Finance

How Often Does A FICO Score Update

Published: March 6, 2024

Learn how often your FICO score updates and stay informed about your financial health. Understand the frequency of FICO score updates and manage your finances effectively. Discover more about finance and credit scores.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

Introduction

Understanding the dynamics of credit scoring is pivotal in managing one's financial well-being. A key player in this realm is the FICO score, a numerical representation of an individual's creditworthiness. This score holds significant sway in various financial transactions, influencing loan approvals, interest rates, and even job opportunities. Given its impact, it's crucial to comprehend the factors that govern its updates and the frequency with which these updates occur.

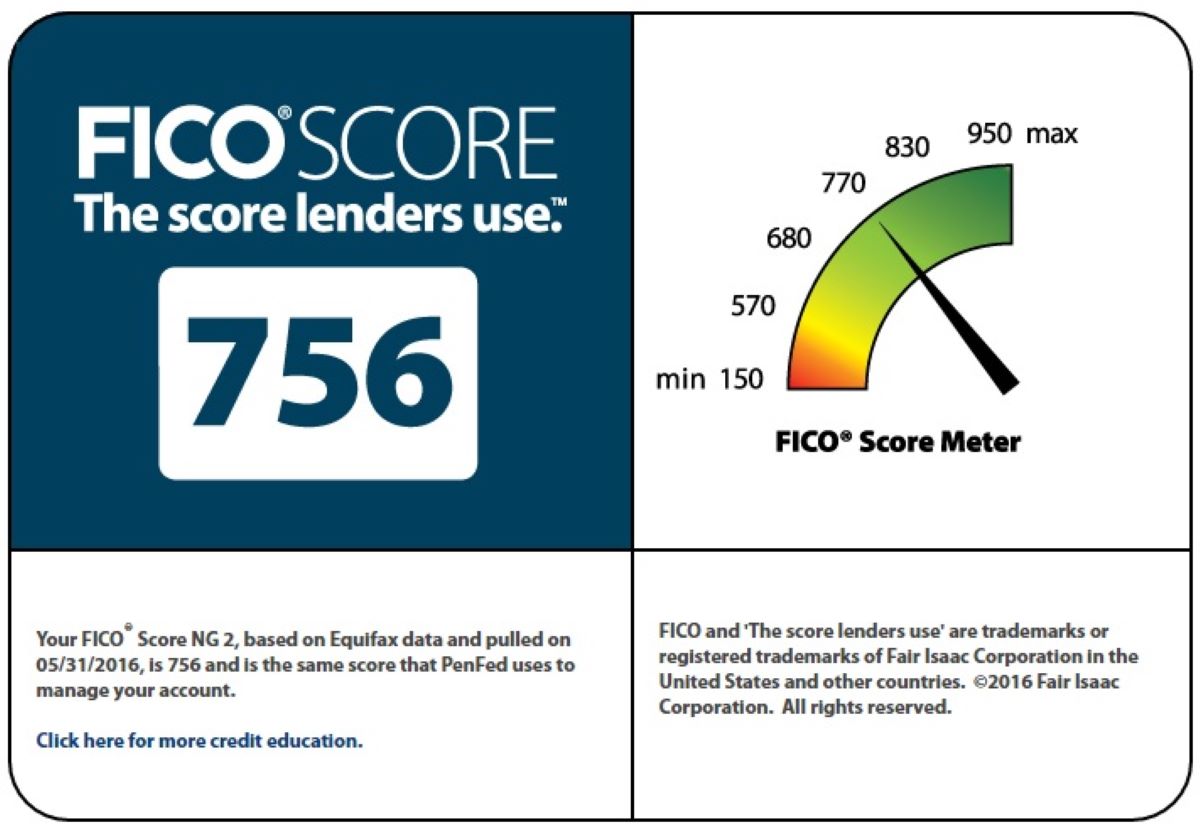

The FICO score serves as a barometer of an individual's credit risk, providing lenders with insights into the likelihood of timely repayment. This three-digit score, ranging from 300 to 850, is derived from information within credit reports, encompassing factors such as payment history, credit utilization, length of credit history, new credit accounts, and the mix of credit types. As such, it encapsulates a comprehensive overview of an individual's credit management habits.

Given its significance, it's natural to wonder about the frequency of FICO score updates. Understanding this aspect can help individuals make informed decisions regarding credit-related activities and financial planning. Therefore, delving into the intricacies of FICO score updates is essential for anyone keen on mastering their financial journey.

What is a FICO Score?

A FICO score, developed by the Fair Isaac Corporation, is a widely used credit scoring model that assesses an individual’s credit risk based on their credit history. This three-digit number, ranging from 300 to 850, plays a pivotal role in determining an individual’s creditworthiness and their ability to access various financial products and services.

The FICO score is calculated based on several factors, each carrying a different weight in the overall score:

- Payment History: This accounts for the largest portion of the FICO score and reflects a borrower’s track record of making on-time payments for credit accounts.

- Credit Utilization: This factor considers the amount of credit being used in relation to the total available credit, with lower utilization generally viewed more favorably.

- Length of Credit History: The length of time credit accounts have been open and the time since the most recent account activity are taken into account.

- New Credit Accounts: Opening multiple new credit accounts within a short period can negatively impact the FICO score, as it may indicate financial distress.

- Credit Mix: Having a diverse mix of credit accounts, such as credit cards, retail accounts, and installment loans, can positively influence the FICO score.

Understanding the components that contribute to the FICO score is essential for individuals looking to improve their creditworthiness. By focusing on these factors, individuals can take proactive steps to enhance their credit profile and, in turn, secure better financial opportunities.

Why Does a FICO Score Update?

A FICO score undergoes updates to reflect the most current information in an individual’s credit report. As individuals engage in financial activities, such as making credit card payments, taking out loans, or applying for new credit accounts, these actions are reported to the credit bureaus. The credit bureaus then update the individual’s credit report with the new information, which subsequently triggers an update to the FICO score.

Furthermore, the regular updates to a FICO score are essential for providing lenders and financial institutions with an accurate assessment of an individual’s creditworthiness. By incorporating the latest credit-related activities, the FICO score ensures that lenders have access to up-to-date information when making lending decisions. This real-time reflection of a borrower’s credit behavior enables lenders to assess risk more accurately and offer appropriate terms and interest rates.

Moreover, frequent updates to the FICO score empower individuals to monitor and track their credit health effectively. By promptly reflecting changes in credit behavior, individuals can gauge the impact of their financial decisions and take corrective measures if necessary. This transparency fosters a sense of financial responsibility and allows individuals to make informed choices regarding credit management and borrowing activities.

Overall, the regular updates to a FICO score serve the dual purpose of providing lenders with current credit risk assessments and empowering individuals to stay informed about their credit standing. This ensures that the FICO score remains a reliable and dynamic indicator of an individual’s creditworthiness, adapting to their financial behaviors in real time.

How Often Does a FICO Score Update?

The frequency of FICO score updates largely depends on the activity reported to the credit bureaus. While there isn’t a specific timeline for when a FICO score updates, it typically occurs when new information is added to an individual’s credit report. This can happen as frequently as once a month, especially when creditors report updated account information to the credit bureaus.

For instance, credit card issuers generally report account information, including payment history and credit utilization, to the credit bureaus once a month. As a result, individuals may observe changes in their FICO scores shortly after their credit card issuers submit updated information. Similarly, loan repayments, new credit applications, and other credit-related activities prompt the credit bureaus to update an individual’s credit report, subsequently leading to a FICO score update.

It’s important to note that while the frequency of FICO score updates is tied to the reporting practices of creditors and the credit bureaus, individuals can actively monitor their credit reports to stay informed about any changes. By regularly reviewing their credit reports, individuals can keep track of the information that influences their FICO scores and identify any discrepancies or inaccuracies that may impact their credit standing.

Understanding the frequency of FICO score updates is crucial for individuals keen on maintaining a healthy credit profile. By staying informed about the factors that prompt score updates, individuals can proactively manage their credit behaviors and make strategic financial decisions to positively impact their FICO scores.

Factors That Impact FICO Score Updates

Several key factors influence the updates to a FICO score, reflecting the dynamic nature of an individual’s credit profile. Understanding these factors is essential for individuals seeking to comprehend the nuances of credit scoring and its impact on their financial well-being.

Credit Account Activity: The activity on credit accounts, such as making payments, opening new accounts, or closing existing ones, significantly impacts FICO score updates. Timely payments and responsible credit management can positively influence the score, while missed payments or excessive new credit applications may lead to score fluctuations.

Credit Utilization: The ratio of credit balances to credit limits, known as credit utilization, plays a pivotal role in FICO score updates. High credit utilization can negatively impact the score, while maintaining lower utilization levels can contribute to score improvements.

Credit Inquiries: When individuals apply for new credit, the resulting credit inquiries can impact FICO scores. Multiple credit inquiries within a short timeframe may signal higher risk to lenders, potentially leading to score reductions.

Credit Mix and Account Types: The diversity of credit accounts, including credit cards, mortgages, and installment loans, can influence FICO score updates. A well-managed mix of credit types may positively impact the score, reflecting responsible credit management.

Public Records and Collections: Events such as bankruptcies, foreclosures, and collections can significantly impact FICO scores upon being reported to the credit bureaus. These negative events may lead to substantial score reductions and can take time to recover from.

By understanding the factors that impact FICO score updates, individuals can make informed decisions regarding their credit behaviors and financial activities. Proactively managing these factors can lead to improvements in credit scores, opening doors to better financial opportunities and lending terms.

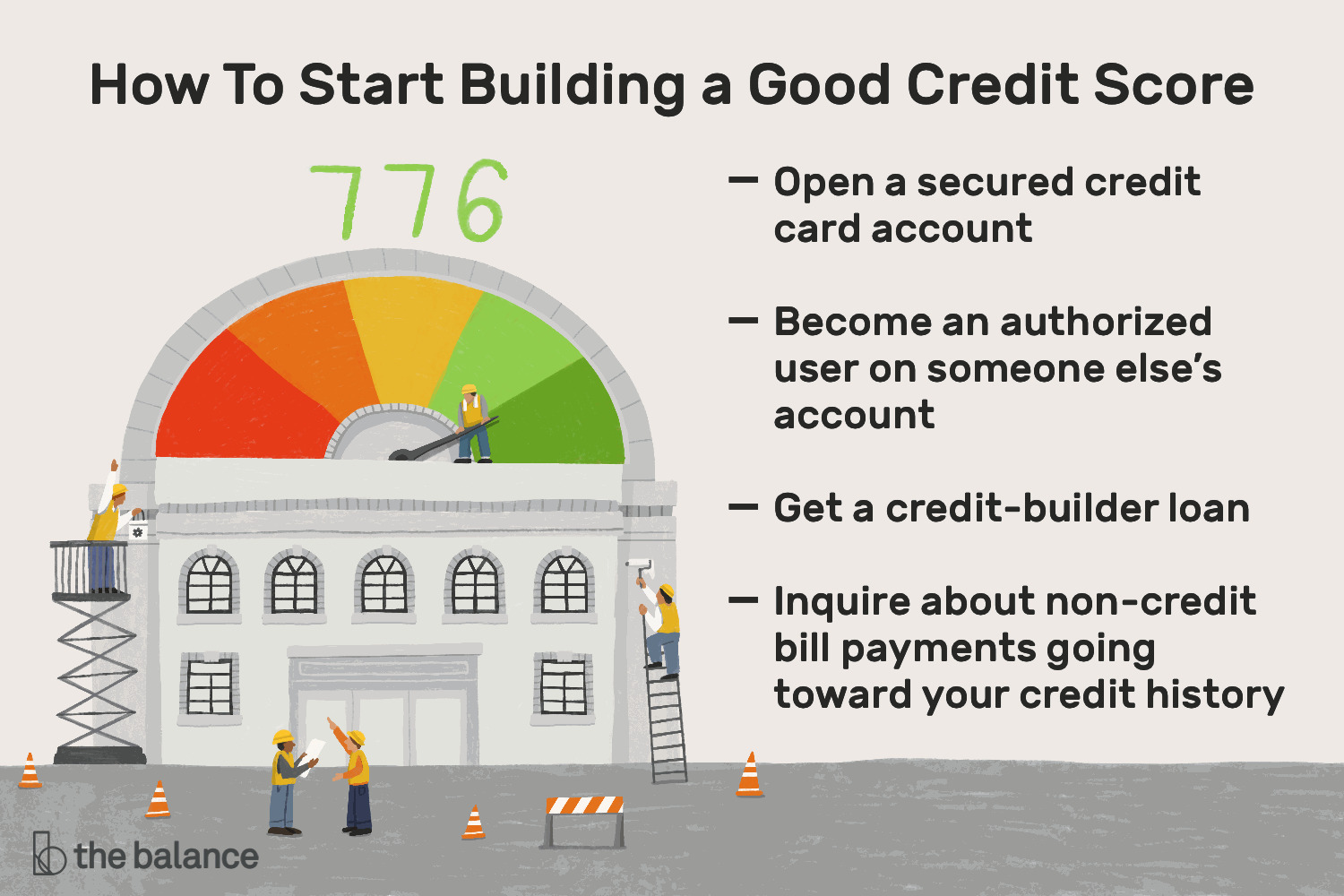

Importance of Regularly Monitoring Your FICO Score

Regular monitoring of your FICO score is a crucial aspect of maintaining a healthy financial standing and making informed credit-related decisions. By staying attuned to changes in your credit score, you gain valuable insights into your creditworthiness and can take proactive measures to improve or maintain your financial standing.

Early Detection of Errors: Regularly monitoring your FICO score allows you to swiftly identify any errors or inaccuracies in your credit report. By addressing these discrepancies promptly, you can prevent potential negative impacts on your credit standing and ensure that lenders receive accurate information about your creditworthiness.

Identifying Suspicious Activity: Monitoring your FICO score enables you to detect any unauthorized or fraudulent activity on your credit accounts. Spotting such activity early can help mitigate potential damage to your credit profile and prevent unauthorized accounts or transactions from affecting your financial health.

Tracking Credit Health Progress: By regularly checking your FICO score, you can track your credit health progress over time. Observing score fluctuations and understanding the factors driving these changes empowers you to make informed decisions about credit management and take steps to improve your creditworthiness.

Preparing for Financial Milestones: Whether you’re considering major financial milestones such as applying for a mortgage or seeking a new line of credit, monitoring your FICO score allows you to assess your readiness for these endeavors. It provides an opportunity to address any negative factors impacting your score and position yourself favorably for important financial undertakings.

Improving Financial Literacy: Regularly engaging with your FICO score fosters a deeper understanding of credit scoring and financial management. This enhanced financial literacy equips you with the knowledge to make sound financial decisions, manage credit responsibly, and navigate the complexities of the lending landscape.

Overall, the practice of regularly monitoring your FICO score is instrumental in safeguarding your financial well-being, identifying potential issues early, and proactively managing your credit health. By staying informed about your credit standing, you can take charge of your financial future and pursue opportunities with confidence.

Conclusion

Understanding the nuances of FICO score updates is paramount for individuals navigating the intricacies of credit management and financial planning. The FICO score serves as a dynamic indicator of an individual’s creditworthiness, reflecting their credit behaviors and financial decisions. By comprehending the factors that prompt FICO score updates and the frequency of these updates, individuals can gain valuable insights into their credit health and make informed choices regarding credit-related activities.

Regularly monitoring your FICO score is not only a proactive measure but also a fundamental aspect of maintaining a healthy financial profile. It empowers individuals to detect errors, identify suspicious activity, track their credit health progress, and prepare for significant financial milestones. Moreover, this practice contributes to the ongoing development of financial literacy, equipping individuals with the knowledge to navigate the credit landscape effectively.

As the financial landscape continues to evolve, the significance of the FICO score in lending decisions and financial opportunities remains steadfast. By staying attuned to changes in their FICO scores and understanding the factors that influence these changes, individuals can position themselves favorably for various financial endeavors and proactively manage their credit health.

In essence, the journey of mastering one’s financial well-being is intrinsically linked to the understanding and management of the FICO score. By embracing the role of the FICO score as a barometer of creditworthiness and actively engaging with its updates, individuals can navigate the complexities of credit management with confidence and foresight.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance