

To manage new credit inquiries and potentially increase your credit score:

- Be selective when applying for new credit: Avoid applying for multiple credit accounts within a short period. It’s important to carefully evaluate whether new credit is necessary and consider the potential impact on your credit score before submitting applications.

- Shop for credit within a focused timeframe: When applying for loans or credit cards, try to do so within a specific period. Credit scoring models typically group similar inquiries made within a certain window as a single inquiry, minimizing the impact on your credit score.

- Monitor for unauthorized inquiries: Regularly review your credit report for any unfamiliar or unauthorized inquiries. If you notice any unauthorized inquiries, contact the credit bureaus to have them investigated and removed from your credit report.

- Limit rate shopping: While it’s important to compare offers and find the best terms, limit rate shopping to a reasonable timeframe. For example, if you’re applying for a mortgage or an auto loan, submit your applications within a short window to minimize the impact on your credit score.

- Focus on building a positive credit history: Rather than seeking out new credit, concentrate on maintaining a positive payment history and responsible credit behavior. Over time, as you build a strong credit history, the impact of recent inquiries will lessen.

It’s essential to note that not all inquiries will have a significant impact on your credit score, especially over time. The negative impact of inquiries fades as newer positive information is added to your credit history.

By being mindful of your credit applications, strategically managing new inquiries, and focusing on responsible credit behavior, you can minimize the impact of new credit inquiries on your credit score and work towards increasing it over time.

Errors on Credit Report

Errors on your credit report can be a significant factor preventing your credit score from increasing. Inaccurate information or fraudulent activity can have a negative impact on your creditworthiness and hinder your efforts to improve your credit score.

It’s important to regularly review your credit report to identify any errors or discrepancies. Here’s how you can address errors on your credit report:

- Obtain copies of your credit reports: Request copies of your credit reports from each of the three major credit bureaus – Experian, TransUnion, and Equifax. Review them thoroughly to identify any errors or inconsistencies.

- Identify potential errors: Pay close attention to personal information, account details, payment history, and any negative or fraudulent activities listed on your credit report. Look for discrepancies or unfamiliar accounts that may indicate errors or unauthorized activity.

- Dispute errors with the credit bureaus: If you find any errors, file a dispute with the credit bureau reporting the inaccurate information. Provide any supporting documentation, such as receipts or statements, to help substantiate your claim. The credit bureau is required to investigate and correct any errors within a reasonable timeframe.

- Notify the relevant creditors: In addition to disputing errors with the credit bureaus, directly contact the creditors associated with the inaccurate information. Provide them with the details of the error and any supporting documentation. They are responsible for investigating and rectifying inaccurate reporting to the credit bureaus.

- Monitor changes and follow up: After disputing errors, monitor your credit reports to ensure that the corrections are made. Follow up with both the credit bureau and the creditors if necessary to ensure the inaccuracies are resolved.

It’s worth noting that the process of disputing errors on your credit report can take time. However, addressing and rectifying these errors is crucial for the accuracy of your credit profile and the improvement of your credit score.

By regularly reviewing your credit reports, identifying and disputing errors promptly, and following up on the resolution of inaccuracies, you can ensure the accuracy of your credit information and increase your credit score over time.

Improving Your Credit Score

If your credit score is not increasing as desired, taking proactive steps to improve it is within your control. Here are some strategies you can implement to work towards increasing your credit score:

- Pay your bills on time: Consistently making on-time payments is crucial for improving your credit score. Set up payment reminders or automated payments to ensure you never miss a due date.

- Lower your credit utilization: Aim to keep your credit card balances low. Pay off debt and avoid maxing out your credit cards to maintain a healthy credit utilization ratio.

- Build a credit history: If you have limited or no credit history, establish credit by opening a starter credit account, becoming an authorized user, or reporting rental payments. This helps demonstrate your creditworthiness to lenders.

- Diversify your credit mix: Seek opportunities to diversify your credit mix by obtaining different types of credit accounts. This shows lenders your ability to handle multiple forms of credit responsibly.

- Be cautious with new credit inquiries: Avoid excessive credit applications within a short period, as they can negatively impact your credit score. Only apply for new credit when necessary, and be mindful of the potential consequences.

- Regularly review your credit report: Stay vigilant by monitoring your credit report for errors or fraudulent activity. Dispute any inaccuracies and follow up to ensure they are resolved.

- Manage your debts responsibly: Maintain a responsible approach to managing your debts. Make payments on time, avoid accruing new debt unnecessarily, and pay off existing debts systematically.

- Be patient and consistent: Building a solid credit profile takes time. Be patient and consistent in your efforts to practice responsible credit habits, as positive financial behavior over time will reflect in an increased credit score.

Remember, improving your credit score is a gradual process. It requires consistent effort, responsible financial behavior, and time to see significant changes. By implementing these strategies and adopting healthy credit management practices, you can gradually improve your credit score and strengthen your financial standing.

Paying Bills on Time

One of the most essential steps you can take to improve your credit score is to consistently pay your bills on time. Payment history is a crucial factor in determining your creditworthiness, accounting for a significant portion of your credit score. Here are some tips for paying bills on time:

- Set up reminders: Utilize electronic reminders, such as calendar alerts or mobile apps, to ensure you never miss a due date. This will help you stay organized and prompt you to make timely payments.

- Automate payments: If possible, set up automatic payments for your regular bills. This way, payments will be deducted from your designated account on the scheduled due date, reducing the risk of forgetting or paying late.

- Consider payment consolidation: Consolidate your bills to streamline the payment process. This can help you keep track of due dates more effectively and minimize the chances of missing any payments.

- Prioritize payments: If you’re unable to pay all your bills in full, prioritize essential payments, such as mortgage or rent, utilities, and minimum payments on your credit cards. Missing these payments can have a significant negative impact on your credit score.

- Communicate with creditors: If you’re facing financial challenges and are unable to make a payment, reach out to your creditors. Explain your situation and explore possibilities for temporary relief or alternative payment arrangements.

- Monitor and reconcile: Regularly check your bank account and credit card statements to ensure that payments are being processed correctly. Sometimes errors can occur, and it’s important to address them promptly to avoid any negative consequences.

- Develop a budget: Creating a budget can help you allocate funds for bill payments and other financial obligations. By understanding your income and expenses, you can better manage your cash flow and make timely payments.

Consistently paying your bills on time demonstrates to lenders that you are responsible and reliable when it comes to managing credit. Over time, this positive payment history will contribute to an improved credit score and enhance your overall creditworthiness.

Remember, paying bills on time is a fundamental step towards financial stability and creditworthiness. By prioritizing due dates, utilizing reminders, and automating payments, you can foster good payment habits that will positively impact your credit score.

Lowering Credit Utilization

Lowering your credit utilization is a crucial step in improving your credit score. Credit utilization refers to the percentage of your available credit that you are currently using. A high credit utilization ratio can negatively impact your credit score and suggest a higher risk to lenders. Here are some strategies to lower your credit utilization:

- Pay down existing balances: Focus on paying off your outstanding credit card balances. By reducing the amount you owe, you can lower your credit utilization ratio and potentially increase your credit score.

- Make multiple payments each month: Consider making multiple payments throughout the month, especially if your credit card issuers report balances at specific times. Spacing out payments can lower the balance reported to the credit bureaus, resulting in a lower credit utilization ratio.

- Request a credit limit increase: Contact your credit card issuer and ask for a credit limit increase. A higher credit limit means you have more available credit, which can lower your credit utilization ratio as long as your spending remains consistent.

- Keep credit cards open: Closing credit card accounts can reduce your available credit and potentially increase your credit utilization ratio. Instead, consider keeping these accounts open, even if you no longer actively use them, to maintain a lower overall credit utilization ratio.

- Pay off balances in full each month: Whenever possible, pay off your credit card balances in full every month. This allows you to avoid accruing interest and keeps your credit utilization ratio as low as possible.

- Reduce spending: Limit discretionary spending and avoid unnecessary purchases to prevent your credit card balances from increasing. Consciously managing your spending habits can help maintain a low credit utilization ratio.

- Monitor credit utilization: Regularly monitor your credit card balances and credit utilization ratio. Staying aware of your utilization rate can help you make informed decisions and take necessary actions to lower it if it starts increasing.

Lowering your credit utilization demonstrates responsible credit management to lenders and can have a positive impact on your credit score. By actively working to decrease your credit card balances and keeping your credit utilization ratio low, you can improve your creditworthiness and increase your credit score over time.

Remember, maintaining a low credit utilization ratio is an ongoing effort. By consistently managing your credit card balances and keeping them as low as possible, you can positively impact your credit utilization and enhance your overall credit profile.

Building a Credit History

Building a solid credit history is essential for improving your credit score and establishing your creditworthiness. If you have a limited credit history or are new to credit, there are steps you can take to start building a positive credit history. Here’s how you can build your credit history:

- Open a starter credit account: Consider applying for a secured credit card or a credit card designed for individuals with limited credit history. Use it responsibly, making small purchases and paying off the balance in full each month.

- Become an authorized user: Ask a family member or a close friend with a good credit history to add you as an authorized user on one of their credit accounts. This allows you to benefit from their positive credit history and establish your own.

- Report rental payments: Some services allow you to report your rental payments to credit bureaus. By reporting your consistent and on-time rent payments, you can demonstrate responsible financial behavior and enhance your credit history.

- Apply for a credit-builder loan: Credit-builder loans are specifically designed to help individuals build credit. These loans require you to make regular payments, helping you establish a positive payment history.

- Pay bills on time: Although not all bills are typically reported to credit bureaus, consistently making on-time payments can establish a pattern of responsible payment behavior, which is beneficial for building your credit history.

- Limit credit applications: Be selective when applying for new credit. Multiple credit applications within a short period can be seen as a potential financial risk. Only apply for credit when necessary to avoid negative impacts on your credit history.

- Practice responsible credit habits: Build a solid credit history by using credit responsibly. This includes making timely payments, keeping balances low, and avoiding unnecessary debt. Responsible credit management is key to establishing and maintaining a positive credit history.

Building a credit history takes time and consistency. As you establish a positive payment history and demonstrate responsible credit habits, your creditworthiness will improve, and lenders will have more confidence in extending credit to you.

Remember, building a credit history is a journey. By actively taking steps to establish credit, making timely payments, and practicing responsible credit habits, you can build a solid credit history and increase your creditworthiness over time.

Diversifying Credit Mix

A diverse credit mix is an important factor in determining your creditworthiness and can positively impact your credit score. Lenders prefer to see that you can handle different types of credit responsibly. If your credit mix is limited, it may be hindering the increase of your credit score. Here are some strategies to diversify your credit mix:

- Apply for different types of credit accounts: Consider applying for different types of credit accounts, such as credit cards, personal loans, or a mortgage. Having a mix of revolving credit (credit cards) and installment credit (loans) can showcase your ability to handle various forms of credit.

- Seek opportunities to add new credit: Look for opportunities to add new credit accounts sparingly. However, it’s important not to open too many new accounts within a short period, as this can negatively impact your credit score. Only apply for the credit you need and can manage responsibly.

- Keep existing credit accounts open: Closing unused credit accounts may reduce your available credit and potentially decrease your credit mix diversity. Unless there are compelling reasons to close an account, consider keeping it open to contribute to your credit mix and length of credit history.

- Apply for a secured credit card: If you have a limited credit history or difficulty qualifying for traditional credit cards, a secured credit card can be a great option. It requires a security deposit, and your credit limit is typically equal to the deposited amount. Responsible use of a secured card can help establish a positive credit history.

- Become an authorized user on someone else’s account: Ask a family member or close friend with good credit to add you as an authorized user on one of their accounts. You can benefit from their positive credit history, which can help diversify your credit mix.

Keep in mind that diversifying your credit mix should be done cautiously and responsibly. It’s important to manage all credit accounts wisely, making timely payments, and keeping balances low to maintain a healthy credit profile.

By actively seeking opportunities to diversify your credit mix, you can demonstrate your ability to handle different types of credit responsibly. Over time, this can contribute to an improved credit score and enhance your overall creditworthiness.

Being Cautious with New Inquiries

When it comes to new credit inquiries, exercising caution is crucial to protect your credit score and maintain a healthy credit profile. Each time you apply for new credit, such as a loan or credit card, a hard inquiry is added to your credit report. Multiple inquiries within a short period can negatively impact your credit score. Here are some tips for being cautious with new inquiries:

- Apply for credit when necessary: Only apply for new credit when it’s necessary and fits within your financial goals. Be selective and avoid submitting credit applications for every offer you receive, as each inquiry can have an impact on your credit score.

- Research and compare before applying: Before applying for credit, take the time to research and compare different lenders and offers. This way, you can make an informed decision and choose the best option that suits your needs without unnecessary credit applications.

- Space out credit applications: If you need to apply for multiple types of credit, such as a mortgage and a car loan, space out the applications over a reasonable period. This can help minimize the impact of multiple inquiries on your credit score.

- Avoid unnecessary credit inquiries: Be cautious when prompted to apply for additional credit at the point of sale, such as retail store credit cards. While these offers may provide benefits, it’s important to evaluate whether they align with your overall financial goals and credit needs.

- Monitor your credit: Regularly monitor your credit report to keep track of inquiries and ensure they are accurate. If you notice any unauthorized inquiries, report them immediately to the credit bureaus to have them investigated and removed.

Remember, while credit inquiries have a temporary impact on your credit score, it’s important to be cautious and selective when seeking new credit. Being mindful of the number of inquiries can help you maintain a healthier credit profile and increase your chances of achieving your financial goals.

By practicing restraint and being proactive in managing your credit inquiries, you can minimize potential negative effects on your credit score and maintain a stable credit history.

Correcting Errors on Credit Report

Reviewing and correcting errors on your credit report is vital for maintaining an accurate credit history and ensuring that your credit score is not unduly affected. Mistakes or inaccuracies can lower your credit score and may even impact your ability to obtain credit. To correct errors on your credit report, take the following steps:

- Regularly review your credit report: Obtain a copy of your credit report from each of the major credit bureaus—Experian, TransUnion, and Equifax. Carefully review the report, paying close attention to account details, personal information, and any discrepancies.

- Identify errors: Look for any errors or inaccuracies, such as incorrect personal information, accounts you don’t recognize, or duplicate entries. Additionally, watch out for any negative items that have exceeded the legally allowed reporting time.

- Document the errors: Gather any evidence or supporting documentation that proves the inaccuracies on your credit report. This may include billing statements, loan agreements, or any other relevant paperwork.

- Dispute the errors: Submit a dispute letter to the credit bureau(s) reporting the errors. Include specific details about the inaccuracies and provide copies of supporting documentation as proof. You can usually initiate a dispute online, through the credit bureau’s website, or by mail.

- Communicate with creditors: In addition to disputing with the credit bureaus, contact the creditors associated with the inaccuracies. Provide them with the same information and supporting documentation, requesting that they update their records and report accurate information to the credit bureaus.

- Follow up and stay organized: Keep records of all communications, including dates, names of individuals spoken to, and copies of all correspondence. Follow up regularly with both the credit bureaus and creditors to ensure that the errors are being investigated and corrected.

- Monitor your credit report: After disputing errors, continue to monitor your credit report to ensure that the corrections have been made. It’s recommended to review your credit report at least once a year to catch any new errors that may arise.

Correcting errors on your credit report is crucial to maintaining an accurate credit history. By being proactive and thorough in identifying and disputing inaccuracies, you can ensure the information presented to lenders is correct and maintain a healthier credit profile.

Remember, it may take time for errors to be resolved, so be patient throughout the process. By persistently advocating for accurate reporting, you can help protect your creditworthiness and maintain an up-to-date credit report.

Conclusion

Improving your credit score requires a combination of understanding the factors that influence it and taking proactive steps to enhance your creditworthiness. Throughout this article, we have discussed various reasons why your credit score may not be increasing as expected.

Factors such as late payments, high credit utilization, a limited credit history, a lack of credit mix, new credit inquiries, and errors on your credit report can all contribute to a stagnant credit score. However, by addressing these factors and implementing the recommended strategies, you can work towards boosting your credit score and achieving your financial goals.

Paying bills on time, managing credit utilization, building a credit history, diversifying your credit mix, being cautious with new inquiries, and correcting errors on your credit report are all key steps to improving your credit score.

Remember, improving your credit score is a gradual process that requires consistent effort and responsible financial behavior. Don’t get discouraged if you don’t see immediate results. Patience and persistence will pay off in the long run as you establish a strong credit profile.

By implementing the tips and strategies outlined in this article, you can take control of your credit and work towards a healthier credit score. Monitor your credit, make responsible financial decisions, and stay proactive in managing your credit history. Over time, your creditworthiness will improve, opening doors to better financial opportunities.

Building and maintaining good credit is an ongoing process. Regularly assess your financial habits, stay vigilant, and adapt as needed. With perseverance and a commitment to responsible credit management, you can achieve a higher credit score and enjoy the benefits that come with it.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance