Finance

How Credit Work

Modified: March 4, 2024

Learn how credit works and its impact on your financial situation. Discover key insights and tips to manage your finances effectively.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

Introduction

When it comes to managing our finances, one important aspect that often comes into play is credit. Whether you’re applying for a loan, renting an apartment, or even getting a new credit card, understanding how credit works is crucial.

Credit refers to the ability to borrow money or access goods and services with the promise of repayment at a later date. It plays a significant role in our financial lives and can impact our ability to make purchases, secure favorable interest rates, and even influence our overall financial well-being.

In this article, we will dive deep into the world of credit, exploring what it is, the different types of credit available, how it works, and the factors that can affect our creditworthiness. Additionally, we will discuss strategies for building and improving credit, using credit responsibly, and explore the advantages and disadvantages of credit.

By the end of this article, you’ll have a comprehensive understanding of credit and be better equipped to make informed financial decisions.

What is Credit?

Credit is a financial tool that allows individuals and businesses to borrow money or purchase goods and services with the promise of repayment in the future. It is essentially a form of trust extended by a lender to a borrower, based on the borrower’s ability to repay the borrowed amount or fulfill their financial obligations.

When you utilize credit, you are essentially borrowing money from a lender, such as a bank or a credit card company, with the understanding that you will repay the borrowed amount over time, usually with interest. This borrowed amount is typically referred to as the principal.

There are various forms of credit available, including loans, credit cards, lines of credit, and even store credit. Each type of credit may have different terms, such as interest rates, repayment schedules, and credit limits, but they all work on the same basic principle.

One key element of credit is the concept of a credit agreement or contract. This agreement outlines the terms and conditions of the credit arrangement, including the loan amount, interest rate, repayment period, and any additional fees or charges that may be applicable.

It is important to note that credit is not inherently good or bad. It is simply a financial tool that can be used wisely or mismanaged. When used responsibly, credit can provide individuals and businesses with the ability to make purchases, invest in assets, and even weather unexpected financial emergencies. However, if not managed properly, credit can lead to debt, high interest payments, and financial stress.

Understanding credit is essential for effectively managing your finances and making informed decisions. By grasping the basics of credit, you can navigate the world of borrowing and lending with confidence, ensuring that you are utilizing credit to your advantage and minimizing any potential risks.

Types of Credit

Credit comes in various forms, each tailored to specific financial needs and circumstances. Understanding the different types of credit available can help you make informed decisions when borrowing money or accessing goods and services.

1. Loans: Loans are a common form of credit where a borrower receives a sum of money from a lender and agrees to repay it over a set period of time, usually with interest. Examples of loans include mortgages, student loans, car loans, and personal loans.

2. Credit Cards: Credit cards provide a line of credit that allows you to make purchases up to a certain limit. You are required to make monthly minimum payments, and any unpaid balance will accrue interest. Credit cards offer convenience and can help build your credit history.

3. Lines of Credit: A line of credit is similar to a credit card but typically comes with a higher credit limit. It allows you to access funds on an as-needed basis, and interest is charged only on the amount borrowed. Lines of credit are commonly used for business purposes or as a safety net for unexpected expenses.

4. Store Credit: Many retailers offer store credit, allowing customers to make purchases on credit directly through the store. Store credit often comes with special promotions or discounts but may have higher interest rates compared to traditional credit cards.

5. Secured Credit: Secured credit requires collateral to secure the loan. This collateral, such as a house or a car, serves as a guarantee for the lender in case the borrower defaults on the loan. Secured credit typically offers lower interest rates due to the reduced risk for the lender.

6. Unsecured Credit: Unsecured credit does not require collateral and is based solely on the borrower’s creditworthiness. Credit cards and personal loans are examples of unsecured credit. Since there is no collateral involved, the interest rates may be higher compared to secured credit.

It is important to carefully assess your financial needs and evaluate the terms and conditions before choosing the type of credit that best suits your situation. Each type of credit has its own advantages and should be used responsibly to avoid excessive debt and financial strain.

Credit Scores and Reports

Credit scores and reports play a crucial role in the credit landscape. They provide lenders and creditors with information about an individual’s creditworthiness and help determine the terms and conditions of credit offers. Understanding how credit scores and reports work is essential for managing your credit effectively.

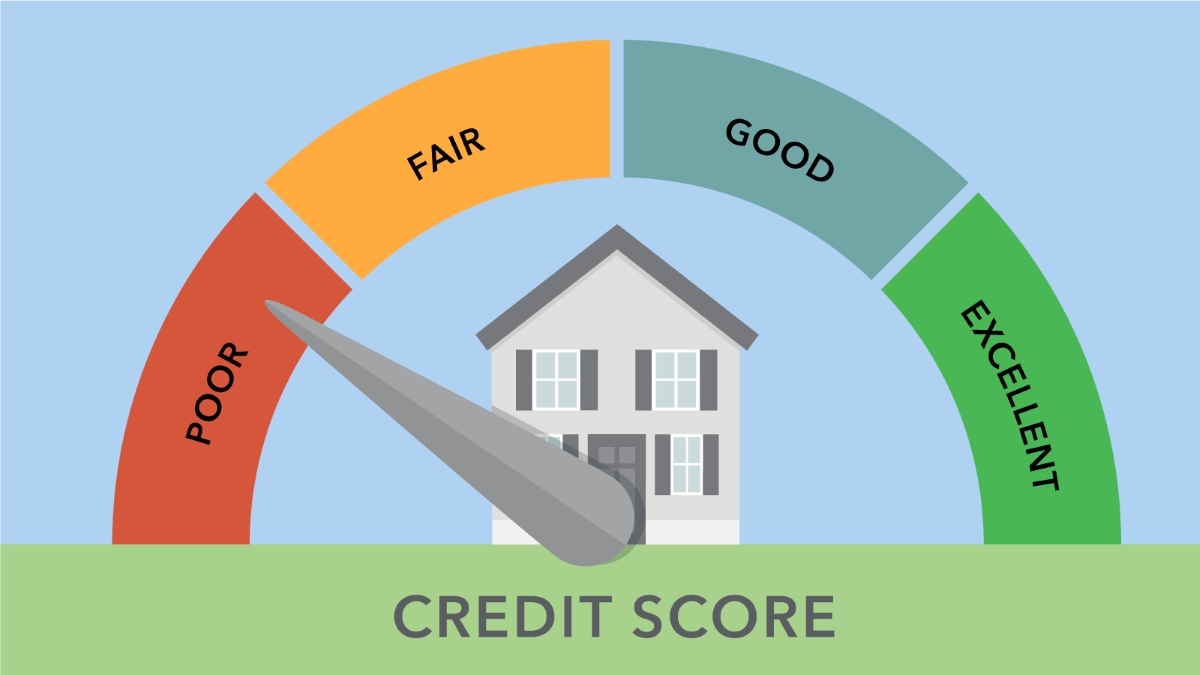

Credit Scores: A credit score is a numerical value that represents an individual’s creditworthiness. It is calculated using a variety of factors, including payment history, credit utilization, length of credit history, types of credit used, and new credit applications. The most commonly used credit scoring model is the FICO score, ranging from 300 to 850. The higher the credit score, the better the individual’s creditworthiness and the more favorable the credit terms they may be offered.

Credit Reports: A credit report is a detailed record of an individual’s credit history. It includes information about the individual’s personal details, credit accounts, payment history, credit inquiries, and public records like bankruptcies or liens. Credit reports are maintained by credit reporting agencies, such as Equifax, Experian, and TransUnion. Consumers have the right to request a free copy of their credit report from each of these agencies once a year.

Importance of Credit Scores and Reports: Credit scores and reports are important because they provide a snapshot of your creditworthiness. Lenders and creditors use this information to determine the risk of lending you money or extending credit. A higher credit score indicates a lower risk, making it easier to qualify for loans and credit cards with favorable terms. Additionally, credit scores can affect other aspects of your financial life, such as insurance premiums and rental applications.

Monitoring and Improving Credit: It is crucial to regularly monitor your credit reports for any errors or fraudulent activity. Discrepancies can negatively impact your credit score, so it is important to address them promptly. To improve your credit score, focus on making timely payments, reducing credit card balances, and avoiding excessive new credit applications. Over time, responsible credit behavior can lead to an improved credit score and better access to credit.

Knowing your credit score and understanding the information on your credit report allows you to make better financial decisions. By maintaining a good credit score, you can enjoy the benefits of favorable credit terms, lower interest rates, and increased financial opportunities.

How Credit Works

Credit works by allowing individuals and businesses to borrow money or access goods and services with the promise of repayment in the future. Here is a breakdown of how credit works:

Borrower and Lender: In a credit transaction, there are two primary parties involved – the borrower and the lender. The borrower is the individual or business that seeks to access credit, while the lender is the entity that provides the credit.

Credit Application: To access credit, the borrower usually needs to complete a credit application, providing personal and financial information. The lender evaluates this information to assess the borrower’s creditworthiness and determine if they are eligible for credit.

Approval and Terms: If approved, the lender sets the terms of the credit agreement, outlining the loan amount, interest rate, repayment period, and any other applicable fees or charges. The terms may vary depending on the type of credit and the borrower’s credit history.

Drawdown or Credit Utilization: Once the credit is approved, the borrower can access the funds or make purchases up to the approved credit limit. This is known as the drawdown or credit utilization. For example, if someone has a credit card with a $5,000 limit, they can make purchases or withdraw cash up to that amount.

Repayment: The borrower is responsible for repaying the borrowed amount plus any interest or fees according to the terms agreed upon. Repayment can be made in installments over a specified period. Missed or late payments can negatively affect the borrower’s credit history and may incur additional fees or penalties.

Interest and Fees: Lenders charge interest as a fee for allowing the borrower to use their funds. The interest rate can be fixed or variable and is typically expressed as an annual percentage. Credit agreements may also include other fees, such as annual fees, late payment fees, or balance transfer fees.

Credit Reporting: Credit activities, such as loan repayment history and credit card utilization, are reported to credit bureaus. These credit bureaus compile the information into a credit report, which influences the borrower’s credit score. Maintaining a positive payment history and low credit utilization can help improve your credit score.

Credit Limits and Available Credit: Credit accounts have limits, indicating the maximum amount of credit available to the borrower. As the borrower repays the borrowed amount, the available credit increases. It’s important to manage credit responsibly and avoid reaching or exceeding the credit limit.

Understanding how credit works is essential for making informed borrowing decisions and maintaining a healthy credit profile. By responsibly utilizing credit and making timely repayments, borrowers can establish a positive credit history and access credit when needed.

Factors that Affect Credit

Several factors play a significant role in determining an individual’s creditworthiness and can impact their credit score. Here are the key factors that affect credit:

Payment History: Your payment history has the most substantial influence on your credit score. Lenders assess whether you make your payments on time and in full. Late or missed payments can have a negative impact on your credit score.

Credit Utilization: Credit utilization refers to the percentage of your available credit that you are using. Keeping your credit utilization low is important for a good credit score. High utilization suggests a higher dependency on credit and can be perceived as a risk by creditors.

Length of Credit History: The length of your credit history is another crucial factor. Having a longer credit history can demonstrate your ability to manage credit responsibly over time. It allows lenders to assess your creditworthiness based on a more extended period of financial behavior.

Types of Credit: The types of credit accounts you have, such as credit cards, loans, or mortgages, can impact your credit score. A healthy mix of credit accounts can positively influence your credit, showing that you can handle different types of credit responsibly.

New Credit Applications: When you apply for new credit, it results in a credit inquiry on your report. Multiple recent credit inquiries can indicate an increased credit risk, potentially lowering your credit score. It’s important to be selective and avoid unnecessary credit applications.

Public Records: Public records, such as bankruptcies, judgments, or liens, can significantly impact your credit score. These records indicate financial difficulties or potential legal issues, which can raise concerns for lenders.

Credit Mix: Having a diverse credit mix, including revolving accounts like credit cards and installment accounts like loans, can positively impact your credit score. It demonstrates your ability to manage different types of credit responsibly.

Credit History: Your overall credit history takes into account the length of your credit accounts, the average age of your credit, and the time since your most recent activity. A longer, positive credit history indicates a more stable financial track record, positively influencing your credit score.

It’s important to note that the significance of these factors may vary based on individual circumstances and the credit scoring model used. By understanding these factors, you can take proactive steps to build and maintain a good credit score, enabling you to access credit on favorable terms.

Building and Improving Credit

Building and improving credit is essential for achieving financial goals and securing favorable credit terms. Here are some strategies to help you build and improve your credit:

1. Establish Credit: If you have no credit history, start by opening a credit account, such as a secured credit card or a credit-builder loan. These accounts are designed to help individuals build credit by making regular, on-time payments and demonstrating responsible credit behavior.

2. Make Timely Payments: Paying your bills and credit obligations on time is crucial. Late payments can have a negative impact on your credit score. Set up payment reminders or automatic payments to ensure you never miss a payment.

3. Keep Credit Utilization Low: Aim to keep your credit utilization ratio below 30%. This means using no more than 30% of your available credit. High credit utilization can signal excessive reliance on credit and impact your credit score. Consider increasing your credit limit or paying down balances to lower your utilization ratio.

4. Manage Debt Responsibly: If you have existing debt, develop a plan to pay it down. Focus on high-interest debt first while making at least minimum payments on other accounts. Consistently reducing debt demonstrates responsible financial management.

5. Maintain a Healthy Credit Mix: Having a mix of different types of credit, such as credit cards, loans, and a mortgage, can positively impact your credit score. However, only take on new credit when necessary and ensure you can manage the payments.

6. Regularly Check Your Credit Report: Review your credit report annually and check for any errors or discrepancies. Dispute any inaccuracies to ensure your credit history is represented correctly, as this can affect your credit score.

7. Limit New Credit Applications: Be cautious about applying for too much new credit within a short period. Multiple credit inquiries can raise concerns for lenders and lower your credit score. Only apply for credit when necessary and consider pre-qualifying first.

8. Stay Informed: Stay up to date with changes in your credit score, credit report, and overall financial situation. Monitor your credit regularly, utilize credit monitoring tools, and seek professional guidance if needed.

Building and improving credit takes time and consistent effort. By following these strategies and practicing responsible credit management, you can establish a positive credit history, improve your credit score, and unlock better credit opportunities in the future.

Using Credit Responsibly

Using credit responsibly is crucial to maintaining a healthy financial life and avoiding excessive debt. Here are some key practices to help you use credit responsibly:

1. Stick to a Budget: Create a budget and track your expenses to ensure you can comfortably afford your credit obligations. Only use credit for purchases within your budget and avoid overspending.

2. Pay in Full and On Time: Aim to pay your credit card balances in full each month to avoid accruing interest charges. If that’s not possible, at least make the minimum payment by the due date to avoid late payment fees and negative impacts on your credit score.

3. Avoid Maximum Credit Utilization: Keep your credit utilization ratio below 30% of your available credit. Maxing out your credit cards can negatively impact your credit score and make it harder to manage debt.

4. Be Selective with Credit Applications: Think carefully before applying for new credit. Each credit application can result in a hard inquiry on your credit report, which can temporarily lower your credit score. Only apply for credit when you truly need it and have the means to manage it.

5. Read and Understand the Terms: Before signing any credit agreement, thoroughly read and understand the terms and conditions, including interest rates, fees, and any penalties. This allows you to make informed decisions and avoid any surprises down the line.

6. Regularly Review Your Statements: Monitor your credit card and loan statements regularly to ensure all charges are accurate. Report any discrepancies or suspicious activity to the issuer or lender immediately.

7. Avoid Taking on Unmanageable Debt: Be mindful of your overall debt load and avoid taking on more debt than you can comfortably repay. Excessive debt can lead to financial stress and negatively impact your credit score.

8. Use Credit-Building Tools: If you have a limited credit history, consider using credit-building tools such as secured credit cards or credit-builder loans. These tools can help establish a positive credit history when used responsibly.

9. Regularly Monitor Your Credit: Keep an eye on your credit score and credit report. Many financial institutions and credit reporting agencies provide free credit monitoring tools that can help you stay informed about changes in your credit status.

By following these practices, you can use credit responsibly, maintain a good credit score, and build a solid financial foundation. Responsible credit usage not only provides you with financial flexibility but also opens doors to better credit opportunities and financial well-being.

Advantages and Disadvantages of Credit

Credit can be a valuable financial tool, providing numerous advantages to individuals and businesses. However, it is important to be aware of the disadvantages and potential pitfalls that come with credit. Here are the key advantages and disadvantages of credit:

Advantages:

- Financial Flexibility: Credit allows you to make large purchases or investments that you may not have enough cash on hand for. It provides the flexibility to spread out payments over time.

- Building Credit History: Using credit responsibly and making timely payments helps build a positive credit history, making it easier to qualify for future loans and credit at better terms.

- Emergency Preparedness: Credit can serve as a safety net during unexpected financial emergencies when immediate funds are required.

- Convenience: Credit cards and other forms of credit offer convenience and ease of payment, especially for online and in-person transactions.

- Rewards and Benefits: Many credit cards offer rewards programs, cashback, or travel benefits, allowing you to earn rewards for your spending.

Disadvantages:

- Accumulating Debt: One of the major pitfalls of credit is the potential to accumulate debt. If credit is not managed responsibly, it can lead to excessive debt, high-interest charges, and financial stress.

- Interest and Fees: Credit comes with interest charges and fees, such as annual fees, late payment fees, or balance transfer fees. These costs can add up over time, increasing the overall expense of using credit.

- Potential Overspending: Credit cards and other forms of credit may tempt individuals to spend beyond their means, leading to financial strain and difficulty in repaying debt.

- Impact on Credit Score: Mismanaged credit can have a negative impact on your credit score. Late payments, high credit utilization, and defaults can lower your credit score, making it harder to access credit in the future.

- Dependency on Credit: Overreliance on credit can lead to a dangerous cycle of debt. It is important to strike a balance and use credit responsibly, being mindful of your financial obligations.

Understanding the advantages and disadvantages of credit allows you to make informed decisions and use credit as a helpful financial tool while minimizing potential risks. Using credit responsibly, managing debt, and making timely payments can help you maximize the benefits and avoid the negative consequences of credit.

Conclusion

Credit is a powerful financial tool that can provide individuals and businesses with opportunities for growth, flexibility, and financial security. Understanding how credit works and using it responsibly is essential for navigating the complex world of personal finance.

Throughout this article, we have explored the various aspects of credit, including what it is, the types of credit available, the influence of credit scores and reports, and the factors that affect creditworthiness. We have also discussed strategies for building and improving credit, using credit responsibly, and touched upon the advantages and disadvantages of credit.

Remember, credit is not inherently good or bad. It all depends on how it is managed and utilized. When used responsibly, credit can help achieve financial goals, provide convenience, and create opportunities. However, it is crucial to avoid overextending oneself and falling into the trap of excessive debt or missing payments.

To use credit wisely, always make payments on time, keep credit utilization low, and be selective with new credit applications. Regularly monitor your credit reports and scores, and take proactive steps to correct any errors or discrepancies. Consider seeking professional advice if you need help managing your credit or improving your financial situation.

By understanding the ins and outs of credit, you can make informed decisions and maintain a healthy financial profile. Use credit as a tool to enhance your financial well-being, secure favorable terms, and achieve your short-term and long-term goals.

Remember, building and maintaining good credit takes time and consistent effort. With responsible credit usage, you can pave the way to a brighter financial future and enjoy the benefits that credit can bring.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance