Home>Finance>How Are Credit Unions Different From Banks Apex

Finance

How Are Credit Unions Different From Banks Apex

Modified: February 21, 2024

Discover the key differences between credit unions and banks in Apex. Understand the unique financial advantages offered by credit unions in the finance industry.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

Introduction

When it comes to managing our finances, we often turn to traditional institutions like banks. However, there is another option that not many people are aware of: credit unions. While both banks and credit unions offer financial services, there are several key differences between the two. Understanding these differences can help you make informed decisions about where to keep your money and access financial services.

So, what exactly is a credit union? In simple terms, a credit union is a member-owned, not-for-profit financial cooperative. It is formed by a group of individuals who come together to pool their resources and provide financial services to the members. On the other hand, banks are for-profit institutions that are owned by shareholders or investors.

Although both credit unions and banks offer similar financial services, such as checking and savings accounts, loans, and credit cards, there are distinct differences in terms of ownership, membership, purpose, governance, and overall operations.

In this article, we will explore these differences in detail to help you better understand how credit unions set themselves apart from traditional banks. Whether you are looking for a better banking experience or considering joining a credit union, this article will provide you with valuable insights to make an informed decision.

Ownership Structure

One of the primary differences between credit unions and banks lies in their ownership structure. Banks are typically owned by shareholders or investors who expect to make a profit from their investments. These shareholders have the final say in the decision-making process and are primarily focused on maximizing profits.

On the other hand, credit unions operate under a different model. Credit unions are owned and controlled by their members. When you become a member of a credit union, you become a partial owner and have a say in the decisions made by the credit union. This cooperative ownership structure means that credit unions are primarily focused on serving the best interests of their members rather than generating profits for investors.

This ownership structure gives credit unions the flexibility to offer better interest rates on loans and higher yields on savings accounts compared to traditional banks. Since credit unions don’t have external shareholders to answer to, they can prioritize the needs of their members and pass on the benefits in the form of lower fees, reduced loan rates, and higher interest on deposits.

Furthermore, credit unions often operate on a not-for-profit basis, which means that any surplus generated is reinvested back into the credit union or returned to the members in the form of dividends or improved services. This structure ensures that the financial well-being of the members remains at the forefront of the credit union’s priorities.

Overall, the ownership structure of credit unions sets them apart from banks by putting the power in the hands of the members, fostering a sense of community and cooperation, and ultimately driving a focus on member satisfaction rather than maximizing profits.

Membership

Membership is another key distinction between credit unions and banks. Banks typically have open membership, meaning that anyone can open an account or become a customer by meeting the bank’s requirements and fulfilling the necessary documentation.

On the other hand, credit unions have a more restricted membership policy. To become a member of a credit union, you typically need to meet certain eligibility criteria. This can include factors such as your occupation, geographic location, or affiliation with a specific organization, such as a company, association, or community group. Credit unions often prioritize serving specific communities or groups of individuals.

The membership eligibility requirements vary from one credit union to another, but the aim is to create a sense of common bond among the members and foster a cooperative community. By having a more targeted membership base, credit unions can better understand and cater to the unique financial needs and goals of their members.

Membership in a credit union often comes with certain perks and benefits. Since credit unions are member-focused, they strive to provide personalized and attentive service to their members. This can include lower interest rates on loans, higher interest rates on savings accounts, and fewer fees compared to traditional banks.

Joining a credit union also grants you the opportunity to have a voice in the decision-making process. As a member, you typically have the right to vote for the credit union’s board of directors and participate in annual meetings to discuss important matters that affect the credit union and its members.

It’s important to note that although credit unions have membership requirements, they are often more inclusive than they may seem. Many credit unions have expanded their eligibility criteria to include a wider range of individuals, ensuring that more people can benefit from the advantages of joining a credit union.

In summary, credit unions have a more restricted membership policy compared to banks. By maintaining a focused membership base, credit unions can provide personalized service and better cater to the unique needs of their members.

Purpose

The purpose of credit unions and banks also differs significantly. While both institutions provide financial services, their underlying goals and missions vary.

When it comes to banks, their primary purpose is to generate profits for their shareholders or investors. This profit-driven approach often influences the decision-making process in banks, as they prioritize maximizing returns and expanding their market share.

On the other hand, credit unions are driven by a different purpose. The goal of a credit union is to provide financial services that meet the specific needs of their members and promote their financial well-being. As member-owned cooperatives, credit unions strive to provide accessible and affordable financial services to their members.

With their not-for-profit structure, credit unions can prioritize the needs of their members over profit. This means that credit unions often offer more competitive interest rates on loans, lower fees, and higher interest rates on savings accounts compared to traditional banks.

Additionally, credit unions often have a strong focus on financial education and empowerment. They aim to help their members improve their financial literacy, make informed financial decisions, and achieve their financial goals. Credit unions may offer workshops, seminars, and resources to enhance the financial knowledge and skills of their members.

Furthermore, credit unions are also committed to reinvesting any surplus funds back into the organization or returning them to the members in the form of dividends or improved services. This helps ensure that the financial benefits of the credit union are shared among its members.

In essence, credit unions exist to serve the financial needs of their members and promote their financial well-being, while banks primarily focus on generating profits for their shareholders. The purpose-driven approach of credit unions enables them to provide more personalized, member-centric services and prioritize the long-term financial success of their members.

Governance

The governance structure of credit unions and banks is another aspect that sets them apart. While both institutions have a board of directors responsible for overseeing the organization, their governing principles and decision-making processes differ.

In a bank, the board of directors is usually made up of individuals who may or may not have a direct connection to the institution’s customers or stakeholders. The board’s primary focus is to maximize profits for the shareholders and ensure the long-term success of the bank.

On the contrary, credit unions operate under a democratic governance model. The board of directors is typically composed of unpaid volunteers who are elected by the credit union’s members. These directors are themselves members of the credit union and are responsible for representing the interests of the membership.

The democratic governance structure of credit unions ensures that decision-making is driven by the needs and priorities of the members. Each member typically holds one vote, regardless of the size of their account. This means that every member has an equal say in electing the board of directors and influencing important decisions, such as setting interest rates, approving policies, and adopting strategic initiatives.

This member-centric governance structure allows credit unions to maintain a strong connection to the communities they serve and tailor their operations and services to best meet the needs of their membership.

Furthermore, credit unions often have supervisory committees or audit committees to monitor the financial health and compliance of the credit union. These committees are accountable to the members and ensure that the credit union operates in a transparent and responsible manner.

Overall, the democratic governance structure of credit unions empowers their members to have a voice in the decision-making process, ensuring that the institution operates in their best interest and aligns with their values and goals.

Profit Distribution

One of the fundamental differences between credit unions and banks is how they distribute their profits. As not-for-profit financial cooperatives, credit unions have a unique approach to profit distribution compared to traditional banks.

In a bank, the profits generated by the institution are typically distributed among the shareholders or investors in the form of dividends. The goal is to maximize returns for those who have invested in the bank.

On the other hand, credit unions operate under the principle of “people helping people.” Instead of distributing profits to external shareholders, credit unions channel their surplus funds back into the organization or return them to the members themselves.

Profit distribution in credit unions is often done in the following ways:

- Dividends: Credit unions may distribute a portion of their surplus funds to the members in the form of dividends. These dividends are often paid out annually and are based on factors such as the member’s account activity, loan utilization, or savings balance.

- Reduced Fees and Better Rates: Credit unions strive to provide their members with more favorable terms on loans and savings accounts. They often offer lower interest rates on loans, higher interest rates on savings accounts, and lower fees compared to traditional banks, effectively passing on the financial benefits directly to the members.

- Investments in Services: Credit unions may also reinvest their surplus funds back into the organization to enhance the services and products offered to their members. This can include improving technology infrastructure, expanding branch networks, or introducing new services that better meet the evolving needs of the membership.

Additionally, credit unions may also allocate funds for community development initiatives or support social causes that align with their mission and values. This demonstrates their commitment to giving back to the communities they serve.

The profit distribution approach of credit unions reflects their member-centered philosophy and their dedication to improving the financial well-being of their members and the communities in which they operate.

Services and Products

When it comes to the range of services and products offered, both credit unions and banks provide similar financial offerings, such as checking accounts, savings accounts, loans, and credit cards. However, there can be differences in the specifics and the overall approach to providing these services.

While banks often have a wider geographic presence and a larger branch network, credit unions may have a more localized presence, serving specific communities or groups of individuals.

One key advantage of credit unions is their focus on providing personalized, member-centric services. Since credit unions are owned by their members, they are more likely to go the extra mile to meet the individual needs of their members. They often have a customer service approach that prioritizes building long-lasting relationships and understanding the financial goals and challenges of each member.

Credit unions also place a strong emphasis on financial education and empowerment. They may offer resources, workshops, or one-on-one guidance to help their members improve their financial literacy, make informed financial decisions, and achieve their goals. This dedication to financial education sets credit unions apart and helps members build a stronger financial foundation.

Furthermore, credit unions may offer competitive interest rates on loans and higher interest rates on savings accounts compared to traditional banks. This can provide members with cost savings on borrowing and the opportunity to grow their savings more effectively.

In terms of technology and digital services, while banks have traditionally been at the forefront of innovation, many credit unions are catching up and investing in digital platforms to provide online banking, mobile banking, and remote access to their services.

It is worth noting that credit unions also often collaborate with other credit unions or participate in shared branching networks, allowing members to access their accounts and conduct transactions at various locations across the country. This provides a level of convenience and accessibility comparable to what traditional banks offer.

In summary, while credit unions and banks offer similar financial services and products, credit unions often stand out for their personalized service, focus on financial education, competitive rates, and commitment to meeting the unique needs of their members and communities.

Access to Funds

Access to funds is an essential aspect of banking, and both credit unions and banks provide various ways for their customers or members to access their money. However, there may be differences in the availability and convenience of accessing funds between the two.

Banks generally have a wider network of ATMs and branches, making it more convenient for customers to access their funds. They often have ATMs located in various locations, allowing customers to withdraw cash, deposit checks, and perform other transactions easily. Banks also offer online and mobile banking services, providing customers with 24/7 access to their accounts and the ability to transfer funds, pay bills, and make other financial transactions from the comfort of their own homes.

Credit unions, on the other hand, may have a more limited branch and ATM network, particularly if they are community-based or serve specific groups of individuals. However, credit unions have adopted various strategies to ensure their members have access to funds.

Many credit unions participate in shared branching networks, which allow members to access their accounts and conduct transactions at other credit union branches across the country. This expands the availability of branch services beyond the credit union’s own physical locations, providing members with additional options for accessing their funds.

Credit unions may also partner with specific ATM networks to offer surcharge-free access to ATMs for their members. This means that even if a credit union does not have an extensive ATM network of its own, its members can still access their funds without incurring additional fees at partner ATMs.

In terms of digital banking, credit unions have been steadily increasing their online and mobile banking services. This allows members to check account balances, transfer funds, pay bills, and even deposit checks remotely. While the level of technological sophistication and convenience may vary among credit unions, many are investing in digital infrastructure to provide their members with seamless access to their funds.

Overall, while banks may have a larger network of physical branches and ATMs, credit unions are finding innovative ways to ensure their members have access to funds, whether through shared branching networks, partnerships with ATM networks, or expanding their digital banking capabilities.

Regulation

Both credit unions and banks operate within a regulatory framework to ensure the safety and soundness of the financial system and protect the interests of consumers. However, the regulatory oversight for credit unions differs from that of traditional banks.

Banks are primarily regulated by federal banking agencies, such as the Office of the Comptroller of the Currency (OCC), the Federal Reserve, and the Federal Deposit Insurance Corporation (FDIC). These agencies enforce regulations and monitor the activities of banks to ensure compliance with laws, maintain financial stability, and protect the deposits of customers.

Credit unions, on the other hand, are regulated by the National Credit Union Administration (NCUA) in the United States. The NCUA is an independent federal agency responsible for overseeing and regulating federal credit unions. Additionally, state-chartered credit unions may also come under the regulatory oversight of state banking authorities.

The NCUA and state regulators enforce regulations to ensure the safety and soundness of credit unions, protect the rights of credit union members, and safeguard their deposits. These regulations cover areas such as capital requirements, lending practices, membership eligibility, governance, and disclosures.

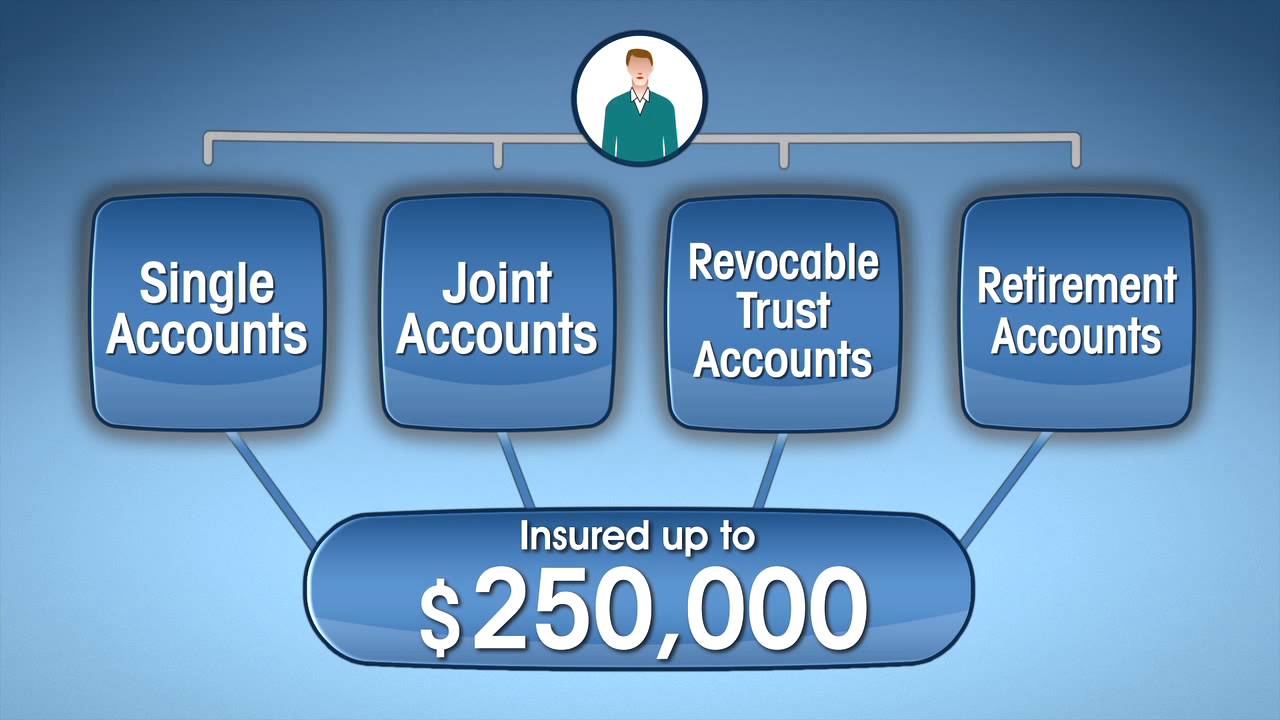

One notable difference in regulation is deposit insurance coverage. While banks are typically insured by the FDIC, which provides deposit insurance coverage up to $250,000 per depositor, credit unions have a similar program called the National Credit Union Share Insurance Fund (NCUSIF). The NCUSIF provides deposit insurance coverage up to $250,000 per share owner, offering the same level of protection to credit union members as the FDIC does to bank customers.

It’s important to note that the regulatory framework for both credit unions and banks aims to ensure the safety, stability, and fair treatment of customers or members. Both types of institutions must comply with applicable laws, maintain financial integrity, and adhere to consumer protection guidelines.

By adhering to regulations and maintaining strong regulatory oversight, both credit unions and banks work to instill confidence in consumers and provide a secure and reliable financial system.

Insurance Coverage

Insurance coverage is a critical aspect to consider when choosing a financial institution, as it provides protection for your deposits against potential risks. Both banks and credit unions offer insurance coverage, although the specific programs and coverage limits may vary.

Banks in the United States are typically insured by the Federal Deposit Insurance Corporation (FDIC). The FDIC provides deposit insurance coverage up to $250,000 per depositor, per ownership category, in case of bank failure or insolvency. This means that if a bank fails, the FDIC will reimburse depositors up to the coverage limit for their eligible deposits.

Credit unions, on the other hand, are backed by the National Credit Union Administration (NCUA) through the National Credit Union Share Insurance Fund (NCUSIF). Similar to the FDIC, the NCUSIF provides deposit insurance coverage to credit union members. The coverage limit is also $250,000 per share owner, per ownership category. This means that if a credit union were to experience financial difficulties, the NCUSIF would step in to protect the members’ deposits up to the coverage limit.

It’s important to understand that both the FDIC and the NCUSIF are federal agencies that strive to maintain the stability and confidence of the banking system. The insurance coverage they provide helps ensure that your deposits are protected, giving you peace of mind as a consumer.

When considering insurance coverage for your deposits, it’s crucial to note that both banks and credit unions may offer additional coverage limits by structuring accounts in different ownership categories. For example, joint accounts, retirement accounts, and trust accounts may have separate coverage limits, effectively providing higher insurance coverage for individuals who have deposits in different categories.

It’s always a good practice to review your account ownership and insurance coverage limits to ensure that your deposits are fully protected. If you have concerns about the insurance coverage offered by a specific financial institution, you can verify their insurance status with the FDIC or the NCUA.

Overall, both banks and credit unions provide deposit insurance coverage to protect your funds. Understanding the coverage limits and verifying the insurance status of the institution can help you make an informed decision when choosing where to deposit your money.

Conclusion

In conclusion, credit unions and banks may offer similar financial services, but there are notable differences between the two. Credit unions differentiate themselves through their ownership structure, membership requirements, purpose, governance, profit distribution, services and products, access to funds, regulation, and insurance coverage.

Credit unions operate as member-owned, not-for-profit financial cooperatives, prioritizing the needs of their members rather than generating profits for external shareholders. Their cooperative nature fosters a sense of community and cooperation among members. Banks, on the other hand, are for-profit institutions owned by shareholders or investors.

Membership in a credit union typically requires meeting certain eligibility criteria, promoting a targeted membership base and a strong sense of common bond among members. Credit unions focus on providing personalized services, competitive rates, and dividends or reinvesting surplus funds back into the organization for the benefit of the members.

Governance in credit unions follows a democratic model, with board members elected by the members, ensuring that important decisions are made with the members’ best interests in mind. Banks are typically directed by individuals who may or may not have a direct connection to the customers.

Credit unions and banks also differ in terms of profit distribution, with credit unions prioritizing returning profits to members through dividends, reduced fees, and better rates. Banks distribute profits to shareholders or investors in the form of dividends.

Credit unions offer services and products similar to banks, but their member-centric approach often leads to more personalized attention and a focus on financial education. Although banks may have a wider physical network and more extensive digital services, credit unions can provide access to funds through shared branching networks and partnerships.

In terms of regulation, credit unions are overseen by the NCUA or state regulators, while banks are regulated by federal agencies such as the FDIC. Both institutions operate within a regulatory framework to ensure financial stability and consumer protection.

Lastly, both credit unions and banks offer deposit insurance coverage, with the FDIC providing coverage for bank deposits and the NCUSIF for credit union deposits, up to $250,000 per depositor, per ownership category.

Ultimately, the choice between a credit union and a bank depends on individual preferences and needs. Credit unions can offer a more personalized and community-oriented banking experience, while banks may provide broader access to services. Evaluating factors such as ownership structure, membership eligibility, purpose, services, and regulatory protections can help you make an informed decision that aligns with your financial goals and values.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance