Finance

What Is A Good Balance Sheet

Modified: February 21, 2024

Learn what a good balance sheet looks like in finance. Understand the key elements and ratios that contribute to a strong financial position.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

Introduction

A balance sheet is a fundamental financial statement that provides a snapshot of a company’s financial position at a specific point in time. It presents a summary of a company’s assets, liabilities, and equity, giving investors, lenders, and stakeholders insight into its financial health and stability.

Understanding a balance sheet is essential for evaluating a company’s financial performance and making informed decisions. By analyzing the components of a balance sheet, investors can assess a company’s ability to generate profits, manage debt, and maintain a sustainable business model.

In this article, we will dive into the key elements of a balance sheet and explore its significance for financial analysis. We will also discuss what constitutes a strong balance sheet and highlight warning signs of a weak one.

Whether you are an investor, a business owner, or simply curious about financial management, having an understanding of balance sheets is crucial for making sound financial decisions. So, let’s dive in and explore the world of balance sheets!

Definition of a Balance Sheet

A balance sheet is a financial statement that provides a snapshot of a company’s financial position at a specific point in time. It is sometimes referred to as a statement of financial position. The balance sheet follows the basic accounting equation: Assets = Liabilities + Equity.

This equation represents the underlying concept of a balance sheet, which states that a company’s assets must be financed by either debt (liabilities) or the company’s own funds (equity).

The balance sheet is divided into three main sections: assets, liabilities, and equity. Each section represents a different aspect of the company’s financial position.

The assets section of a balance sheet includes all of the company’s resources that have economic value. This includes tangible assets like cash, inventory, and equipment, as well as intangible assets like patents and trademarks.

The liabilities section represents the company’s obligations or debts. This includes loans, accounts payable, and other financial obligations that the company needs to repay in the future.

The equity section represents the residual interest in the company’s assets after deducting liabilities. It includes the owner’s capital contributions, retained earnings, and other equity-related items. It essentially represents the net worth of the company.

By presenting these three sections side-by-side, a balance sheet provides a clear picture of the company’s financial position, showing how assets are financed (either through debt or equity) and indicating the level of financial risk and stability.

The balance sheet is typically prepared at the end of an accounting period, such as the end of a month, quarter, or year. It provides valuable information for both internal and external stakeholders, including investors, creditors, and management, helping them assess the company’s financial strength and performance.

Purpose of a Balance Sheet

A balance sheet serves several important purposes for businesses, investors, and other stakeholders. Let’s explore the main objectives and benefits of a balance sheet:

- Assessing Financial Health: The primary purpose of a balance sheet is to provide an overview of a company’s financial health and stability. It allows stakeholders to evaluate the company’s liquidity, solvency, and overall financial position.

- Evaluating Risk and Return: By examining the balance sheet, investors and creditors can assess the risk and potential return associated with investing or lending to a company. It helps them make informed decisions by providing insights into the company’s ability to meet its financial obligations and generate profits.

- Tracking Financial Performance: A balance sheet is a useful tool for tracking a company’s financial performance over time. By comparing balance sheets from different periods, stakeholders can identify trends, patterns, and changes in the company’s financial position, which can reveal valuable insights about the company’s growth, profitability, and financial management.

- Facilitating Decision-Making: Business owners and managers rely on balance sheets to make critical decisions about resource allocation, investment opportunities, and debt management. It helps them evaluate the impact of their decisions on the company’s financial position and make informed choices to maximize profitability and long-term sustainability.

- Providing Transparency and Accountability: A balance sheet promotes transparency and accountability by providing a clear and concise summary of a company’s financial position. It enables stakeholders, such as shareholders and regulatory bodies, to monitor the company’s financial activities and ensure compliance with financial reporting standards.

Overall, the purpose of a balance sheet is to provide a comprehensive overview of a company’s financial position, helping stakeholders assess its strength, evaluate risk, track performance, support decision-making, and promote transparency. It is a crucial financial statement that provides valuable insights into the financial health and stability of a company.

Key Components of a Balance Sheet

A balance sheet is divided into three main components: assets, liabilities, and equity. Each component represents a different aspect of a company’s financial position. Let’s take a closer look at these key components:

- Assets: Assets represent the resources owned or controlled by a company that have economic value. They can be classified into current assets and non-current assets. Current assets are those that are expected to be converted into cash within one year, such as cash and cash equivalents, accounts receivable, and inventory. Non-current assets, on the other hand, are assets that are expected to provide value to the company for more than one year, such as property, plant, and equipment, investments, and intangible assets.

- Liabilities: Liabilities represent the obligations or debts owed by a company to external parties. Like assets, liabilities can also be categorized into current liabilities and non-current liabilities. Current liabilities are those that are expected to be settled within one year, including accounts payable, short-term loans, and accrued expenses. Non-current liabilities are long-term obligations that are not due within one year, such as long-term debt and lease obligations.

- Equity: Equity represents the residual interest in the assets of a company after deducting its liabilities. It represents the ownership interest of shareholders in the company. Equity includes items such as common stock, retained earnings, and additional paid-in capital. Changes in equity can occur through capital contributions, net income from operations, dividends, and other comprehensive income.

Additional Considerations: It is important to note that balance sheets can vary depending on the type of organization. For example, a balance sheet for a non-profit organization may include a separate section for net assets, while a balance sheet for a sole proprietorship may include the owner’s capital contribution and drawings. Furthermore, balance sheet items are typically presented in descending order of liquidity, meaning that the most liquid assets or liabilities are listed first.

By presenting these key components side-by-side, a balance sheet provides stakeholders with a comprehensive view of a company’s financial position. It allows for a better understanding of the resources available to the company, its financial obligations, and the ownership interest of shareholders.

Assets

When analyzing a balance sheet, one of the key components to focus on is the assets section. Assets represent the resources owned or controlled by a company that have economic value. By understanding the different types of assets and their significance, stakeholders can gain insights into a company’s financial health and potential for generating future income.

Assets are typically classified into two categories: current assets and non-current assets.

- Current Assets: Current assets are those that are expected to be converted into cash within one year or the normal operating cycle of a business. Some common examples of current assets include:

- Cash and Cash Equivalents: This includes physical cash, bank account balances, and short-term investments that can be readily converted into cash.

- Accounts Receivable: This represents money owed to the company by customers or clients for goods or services provided on credit. It is considered an asset as it is expected to be converted into cash in the future.

- Inventory: Inventory refers to the goods or products held by a company for sale or in the process of being produced. It includes raw materials, work-in-progress, and finished goods.

- Prepaid Expenses: Prepaid expenses are costs paid in advance for goods or services that will be consumed within the next year, such as insurance premiums or rent.

- Non-Current Assets: Non-current assets, also known as long-term assets, are those that are not expected to be converted into cash within one year. Some examples of non-current assets include:

- Property, Plant, and Equipment: This category includes tangible assets such as land, buildings, vehicles, machinery, and equipment that are used in the production of goods or services.

- Investments: Investments can include long-term holdings in stocks, bonds, or other securities with the intention of earning a return on investment.

- Intangible Assets: Intangible assets are non-physical assets that have value, such as patents, trademarks, copyrights, and goodwill.

- Long-Term Investments: Long-term investments refer to investments in other companies or entities that are intended to be held for an extended period, typically more than one year.

Assets play a crucial role in assessing a company’s financial strength and liquidity. The composition and value of a company’s assets can provide insights into its ability to generate cash flows, meet short-term obligations, and invest in future growth opportunities. By analyzing the assets section of a balance sheet, stakeholders can make informed decisions about the financial viability and performance of a company.

Liabilities

When evaluating a company’s financial health, one important component to consider on a balance sheet is the liabilities section. Liabilities represent the financial obligations or debts that a company owes to external parties. Understanding the different types of liabilities can provide insights into a company’s liquidity, financial obligations, and potential risks.

Similar to assets, liabilities can be categorized into two main types: current liabilities and non-current liabilities.

- Current Liabilities: Current liabilities are financial obligations that are expected to be settled within one year or the normal operating cycle of a business. Common examples of current liabilities include:

- Accounts Payable: Accounts payable refers to the amounts owed by a company to its suppliers or vendors for goods or services received but not yet paid for.

- Short-Term Loans: Short-term loans represent borrowing arrangements with a repayment period of less than one year, such as lines of credit or commercial paper.

- Accrued Expenses: Accrued expenses are expenses that have been incurred but not yet paid. This can include employee salaries, utilities, and interest on outstanding debts.

- Income Tax Payable: Income tax payable represents the amount of income tax owed to the government for the current fiscal year.

- Non-Current Liabilities: Non-current liabilities, also known as long-term liabilities, are financial obligations that are not expected to be settled within one year. Examples of non-current liabilities include:

- Long-Term Debt: Long-term debt includes loans or bonds with a maturity date of more than one year. This can include mortgages, long-term bank loans, and corporate bonds.

- Deferred Income Taxes: Deferred income taxes arise when there are temporary differences between the accounting income and taxable income. It represents the amount of taxes that will be due in future periods.

- Lease Obligations: Lease obligations represent the long-term rental agreements for assets such as buildings, vehicles, or equipment.

- Pension Liabilities: Pension liabilities are financial obligations related to the company’s retirement or pension plans.

Liabilities reflect the financial obligations a company has to meet. Analyzing the liabilities section of a balance sheet helps stakeholders understand the company’s ability to meet its short-term and long-term obligations. It is vital for assessing a company’s financial stability, debt management, and overall risk profile. By evaluating the liabilities section alongside other financial metrics, stakeholders can make informed decisions about investing, lending, or transacting with a company.

Equity

The equity section of a balance sheet represents the residual interest in a company’s assets after deducting its liabilities. It represents the ownership interest of shareholders or owners in the company. Understanding the components of equity can provide insights into the company’s net worth, retained earnings, and the financial stake of shareholders.

Equity can be broken down into several key elements:

- Common Stock: Common stock represents the initial investment made by shareholders in exchange for ownership rights in the company. It represents the par value, or face value, of the shares issued.

- Retained Earnings: Retained earnings reflect the accumulated profits or losses that the company has retained rather than distributed to shareholders as dividends. It represents the portion of the earnings that has been reinvested back into the company.

- Additional Paid-In Capital: Additional paid-in capital, also known as capital surplus, represents the amount of capital contributed to the company by shareholders above the par value of the shares. It includes amounts received from the issuance of shares at a premium.

- Treasury Stock: Treasury stock represents shares of a company’s own stock that have been repurchased by the company. It is recorded as a reduction of equity and can be reissued or retired by the company.

- Accumulated Other Comprehensive Income: Accumulated other comprehensive income represents gains or losses that are not included in the calculation of net income, such as unrealized gains or losses on investments or foreign currency translation adjustments.

The equity section represents the funding provided by shareholders and the accumulated profits or losses of the company. It shows the net worth of the company after accounting for its liabilities. Positive equity indicates that the company’s assets exceed its liabilities, while negative equity indicates that liabilities exceed assets, which may be a cause for concern.

Equity is a vital component for evaluating a company’s financial position. It represents the stake and ownership interest of shareholders, and changes in equity can occur through capital contributions, net income, dividends, and other comprehensive income. Analyzing the equity section of a balance sheet helps stakeholders understand the financial health of the company and its ability to generate value for shareholders.

Importance of a Balanced Balance Sheet

A balanced balance sheet is a key indicator of a company’s financial stability and strength. It reflects the relationship between a company’s assets, liabilities, and equity, and portrays a clear picture of its financial health. A balanced balance sheet is crucial for several reasons:

- Assessing Financial Stability: A balanced balance sheet demonstrates that a company has a solid financial foundation. It indicates that a company’s assets are appropriately funded by its liabilities and equity, reducing the risk of insolvency and financial instability.

- Ensuring Liquidity: A balanced balance sheet ensures that a company has sufficient current assets to meet its short-term financial obligations. It shows that the company can readily convert its assets into cash if needed, providing reassurance to creditors and investors.

- Facilitating Borrowing: Lenders and creditors often review a company’s balance sheet to evaluate its creditworthiness. A balanced balance sheet creates a positive impression, making it easier for the company to access credit or negotiate favorable terms with lenders and creditors.

- Building Investor Confidence: Investors seek companies with stable financial positions and well-balanced balance sheets. A balanced balance sheet signals that the company is effectively managing its resources, generating consistent profits, and minimizing financial risks. Consequently, it attracts potential investors and builds investor confidence.

- Supporting Growth and Expansion: A balanced balance sheet provides a strong foundation for growth and expansion initiatives. It indicates that the company has the financial capacity to invest in new projects, acquire assets, or expand operations without jeopardizing its financial stability.

- Maintaining Compliance: Many regulatory bodies require companies to maintain a balanced balance sheet. Adhering to these financial standards ensures compliance, helps avoid penalties, and provides transparency to regulatory authorities.

A balanced balance sheet serves as a vital tool for decision-making, risk management, and stakeholder communication. It provides a comprehensive snapshot of a company’s financial position, allowing investors, lenders, and stakeholders to make informed choices about investing, lending, and partnering with the company. By maintaining a balanced balance sheet, a company can enhance its financial credibility and pave the way for long-term success.

Analyzing a Balance Sheet

Analyzing a balance sheet is a critical step in understanding a company’s financial health and performance. It involves assessing the relationships between different components and identifying key metrics to evaluate the company’s liquidity, solvency, and profitability. Here are some important factors to consider when analyzing a balance sheet:

- Liquidity Ratios: Liquidity ratios assess a company’s ability to meet its short-term financial obligations. Common liquidity ratios include the current ratio (current assets divided by current liabilities) and the quick ratio (current assets minus inventory divided by current liabilities). These ratios help determine whether a company has enough liquid assets to cover its immediate liabilities.

- Solvency Ratios: Solvency ratios measure a company’s long-term financial stability and ability to meet its long-term obligations. Examples of solvency ratios include the debt-to-equity ratio (total debt divided by total equity) and the interest coverage ratio (earnings before interest and taxes divided by interest expenses). These ratios provide insights into a company’s debt and leverage levels.

- Profitability Ratios: Profitability ratios evaluate a company’s ability to generate profits and maximize returns. Key profitability ratios include the gross profit margin (gross profit divided by net sales) and the return on equity (net income divided by total equity). These ratios help assess the company’s efficiency in generating profits and managing costs.

- Asset Turnover Ratios: Asset turnover ratios measure the efficiency of a company’s asset utilization. Examples include the inventory turnover ratio (cost of goods sold divided by average inventory) and the accounts receivable turnover ratio (net credit sales divided by average accounts receivable). These ratios indicate how well a company is utilizing its assets to generate sales.

- Financial Trends: Analyzing balance sheets over multiple reporting periods allows for tracking financial trends and identifying patterns. Comparing key balance sheet items, such as total assets, total liabilities, and equity, can provide insights into a company’s growth, financial stability, and capital structure changes.

When analyzing a balance sheet, it is crucial to consider the industry context and benchmark against competitors or sector averages. Additionally, understanding the company’s business model, market conditions, and strategic initiatives can provide valuable insights into the interpretation of balance sheet figures.

By conducting a comprehensive analysis of a balance sheet, investors, lenders, and stakeholders can gain a deeper understanding of a company’s financial position, profitability, and risk profile. This information facilitates informed decision-making and assists in evaluating the company’s overall financial performance.

Common Elements of a Strong Balance Sheet

A strong balance sheet is indicative of a company’s financial stability, resilience, and ability to weather economic uncertainties. It reflects a healthy financial position, highlighting the following common elements:

- Adequate Liquidity: A strong balance sheet demonstrates sufficient liquidity through a healthy proportion of current assets to current liabilities. This indicates that the company has enough liquid assets to cover its short-term financial obligations.

- Low Debt Levels: Maintaining a manageable level of debt is crucial for a strong balance sheet. It is characterized by a reasonable debt-to-equity ratio, indicating that the company is not overly reliant on borrowed funds and has the ability to meet its financial obligations.

- Positive Equity: Equity is a measure of a company’s net worth. A strong balance sheet exhibits positive equity, indicating that the company’s assets exceed its liabilities. This represents a strong financial base for the company.

- Healthy Profitability: A strong balance sheet is supported by consistent profitability. It is characterized by a strong gross profit margin, indicating effective cost management and pricing strategies. Moreover, sustainable net income demonstrates the company’s ability to generate profits over time.

- Diversified Asset Base: A well-diversified asset base is another characteristic of a strong balance sheet. It signifies that the company has a range of assets spread across different categories, reducing the risk associated with relying heavily on a single asset type.

- Conservative Approach to Risk: Mitigating risk is paramount for a strong balance sheet. Companies with strong balance sheets often exercise prudence in their investment and financing decisions, avoiding excessive risk-taking and maintaining a conservative financial approach.

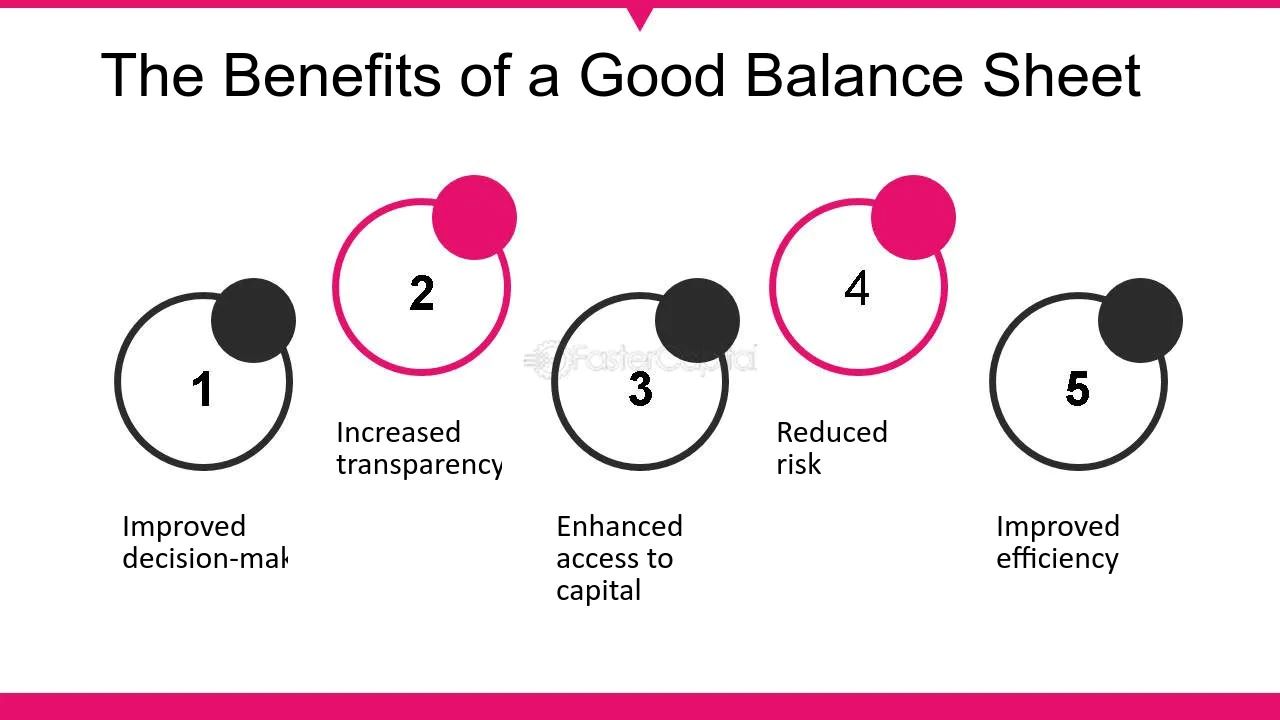

A strong balance sheet provides several benefits, including increased investor and lender confidence, improved access to capital, and enhanced resilience during economic downturns. It indicates the company’s financial strength and capacity to sustain and grow its operations.

It’s important to note that what constitutes a strong balance sheet may vary depending on the industry and the company’s lifecycle stage. Comparing the balance sheet to industry benchmarks and evaluating historical trends can provide a better understanding of the company’s financial health.

By fostering the common elements of a strong balance sheet, companies can position themselves for long-term success, build stakeholder trust, and effectively navigate the dynamic business environment.

Warning Signs of a Weak Balance Sheet

A weak balance sheet can indicate financial instability and potential risks for a company. It is important to be aware of certain warning signs that may suggest a weak balance sheet. These indicators can help stakeholders identify areas of concern and make informed decisions. Here are some warning signs to watch out for:

- High Debt Levels: Excessive debt can strain a company’s financial position. A weak balance sheet often exhibits a high debt-to-equity ratio, indicating that the company has a significant amount of debt in relation to its equity. This can increase financial risk and reduce the company’s ability to meet its obligations.

- Limited Liquidity: Insufficient liquidity can hinder a company’s ability to cover short-term obligations. Warning signs of weak liquidity include a low current ratio or quick ratio, suggesting that the company may struggle to convert its assets into cash quickly enough to meet its immediate financial needs.

- Negative Equity: Negative equity occurs when a company’s liabilities exceed its assets. This is an alarming sign, indicating that the company has accumulated losses or faced financial challenges. Negative equity erodes shareholder value and raises concerns about the company’s long-term viability.

- Declining Profitability: A weak balance sheet may be accompanied by declining profitability. This can be observed through decreasing gross profit margins, declining net income, or consistent losses over multiple reporting periods. Falling profitability can indicate challenges in maintaining sustainable revenue streams or managing costs effectively.

- Stagnant or Declining Asset Quality: An unhealthy balance sheet may include assets that are deteriorating in value or generating insufficient returns. This can be evident through the presence of obsolete inventory, impaired long-term assets, or a high proportion of non-performing loans in the case of financial institutions.

- Inadequate Capitalization: Weak capitalization refers to a lack of sufficient capital to support the company’s operations and growth. It can be indicated by a low equity-to-assets ratio or inadequate retained earnings. Insufficient capitalization may hinder the company’s ability to invest in new opportunities or weather financial setbacks.

Identifying these warning signs of a weak balance sheet is crucial for stakeholders such as investors, lenders, and suppliers. It helps them evaluate the financial risks associated with the company and make informed decisions about their level of involvement.

However, it is important to consider industry-specific factors, business cycles, and any strategic initiatives the company may be undertaking when assessing a balance sheet. Context is key in determining the significance of these warning signs and their potential impact on the overall financial health of the company.

By recognizing these warning signs and taking appropriate action, stakeholders can mitigate risks, protect their investments, and potentially avoid becoming entangled in financially unstable entities.

Conclusion

Understanding balance sheets and their significance is essential for assessing the financial health and stability of a company. By examining the components of a balance sheet, including assets, liabilities, and equity, stakeholders can gain valuable insights into a company’s liquidity, solvency, profitability, and overall financial position.

A balanced balance sheet, characterized by adequate liquidity, manageable debt levels, positive equity, healthy profitability, and diversified assets, signals a strong and stable financial foundation. It instills investor confidence, facilitates access to capital, and provides resilience during challenging economic times.

Conversely, warning signs of a weak balance sheet, such as high debt levels, limited liquidity, negative equity, declining profitability, poor asset quality, and inadequate capitalization, indicate potential financial risks and instability.

Analyzing and interpreting a balance sheet requires a holistic view, considering industry benchmarks, historical trends, and the company’s specific circumstances. This enables stakeholders to make informed decisions, assess risk, and understand the company’s ability to generate sustainable profits, meet financial obligations, and support future growth and expansion.

In conclusion, balance sheets are powerful financial tools that provide crucial insights into a company’s financial position. By leveraging the information presented in a balance sheet, stakeholders can make more informed decisions and effectively navigate the dynamic world of finance.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance