Finance

Why Is Prepaid Insurance An Asset?

Modified: March 1, 2024

Learn the importance of prepaid insurance as an asset in finance. Understand why businesses strategically allocate funds for insurance coverage.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

Introduction

When it comes to managing finances, insurance plays a crucial role in protecting assets and mitigating risks. One commonly encountered term in the world of insurance is “prepaid insurance.” But what exactly is prepaid insurance and why is it considered an asset?

Prepaid insurance refers to the payment made by an individual or a business to an insurance company for coverage that extends beyond the current accounting period. In other words, it is an arrangement where insurance premiums are paid in advance to ensure coverage for a specified period. This prepayment period can range from a few months to several years, depending on the terms of the insurance policy.

Assets, in financial terms, are resources owned by an individual or a company that hold economic value and can be converted into cash or provide future benefits. Common examples of assets include cash, property, and investments. But how does prepaid insurance fit into this category?

An asset is typically characterized by its ability to generate economic benefits. In the case of prepaid insurance, it becomes an asset because it provides future protection and coverage against potential risks and losses. It acts as a safety net for unexpected events, such as accidents, natural disasters, or other liabilities.

Now that we understand the definition of prepaid insurance and the concept of assets, let’s dive deeper into why prepaid insurance is considered an asset.

Definition of Prepaid Insurance

Prepaid insurance refers to the payment made by an individual or a business to an insurance company in advance for insurance coverage that extends beyond the current accounting period. It is a way to secure protection and coverage against potential risks and losses in the future. The insurance premium paid is allocated to a specific period, during which the insurance policy is effective.

Typically, prepaid insurance is recorded as an asset on the balance sheet of the entity purchasing the insurance. This is because the prepayment of insurance premiums represents a resource with future benefits. The amount paid for the insurance coverage is considered an asset until it is used up or its coverage expires.

It is important to note that prepaid insurance is different from regular insurance payments. Regular insurance payments, such as monthly premiums, are expensed as they are incurred and do not count as assets. Prepaid insurance, on the other hand, involves a lump sum payment made in advance for coverage that extends beyond the current period.

The duration of prepaid insurance can vary depending on the terms of the insurance policy. It can be as short as a few months or as long as several years. The specific duration and coverage details are outlined in the insurance contract between the policyholder and the insurance company.

Prepaid insurance can be applicable to various types of insurance coverage, including property insurance, liability insurance, health insurance, and auto insurance, among others. It provides a level of financial security and peace of mind by ensuring that the insured party is protected against potential losses or damages during the specified coverage period.

Understanding the definition of prepaid insurance is essential for individuals and businesses to effectively manage their financial resources and protect their assets. By prepaying insurance premiums, they can secure future coverage, alleviate potential risks, and maintain financial stability.

Understanding Assets

In the realm of finance, assets are resources or properties owned by an individual or a company that hold economic value and can be converted into cash or provide future benefits. They are essential elements of financial statements and play a crucial role in determining an entity’s financial position.

Assets can be classified into different categories based on their nature and characteristics. Common examples of assets include cash, investments, property, equipment, inventory, and accounts receivable. These assets are considered valuable and contribute to an entity’s overall wealth.

Assets can be further categorized into two main types: current assets and non-current assets. Current assets are those that are expected to be converted into cash or consumed within one year or the normal operating cycle of a business. Examples of current assets include cash, accounts receivable, and inventory. Non-current assets, on the other hand, are long-term assets that are not expected to be converted into cash or consumed within a short period. Examples of non-current assets include property, plant, and equipment, investments, and intangible assets.

Assets have several key characteristics. Firstly, they have economic value and can be bought, sold, or used to generate income. This means that assets have a monetary worth that can be quantified. Secondly, assets have a useful life, which refers to the duration over which they provide benefits or generate income. The useful life of an asset can vary depending on its nature and usage.

Another important characteristic of assets is their ability to generate future economic benefits. This means that assets are expected to contribute to an entity’s ability to generate cash flows or provide other financial advantages in the future. For example, rental property can generate rental income, while investments can appreciate in value.

Assets are recorded on the balance sheet of an entity, which is a financial statement that provides a snapshot of its financial position at a specific point in time. The balance sheet shows the value of an entity’s assets, liabilities, and owner’s equity. By analyzing the balance sheet, stakeholders can assess the financial health and stability of an entity.

Understanding assets is vital for individuals and businesses in managing their financial resources effectively. By identifying and properly managing assets, entities can make informed decisions, allocate resources efficiently, and maximize their financial well-being.

Why Prepaid Insurance is an Asset

Prepaid insurance is considered an asset because it holds economic value and provides future benefits to the policyholder. Here are a few reasons why prepaid insurance is classified as an asset:

- Protection and Coverage: Prepaid insurance ensures that the policyholder is protected against potential risks and losses. By paying in advance for insurance coverage, individuals and businesses secure a safety net for unexpected events, such as accidents, natural disasters, or liability claims.

- Future Economic Benefits: Unlike regular insurance payments, which are expensed as they are incurred, prepaid insurance offers coverage beyond the current accounting period. As a result, it represents a future economic benefit for the policyholder. The amount paid for prepaid insurance is an investment toward mitigating potential risks and safeguarding valuable assets.

- Resource with Value: Prepaid insurance represents a resource that holds economic value. The amount paid for the insurance coverage can be quantified and contributes to an entity’s overall wealth. As such, it meets the criteria of being an asset on the balance sheet.

- Convertible to Cash: In certain circumstances, prepaid insurance can be converted into cash. For example, if the policyholder decides to cancel or terminate the insurance policy, they may be eligible for a refund or a portion of the prepaid premium. This ability to convert the prepaid insurance into cash further enhances its classification as an asset.

- Enhances Financial Stability: Having prepaid insurance as an asset provides a sense of financial stability and security. It allows individuals and businesses to better manage potential risks and liabilities, ensuring that they are adequately covered in case of unforeseen events. This financial stability contributes to the overall well-being of the entity.

Overall, prepaid insurance is classified as an asset due to its ability to generate future economic benefits, its value as a resource, and its role in providing protection and coverage. By recognizing prepaid insurance as an asset, individuals and businesses can accurately assess their financial position and make informed decisions about managing their insurance needs.

Factors Contributing to Prepaid Insurance as an Asset

Several factors contribute to the classification of prepaid insurance as an asset:

- Payment in Advance: Prepaid insurance involves making a lump-sum payment in advance for insurance coverage that extends beyond the current accounting period. This payment is considered an asset because it represents a resource with future benefits. The prepaid premium is recognized as an asset until it is used up or its coverage expires.

- Future Protection and Coverage: By prepaying insurance premiums, individuals and businesses secure protection and coverage against potential risks and losses in the future. This foresight and proactive approach ensure that the policyholder is prepared for unexpected events that may result in financial strain. The future benefits of this protection contribute to the classification of prepaid insurance as an asset.

- Transferable Value: Prepaid insurance policies often have transferable value. If the policyholder decides to sell the insurance policy or transfer the coverage to another party, the prepaid premium can be reallocated or refunded. This transferability adds to the asset value of prepaid insurance.

- Insurance as a Controllable Resource: Prepaid insurance represents a controllable resource for individuals and businesses. By actively managing their insurance needs and making prepayments, entities can ensure that they have the necessary coverage in place and are protected in case of unexpected events. This level of control and flexibility further enhances the asset value of prepaid insurance.

- Reduction of Expenses: Prepaid insurance can also contribute to the reduction of expenses in the future. By prepaying insurance premiums, entities can spread out the cost over a defined period, potentially resulting in lower expenses and improved financial stability. This reduction in future expenses is an additional factor that supports the classification of prepaid insurance as an asset.

These factors collectively contribute to prepaid insurance being recognized as an asset. The ability to make payments in advance, secure future protection and coverage, transfer the value, maintain control over insurance needs, and potentially reduce expenses all contribute to the value of prepaid insurance as an asset on the balance sheet.

Importance of Prepaid Insurance as an Asset

Prepaid insurance serves as an important asset for individuals and businesses due to several key reasons:

- Financial Security: Prepaid insurance provides a sense of financial security by ensuring that individuals and businesses are protected against potential risks and losses. By prepaying insurance premiums, entities can minimize the financial impact of unexpected events, such as accidents, damages, or liability claims. This financial security contributes to overall peace of mind and stability.

- Protection of Assets: Assets are valuable resources that individuals and businesses work hard to acquire and maintain. Prepaid insurance helps protect these assets by providing coverage and compensation in case of damage, loss, or other liabilities. By having prepaid insurance as an asset, entities can safeguard their investments and minimize potential financial setbacks.

- Risk Mitigation: Every entity faces certain risks and uncertainties. Prepaid insurance acts as a risk management tool by mitigating potential risks. It allows individuals and businesses to transfer part of the risk to an insurance provider, reducing the financial burden associated with unexpected events. By managing and preemptively addressing risks, prepaid insurance helps maintain stability and continuity.

- Compliance Requirements: Depending on the industry and jurisdiction, certain entities may be required to carry specific insurance coverage. Prepaid insurance ensures compliance with legal and regulatory obligations. By having prepaid insurance as an asset, entities demonstrate their commitment to fulfilling these requirements, which is crucial for maintaining business operations and credibility.

- Financial Planning and Budgeting: Prepaid insurance facilitates effective financial planning and budgeting. By prepaying insurance premiums, entities can allocate resources in advance and incorporate insurance costs into their financial projections. This allows for better financial planning, expense management, and improved budgeting accuracy.

The importance of prepaid insurance as an asset cannot be overstated. It provides financial security, protects assets, mitigates risks, ensures compliance with regulations, and aids in financial planning. By recognizing prepaid insurance as an asset, individuals and businesses can make informed decisions, properly allocate resources, and maintain stability in the face of potential risks and uncertainties.

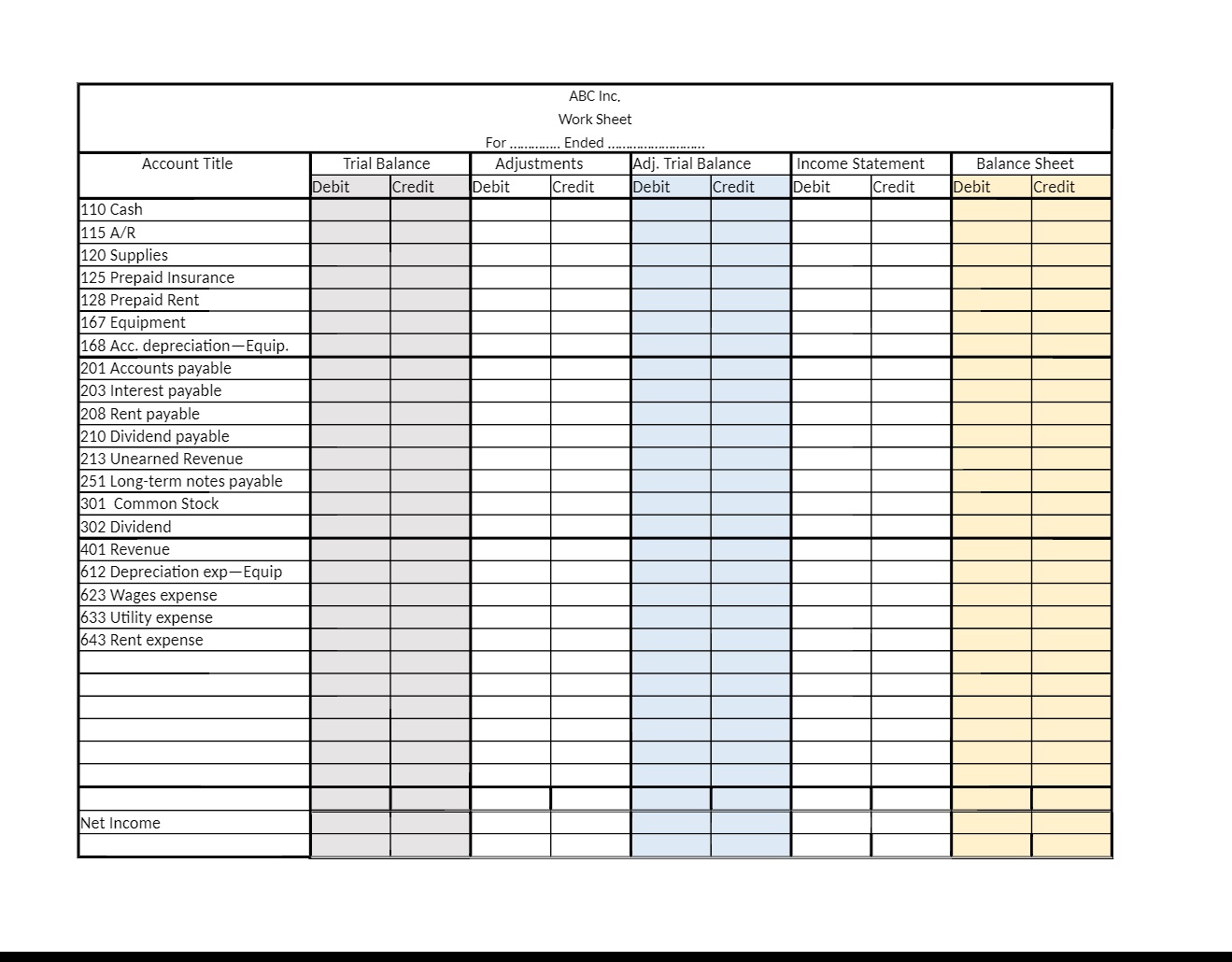

Prepaid Insurance as a Balance Sheet Item

Prepaid insurance is recorded as a balance sheet item because it represents an asset that holds economic value. The balance sheet is a financial statement that provides a snapshot of an entity’s financial position at a specific point in time.

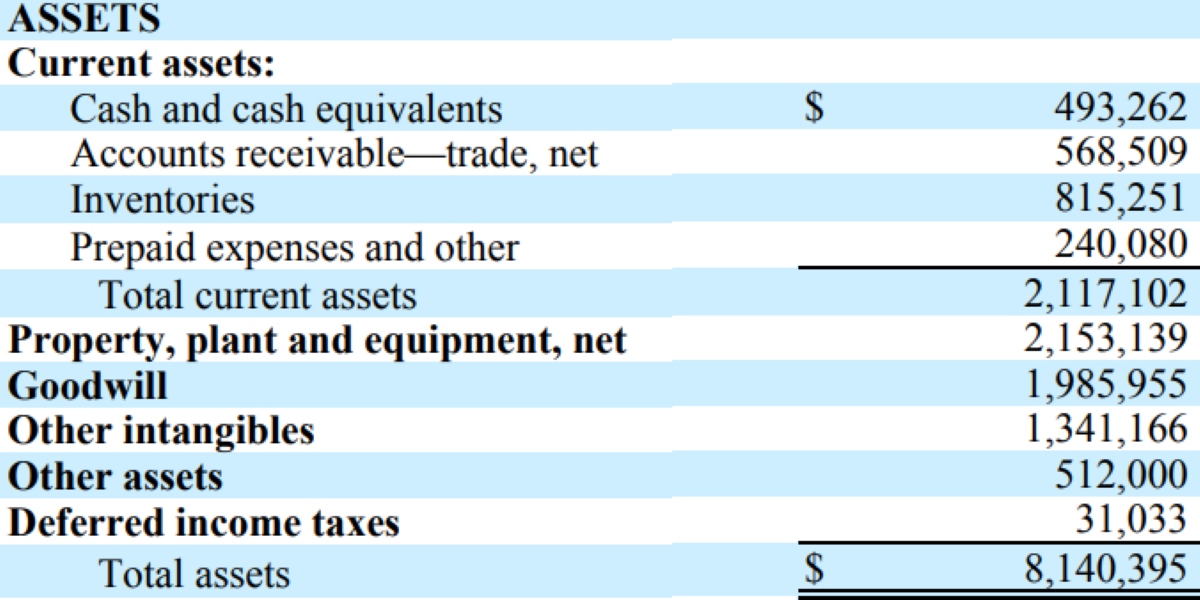

On the balance sheet, prepaid insurance is listed as a current asset if it will be consumed within one year or the normal operating cycle of a business. If the prepaid insurance coverage extends beyond the one-year mark, it is classified as a non-current asset.

The amount recorded as prepaid insurance on the balance sheet is typically the total premium paid for the coverage period. This amount is initially recognized as an asset because it represents a resource with future benefits.

As time passes and the coverage period progresses, the prepaid insurance is gradually recognized as an expense on the income statement. This recognition is done systematically over the duration of the insurance policy, typically on a monthly or quarterly basis. The portion of the prepaid insurance that has expired or been used up is expensed as insurance expense.

The balance sheet reflects the net value of prepaid insurance, which is the difference between the initial asset amount recorded and the portion that has been expensed over time. The net value of prepaid insurance is updated on the balance sheet regularly to reflect the remaining coverage period and the corresponding value of the asset.

It is important for entities to accurately account for prepaid insurance on the balance sheet to ensure proper assessment of their financial standing. In addition, proper accounting of prepaid insurance allows for informed decision-making, budgeting, and expense management.

By recording prepaid insurance as a balance sheet item, entities can clearly identify the value of the insurance coverage they have paid for in advance. This information is crucial for investors, creditors, and other stakeholders who evaluate the entity’s financial health and stability. It also provides transparency and accountability in financial reporting.

Overall, prepaid insurance as a balance sheet item highlights the value and importance of insurance coverage as an asset for entities. It allows for effective management of resources, assessment of financial position, and prudent decision-making.

Conclusion

Prepaid insurance serves as a valuable asset for individuals and businesses in managing their financial resources and mitigating risks. By making advance payments for insurance coverage, entities secure future protection and coverage against potential losses and liabilities.

Throughout this article, we have explored the definition of prepaid insurance and its classification as an asset. We have discussed how prepaid insurance provides economic value, offers future benefits, and acts as a controllable resource.

Prepaid insurance is an essential component of an entity’s balance sheet, where it is recorded as a current or non-current asset. It represents a financial safety net, providing financial security, protecting valuable assets, and mitigating potential risks.

Moreover, prepaid insurance plays a critical role in financial planning and budgeting. By prepaying insurance premiums, entities can allocate resources in advance, incorporate insurance costs into their financial projections, and ensure compliance with legal and regulatory requirements.

Recognizing prepaid insurance as an asset on the balance sheet allows individuals and businesses to assess their financial position accurately, make informed decisions, and effectively manage their insurance needs. It provides stakeholders with transparency, reliability, and a clear understanding of the entity’s financial health and stability.

In conclusion, prepaid insurance is not just a contract for protection, but an asset with economic value and future benefits. It represents a prudent approach to risk management, financial stability, and responsible financial planning. By understanding the importance and implications of prepaid insurance as an asset, individuals and businesses can navigate the complex world of insurance with confidence.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance